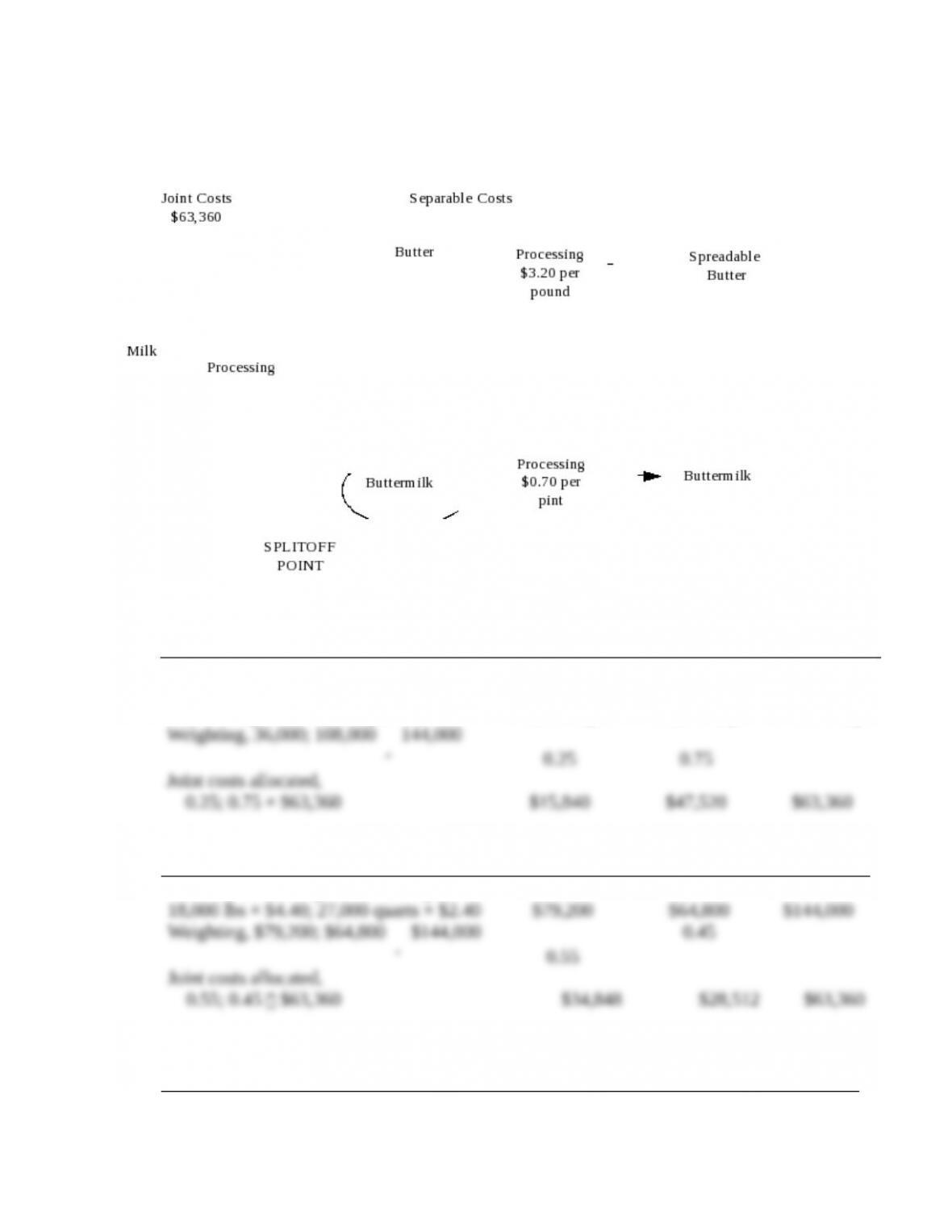

Weighting, $108,000; $64,800

$172,800

0.625

0.375

Joint costs allocated,

0.625; 0.375 $63,360

$39,600

$23,760

$63,360

d. Constant gross-margin percentage NRV method:

Step 1:

Final sales value of total production (see 1c.) $230,400

Deduct joint and separable costs ($63,360 + $57,600) 120,960

Gross margin $109,440

Gross-margin percentage ($109,440 ÷ $230,400) 47.50%

Step 2:

Butter

Buttermilk

Total

Final sales value of total production

$165,600

$64,800

$230,400

Deduct gross margin, using overall

gross-margin percentage of sales (47.50%)

78,660

30,780

109,440

Total production costs

86,940

34,020

120,960

Step 3:

Deduct separable costs

57,600

0

57,600

Joint costs allocated

$29,340

$34,020

$63,360

2. Advantages and disadvantages:

– Physical-Measure

Advantage: Low information needs. Only knowledge of joint cost and physical

distribution is needed.

Disadvantage: Allocation is unrelated to the revenue-generating ability of products.

– Sales Value at Splitoff

Advantage: Considers market value of products as basis for allocating joint cost. Relative

sales value serves as a proxy for relative benefit received by each product from the joint

cost.

Disadvantage: Uses selling price at the time of splitoff even if product is not sold by the

firm in that form. Selling price may not exist for product at splitoff.

– Net Realizable Value

Advantages: Allocates joint costs using ultimate net value of each product; applicable

when the option to process further exists

Disadvantages: High information needs; Makes assumptions about expected outcomes of

future processing decisions

Weighting, $375,000; $562,500

$937,500

0.40

0.60

Joint costs allocated, 0.40; 0.60 × $600,000

$240,000

$360,000

$600,000

Floor Mats

Car Mats

Rubber

Shreds

Total

Revenues, 25,000 × $12;

85,000 × $6

$300,000

$510,000

$30,100d

$840,100

Cost of goods sold:

Joint costs allocated, 0.40;

0.60 × $600,000

$240,000

$360,000

$600,000

Less: Ending inventory

( 48,000)e

( 33,600)f

( 81,600)

Cost of goods sold

$192,000

$326,400

$518,400

Gross margin

$108,000

$183,600

$30,100

$321,700

d 43,000 lbs × $0.70 per lb. = $30,100

e 6,250 × $240,000/31,250 = $48,000

f 8,750 × $360,000/93,750 = $33,600

3. The production method of accounting for the byproduct is only appropriate if The Mat

Place is positive they can sell the byproduct at the expected selling price. Moreover, The

Mat Place should view the byproduct’s contribution to the firm as material enough to find

it worthwhile to record and track any inventory that may arise. The sales method is

appropriate if either the disposition of the byproduct is unsure or the selling price is

unknown, or if the amounts involved are so negligible as to make it economically infeasible

for The Mat Place to keep track of byproduct inventories.

16-34 (15 min.) Byproduct-costing journal entries (continuation of 16–33).

The Mat Place’s accountant needs to record the information about the joint and byproducts in the

general journal, but is not sure what the entries should be. The company has hired you as a

consultant to help its accountant.

Required:

1. Show journal entries at the time of production and at the time of sale assuming the Mat Place

accounts for the byproduct using the production method.

2. Show journal entries at the time of production and at the time of sale assuming the Mat Place

accounts for the byproduct using the sales method.