Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

18-

1

CHAPTER 18

SPOILAGE, REWORK, AND SCRAP

18-1 Managers have found that improved quality and intolerance for high spoilage have lowered

overall costs and increased sales.

18-2 Spoilage—units of production that do not meet the standards required by customers for

good units and that are discarded or sold at reduced prices.

Rework—units of production that do not meet the specifications required by customers but

that are subsequently repaired and sold as good finished units.

Scrap—residual material that results from manufacturing a product. It has low total sales

value compared to the total sales value of the product.

18-3 Yes. Normal spoilage is spoilage inherent in a particular production process that arises

even under efficient operating conditions. Management decides the spoilage rate it considers

normal depending on the production process.

18-4 Abnormal spoilage is spoilage that is not inherent in a particular production process and

would not arise under efficient operating conditions. Costs of abnormal spoilage are “lost costs,”

measures of inefficiency that should be written off directly as losses for the accounting period.

18-5 Management effort can affect the spoilage rate. Many companies are relentlessly reducing

their rates of normal spoilage, spurred on by competitors who, likewise, are continuously reducing

costs.

18-6 Normal spoilage typically is expressed as a percentage of good units passing the inspection

point. Given actual spoiled units, we infer abnormal spoilage as follows:

Abnormal spoilage = Actual spoilage – Normal spoilage.

18-7 Accounting for spoiled goods deals with cost assignment, rather than with cost incurrence,

because the existence of spoiled goods does not involve any additional cost beyond the amount

already incurred.

18-8 Yes. Normal spoilage rates should be computed from the good output or from the normal

input, not the total input. Normal spoilage is a given percentage of a certain output base. This base

should never include abnormal spoilage, which is included in total input. Abnormal spoilage does

not vary in direct proportion to units produced and to include it would cause the normal spoilage

count to fluctuate irregularly and not vary in direct proportion to the output base.

18-9 Yes, the point of inspection is the key to the assignment of spoilage costs. Normal spoilage

costs do not attach solely to units transferred out. Thus, if units in ending work in process have

passed inspection, they should have normal spoilage costs added to them.

18-10 No. If abnormal spoilage is detected at a different point in the production cycle than normal

spoilage, then unit costs would differ. If, however, normal and abnormal spoilage are detected at

the same point in the production cycle, their unit costs would be the same.

18-11 No. Spoilage may be considered a normal characteristic of a given production cycle. The

costs of normal spoilage caused by a random malfunction of a machine would be charged as a part

of the manufacturing overhead allocated to all jobs. Normal spoilage attributable to a specific job

is charged to that job.

18-12 No. Unless there are special reasons for charging normal rework to jobs that contained the

bad units, the costs of extra materials, labor, and so on are usually charged to manufacturing

overhead and allocated to all jobs.

18-

2

18-13 Yes. Abnormal rework is a loss just like abnormal spoilage. By charging it to

manufacturing overhead, the abnormal rework costs are spread over other jobs and also included

in inventory to the extent a job is not complete. Abnormal rework is rework over and above what

is expected during a period and is recognized as a loss for that period.

18-14 A company is justified in inventorying scrap when its estimated net realizable value is

significant and the time between storing it and selling or reusing it is quite long.

18-15 Companies measure scrap to measure efficiency and to also control a tempting source of

theft. Managers of companies that report high levels of scrap focus attention on ways to reduce

scrap and to use the scrap the company generates more profitably. Some companies, for example,

might redesign products and processes to reduce scrap. Others may also examine if the scrap can

be reused to save substantial input costs.

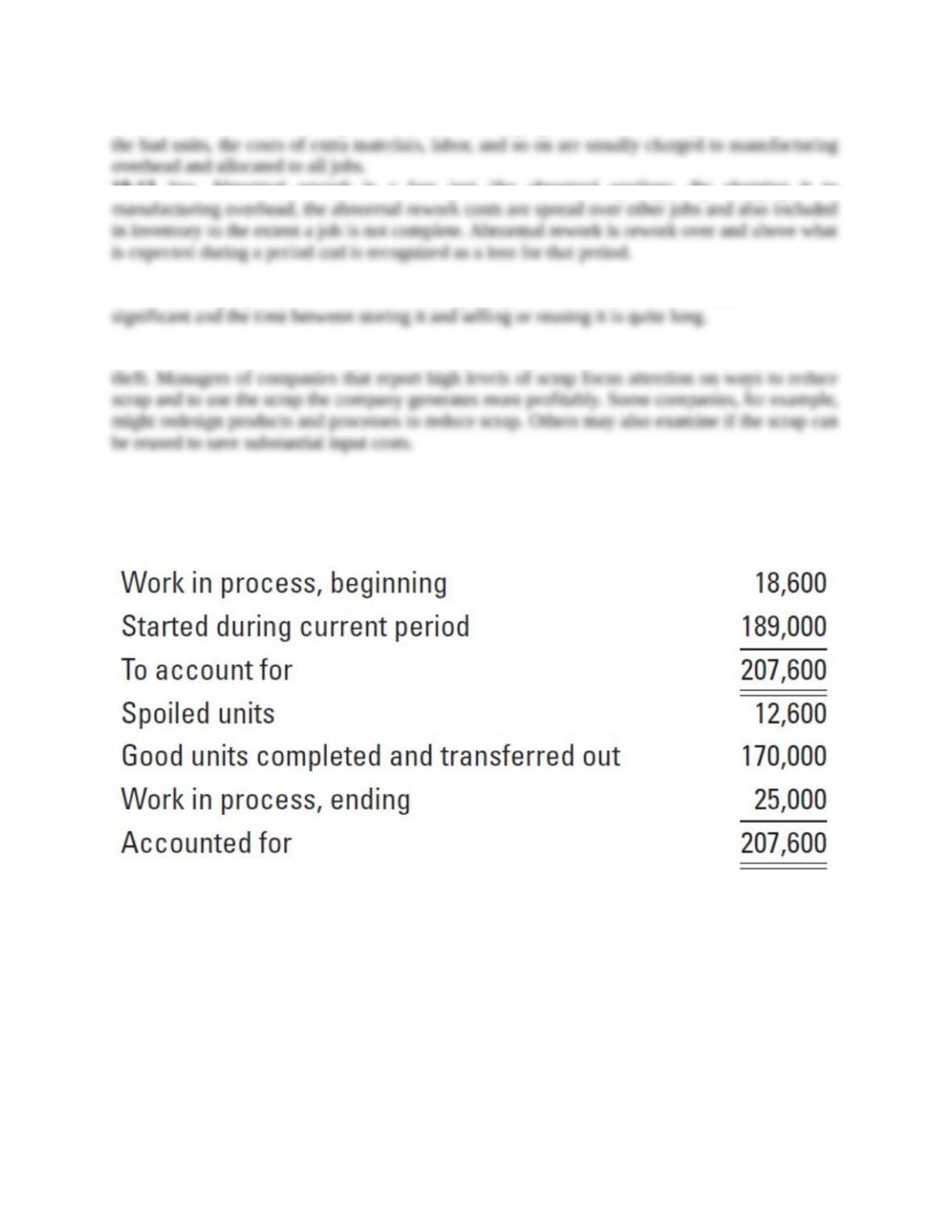

18-16 (5–10 min.) Normal and abnormal spoilage in units.

The following data, in physical units, describe a grinding process for January:

Inspection occurs at the 100% completion stage. Normal spoilage is 4% of the good units passing

inspection.

Required:

1. Compute the normal and abnormal spoilage in units.

2. Assume that the equivalent-unit cost of a spoiled unit is $11. Compute the amount of potential

savings if all spoilage were eliminated, assuming that all other costs would be unaffected.

Comment on your answer.

SOLUTION

1. Total spoiled units 12,600

Normal spoilage in units, 4% 170,000 6,800

18-

3

Abnormal spoilage in units 5,800

2. Abnormal spoilage, 5,800 $11 $ 63,800

Normal spoilage, 6,800 $11 74,800

Potential savings, 12,600 $11 $138,600

Regardless of the targeted normal spoilage, abnormal spoilage is nonrecurring and avoidable.

The targeted normal spoilage rate is subject to change. Many companies have reduced their

spoilage to almost zero, which would realize all potential savings. Of course, zero spoilage usually

means higher-quality products, more customer satisfaction, more employee satisfaction, and

various beneficial effects on nonmanufacturing (for example, purchasing) costs of direct materials.

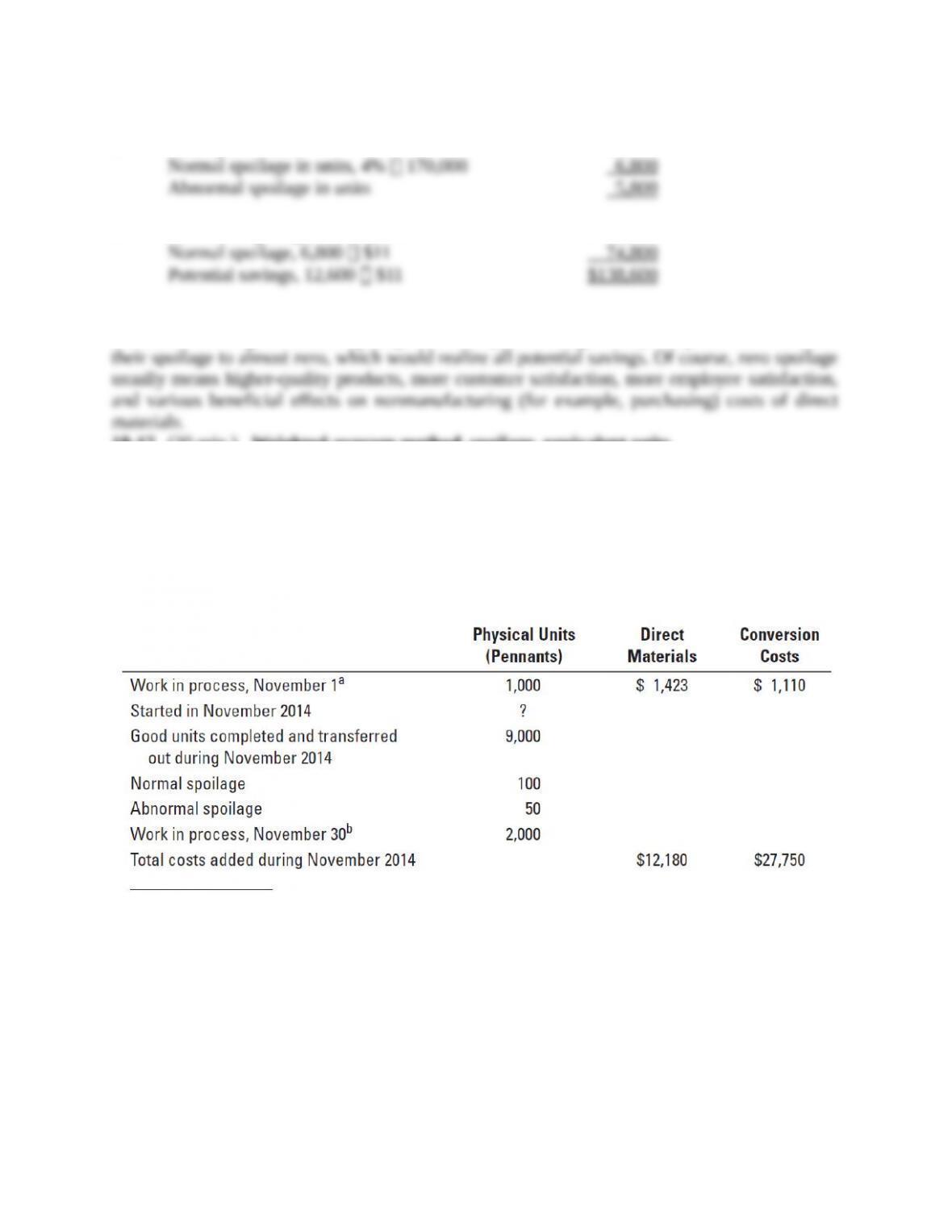

18-17 (20 min.) Weighted-average method, spoilage, equivalent units.

(CMA, adapted) Consider the following data for November 2014 from Gray Manufacturing

Company, which makes silk pennants and uses a process-costing system. All direct materials are

added at the beginning of the process, and conversion costs are added evenly during the process.

Spoilage is detected upon inspection at the completion of the process. Spoiled units are disposed

of at zero net disposal value. Gray Manufacturing Company uses the weighted-average method of

process costing.

aDegree of completion: direct materials, 100%; conversion costs, 50%.

bDegree of completion: direct materials, 100%; conversion costs, 30%.

Required:

Compute equivalent units for direct materials and conversion costs. Show physical units in the first

column of your schedule.

SOLUTION

Solution Exhibit 18-17 calculates equivalent units of work done to date for direct materials and

conversion costs.

SOLUTION EXHIBIT 18-17

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing with Spoilage,

Gray Manufacturing Company for November 2014.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period

To account for

Good units completed and transferred out

during current period:

Normal spoilage*

100 100%; 100 100%

Abnormal spoilage†

50 100%; 50 100%

Work in process, ending‡ (given)

2,000 100%; 2,000 30%

Accounted for

Equivalent units of work done to date

1,000

10,150a

11,150

9,000

100

50

2,000

11,150

9,000

100

50

2,000

11,150

9,000

100

50

600

9,750

a From below, 11,150 total units are accounted for. Therefore, units started during current period must be = 11,150 – 1,000 = 10,150.

*Degree of completion of normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 30%.

18-18 (20−25 min.) Weighted-average method, assigning costs (continuation of 18-17).

Required:

For the data in Exercise 18-17, summarize the total costs to account for; calculate the cost per

equivalent unit for direct materials and conversion costs; and assign costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work-in-

process inventory.

SOLUTION

Solution Exhibit 18-18 summarizes total costs to account for, calculates the costs per equivalent

unit for direct materials and conversion costs, and assigns total costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to ending work in process.

Solution Exhibit 18-18 summarizes total costs to account for,

SOLUTION EXHIBIT 18-18

Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory;

Weighted-Average Method of Process Costing,

Gray Manufacturing Company, November 2014.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs incurred to date

Divided by equivalent units of work done to date

Cost per equivalent unit

(Step 5) Assignment of costs

Good units completed and transferred out (9,000 units)

$ 2,533

39,930

$42,463

$ 1,423

12,180

$13,603

$13,603

11,150

$ 1.22

$ 1,110

27,750

$28,860

$28,860

9,750

$ 2.96

Costs before adding normal spoilage

Normal spoilage (100 units)

(A) Total cost of good units completed & transf. out

(B) Abnormal spoilage (50 units)

(C) Work in process, ending (2,000 units)

(A)+(B)+(C) Total costs accounted for

$37,620

418

38,038

209

4,216

$42,463

(9,000# $1.22) + (9,000# $2.96)

(100# $1.22) + (100# $2.96)

(50# $1.22) + (50# $2.96)

(2,000# $1.22) + (600# $2.96)

$13,603 + $28,860

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-17.

18-19 (15 min.) FIFO method, spoilage, equivalent units.

Refer to the information in Exercise 18-17. Suppose Gray Manufacturing Company uses the FIFO

method of process costing instead of the weighted-average method.

Required:

Compute equivalent units for direct materials and conversion costs. Show physical units in the first

column of your schedule.

SOLUTION

Solution Exhibit 18-19 calculates equivalent units of work done in the current period for direct

materials and conversion costs.

SOLUTION EXHIBIT 18-19

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

Gray Manufacturing Company for November 2014.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period

To account for

Good units completed and transferred out during current period:

From beginning work in process||

1,000 (100% −100%); 1,000 (100% − 50%)

1,000

10,150a

11,150

1,000

0

500

Started and completed

8,000 100%; 8,000 100%

Normal spoilage*

100 100%; 100 100%

Abnormal spoilage†

50 100%; 50 100%

Work in process, ending‡

2,000 100%; 2,000 30%

Accounted for

Equivalent units of work done in current period

8,000#

100

50

2,000

____

11,150

8,000

100

50

2,000

10,150

8,000

100

50

600

9,250

a From below, 11,150 total units are accounted for. Therefore, units started during current period must be 11,150 –

1,000 = 10,150.

||Degree of completion in this department: direct materials, 100%; conversion costs, 50%.

#9,000 physical units completed and transferred out minus 1,000 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion of normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 30%.

18-20 (20−25 min.) FIFO method, assigning costs (continuation of 18-19).

Required:

For the data in Exercise 18-17, use the FIFO method to summarize the total costs to account for;

calculate the cost per equivalent unit for direct materials and conversion costs; and assign costs to

units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units

in ending work in process.

SOLUTION

Solution Exhibit 18-20 summarizes total costs to account for, calculates the costs per equivalent

unit for direct materials and conversion costs, and assigns total costs to units completed and

transferred out (including normal spoilage), to abnormal spoilage, and to ending work in process.

SOLUTION EXHIBIT 18-20

Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing,

Gray Manufacturing Company, November 2014.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs added in current period

Divided by equivalent units of work done in current period

Cost per equivalent unit

$ 2,533

39,930

$42,463

$ 1,423

12,180

$13,603

$12,180

10,150

$ 1.20

$ 1,110

27,750

$28,860

$27,750

9,250

$ 3

18-

7

(Step 5) Assignment of costs:

Good units completed and transferred out (9,000 units)

Work in process, beginning (1,000 units)

Costs added to beg. work in process in current period

Total from beginning inventory before normal

spoilage

Started and completed before normal spoilage (8,000 units)

Normal spoilage (100 units)

(A) Total costs of good units completed and transferred out

(B) Abnormal spoilage (50 units)

(C) Work in process, ending (2,000 units)

(A)+(B)+(C) Total costs accounted for

$ 2,533

1,500

4,033

33,600

420

38,053

210

4,200

$42,463

$1,423 + $1,110

(0a $1.20) + (500a $3)

(8,000a $1.20) + (8,000a $3)

(100a $1.20) + (100a $3)

(50a $1.20) + (50a $3)

(2,000a $1.20) + (600a $3)

$13,603 + $28,860

a Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-19.

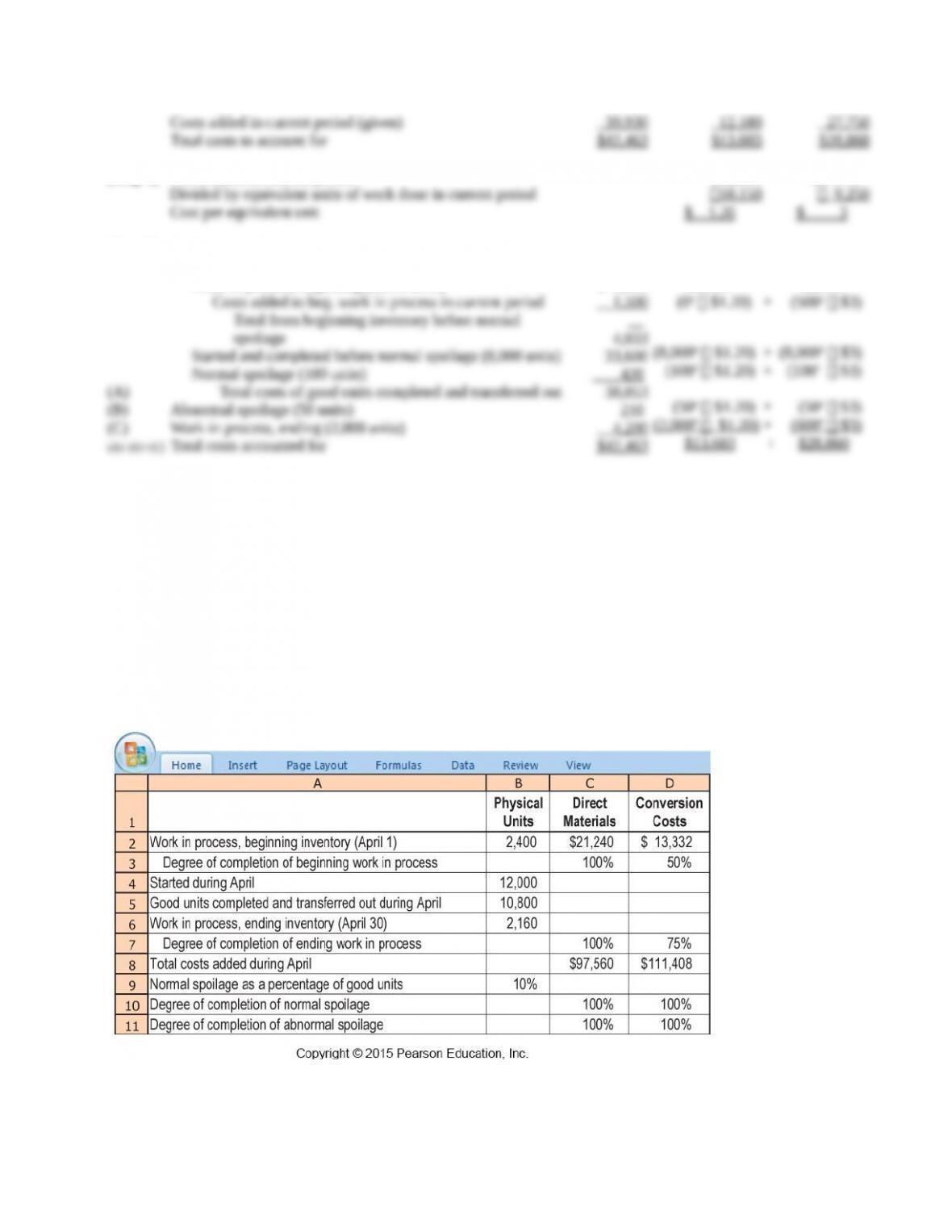

18-21 (35 min.) Weighted-average method, spoilage.

LaCroix Company produces handbags from leather of moderate quality. It distributes the product

through outlet stores and department store chains. At LaCroix’s facility in northeast Ohio, direct

materials (primarily leather hides) are added at the beginning of the process, while conversion

costs are added evenly during the process. Given the importance of minimizing product returns,

spoiled units are detected upon inspection at the end of the process and are discarded at a net

disposal value of zero.

LaCroix uses the weighted-average method of process costing. Summary data for April 2014

are as follows:

Required:

1. For each cost category, calculate equivalent units. Show physical units in the first column of

your schedule.

2. Summarize the total costs to account for; calculate the cost per equivalent unit for each cost

category; and assign costs to units completed and transferred out (including normal spoilage),

to abnormal spoilage, and to units in ending work in process.

18-

8

SOLUTION

1. Solution Exhibit 18-21, Panel A calculates equivalent units of work done to date for direct

materials and conversion costs.

2. Solution Exhibit 18-21, Panel B summarizes total costs to account for, calculates the costs

per equivalent unit for direct materials and conversion costs, and assigns total costs to units

completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in

ending work in process, using the weighted-average method.

SOLUTION EXHIBIT 18-21

Weighted-Average Method of Process Costing with Spoilage,

La Croix Company for April 2014

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

2,400

Started during current period (given)

12,000

To account for

14,400

Good units completed and tsfd. out during current period:

10,800

10,800

10,800

Normal spoilagea

1,080

(1,080

100%; 1,080

100%)

1,080

1,080

Abnormal spoilageb

360

(360

100%; 360

100%)

360

360

Work in process, endingc (given)

2,160

(2,160

100%; 2,160

75%)

______

2,160

1,620

Accounted for

14,400

______

______

Equivalent units of work done to date

14,400

13,860

aNormal spoilage is 10% of good units transferred out: 10% × 10,800 = 1,080 units.

Degree of completion of normal spoilage

in this department: direct materials, 100%; conversion costs, 100%.

bTotal spoilage = Beg. units + Units started - Good units transferred out – Ending units = 2,400 + 12,000 – 10,800 – 2,160 = 1,440;

Abnormal spoilage = Total spoilage – Normal spoilage = 1,440 – 1,080 = 360 units. Degree of completion of abnormal spoilage

in this department: direct materials, 100%; conversion costs, 100%.

cDegree of completion in this department: direct materials, 100%; conversion costs, 75%.

PANEL B: Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3)

Work in process, beginning (given)

$ 34,572

$21,240

$ 13,332

Costs added in current period (given)

208,968

97,560

111,408

Total costs to account for

$243,540

$118,800

$124,740

(Step 4)

Costs incurred to date

$118,800

$124,740

Divide by equivalent units of work done to date

14,400

÷13,860

Cost per equivalent unit

$ 8.25

$ 9.00

(Step 5)

Assignment of costs

Good units completed and transferred out (10,800 units)

Costs before adding normal spoilage

$186,300

(10,800d $8.25) + (10,800 d $9.00)

Normal spoilage (1,080 units)

18,630

(1,080d $8.25) + (1,080d $9.00)

(A)

Total costs of good units completed and transferred out

204,930

(B)

Abnormal spoilage (360 units)

6,210

(360d $8.25) + (360d $9.00)

(C)

Work in process, ending (2,160 units):

32,400

(2,160d $8.25) + (1,620d $9.00)

(A) + (B) + (C)

Total costs accounted for

$243,540

$118,800 + $124,680

dEquivalent units of direct materials and conversion costs calculated in step 2 of Solution Exhibit 18-21A.

18-22 (35 min.) FIFO method, spoilage.

Required:

1. Do Exercise 18-21 using the FIFO method.

2. What are the managerial issues involved in selecting or reviewing the percentage of spoilage

considered normal? How would your answer to requirement 1 differ if all spoilage were viewed

as normal?

SOLUTION

1. Solution Exhibit 18-22, Panel A calculates equivalent units of work done in the current

period for direct materials and conversion costs.

Solution Exhibit 18-22, Panel B summarizes total costs to account for, calculates the costs

per equivalent unit for direct materials and conversion costs, and assigns total costs to units

completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in

ending work in process, using the FIFO method.

SOLUTION EXHIBIT 18-22

First-in, first-out (FIFO) Method of Process Costing with Spoilage,

La Croix Company for April 2014

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 2)

(Step 1)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out during current period:

From beginning work in process||

2,400 (100% −100%); 2,400 (100% − 50%)

Started and completed

8,400 100%; 8,400 100%

Normal spoilage*

1,080 100%; 1,080 100%

Abnormal spoilage†

360 100%; 360 100%

Work in process, ending‡

2,160 100%; 2,160 75%

Accounted for

Equivalent units of work done in current period

2,400

12,000

14,400

2,400

8,400#

1,080

360

2,160

____

14,400

0

8,400

1,080

360

2,160

12,000

1,200

8,400

1,080

360

1,620

___

12,660

||Degree of completion in this department: direct materials, 100%; conversion costs, 50%.

#10,800 physical units completed and transferred out minus 2,400 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion of normal spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Degree of completion of abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 75%.

PANEL B: Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs added in current period

Divided by equivalent units of work done in current period

Cost per equivalent unit

(Step 5) Assignment of costs:

Good units completed and transferred out (10,800 units)

$ 34,572

208,968

$243,540

$21,240

97,560

$118,800

$97,560

12,000

$ 8.13

$ 13,332

111,408

$124,740

$111,408

12,660

$ 8.80

Work in process, beginning (2,400 units)

Costs added to beg. work in process in current period

Total from beginning inventory before normal spoilage

Started and completed before normal spoilage (8,400 units)

Normal spoilage (1,080 units)

(A) Total costs of good units completed and transferred out

(B) Abnormal spoilage (360 units)

(C) Work in process, ending (2,160 units)

(A)+(B)+(C) Total costs accounted for

$ 34,572

10,560

45,132

142,212

18,284

205,628

6,095

31,817

$243,540

$21,240 + $13,332

(0a $8.13) + (1,200a $8.80)

(8,400a $8.13) + (8,400a $8.80)

(1,080a $8.13) + (1,080a $8.80)

(360a $8.13) + (360a $8.80)

(2,160a $8.13) + (1,620a $8.80)

$118,800 + $124,740

18-

11

a Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

2. The issues related to the determination of the percentage of spoilage considered normal

are similar to the factors discussed in Chapter 17 regarding the importance of verifying the

estimated completion percentages of ending work-in-process, especially with regard to

conversion costs. A supervisor who wants to show better operating income performance might

categorize more of the spoilage as normal, thereby reducing the amount that must be written off

against income as the loss from abnormal spoilage. Managers must stress the value of consistent

and unbiased estimates of normal spoilage percentages and drive home the importance of

pursuing ethical actions and reporting the correct income figures, regardless of the short-term

consequences of doing so.

In the above example, if all 1,440 units spoiled were considered normal spoilage, then

the cost of goods completed and transferred out would increase to $211,723 ($205,628 +

$6,095), while ending work-in-process would stay unchanged at $31,817. Of course, the $6,095

would no longer be written off as a period expense by the LaCroix facility in northeast Ohio.

18-23 (10 min.) Spoilage, journal entries.

Safeclear, Inc., is the leading manufacturer of automotive glass components such as windshields.

The company uses a process-costing system to account for its work-in-process inventories. When

Job 26, an order for windshields for the Chevy Malibu, was being processed, a piece of laminated

sheet glass was off-center in the cutting machine and two windshields were spoiled. Because this

problem occurs periodically, it is considered normal spoilage and is consequently recorded as an

overhead cost. Because this step comes first in the process of making the windshields, the only

costs incurred were $325 for direct materials. Assume the laminated glass cannot be sold, and its

cost has been recorded in work-in-process inventory.

Required:

Prepare the journal entries to record the spoilage incurred.