11-

1

CHAPTER 11

DECISION MAKING AND RELEVANT INFORMATION

11-1 The five steps in the decision process outlined in Exhibit 11-1 of the text are

1. Identify the problem and uncertainties.

2. Obtain information.

3. Make predictions about the future.

4. Make decisions by choosing among alternatives.

5. Implement the decision, evaluate performance, and learn.

11-2 Relevant costs are expected future costs that differ among the alternative courses of action

being considered. Historical costs are irrelevant because they are past costs and, therefore, cannot

differ among alternative future courses of action.

11-3 No. Relevant costs are defined as those expected future costs that differ among alternative

courses of action being considered. Thus, future costs that do not differ among the alternatives are

irrelevant to deciding which alternative to choose.

11-4 Quantitative factors are outcomes that are measured in numerical terms. Some quantitative

factors are financial––that is, they can be easily expressed in monetary terms. Direct materials are

an example of a quantitative financial factor. Other quantitative nonfinancial factors, such as on–

time flight arrivals, cannot be easily expressed in monetary terms. Qualitative factors are outcomes

that are difficult to measure accurately in numerical terms. An example is employee morale.

11-5 Two potential problems that should be avoided in relevant cost analysis are

(i) Do not assume all variable costs are relevant and all fixed costs are irrelevant.

(ii) Do not use unit-cost data directly. It can mislead decision makers because

a. it may include irrelevant costs, and

b. comparisons of unit costs computed at different output levels lead to erroneous

conclusions.

11-6 No. Some variable costs may not differ among the alternatives under consideration and,

hence, will be irrelevant. Some fixed costs may differ among the alternatives and, hence, will be

relevant.

11-7 No. Some of the total manufacturing cost per unit of a product may be fixed and, hence,

will not differ between the make and buy alternatives. These fixed costs are irrelevant to the make-

or-buy decision. The key comparison is between purchase costs and the costs that will be saved if

the company purchases the component parts from outside plus the additional benefits of using the

resources freed up in the next best alternative use (opportunity cost). Furthermore, managers

should consider nonfinancial factors such as quality and timely delivery when making outsourcing

decisions.

11-8 Opportunity cost is the contribution to income that is forgone (rejected) by not using a

limited resource in its next-best alternative use.

11-

2

11-9 No. When deciding on the quantity of inventory to buy, managers must consider both the

purchase cost per unit and the opportunity cost of funds invested in the inventory. For example,

the purchase cost per unit may be low when the quantity of inventory purchased is large, but the

benefit of the lower cost may be more than offset by the high opportunity cost of the funds invested

in acquiring and holding inventory.

11-10 No. Managers should aim to get the highest contribution margin per unit of the constraining

(that is, scarce, limiting, or critical) factor. The constraining factor is what restricts or limits the

production or sale of a given product (for example, availability of machine–hours).

11-11 No. For example, if the revenues that will be lost exceed the costs that will be saved, the

branch or business segment should not be shut down. Shutting down will only increase the loss.

Allocated costs and fixed costs that will not be saved are irrelevant to the shut-down decision.

11-12 Cost written off as depreciation is irrelevant when it pertains to a past cost such as

equipment already purchased. But the purchase cost of new equipment to be acquired in the future

that will then be written off as depreciation is often relevant.

11-13 No. Managers often favor the alternative that makes their performance look best so they

focus on the measures used in the performance-evaluation model. If the performance-evaluation

model does not emphasize maximizing operating income or minimizing costs, managers will most

likely not choose the alternative that maximizes operating income or minimizes costs.

11-14 The three steps in solving a linear programming problem are

(i) Determine the objective function.

(ii) Specify the constraints.

(iii) Compute the optimal solution.

11-15 The text outlines two methods of determining the optimal solution to an LP problem:

(i) Trial-and-error approach

(ii) Graphic approach

Most LP applications in practice use standard software packages that rely on the simplex method

to compute the optimal solution.

11-16 (20 min.) Disposal of assets.

Answer the following questions.

1. A company has an inventory of 1,250 assorted parts for a line of missiles that has been

discontinued. The inventory cost is $76,000. The parts can be either (a) remachined at total

additional costs of $26,500 and then sold for $33,500 or (b) sold as scrap for $2,500. Which

action is more profitable? Show your calculations.

2. A truck, costing $100,500 and uninsured, is wrecked its first day in use. It can be either (a)

disposed of for $18,000 cash and replaced with a similar truck costing $103,000 or (b) rebuilt

for $88,500 and thus be brand-new as far as operating characteristics and looks are concerned.

Which action is less costly? Show your calculations.

11-

3

SOLUTION

1. This is an unfortunate situation, yet the $76,000 costs are irrelevant regarding the decision

to remachine or scrap. The only relevant factors are the future revenues and future costs. By

ignoring the accumulated costs and deciding on the basis of expected future costs, operating

income will be maximized (or losses minimized). The difference in favor of remachining is $4,500:

(a) (b)

Remachine Scrap

Future revenues $33,500 $2,500

Deduct future costs 26,500 –

Operating income $ 7,000 $2,500

Difference in favor of remachining $4,500

2. This, too, is an unfortunate situation. But the $101,500 original cost is irrelevant to this

decision. The difference in relevant costs in favor of replacing is $3,500 as follows:

(a) (b)

Replace Rebuild

New truck $103,000 –

Deduct current disposal

price of existing truck 18,000 –

Rebuild existing truck – $88,500

$ 85,000 $88,500

Difference in favor of replacing $3,500

Note, here, that the current disposal price of $18,000 is relevant, but the original cost (or book

value, if the truck were not brand new) is irrelevant.

11-17 (20 min.) Relevant and irrelevant costs.

Answer the following questions.

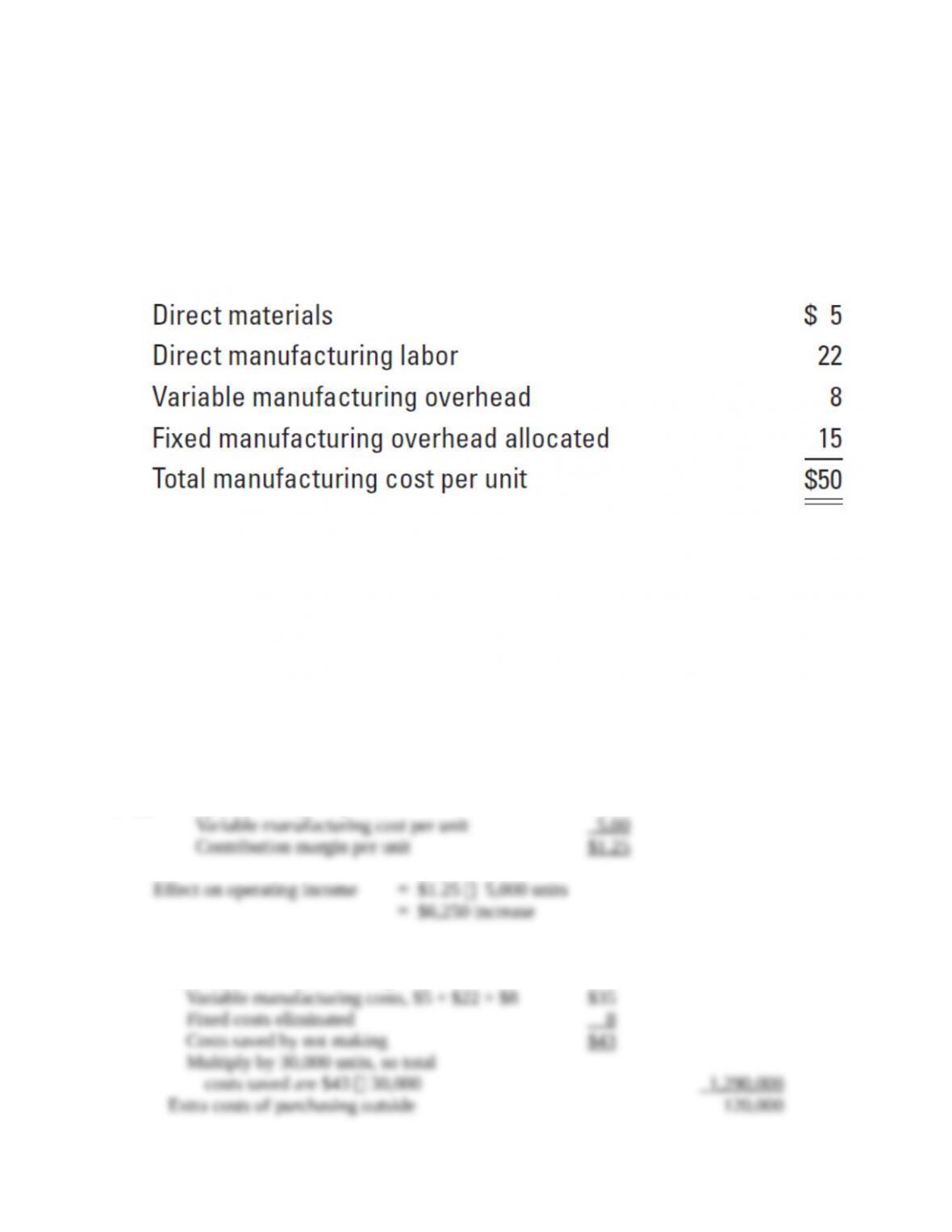

1. DeCesare Computers makes 5,200 units of a circuit board, CB76, at a cost of $280 each.

Variable cost per unit is $190 and fixed cost per unit is $90. Peach Electronics offers to supply

5,200 units of CB76 for $260. If DeCesare buys from Peach it will be able to save $10 per unit

in fixed costs but continue to incur the remaining $80 per unit. Should DeCesare accept Peach’s

offer? Explain.

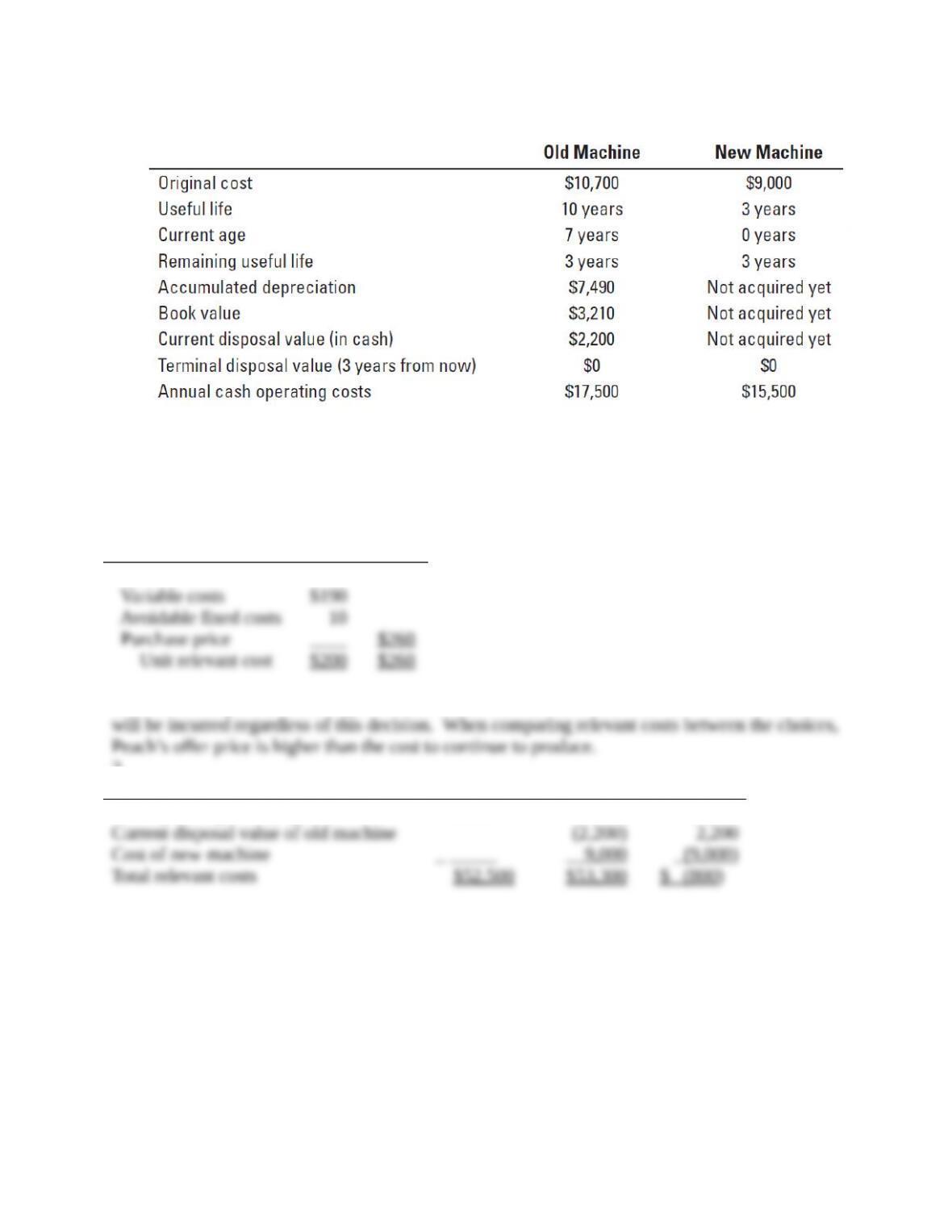

2. LN Manufacturing is deciding whether to keep or replace an old machine. It obtains the

following information:

11-

4

LN Manufacturing uses straight-line depreciation. Ignore the time value of money and income

taxes. Should LN Manufacturing replace the old machine? Explain.

SOLUTION

1.

Make

Buy

Relevant costs

Variable costs

$190

Avoidable fixed costs

10

Purchase price

____

$260

Unit relevant cost

$200

$260

DeCesare Computers should reject Peach’s offer. The $80 of fixed costs is irrelevant because it

will be incurred regardless of this decision. When comparing relevant costs between the choices,

Peach’s offer price is higher than the cost to continue to produce.

2.

Keep

Replace

Difference

Cash operating costs (3 years)

$52,500

$46,500

$6,000

Current disposal value of old machine

(2,200)

2,200

Cost of new machine

_ _____

9,000

(9,000)

Total relevant costs

$52,500

$53,300

$ (800)

LN Manufacturing should keep the old machine. The cost savings are less than the cost to purchase

the new machine.

11-18 (15 min.) Multiple choice.

(CPA) Choose the best answer.

1. The Dalton Company manufactures slippers and sells them at $12 a pair. Variable

manufacturing cost is $5.00 a pair, and allocated fixed manufacturing cost is $1.25 a pair. It

has enough idle capacity available to accept a one-time–only special order of 5,000 pairs of

11-

5

slippers at $6.25 a pair. Dalton will not incur any marketing costs as a result of the special

order. What would the effect on operating income be if the special order could be accepted

without affecting normal sales: (a) $0, (b) $6,250 increase, (c) $28,750 increase, or (d) $31,250

increase? Show your calculations.

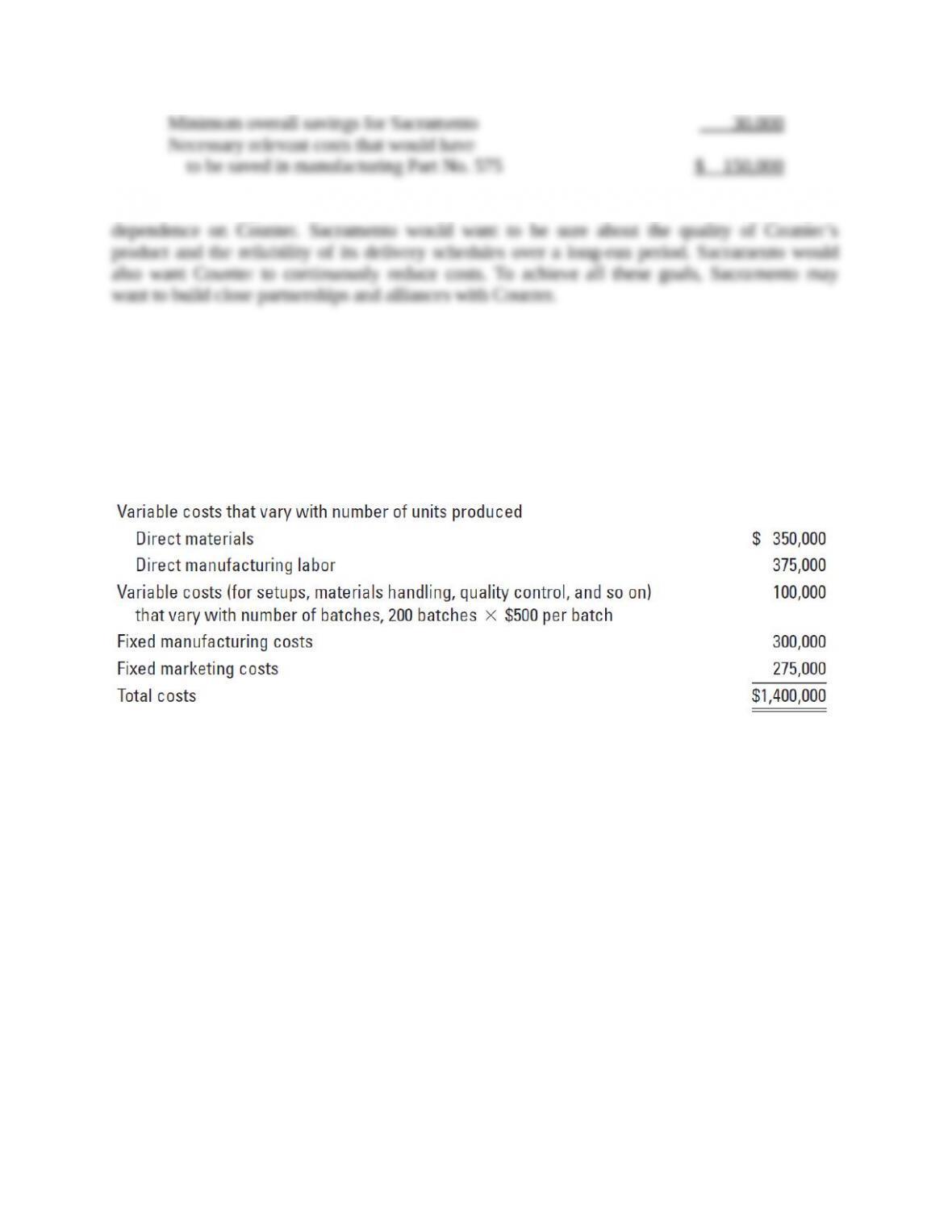

2. The Sacramento Company manufactures Part No. 498 for use in its production line. The

manufacturing cost per unit for 30,000 units of Part No. 498 is as follows:

The Counter Company has offered to sell 30,000 units of Part No. 498 to Sacramento for $47 per

unit. Sacramento will make the decision to buy the part from Counter if there is an overall savings

of at least $30,000 for Sacramento. If Sacramento accepts Counter’s offer, $8 per unit of the fixed

overhead allocated would be eliminated. Furthermore, Sacramento has determined that the

released facilities could be used to save relevant costs in the manufacture of Part No. 575. For

Sacramento to achieve an overall savings of $30,000, the amount of relevant costs that would have

to be saved by using the released facilities in the manufacture of Part No. 575 would be which of

the following: (a) $90,000, (b) $150,000, (c) $180,000, or (d) $210,000? Show your calculations.

What other factors might Sacramento consider before outsourcing to Counter?

SOLUTION

1. (b) Special order price per unit $6.25

Variable manufacturing cost per unit 5.00

Contribution margin per unit $1.25

Effect on operating income = $1.25 5,000 units

= $6,250 increase

2. (b) Costs of purchases, 30,000 units $47 $1,410,000

Total relevant costs of making:

Variable manufacturing costs, $5 + $22 + $8 $35

Fixed costs eliminated 8

Costs saved by not making $43

Multiply by 30,000 units, so total

costs saved are $43 30,000 1,290,000

Extra costs of purchasing outside 120,000

Minimum overall savings for Sacramento 30,000

11-

6

Necessary relevant costs that would have

to be saved in manufacturing Part No. 575 $ 150,000

Before outsourcing to Counter, Sacramento must consider the consequence of increasing its

dependence on Counter. Sacramento would want to be sure about the quality of Counter’s product

and the reliability of its delivery schedules over a long-run period. Sacramento would also want

Counter to continuously reduce costs. To achieve all these goals, Sacramento may want to build

close partnerships and alliances with Counter.

11-19 (30 min.) Special order, activity-based costing.

(CMA, adapted) The Gold Plus Company manufactures medals for winners of athletic events and

other contests. Its manufacturing plant has the capacity to produce 11,000 medals each month.

Current production and sales are 10,000 medals per month. The company normally charges $150

per medal. Cost information for the current activity level is as follows:

Gold Plus has just received a special one-time-only order for 1,000 medals at $100 per medal.

Accepting the special order would not affect the company’s regular business. Gold Plus makes

medals for its existing customers in batch sizes of 50 medals (200 batches × 50 medals per batch

= 10,000 medals). The special order requires Gold Plus to make the medals in 25 batches of 40

medals.

Required:

1. Should Gold Plus accept this special order? Show your calculations.

2. Suppose plant capacity were only 10,500 medals instead of 11,000 medals each month. The

special order must either be taken in full or be rejected completely. Should Gold Plus accept

the special order? Show your calculations.

3. As in requirement 1, assume that monthly capacity is 11,000 medals. Gold Plus is concerned

that if it accepts the special order, its existing customers will immediately demand a price

discount of $10 in the month in which the special order is being filled. They would argue that

Gold Plus’s capacity costs are now being spread over more units and that existing customers

should get the benefit of these lower costs. Should Gold Plus accept the special order under

these conditions? Show your calculations.

11-

7

SOLUTION

1. Direct materials cost per unit ($350,000 10,000 units) = $35 per unit

Direct manufacturing labor cost per unit ($375,000 10,000 units) = $37.50 per unit

Variable cost per batch = $500 per batch

Gold Plus’ operating income under the alternatives of accepting/rejecting the special order

are:

Without One-

Time Only

Special Order

10,000 Units

With One–

Time Only

Special Order

11,000 Units

Difference

1,000 Units

Revenues $1,500,000 $1,600,000 $100,000

Variable costs:

Direct materials 350,000 385,0001 35,000

Direct manufacturing labor 375,000 412,5002 37,500

Batch manufacturing costs 100,000 112,5003 12,500

Fixed costs:

Fixed manufacturing costs 300,000 300,000 ––

Fixed marketing costs 275,000 275,000 ––

Total costs 1,400,000 1,485,000 85,000

Operating income $ 100,000 $ 115,000 $ 15,000

1$350,000 + ($35 1,000 units) 2$375,000 + ($37.50 1,000 units) 3$100,000 + ($500 25 batches)

Alternatively, we could calculate the incremental revenue and the incremental costs of the

additional 1,000 units as follows:

Incremental revenue $100 1,000 $100,000

Incremental direct manufacturing costs $35 1,000 units 35,000

Incremental direct manufacturing costs $37.50 1,000 units 37,500

Incremental batch manufacturing costs $500 25 batches 12,500

Total incremental costs 85,000

Total incremental operating income from

accepting the special order $ 15,000

Gold Plus should accept the one-time–only special order if it has no long-term implications because

accepting the order increases Gold Plus’ operating income by $15,000.

If, however, accepting the special order would cause the regular customers to be

dissatisfied or to demand lower prices, then Gold Plus will have to trade off the $15,000 gain from

accepting the special order against the operating income it might lose from regular customers.

2. Gold Plus has a capacity of 10,500 medals. Therefore, if it accepts the special one-time

order of 1,000 medals, it can sell only 9,500 medals instead of the 10,000 medals that it currently

11-

8

sells to existing customers. That is, by accepting the special order, Gold Plus must forgo sales of

500 medals to its regular customers. Alternatively, Gold Plus can reject the special order and

continue to sell 9,500 medals to its regular customers.

Gold Plus’ operating income from selling 9,500 medals to regular customers and 1,000

medals under one-time special order follow:

Revenues (9,500 $150) + (1,000 $100) $1,525,000

Direct materials (9,500 $35) + (1,000 $35) 367,500

Direct manufacturing labor (9,500 $37.50) + (1,000 $37.50) 393,750

Batch manufacturing costs (1901 $500) + (25 $500) 107,500

Fixed manufacturing costs 300,000

Fixed marketing costs 275,000

Total costs 1,443,750

Operating income $ 81,250

1Gold Plus makes regular medals in batch sizes of 50. To produce 9,500 medals requires 190 (9,500 ÷ 50) batches.

Accepting the special order will result in a decrease in operating income of $18,750

($100,000 – $81,250). The special order should, therefore, be rejected.

A more direct approach would be to focus on the incremental effects––the benefits of

accepting the special order of 1,000 units versus the costs of selling 500 fewer units to regular

customers. Increase in operating income from the 1,000-unit special order equals $15,000

(requirement 1). The loss in operating income from selling 500 fewer units to regular customers

equals:

Lost revenue, $150 500 $(75,000)

Savings in direct materials costs, $35 500 17,500

Savings in direct manufacturing labor costs, $37.50 500 18,750

Savings in batch manufacturing costs, $500 10 5,000

Operating income lost $(33,750)

Accepting the special order will result in a decrease in operating income of $18,750 ($15,000 –

$33,750). The special order should, therefore, be rejected.

Even if operating income had increased by accepting the special order, Gold Plus should

consider the effect on its regular customers of accepting the special order. For example, would

selling 1,000 fewer medals to its regular customers cause these customers to find new suppliers

that might adversely impact Gold Plus’s business in the long run.

3. Gold Plus should not accept the special order.

Increase in operating income by selling 1,000 units

under the special order (requirement 1) $ 15,000

Operating income lost from existing customers ($10 10,000) (100,000)

Net effect on operating income of accepting special order $ (85,000)

11-

9

The special order should, therefore, be rejected.

11-20 (30 min.) Make versus buy, activity-based costing.

The Svenson Corporation manufactures cellular modems. It manufactures its own cellular modem

circuit boards (CMCB), an important part of the cellular modem. It reports the following cost

information about the costs of making CMCBs in 2014 and the expected costs in 2015:

Svenson manufactured 8,000 CMCBs in 2014 in 40 batches of 200 each. In 2015, Svenson

anticipates needing 10,000 CMCBs. The CMCBs would be produced in 80 batches of 125 each.

The Minton Corporation has approached Svenson about supplying CMCBs to Svenson in 2015

at $300 per CMCB on whatever delivery schedule Svenson wants.

Required:

1. Calculate the total expected manufacturing cost per unit of making CMCBs in 2015.

2. Suppose the capacity currently used to make CMCBs will become idle if Svenson purchases

CMCBs from Minton. On the basis of financial considerations alone, should Svenson make

CMCBs or buy them from Minton? Show your calculations.

3. Now suppose that if Svenson purchases CMCBs from Minton, its best alternative use of the

capacity currently used for CMCBs is to make and sell special circuit boards (CB3s) to the

Essex Corporation. Svenson estimates the following incremental revenues and costs from

CB3s:

On the basis of financial considerations alone, should Svenson make CMCBs or buy them from

Minton? Show your calculations.

11-

10

SOLUTION

1. The expected manufacturing cost per unit of CMCBs in 2015 is as follows:

Total

Manufacturing

Costs of CMCB

(1)

Manufacturing

Cost per Unit

(2) = (1) ÷ 10,000

Direct materials, $170 10,000

Direct manufacturing labor, $45 10,000

Variable batch manufacturing costs, $1,500 80

Fixed manufacturing costs

Avoidable fixed manufacturing costs

Unavoidable fixed manufacturing costs

Total manufacturing costs

$1,700,000

450,000

120,000

320,000

800,000

$3,390,000

$170

45

12

32

80

$339

2. The following table identifies the incremental costs in 2015 if Svenson (a) made CMCBs

and (b) purchased CMCBs from Minton.

Total

Incremental Costs

Per-Unit

Incremental Costs

Incremental Items

Make

Buy

Make

Buy

Cost of purchasing CMCBs from Minton

Direct materials

Direct manufacturing labor

Variable batch manufacturing costs

Avoidable fixed manufacturing costs

Total incremental costs

$1,700,000

450,000

120,000

320,000

$2,590,000

$3,000,000

$3,000,000

$170

45

12

32

$259

$300

$300

Difference in favor of making

$410,000

$41

Note that the opportunity cost of using capacity to make CMCBs is zero because Svenson would

keep this capacity idle if it purchases CMCBs from Minton.

Svenson should continue to manufacture the CMCBs internally because the incremental

costs to manufacture are $259 per unit compared to the $300 per unit that Minton has quoted. Note

that the unavoidable fixed manufacturing costs of $800,000 ($80 per unit) will continue to be

incurred whether Svenson makes or buys CMCBs. These are not incremental costs under either

the make or the buy alternative and, hence, are irrelevant.

3. Svenson should continue to make CMCBs. The simplest way to analyze this problem is to

recognize that Svenson would prefer to keep any excess capacity idle rather than use it to make

CB3s. Why? Because expected incremental future revenues from CB3s, $2,000,000, are less than

expected incremental future costs, $2,150,000. If Svenson keeps its capacity idle, we know from

requirement 2 that it should make CMCBs rather than buy them.

11-

11

An important point to note is that, because Svenson forgoes no contribution by not being

able to make and sell CB3s, the opportunity cost of using its facilities to make CMCBs is zero. It

is, therefore, not forgoing any profits by using the capacity to manufacture CMCBs. If it does not

manufacture CMCBs, rather than lose money on CB3s, Svenson will keep capacity idle.

A longer and more detailed approach is to use the total alternatives or opportunity cost

analyses shown in Exhibit 11-7 of the chapter.

Choices for Svenson

Relevant Items

Make CMCBs

and Do Not

Make CB3s

Buy CMCBs

and Make

CB3s, if Profitable

TOTAL-ALTERNATIVES APPROACH TO MAKE-OR-BUY DECISIONS

Total incremental costs of

making/buying CMCBs (from

requirement 2)

Because incremental future costs

exceed incremental future revenues

from CB3s, Svenson will make zero

CB3s even if it buys CMCBs from

Minton

Total relevant costs

$2,590,000

0

$2,590,000

$3,000,000

0

$3,000,000

Svenson will minimize manufacturing costs and maximize operating income by making CMCBs.

OPPORTUNITY-COST APPROACH TO MAKE-OR-BUY DECISIONS

Total incremental costs of

making/buying CMCBs (from

requirement 2)

$2,590,000

$3,000,000

Opportunity cost: profit contribution

forgone because capacity will not

be used to make CB3s

0*

0

Total relevant costs

$2,590,000

$3,000,000

*Opportunity cost is zero because Svenson does not give up anything by not making CB3s. Svenson is best off leaving

the capacity idle (rather than manufacturing and selling CB3s).