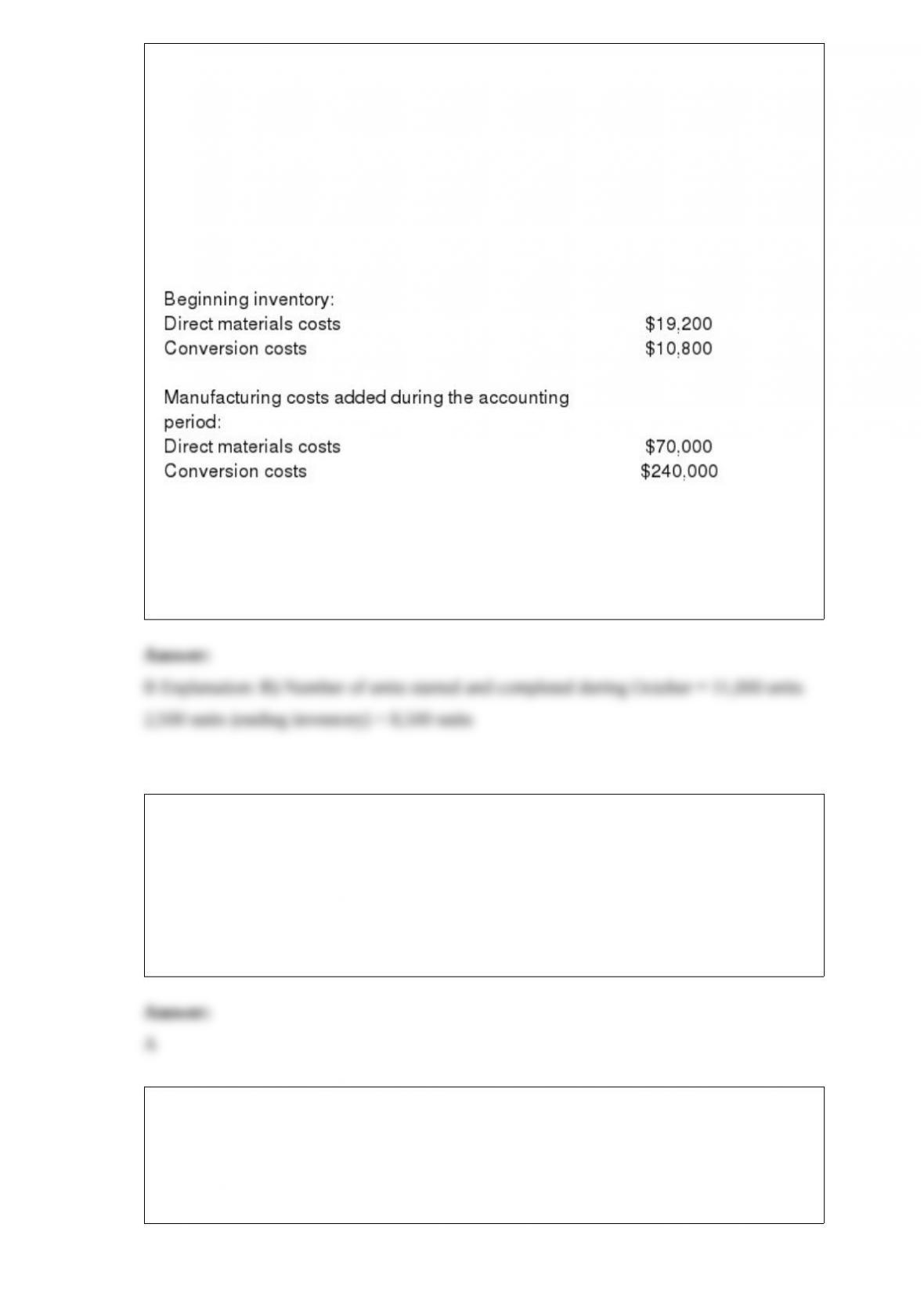

1) Jane Industries manufactures plastic toys. During October, Jane’s Fabrication

Department started work on 10,000 models. During the month, the company completed

11,000 models, and transferred them to the Distribution Department. The company

ended the month with 1,500 models in ending inventory. There were 2,500 models in

beginning inventory. All direct materials costs are added at the beginning of the

production cycle and conversion costs are added uniformly throughout the production

process. The FIFO method of process costing is being followed. Beginning work in

process was 25% complete as to conversion costs, while ending work in process was

50% complete as to conversion costs.

How many of the units that were started and completed during October?

A) 13,500

B) 8,500

C) 9,000

D) 10,000

2) When using a normal costing system, manufacturing overhead is allocated using the

________ manufacturing overhead rate and the ________ quantity of the allocation

base.

A) budgeted; actual

B) budgeted; budgeted

C) actual; budgeted

D) actual; actual

3) What is the operating income using variable costing?

A) $125,125

B) $85,125

C) $65,000

D) $60,125

4) Strategic Analysis of Profitability of Ransham Company:

Income Statement Amounts in 2014 Revenue and Cost Effects of Growth

Component in 2015 Revenue and Cost Effects of Price-Recovery Component in

2015 Cost Effect of Productivity Component in 2015 Income Statement Amounts

in 2015

Revenues ($) 34,000 10,000 F 1,000 U (b) (e)

Costs 23,500 (a) 500 U (c) 26,100

Operating income 10,500 5,500 F 1,500 U 2,400 F (d)

What is the cost effect of the productivity component (c)?

A) $0

B) $1,200 U

C) $900 F

D) $2,400 F

5) Crimson Services, Inc., employs 8 individuals. They are all paid $16.50 per hour.

How would total costs of personnel be classified?

A) variable cost

B) mixed cost

C) irrelevant cost

D) fixed cost

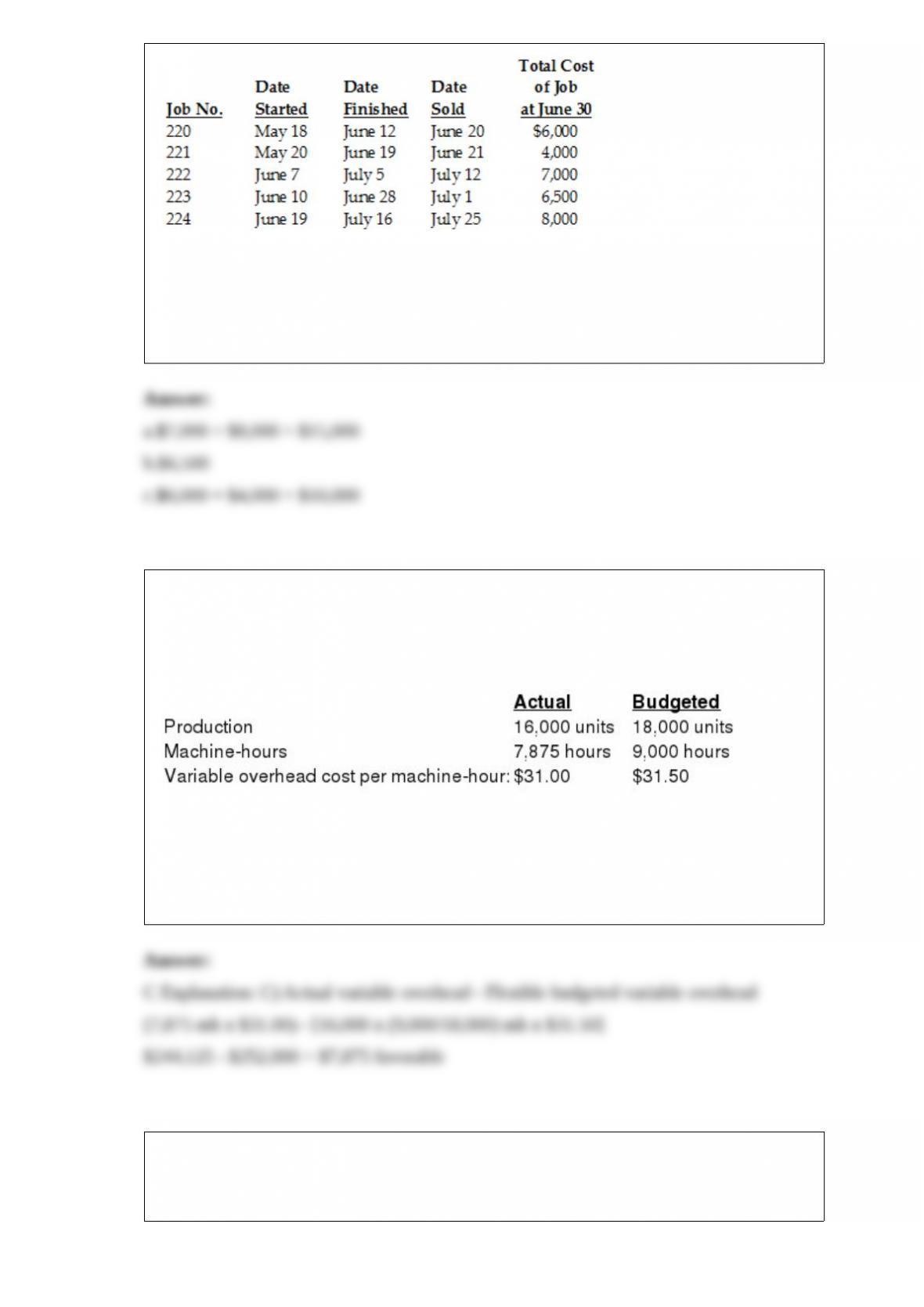

6) Job-cost records for Boucher Company contained the following data:

Required:

a.Compute WIP inventory at June 30

b.Compute finished goods inventory at June 30

c.Compute cost of goods sold for June

7) Russo Corporation manufactured 16,000 air conditioners during November. The

overhead cost-allocation base is $31.50 per machine-hour. The following variable

overhead data pertain to November:

What is the total variable overhead variance

A) $7,875 unfavorable

B) $3,937.50 f unfavorable

C) $7,875 favorable

D) $3,937.50 f favorable

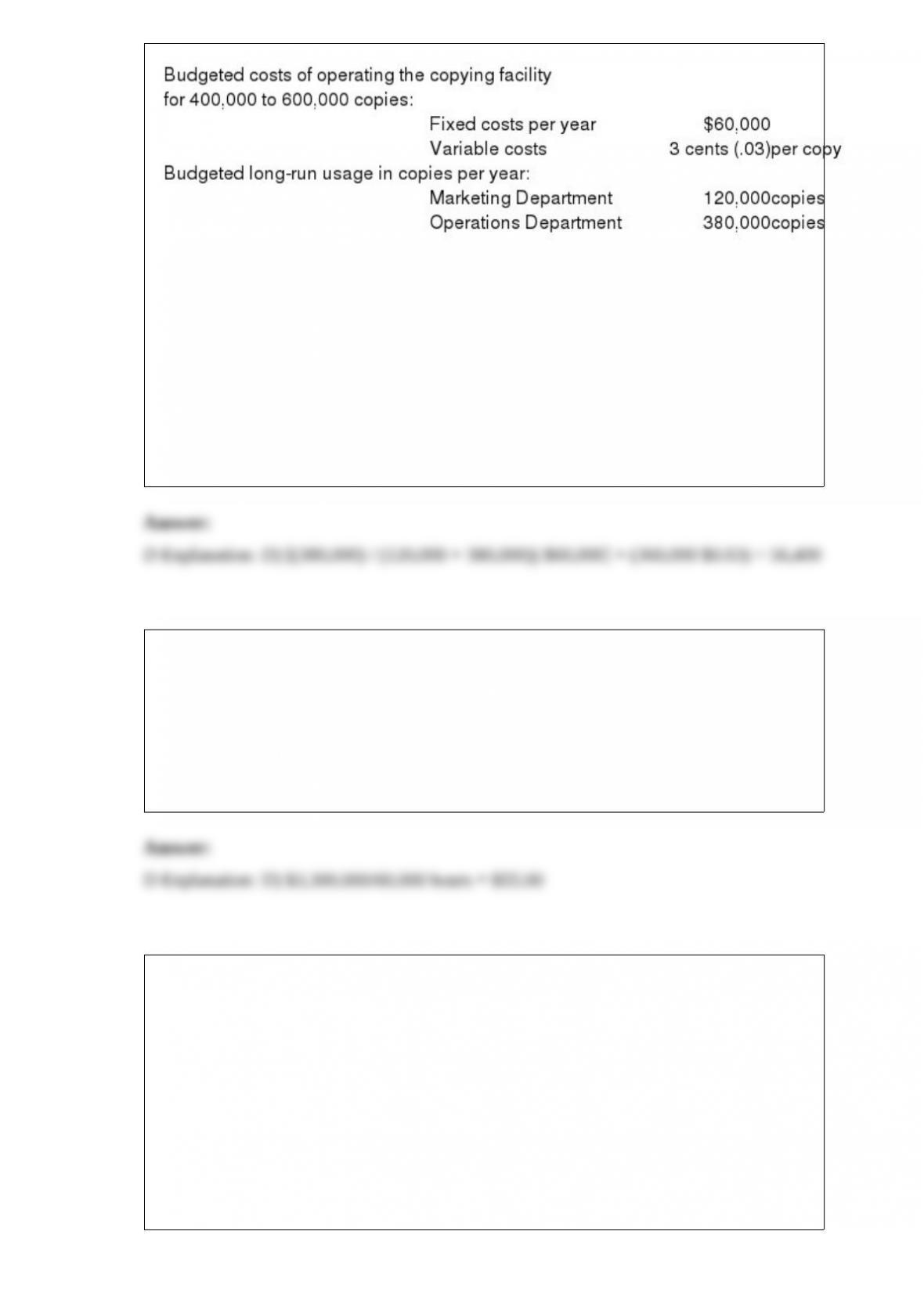

8) The Charmatz Corporation has a central copying facility. The copying facility has

only two users, the Marketing Department and the Operations Department. The

following data apply to the coming budget year:

Budgeted amounts are used to calculate the allocation rates.

Actual usage for the year by the Marketing Department was 80,000 copies and by the

Operations Department was 360,000 copies.

If a dual-rate cost-allocation method is used, what amount of copying facility costs will

be allocated to the Operations Department? Assume budgeted usage is used to allocate

fixed copying costs and actual usage is used to allocate variable copying costs.

A) $60,490

B) $59,890

C) $57,000

D) $56,400

9) Bernard Company’s budgeted manufacturing overhead is $3,300,000. Overhead is

allocated on the basis of direct labor hours. The budgeted direct labor hours for the

period are 60,000. What is the manufacturing overhead rate?

A) $47.00

B) $56.00

C) $75.00

D) $55.00

10) For 2014, Bakers Manufacturing uses machine-hours as the only overhead

cost-allocation base. The direct cost rate is $3.00 per unit. The selling price of the

product is $20.00. The estimated manufacturing overhead costs are $240,000 and

estimated 40,000 machine hours. The actual manufacturing overhead costs are

$300,000 and actual machine hours are 50,000.

What is the profit margin earned if each unit requires two machine-hours?

A) 53.33%

B) 33.33%

C) 66.67%

D) 58.73%