6-1

CHAPTER 6

MASTER BUDGET AND RESPONSIBILITY ACCOUNTING

6-1 The budgeting cycle includes the following elements:

a. Planning the performance of the company as a whole as well as planning the performance

of its subunits. Management agrees on what is expected.

b. Providing a frame of reference, a set of specific expectations against which actual results

can be compared.

c. Investigating variations from plans. If necessary, corrective action follows investigation.

d. Planning again, in light of feedback and changed conditions.

6-2 The master budget expresses management’s operating and financial plans for a specified

period (usually a fiscal year) and includes a set of budgeted financial statements. It is the initial

plan of what the company intends to accomplish in the period.

6-3 Strategy, plans, and budgets are interrelated and affect one another. Strategy specifies how

an organization matches its own capabilities with the opportunities in the marketplace to

accomplish its objectives. Strategic analysis underlies both long–run and short-run planning. In

turn, these plans lead to the formulation of budgets. Budgets provide feedback to managers about

the likely effects of their strategic plans. Managers use this feedback to revise their strategic plans.

.

6-4 We agree that budgeted performance is a better criterion than past performance for judging

managers because inefficiencies included in past results can be detected and eliminated in

budgeting. Also, future conditions may be expected to differ from the past, and these can also be

factored into budgets.

6-5 Production and marketing traditionally have operated as relatively independent business

functions. Budgets can assist in reducing conflicts between these two functions in two ways.

Consider a beverage company such as Coca-Cola or Pepsi-Cola:

• Communication. Marketing could share information about seasonal demand with

production.

• Coordination. Production could ensure that output is sufficient to meet, for example,

high seasonal demand in the summer.

6-6 In many organizations, budgets impel managers to plan. Without budgets, managers drift

from crisis to crisis. Research also shows that budgets can motivate managers to meet targets and

improve their performance. Thus, many top managers believe that budgets meet the cost–benefit

test.

6-7 A rolling budget, also called a continuous budget, is a budget or plan that is always

available for a specified future period, by continually adding a period (month, quarter, or year) to

the period that just ended. A four-quarter rolling budget for 2014 is superseded by a four–quarter

rolling budget for April 2014 to March 2015, and so on.

6-8 The steps in preparing an operating budget are as follows:

1. Prepare the revenues budget.

2. Prepare the production budget (in units).

3. Prepare the direct material usage budget and direct material purchases budget.

4. Prepare the direct manufacturing labor budget.

5. Prepare the manufacturing overhead budget.

6. Prepare the ending inventories budget.

7. Prepare the cost of goods sold budget.

8. Prepare the nonmanufacturing costs budget.

6-2

9. Prepare the budgeted income statement.

The steps in preparing an operating budget are as follows:

6-9 The sales forecast is typically the cornerstone for budgeting because production (and,

hence, costs) and inventory levels generally depend on the forecasted level of sales.

6-10 Sensitivity analysis adds an extra dimension to budgeting. It enables managers to examine

how budgeted amounts change with a change in the underlying assumptions. This assists managers

in monitoring those assumptions that are most critical to a company in attaining its budget and

allows them to make timely adjustments to plans when appropriate.

6-11 Kaizen budgeting explicitly incorporates continuous improvement anticipated during the

budget period into the budget numbers.

6-12 Nonoutput-based cost drivers can be incorporated into budgeting by the use of activity–

based budgeting (ABB). ABB focuses on the budgeted cost of activities necessary to produce and

sell products and services. Nonoutput-based cost drivers, such as the number of parts, number of

batches, and number of new products can be used with ABB.

6-13 The choice of the type of responsibility center determines what the manager is accountable

for and thereby affects the manager’s behavior. For example, if a revenue center is chosen, the

manager will focus on revenues, not on costs or investments. The choice of a responsibility center

type guides the variables to be included in the budgeting exercise.

6-14 Budgeting in multinational companies may involve budgeting in several different foreign

currencies. Further, management accountants must translate operating performance into a single

currency for reporting to shareholders by budgeting for exchange rates. Managers and accountants

must understand the factors that impact exchange rates and, where possible, plan financial

strategies to limit the downside of unexpected unfavorable moves in currency valuations. In

developing budgets for operations in different countries, they must also have good understanding

of political, legal, and economic issues in those countries.

6-15 No. Cash budgets and operating income budgets must be prepared simultaneously. In

preparing their operating income budgets, companies want to avoid unnecessary idle cash and

unexpected cash deficiencies. The cash budget, unlike the operating income budget, highlights

periods of idle cash and periods of cash shortage, and it allows the accountant to plan cost effective

ways of either using excess cash or raising cash from outside to achieve the company’s operating

income goals.

6-16 (15 min.) Sales budget, service setting.

In 2014, Rouse & Sons, a small environmental-testing firm, performed 12,200 radon tests for $290

each and 16,400 lead tests for $240 each. Because newer homes are being built with lead–free

pipes, lead-testing volume is expected to decrease by 10% next year. However, awareness of

radon-related health hazards is expected to result in a 6% increase in radon-test volume each year

in the near future. Jim Rouse feels that if he lowers his price for lead testing to $230 per test, he

will have to face only a 7% decline in lead–test sales in 2015.

Required:

1. Prepare a 2015 sales budget for Rouse & Sons assuming that Rouse holds prices at 2014 levels.

2. Prepare a 2015 sales budget for Rouse & Sons assuming that Rouse lowers the price of a lead

test to $230. Should Rouse lower the price of a lead test in 2015 if the company’s goal is to

maximize sales revenue?

SOLUTION

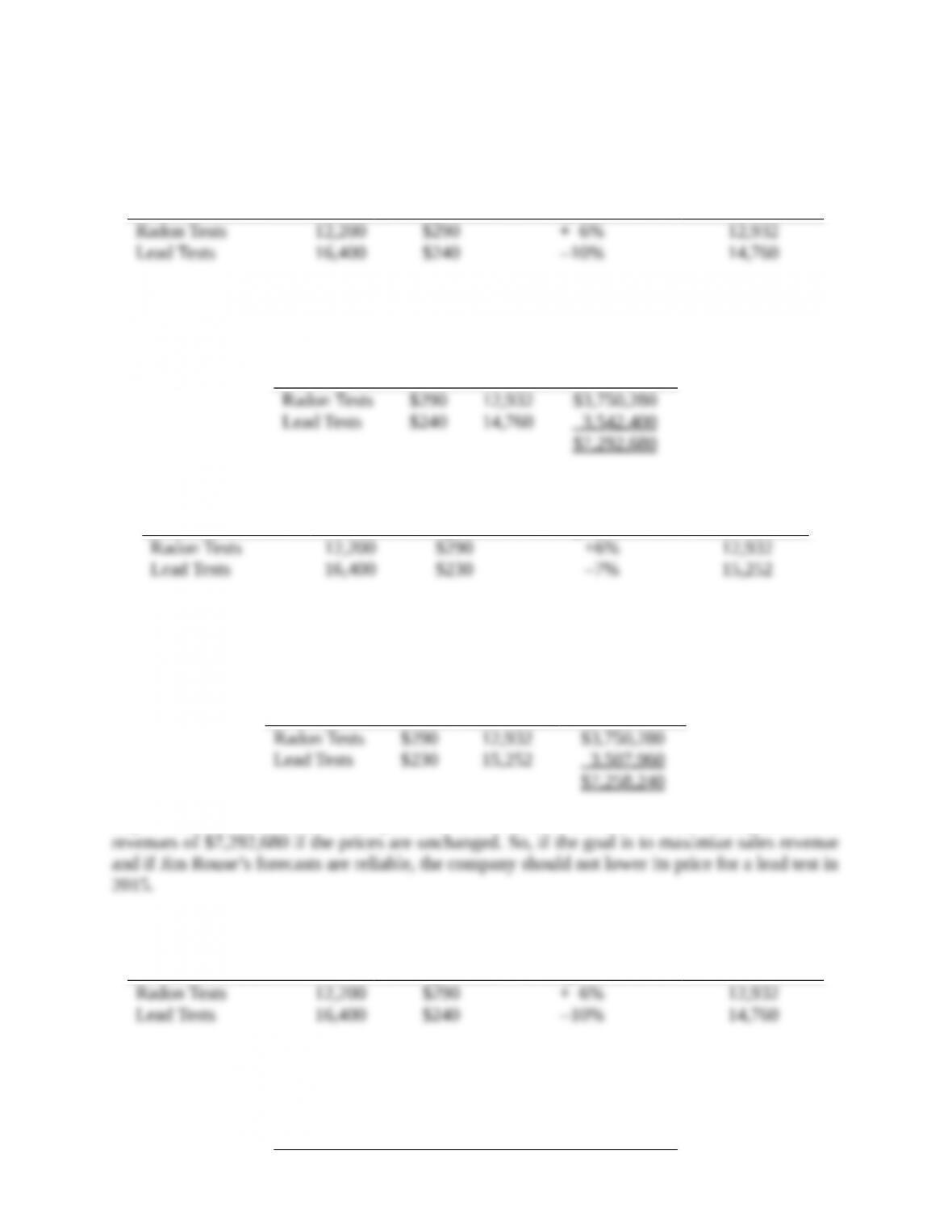

1.

Rouse & Sons

2014

Volume

At 2014

Selling Prices

Expected 2015

Change in Volume

Expected 2015

Volume

Radon Tests

12,200

$290

+ 6%

12,932

Lead Tests

16,400

$240

–10%

14,760

Rouse & Sons Sales Budget

For the Year Ended December 31, 2015

Selling

Price

Units

Sold

Total

Revenues

Radon Tests

$290

12,932

$3,750,280

Lead Tests

$240

14,760

3,542,400

$7,292,680

2.

Rouse & Sons

2014

Volume

Planned 2015

Selling Prices

Expected 2015

Change in Volume

Expected

2015 Volume

Radon Tests

12,200

$290

+6%

12,932

Lead Tests

16,400

$230

–7%

15,252

Rouse & Sons Sales Budget

For the Year Ended December 31, 2015

Selling

Price

Units Sold

Total

Revenues

Radon Tests

$290

12,932

$3,750,280

Lead Tests

$230

15,252

3,507,960

$7,258,240

Expected revenues at the new 2015 prices are $7,258,240, which is lower than the expected 2015

revenues of $7,292,680 if the prices are unchanged. So, if the goal is to maximize sales revenue

and if Jim Rouse’s forecasts are reliable, the company should not lower its price for a lead test in

2015.

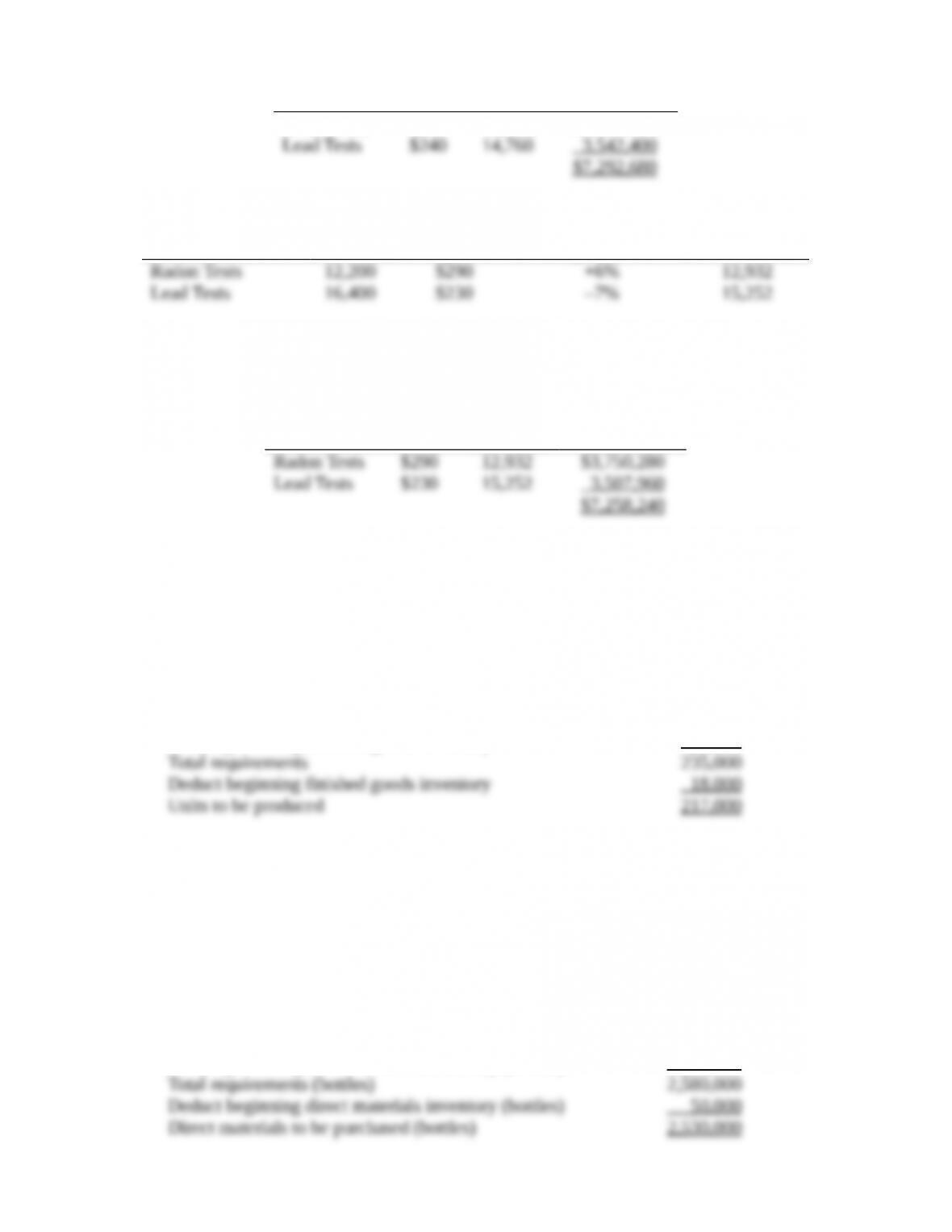

1.

Rouse & Sons

2014

Volume

At 2014

Selling Prices

Expected 2015

Change in Volume

Expected 2015

Volume

Radon Tests

12,200

$290

+ 6%

12,932

Lead Tests

16,400

$240

–10%

14,760

Rouse & Sons Sales Budget

For the Year Ended December 31, 2015

Selling

Price

Units

Sold

Total

Revenues

Radon Tests

$290

12,932

$3,750,280

Lead Tests

$240

14,760

3,542,400

$7,292,680

6-4

2.

Rouse & Sons

2014

Volume

Planned 2015

Selling Prices

Expected 2015

Change in Volume

Expected

2015 Volume

Radon Tests

12,200

$290

+6%

12,932

Lead Tests

16,400

$230

–7%

15,252

Rouse & Sons Sales Budget

For the Year Ended December 31, 2015

Selling

Price

Units Sold

Total

Revenues

Radon Tests

$290

12,932

$3,750,280

Lead Tests

$230

15,252

3,507,960

$7,258,240

6-17 (5 min.) Sales and production budget.

The McKnight Company expects sales in 2015 of 208,000 units of serving trays. McKnight’s

beginning inventory for 2015 is 18,000 trays, and its target ending inventory is 27,000 trays.

Compute the number of trays budgeted for production in 2015.

SOLUTION

Budgeted sales in units 208,000

Add target ending finished goods inventory 27,000

Total requirements 235,000

Deduct beginning finished goods inventory 18,000

Units to be produced 217,000

6-18 (5 min.) Direct materials purchases budget.

Inglenook Co. produces wine. The company expects to produce 2,500,000 two-liter bottles of

Chablis in 2015. Inglenook purchases empty glass bottles from an outside vendor. Its target ending

inventory of such bottles is 80,000; its beginning inventory is 50,000. For simplicity, ignore

breakage. Compute the number of bottles to be purchased in 2015.

SOLUTION

Direct materials to be used in production (bottles) 2,500,000

Add target ending direct materials inventory (bottles) 80,000

Total requirements (bottles) 2,580,000

Deduct beginning direct materials inventory (bottles) 50,000

Direct materials to be purchased (bottles) 2,530,000

6-19 (10 min.) Budgeting material purchases.

6-5

The Howell Company has prepared a sales budget of 43,000 finished units for a 3–month period.

The company has an inventory of 11,000 units of finished goods on hand at December 31 and has

a target finished goods inventory of 19,000 units at the end of the succeeding quarter.

It takes 4 gallons of direct materials to make one unit of finished product. The company has an

inventory of 66,000 gallons of direct materials at December 31 and has a target ending inventory

of 56,000 gallons at the end of the succeeding quarter. How many gallons of direct materials should

Howell Company purchase during the 3 months ending March 31?

SOLUTION

Production Budget:

Finished Goods

(units)

Budgeted sales 43,000

Add target ending finished goods inventory 19,000

Total requirements 62,000

Deduct beginning finished goods inventory 11,000

Units to be produced 51,000

Direct Materials Purchases Budget:

Direct Materials

(in gallons)

Direct materials needed for production (51,000 4) 204,000

Add target ending direct materials inventory 56,000

Total requirements 260,000

Deduct beginning direct materials inventory 66,000

Direct materials to be purchased 194,000

6-20 (15–20 min.) Revenues, production, and purchases budget.

The Mochizuki Co. in Japan has a division that manufactures two–wheel motorcycles. Its budgeted

sales for Model G in 2015 is 915,000 units. Mochizuki’s target ending inventory is 70,000 units,

and its beginning inventory is 115,000 units. The company’s budgeted selling price to its

distributors and dealers is 405,000 yen (¥) per motorcycle.

Mochizuki buys all its wheels from an outside supplier. No defective wheels are accepted.

(Mochizuki’s needs for extra wheels for replacement parts are ordered by a separate division of

the company.) The company’s target ending inventory is 72,000 wheels, and its beginning

inventory is 55,000 wheels. The budgeted purchase price is 18,000 yen (¥) per wheel.

Required:

1. Compute the budgeted revenues in yen.

2. Compute the number of motorcycles that Mochizuki should produce.

3. Compute the budgeted purchases of wheels in units and in yen.

4. What actions can Mochizuki’s managers take to reduce budgeted purchasing costs of wheels

assuming the same budgeted sales for Model G?

6-6

SOLUTION

1. 915,000 motorcycles 405,000 yen = 370,575,000,000 yen

2. Budgeted sales (motorcycles) 915,000

Add target ending finished goods inventory 70,000

Total requirements 985,000

Deduct beginning finished goods inventory 115,000

Units to be produced 870,000

3. Direct materials to be used in production,

870,000 × 2 (wheels) 1,740,000

Add target ending direct materials inventory 72,000

Total requirements 1,812,000

Deduct beginning direct materials inventory 55,000

Direct materials to be purchased (wheels) 1,757,000

Cost per wheel in yen × 18,000

Direct materials purchase cost in yen ¥31,626,000,000

4. Note the relatively small inventory of wheels. In Japan, suppliers tend to be located very close

to the major manufacturer. Inventories are controlled by just–in-time and similar systems.

Indeed, some direct materials inventories are almost nonexistent. Nevertheless, Yoshida’s

managers would want to check why the target ending inventory of wheels (72,000) is greater

than the beginning inventory of 55,000. Could the production process be streamlined and made

more efficient to reduce the need to hold more inventories?

Furthermore, Yoshida could help improve quality, efficiency, and productivity of its

wheels supplier to reduce the cost of manufacturing wheels and hence the price the supplier

charges Yoshida. Toyota routinely aids its suppliers in this way and also reduces costs through

better coordination between suppliers and the company.

6-21 (30 min.) Revenues and production budget.

Price, Inc., bottles and distributes mineral water from the company’s natural springs in northern

Oregon. Price markets two products: 12–ounce disposable plastic bottles and 1-gallon reusable

plastic containers.

Required:

1. For 2015, Price marketing managers project monthly sales of 420,000 12-ounce bottles and

170,000 1-gallon containers. Average selling prices are estimated at $0.20 per 12-ounce bottle

and $1.50 per 1-gallon container. Prepare a revenues budget for Price, Inc., for the year ending

December 31, 2015.

2. Price begins 2015 with 890,000 12–ounce bottles in inventory. The vice president of operations

requests that 12–ounce bottles ending inventory on December 31, 2015, be no less than 680,000

bottles. Based on sales projections as budgeted previously, what is the minimum number of

12-ounce bottles Price must produce during 2015?

3. The VP of operations requests that ending inventory of 1-gallon containers on December 31,

2015, be 240,000 units. If the production budget calls for Price to produce 1,900,000 1-gallon

6-7

containers during 2015, what is the beginning inventory of 1-gallon containers on January 1,

2015?

SOLUTION

1.

Selling

Price

Units

Sold

Total

Revenues

12-ounce bottles

$0.20

5,040,000a

$1,008,000

1-gallon units

1.50

2,040,000b

3,060,000

$4,068,000

a 420,000 × 12 months = 5,040,000

b 170,000 × 12 months = 2,040,000

2. Budgeted unit sales (12-ounce bottles) 5,040,000

Add target ending finished goods inventory 680,000

Total requirements 5,720,000

Deduct beginning finished goods inventory 890,000

Units to be produced 4,830,000

3.

Beginning Budgeted Target Budgeted

= +

inventory sales ending inventory production

−

= 2,040,000 + 240,000 − 1,900,000

= 380,000 1-gallon units

4.

Beginning Budgeted Target Budgeted

= +

inventory sales ending inventory production

−

6-22 (30 min.) Budgeting: direct material usage, manufacturing cost, and gross margin.

Xander Manufacturing Company manufactures blue rugs, using wool and dye as direct materials.

One rug is budgeted to use 36 skeins of wool at a cost of $2 per skein and 0.8 gallons of dye at a

cost of $6 per gallon. All other materials are indirect. At the beginning of the year Xander has an

inventory of 458,000 skeins of wool at a cost of $961,800 and 4,000 gallons of dye at a cost of

$23,680. Target ending inventory of wool and dye is zero. Xander uses the FIFO inventory cost

flow method.

Xander blue rugs are very popular and demand is high, but because of capacity constraints the

firm will produce only 200,000 blue rugs per year. The budgeted selling price is $2,000 each.

There are no rugs in beginning inventory. Target ending inventory of rugs is also zero.

Xander makes rugs by hand, but uses a machine to dye the wool. Thus, overhead costs are

accumulated in two cost pools—one for weaving and the other for dyeing. Weaving overhead is

allocated to products based on direct manufacturing labor–hours (DMLH). Dyeing overhead is

allocated to products based on machine-hours (MH).

There is no direct manufacturing labor cost for dyeing. Xander budgets 62 direct manufacturing

labor-hours to weave a rug at a budgeted rate of $13 per hour. It budgets 0.2 machine-hours to dye

each skein in the dyeing process.

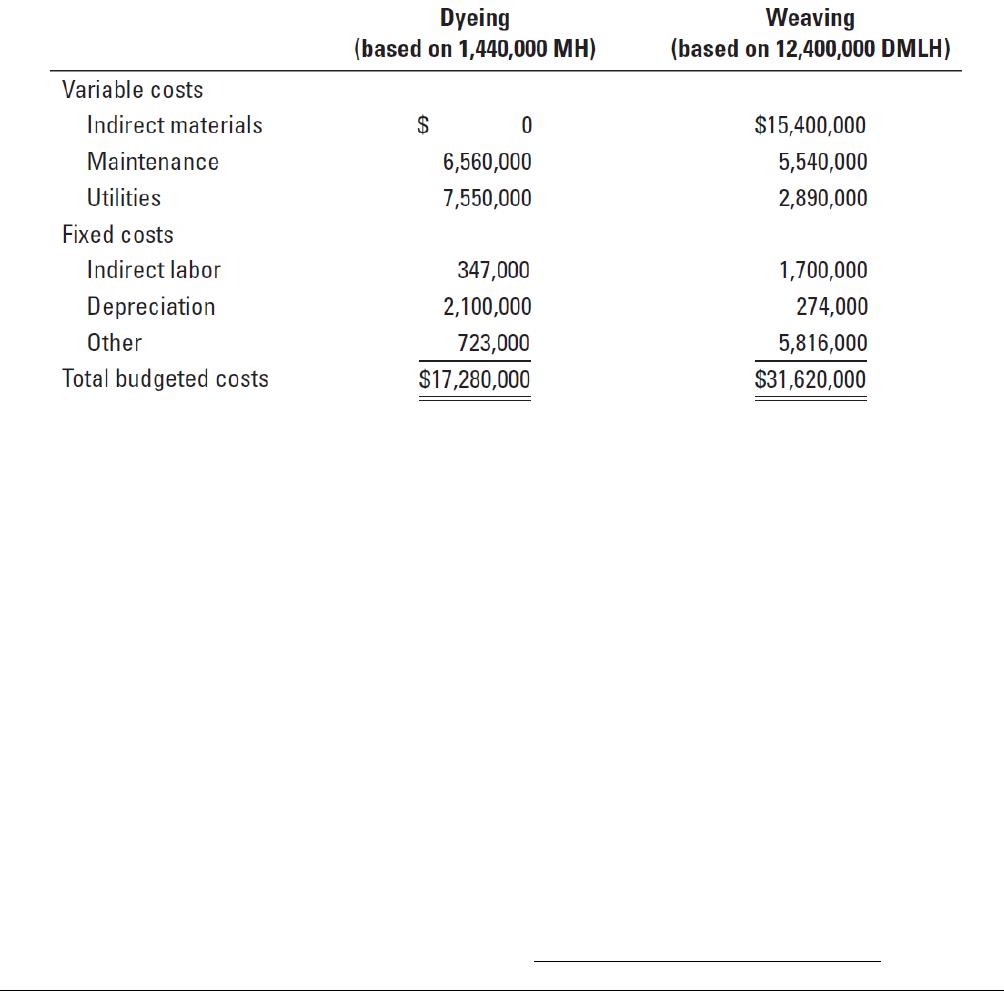

The following table presents the budgeted overhead costs for the dyeing and weaving cost

pools:

Required:

1. Prepare a direct material usage budget in both units and dollars.

2. Calculate the budgeted overhead allocation rates for weaving and dyeing.

3. Calculate the budgeted unit cost of a blue rug for the year.

4. Prepare a revenues budget for blue rugs for the year, assuming Xander sells (a) 200,000 or (b)

185,000 blue rugs (that is, at two different sales levels).

5. Calculate the budgeted cost of goods sold for blue rugs under each sales assumption.

6. Find the budgeted gross margin for blue rugs under each sales assumption.

7. What actions might you take as a manager to improve profitability if sales drop to 185,000

blue rugs?

8. How might top management at Xander use the budget developed in requirements 1–6 to better

manage the company?

SOLUTION

1.

Direct Material Usage Budget in Quantity and Dollars

Material

Wool

Dye

Total

Physical Units Budget

Direct materials required for

Blue Rugs (200,000 rugs × 36 skeins and 0.8 gal.)

7,200,000 skeins

160,000 gal.

Cost Budget

Available from beginning direct materials inventory:

(a)

Wool: 458,000 skeins

$ 961,800

Dye: 4,000 gallons

$ 23,680

To be purchased this period: (b)

Wool: (7,200,000 – 458,000) skeins × $2 per skein

13,484,000

Dye: (160,000 – 4,000) gal. × $6 per gal.

936,000

Direct materials to be used this period: (a) + (b)

$14,445,800

$ 959,680

$15,405,480

2.

Weaving budgeted

overhead rate

=

$31,620,000

12,400,000 DMLH

= $2.55 per DMLH

Dyeing budgeted

overhead rate

=

$17,280,000

1,440,000 MH

= $12 per MH

3.

Budgeted Unit Cost of Blue Rug

Cost per

Unit of Input

Input per

Unit of

Output

Total

Wool

$ 2

36 skeins

$ 72.00

Dye

6

0.8 gal.

4.80

Direct manufacturing labor

13

62 hrs.

806.00

Dyeing overhead

12

7.21 mach-hrs.

86.40

Weaving overhead

2.55

62 DMLH

158.10

Total

$1,127.30

10.2 machine hour per skein

36 skeins per rug = 7.2 machine-hrs. per rug.

4.

Revenue Budget

Units

Selling

Price

Total Revenues

Blue Rugs

200,000

$2,000

$400,000,000

Blue Rugs

185,000

$2,000

$370,000,000

5a.

Sales = 200,000 rugs

Cost of Goods Sold Budget

From Schedule

Total

Beginning finished goods inventory

$ 0

Direct materials used

$ 15,405,480

Direct manufacturing labor ($806 × 200,000)

161,200,000

Dyeing overhead ($86.40 × 200,000)

17,280,000

Weaving overhead ($158.10 × 200,000)

31,620,000

225,505,480

Cost of goods available for sale

225,505,480

6-10

Deduct ending finished goods inventory

0

Cost of goods sold

$225,505,480

5b.

Sales = 185,000 rugs

Cost of Goods Sold Budget

From Schedule

Total

Beginning finished goods inventory

$ 0

Direct materials used

$ 15,405,480

Direct manufacturing labor ($806 × 200,000)

161,200,000

Dyeing overhead ($86.40 × 200,000)

17,280,000

Weaving overhead ($158.10 × 200,000)

31,620,000

225,505,480

Cost of goods available for sale

225,505,480

Deduct ending finished goods inventory

($1,127.30 × 15,000)

16,909,500

Cost of goods sold

$208,595,980

6.

200,000 rugs sold

185,000 rugs sold

Revenue

$400,000,000

$370,000,000

Less: Cost of goods sold

225,505,480

208,595,980

Gross margin

$174,494,520

$161,404,020

7. If sales drop to 185,000 blue rugs, Xander should look to reduce fixed costs and produce

less to reduce variable costs and inventory costs.

8. Top management can look for ways to increase (stretch) sales and improve quality,

efficiency, and input prices to reduce costs in each cost category such as direct materials, direct

manufacturing labor, and overhead costs. Top management can also use the budget to coordinate

and communicate across different parts of the organization, create a framework for judging

performance and facilitating learning, and motivate managers and employees to achieve “stretch”

targets of higher revenues and lower costs.