1) A positive aspect of backflush costing is the presence of the visible audit trail.

2) The credit rating agencies require detailed disclosures of the compensation

arrangements of top-level executives.

3) Minimum transfer price can be arrived at by adding incremental cost per unit

incurred up to the point of transfer with the markup required.

4) The smaller the amount of a cost the more likely it is economically feasible to trace it

to a particular cost object.

5) Performing professional duties in accordance with relevant laws, regulations, and

technical standards is a competent responsibility.

6) The accounting procedures in a backflush-costing system strictly adhere to Generally

Accepted Accounting Principles (GAAP).

7) Cost-based transfer prices are helpful when markets are not perfectly competitive.

8) Multiple regression analysis uses only independent variables and not dependent

variables.

9) A standard is attainable through efficient operations but allows for normal disruptions

such as machine breakdowns and defective production.

10) Budgets are not remedies for weak management talent, faulty organization, or a

poor accounting system.

11) Hybrid transfer prices take into account both cost and market information.

12) Committed fixed costs represent organizational investments with a multi-year

planning horizon that cant be significantly reduced even for short periods.

13) In the manufacturing plant, Alex is paid $40 an hour for straight-time and $60 an

hour for overtime. One week she worked 54 hours, which included 8 hours of overtime,

and 6 hours of idle time caused by material shortages.

Required:

a.What is Alex’s total compensation for the week?

b.What amount of compensation would be reported as direct manufacturing labor?

c.What amount of compensation would be reported as manufacturing overhead?

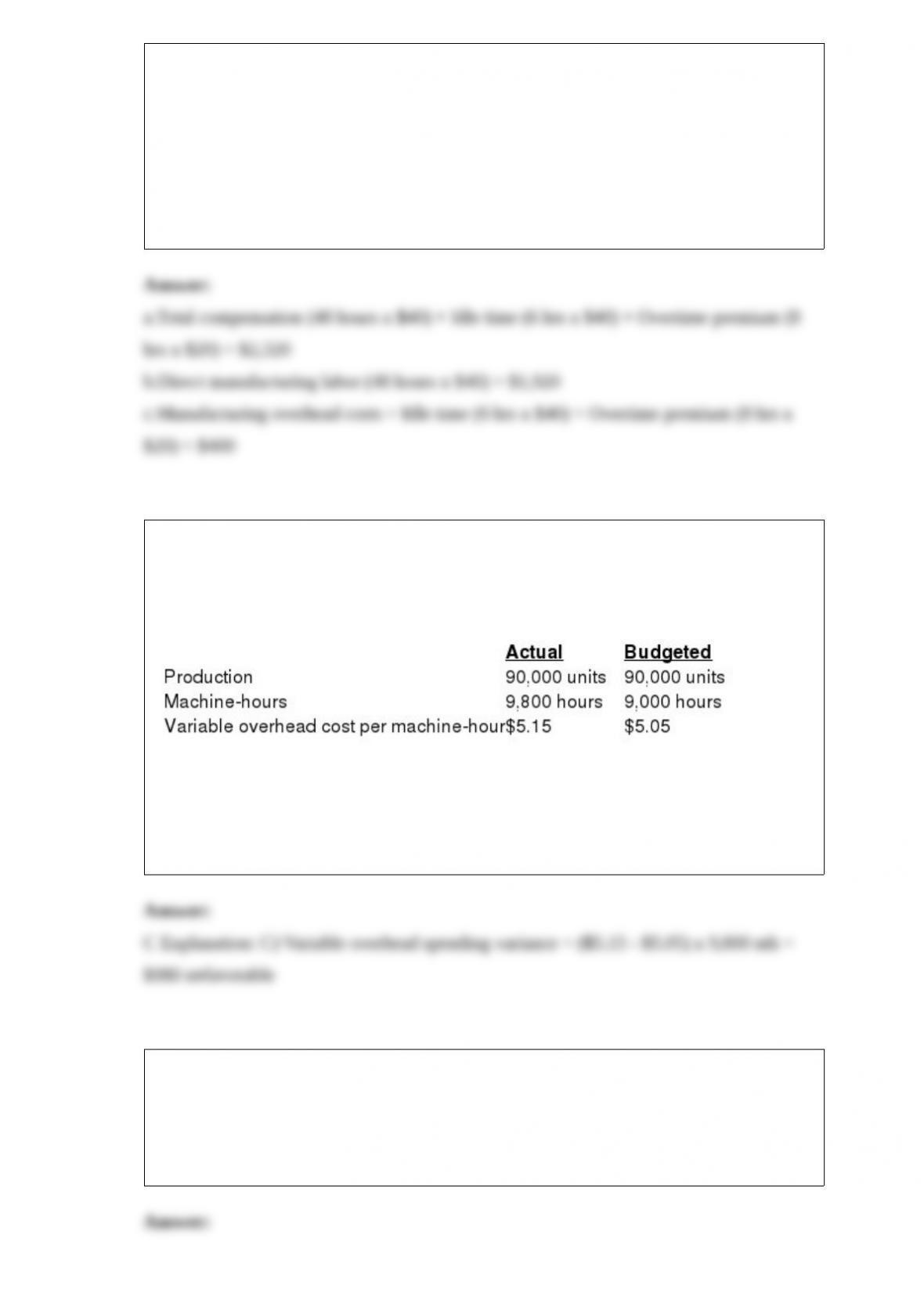

14) Zitrik Corporation manufactured 90,000 buckets during February. The variable

overhead cost-allocation base is $5.05 per machine-hour. The following variable

overhead data pertain to February:

What is the variable overhead spending variance?

A) $980 favorable

B) $900 unfavorable

C) $980 unfavorable

D) $900 favorable

15) Long-run pricing decisions ________.

A) have a time horizon of less than one year

B) include adjusting product mix in a competitive environment

C) and short-run pricing decisions generally have the same relevant costs

D) use prices that include a reasonable return on investment

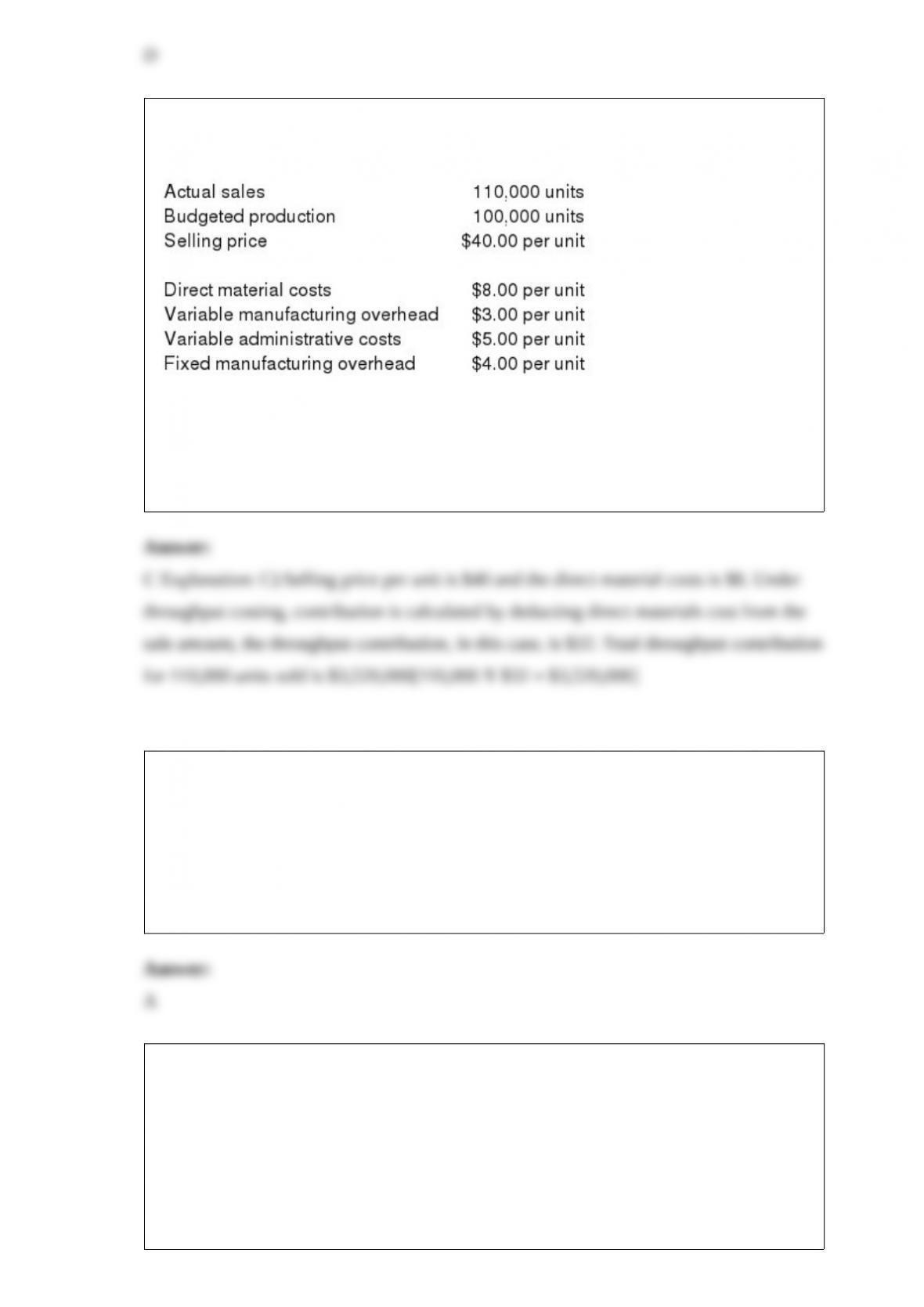

16) Daniel Rubber Company produces a specialty item. Management has provided the

following information:

What is the total throughput contribution?

A) $2,640,000

B) $3,190,000

C) $3,520,000

D) $4,070,000

17) A company would use multiple cost-allocation bases ________.

A) if managers believed the benefits exceeded the additional costs of that costing

system

B) because there is more than one way to allocate overhead

C) because this is a simpler approach than using one cost allocation base

D) if managers believe that using multiple cost-allocation bases is the only acceptable

method

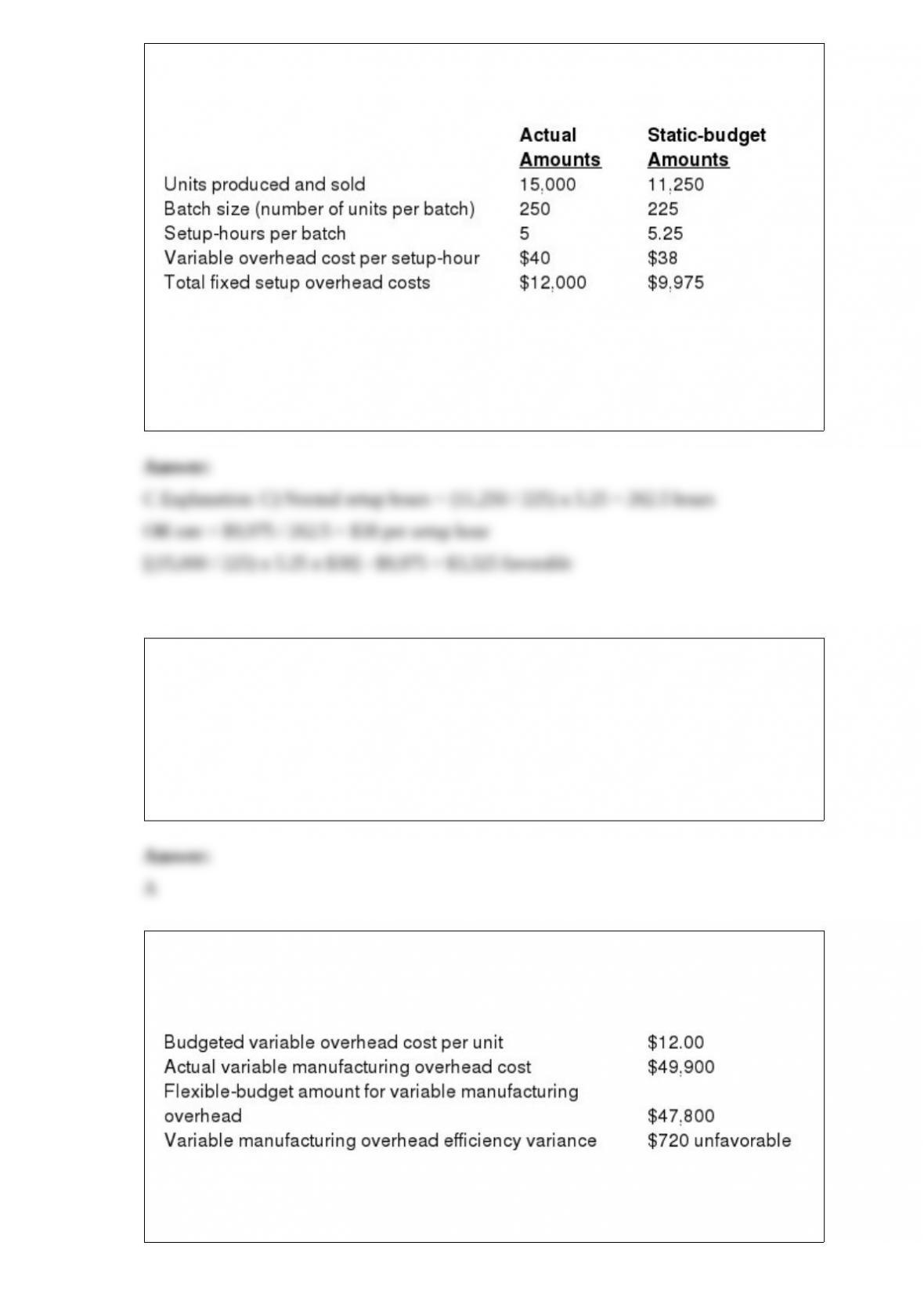

18) Munoz, Inc., produces a special line of plastic toy racing cars. Munoz, Inc.,

produces the cars in batches. To manufacture a batch of the cars, Munoz, Inc., must set

up the machines and molds. Setup costs are batch-level costs because they are

associated with batches rather than individual units of products. A separate Setup

Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are

fixed with respect to the number of setup-hours. The following information pertains to

June 2015:

Calculate the production-volume variance for fixed overhead setup costs.

A) $3,325 unfavorable

B) $400 unfavorable

C) $3,325 favorable

D) $400 favorable

19) ________ is a method of inventory costing in which all variable manufacturing

costs (direct and indirect) are included as inventoriable costs and all fixed

manufacturing costs are excluded.

A) Variable costing

B) Mixed costing

C) Absorption costing

D) Standard costing

20) Neocomfort Corporation manufactured 3,000 chairs during June. The following

variable overhead data relates to June:

What is the variable overhead spending variance?

A) $1,380 favorable

B) $2,820 favorable

C) $2,820 unfavorable

D) $1,380 unfavorable

21) Cost-based prices ________.

A) are one way of setting prices in a competitive market

B) provide an inherit incentive for the producer to control costs

C) pass the majority of risk to the buyer

D) are required in all government contracts

22) The Internal Revenue Service requires the use of ________ for calculating fixed

manufacturing costs per unit.

A) practical capacity

B) theoretical capacity

C) master-budget capacity utilization

D) normal capacity utilization

23) Cysco Corp has a budget of $1,200,000 in 2015 for prevention costs. If it decides to

automate a portion of its prevention activities, it will save $100,000 in variable costs.

The new method will require $50,000 in training costs and $140,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 200,000 units.

Appraisal costs for the year are budgeted at $500,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $30 per failed unit of

finished goods. The internal failure rate is expected to be 5% of all completed items.

The proposed changes will cut the internal failure rate by one-half. Internal failure units

are destroyed. External failure costs average $50 per failed unit. The company’s average

external failures average 2.5% of units sold. The new proposal will reduce this rate to

1%. Assume all units produced are sold and there are no ending inventories.

How much do external failure costs change if all the changes are as the new prevention

procedures anticipated? Assume all units produced are sold and there are no ending

inventories.

A) $126,000 decrease

B) $150,000 decrease

C) $100,000 decrease

D) $122,400 decrease

24) When variances are immaterial, which of the following statements is true of the

journal entry to write-off the variable overhead variance accounts?

A) Cost of Goods Sold account will always be debited.

B) Unfavorable efficiency variance will be credited.

C) Favorable efficiency variance will be credited.

D) Cost of Goods Sold account will always be credited.

25) List and briefly describe the six steps in estimating a cost function under

quantitative analysis.

26) Describe the differences between process costing and job costing. Discuss some

typical products which would be more likely to use process costing as compared to

some which would be more likely to use job costing.

27) What conflicts can arise between using discounted cash flow methods for capital

budgeting decisions and accrual accounting for performance evaluation? How can these

conflicts be reduced?

28) Why do organizations use budgeted rates instead of actual rates to allocate the costs

of support departments to each other and to user departments and divisions? Explain.

29) The textbook discusses three levels of variances,

30) Listed below are elements of the master budget. Determine whether each budget is

an operating budget or a financial budget. Place an O for operating budget or F for a

financial budget.

1.Capital expenditures budget

2.Cost of goods sold budget

3.Revenues budget

4.Budgeted statement of cash flows

5.Distribution costs budget

6.Marketing costs budget

7.Cash budget

8.Direct materials cost budget

9.Budgeted balance sheet

10.Budgeted income statement

31) Explain the difference between the gross margin format and the contribution margin

format for the income statement. What information is highlighted with each?

32) Patrick Ross, the president of Corise’s Wild Game Company, has asked for

information about the cost behavior of manufacturing overhead costs. Specifically, he

wants to know how much overhead cost is fixed and how much is variable. The

following data are the only records available:

Required:

Using the high-low method, determine the overhead cost equation. Use machine-hours

as your cost driver.