1) Transfer-pricing systems enable managers to focus on maximizing the performance

of their subunits.

2) Managers can always view a favorable variable overhead spending variance as

desirable.

3) Linking rewards to performance helps in good management performance.

4) Financing decisions deal with how to best use the limited resources of an

organization.

5) Stockout costs arise when an organization experiences an ability to deliver its goods

to its customers.

6) Additional insight can be gained by dividing the sales-volume variance into the

sales-mix variance and the sales-quantity variance.

7) Percentage of reworked products is an example of a nonfinancial measure of internal

business-process quality.

8) The sales department in any organization is usually a profit center.

9) Purchases of materials are credited to materials control.

10) Joint costing allocates the joint costs to the individual products that are eventually

sold.

11) If there are uniform cash flows, payback period is calculated by dividing net initial

investment by uniform increase in annual future cash flows.

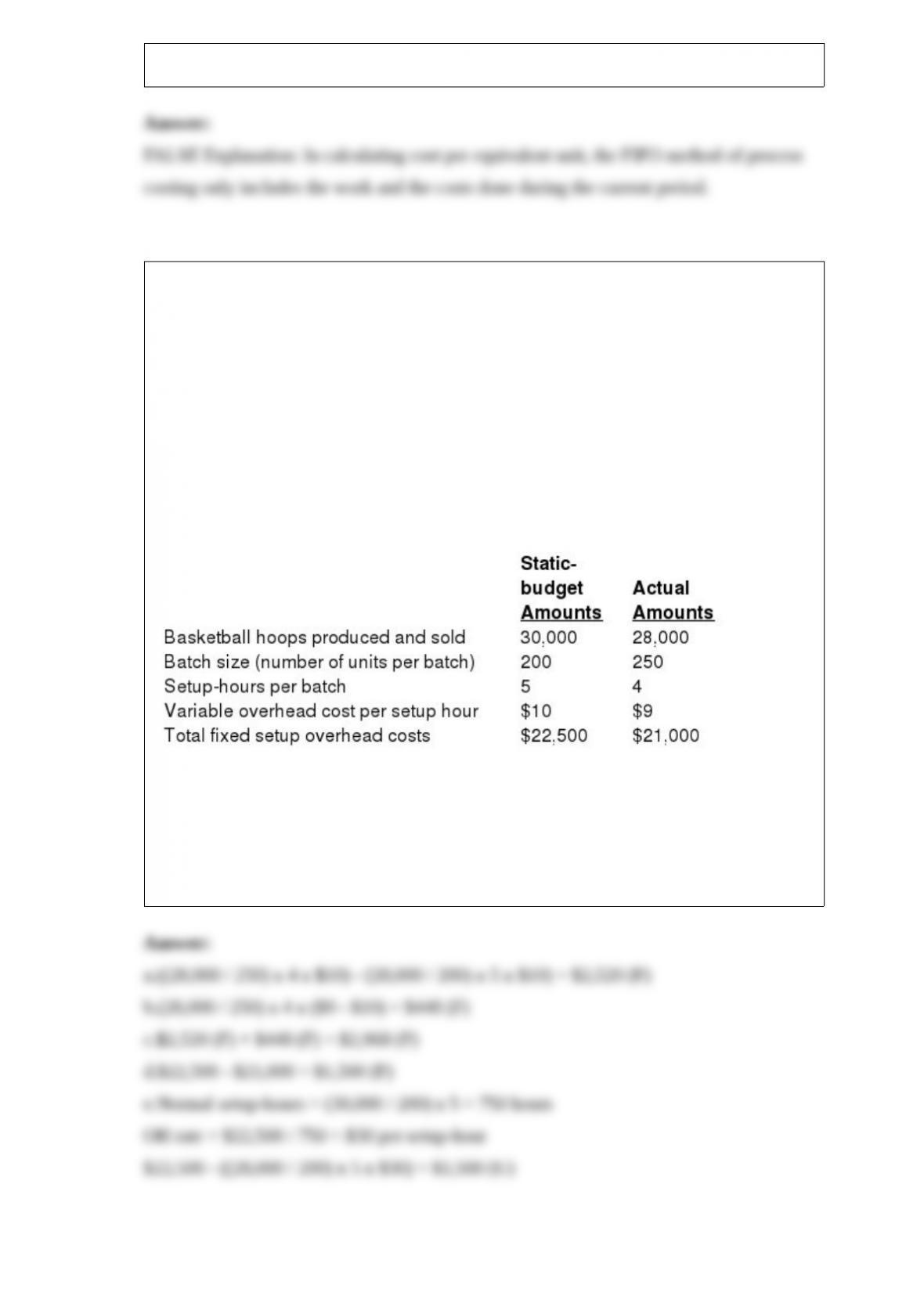

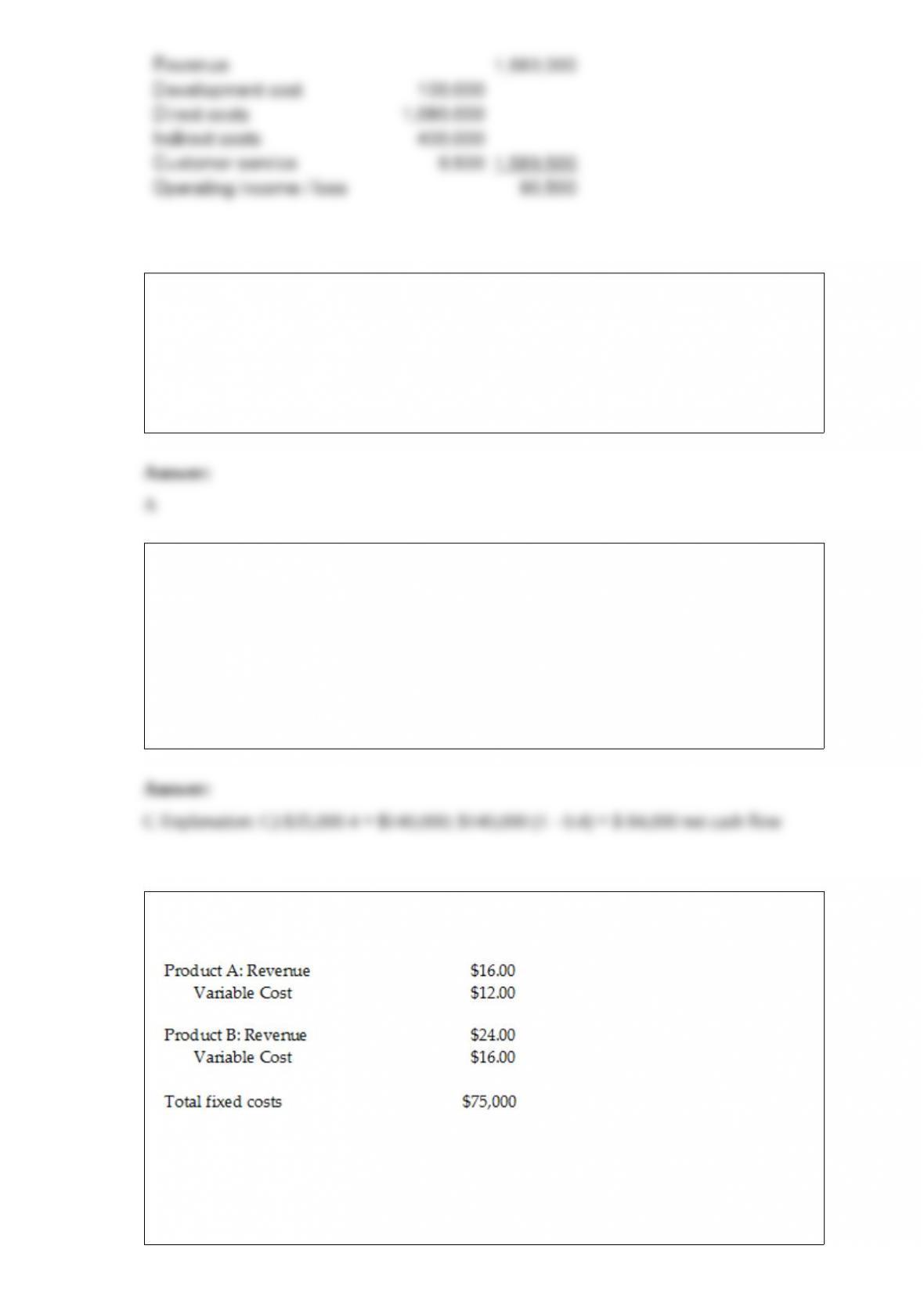

12) In calculating cost per equivalent unit, the FIFO method of process costing merges

the work and the costs of the beginning inventory with the work and the costs done

during the current period.

13) Casey Corporation produces a special line of basketball hoops. Casey Corporation

produces the hoops in batches. To manufacture a batch of the basketball hoops, Casey

Corporation must set up the machines and molds. Setup costs are batch-level costs

because they are associated with batches rather than individual units of products. A

separate Setup Department is responsible for setting up machines and molds for

different styles of basketball hoops.

Setup overhead costs consist of some costs that are variable and some costs that are

fixed with respect to the number of setup-hours. The following information pertains to

January 2005.

Required:

a.Calculate the efficiency variance for variable overhead setup costs.

b.Calculate the spending variance for variable overhead setup costs.

c.Calculate the flexible-budget variance for variable overhead setup costs.

d.Calculate the spending variance for fixed overhead setup costs.

e.Calculate the production-volume variance for fixed overhead setup costs.

14) When managers set and measure target levels of performance and feedback,

________.

A) the historical-cost-based accounting measures are usually adequate for evaluating

economic returns on new investments

B) the historical-cost ROIs cannot be used to evaluate current performance

C) the timing of feedback is not dependent on the sophistication of the organization’s

information technology

D) the timing of feedback depends on the specific level of management receiving the

feedback

15) The biggest advantage of using practical capacity to allocate costs is that it

________.

A) focuses the user’s division with the costs of overused capacity

B) never causes over or under-allocated overhead

C) burdens the user divisions with the costs of unused capacity

D) focuses management’s attention on unused capacity

16) The account analysis method estimates cost functions ________.

A) by classifying cost accounts as variable, fixed, or mixed based on qualitative

analysis

B) using time-and-motion studies

C) at a high cost, which renders it seldom used

D) in a manner that cannot be usefully combined with any other cost estimation

methods

17) For long-run pricing decisions, using stable prices has the advantage of ________.

A) minimizing the need to monitor competitor’s prices frequently

B) reducing the need to change cost structures frequently

C) reducing competition

D) helping to build buyer-seller relationships

18) Stark Corporation has two departments, Car Rental and Truck Rental. Central costs

may be allocated to the two departments in various ways.

If advertising expense of $112,500 is allocated on the basis of sales, the cost per cost

driver rate would be ________.

A) $0.15

B) $0.11

C) $0.10

D) $0.13

19) Jamal, Kareem, Rashid and Associates are in the process of evaluating its new

client services for the business consulting division.

Estate Planning, a new service, incurred $100,000 in development costs and employee

training.

The direct costs of providing this service, which is all labor, averages $27 per hour.

Other costs for this service are estimated at $400,000 per year.

The current program for estate planning is expected to last for two years. At that time, a

new law will be in place that will require new operating guidelines for the tax

consulting.

Customer service expenses average $95 per client, with each job lasting an average of

400 hours. The current staff expects to bill 40,000 hours for each of the two years the

program is in effect. Billing averages $42 per hour.

What is estimated life-cycle operating income for the first year?

A) $190,500

B) $81,000

C) $90,500

D) $181,000

20) A report that measures financial and nonfinancial performance measures for various

organization units in a single report is called a(n) ________.

A) balanced scorecard

B) financial report scorecard

C) goal-congruence report

D) investment success report

21) The Ambitz Corporation has an annual cash inflow from operations from its

investment in a capital asset of $35,000 each year for four years. The corporation’s

income tax rate is 40%. Calculate the total after-tax cash inflow from operations for

four years.

A) $ 140,000

B) $ 150,000

C) $ 84,000

D) $35,000

22) The following information is for the Jeffries Corporation:

What is the breakeven point, assuming the sales mix consists of three units of Product A

and one unit of Product B?

A) 10,000 units of A and 5,000 units of B

B) 11,250 units of A and 3,750 units of B

C) 12,000 units of A and 4,000 units of B

D) 4,000 units of A and 12,000 units of B

23) The payback method of capital budgeting approach to an investment decision

________.

A) considers cash flows over the life of the investment

B) highlights liquidity of the investment

C) considers time value of money

D) ignores the initial investment

24) Buildz Corp has been servicing the Production Casting Department for five years.

Beginning next year, the company is adding a Production Molding Department to

compliment the materials produced by the Production Casting Department. As a result,

data center costs are expected to increase from $800,000 per year to $1,000,000 per

year. The Production Molding Department will use 20% of the data center efforts.

Required:

a.Using the stand-alone cost-allocation method, identify the amount of data center cost

that will be allocated to Production Casting and the Production Molding Department

next year.

b.Using the incremental cost-allocation method, identify the amount of data center cost

that will be allocated to Production Casting and the Production Molding Department

next year.

25) Which of the following taxes does transfer pricing affect?

A) customs duties

B) dividend taxes

C) corporate taxes

D) property taxes

26) Assume a manufacturing company that has started production in the current year.

Which of the following would result in the highest profit being reported if the company

has 1,000 units of ending inventory?

A) throughput costing

B) variable costing

C) absorption costing

D) standard costing

27) The Conity Corporation has an Electric Mixer Division and an Electric Lamp

Division. Of a $13,000,000 bond issuance, the Electric Mixer Division used $9,100,000

and the Electric Lamp Division used $3,900,000 for expansion. Interest costs on the

bond totaled $975,000 for the year.

What amount of interest costs should be allocated to the Electric Lamp Division?

A) $292,500

B) $682,500

C) $2,730,000

D) $3,900,000

28) Which of the following is true of master budgets?

A) They include only financial aspects of a plan and exclude nonfinancial aspects.

B) They aid in coordinating what needs to be done to implement a plan.

C) They aid in quantifying the expectations of all stakeholders.

D) They must be administered rigidly after they are committed to.

29) Can a company identify unused capacity and, if so, how can unused capacity be

managed?

30) A machine has been identified as a bottleneck and the source of the constraint for a

manufacturing company that has multiple products and multiple machines. Discuss

ways the company can overcome the bottleneck.

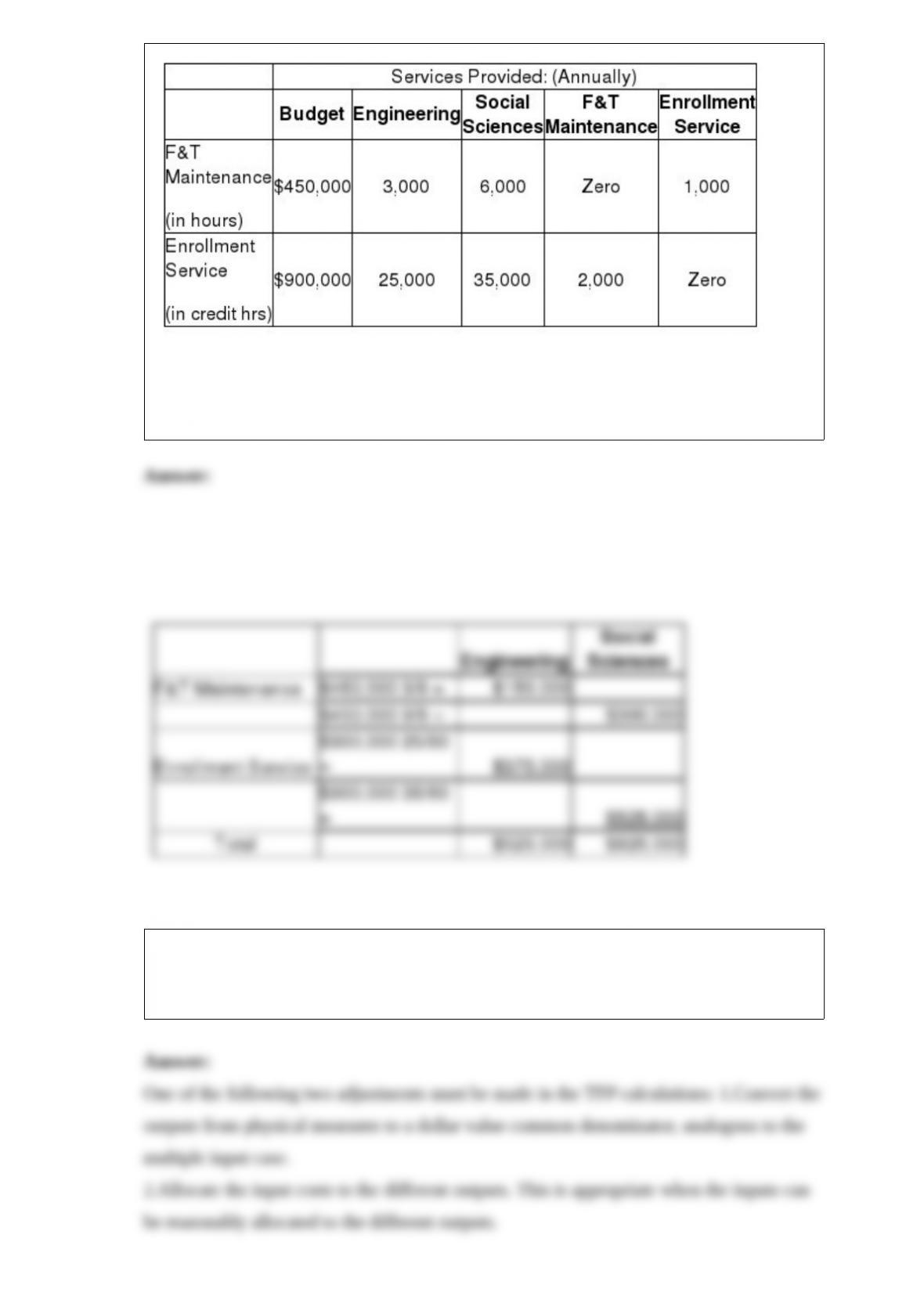

31) Tryst University offers only high-tech graduate-level programs. Tryst has two

principal operating departments, Engineering and Social Sciences, and two support

departments, Facility and Technology Maintenance and Enrollment Services. The base

used to allocate facility and technology maintenance is budgeted total maintenance

hours. The base used to allocate enrollment services is number of credit hours for a

department. The Facility and Technology Maintenance budget is $450,000, while the

Enrollment Services budget is $900,000. The following chart summarizes budgeted

amounts and allocation-base amounts used by each department:

Required:

Use the direct method to allocate support costs to each of the two principal operating

departments, Engineering and Social Sciences. Prepare a schedule showing the support

costs allocated to each department.

32) Total factor productivity (TFP) is easy to compute for a single-product company.

When dealing with a multiproduct company, one of two adjustments must be made.

What are these potential adjustments?

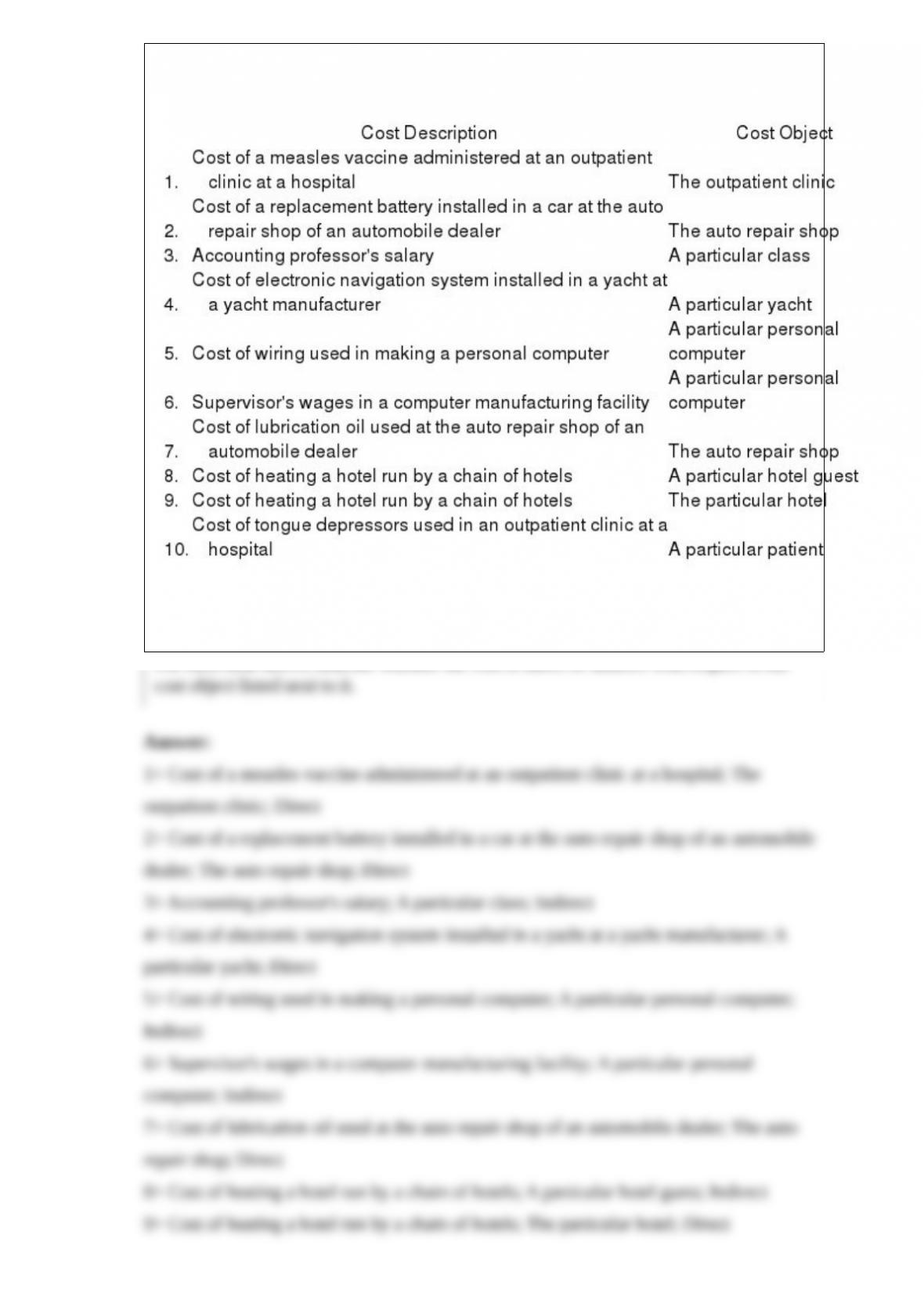

33) A number of costs are listed below.

Required:

For each item above, indicate whether the cost is direct or indirect with respect to the

cost object listed next to it.