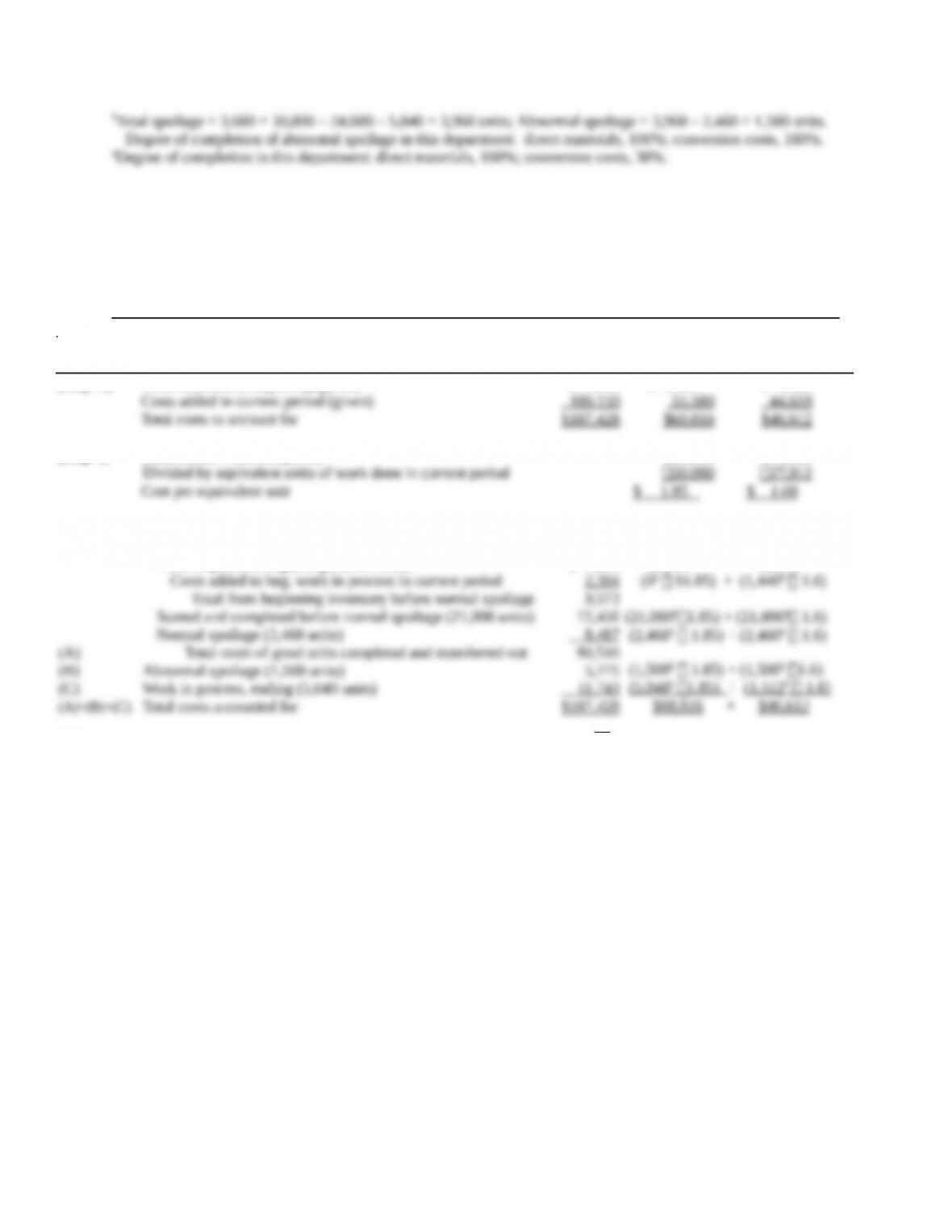

Costs before adding normal spoilage

Normal spoilage (2,460 units)

(A) Total costs of good units completed and

transferred out

(B) Abnormal spoilage (1,500 units)

(C) Work in process, ending (5,040 units)

(A)+(B)+(C) Total costs accounted for

$82,656

8,266

90,922

5,040

11,466

$107,428

(24,600# 1.81) +

(2,460# 1.81) +

(1,500# 1.81) +

(5,040# 1.81) +

$60,816 +

(24,600# 1.55)

(2,460# 1.55)

(1,500# 1.55)

(1,512# 1.55)

$46,612

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.

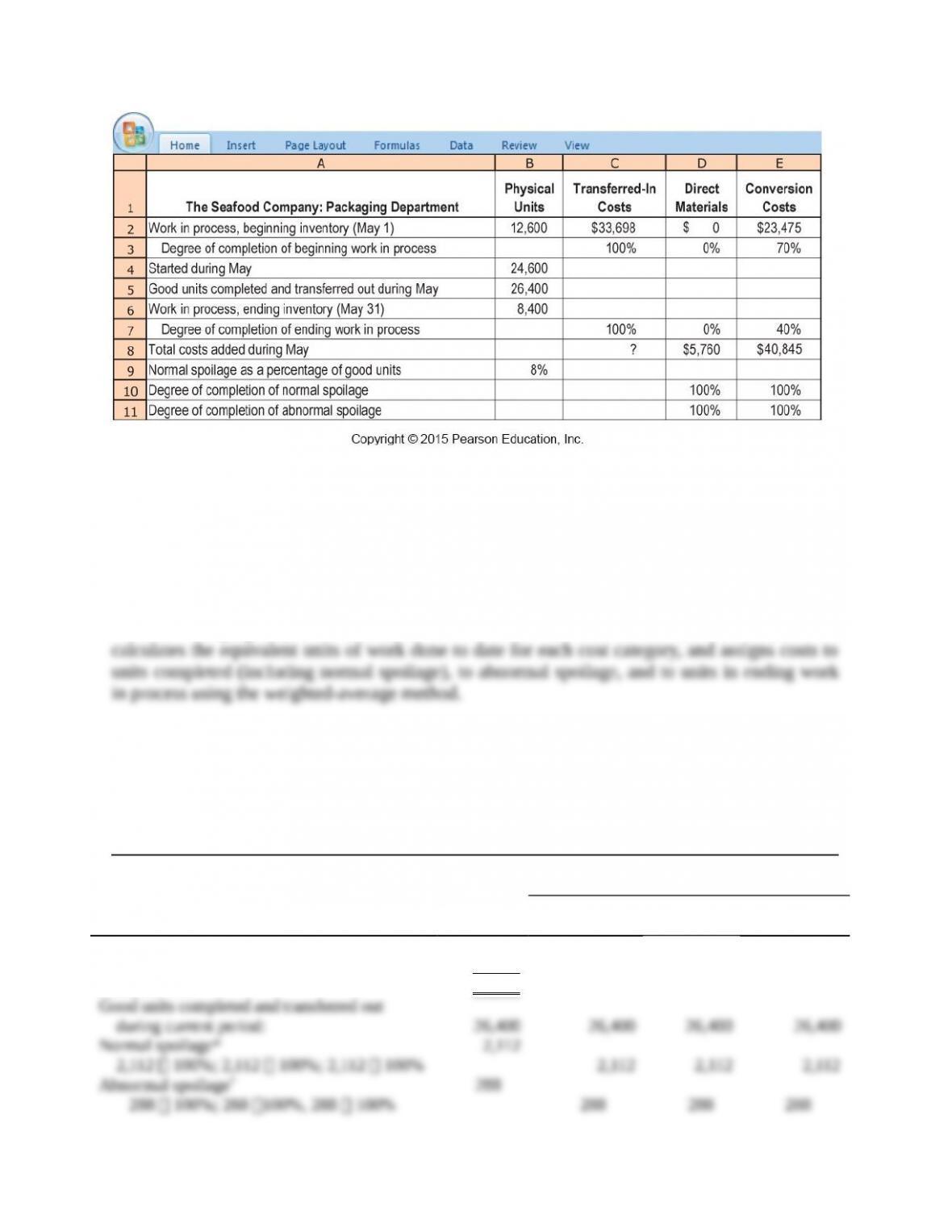

Work in process, ending‡ (given)

8,400 100%; 8,400 0%; 8,400 40%

Accounted for

Equivalent units of work done to date

8,400

37,200

8,400

37,200

0

______

28,800

3,360

_____

32,160

*Normal spoilage is 8% of good units transferred out: 8% 26,400 = 2,112 units. Degree of completion of normal spoilage in

this department: transferred-in costs, 100%; direct materials, 100%; conversion costs, 100%.

†Total spoilage =12,600 + 24,600 – 26,400 – 8,400 = 2,400 units. Abnormal spoilage = 2,400 – 2,112 = 288 units. Degree of

completion of abnormal spoilage in this department: transferred-in costs, 100%; direct materials, 100%; conversion costs,

100%.

‡Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 40%.

PANEL B: Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work–in-Process

Inventory

Total

Production

Costs

Transferred-in

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs incurred to date

Divided by equivalent units of work done to date

Cost per equivalent unit

(Step 5) Assignment of costs

Good units completed and transferred out

(26,400 units)

$ 51,338

143,362

$194,700

$ 33,698

90,922*

$124,620

124,620

37,200

$ 3.35

$ 0

5,760

$5,760

5,760

28,800

$ 0.20

$23,475

40,845

$64,320

64,320

32,160

$ 2.00

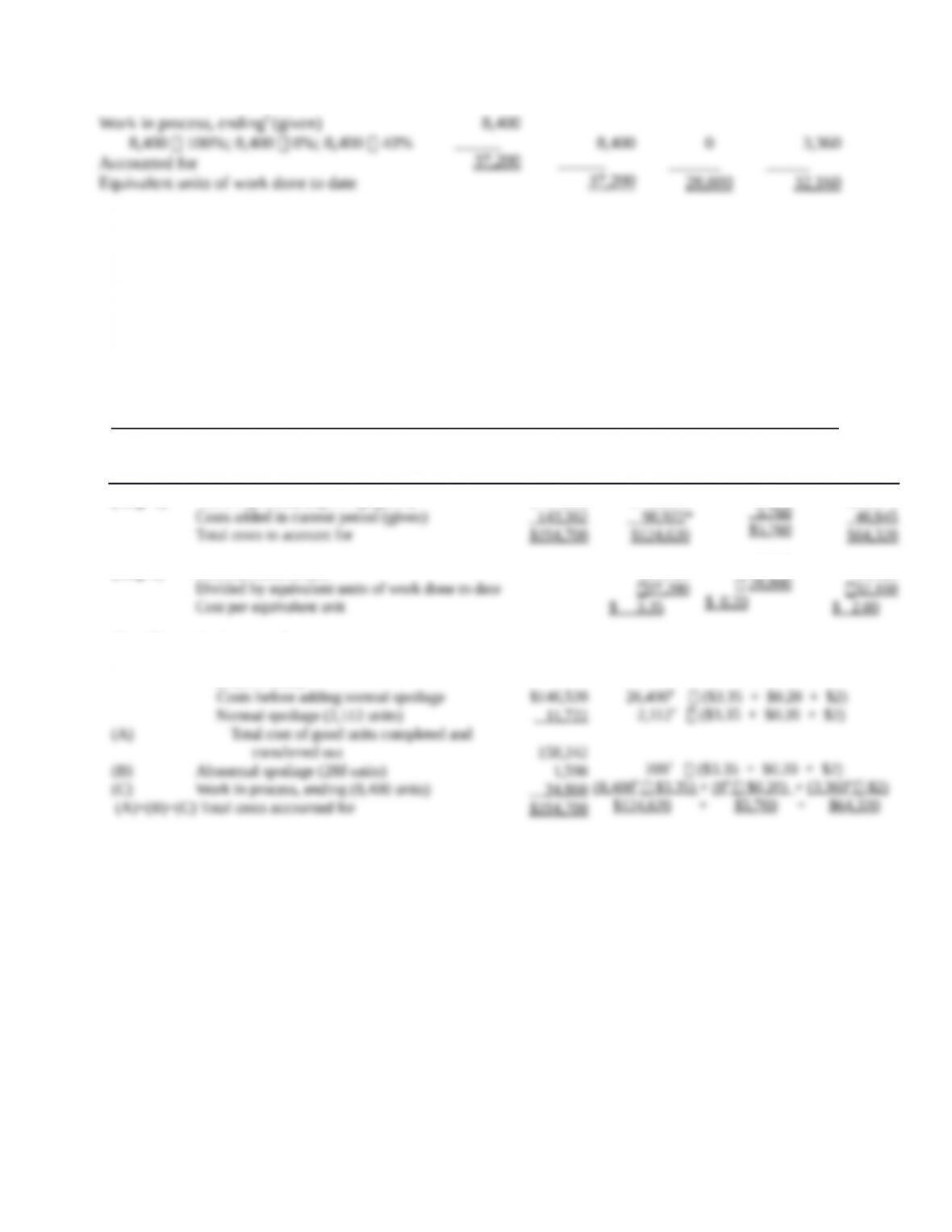

Costs before adding normal spoilage

Normal spoilage (2,112 units)

(A) Total cost of good units completed and

transferred out

(B) Abnormal spoilage (288 units)

(C) Work in process, ending (8,400 units)

(A)+(B)+(C) Total costs accounted for

$146,520

11,722

158,242

1,598

34,860

$194,700

26,400# ($3.35 + $0.20 + $2)

2,112# ($3.35 + $0.20 + $2)

288# ($3.35 + $0.20 + $2)

(8,400# $3.35) + (0# $0.20) + (3,360# $2)

$124,620 + $5,760 + $64,320

*Total costs of good units completed and transferred out in Panel B (Step 5) of Solution Exhibit 18-31.

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.

18-34 (25 min.) FIFO method, Packaging Department (continuation of 18-32).

Refer to the information in Problem 18-33 except that the transferred-in costs of beginning work

in process on May 1 are $33,090 (instead of $33,698). Transferred-in costs for May equal the total

cost of good units completed and transferred out in May from the cleaning department, as

calculated in Problem 18-32 using the FIFO method of process costing.

Required: