$326,250 $293,625 $261,000

Panel C:

Rum Raisin

(112,500 × 0.20e) × $4.00

22,500 × $4.00

(112,500 × 0.20f) × $4.00

22,500 × $4.00

(100,000 × 0.20f) × $4.00

20,000 × $4.00

$90,000 $90,000 $80,000

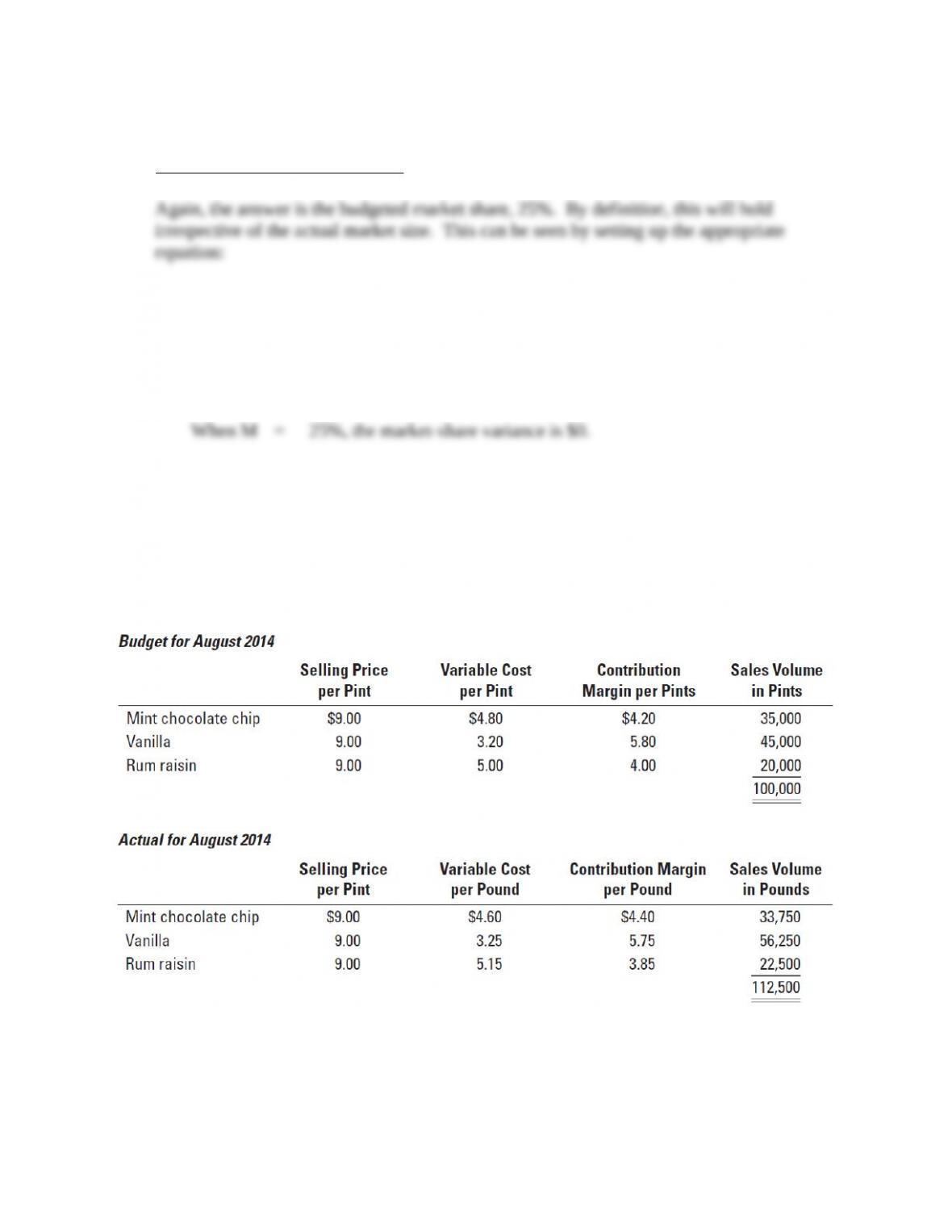

F = favorable effect on operating income; U = unfavorable effect on operating income.

Actual Sales Mix:

aMint choc. chip = 33,750 ÷ 112,500 = 30%

cVanilla = 56,250 ÷ 112,500 = 50%

eRum raisin = 22,500 ÷ 112,500 = 20%

Budgeted Sales Mix:

bMint choc. chip = 35,000 ÷ 100,000 = 35%

dVanilla = 45,000 ÷ 100,000 = 45%

f Rum raisin = 20,000 ÷ 100,000 = 20%

SOLUTION EXHIBIT 14-38 (Cont’d.)

Columnar Presentation of Sales-Volume, Sales-Quantity, and Sales-Mix Variances

for The Robin’s Basket

Flexible Budget:

Actual Pints of

All Flavors Sold

× Actual Sales Mix

× Budgeted Contribution

Margin per Pint

(1)

Actual Pounds of

All Cookies Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pound

(2)

Static Budget:

Budgeted Pounds of

All Cookies Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pound

(3)

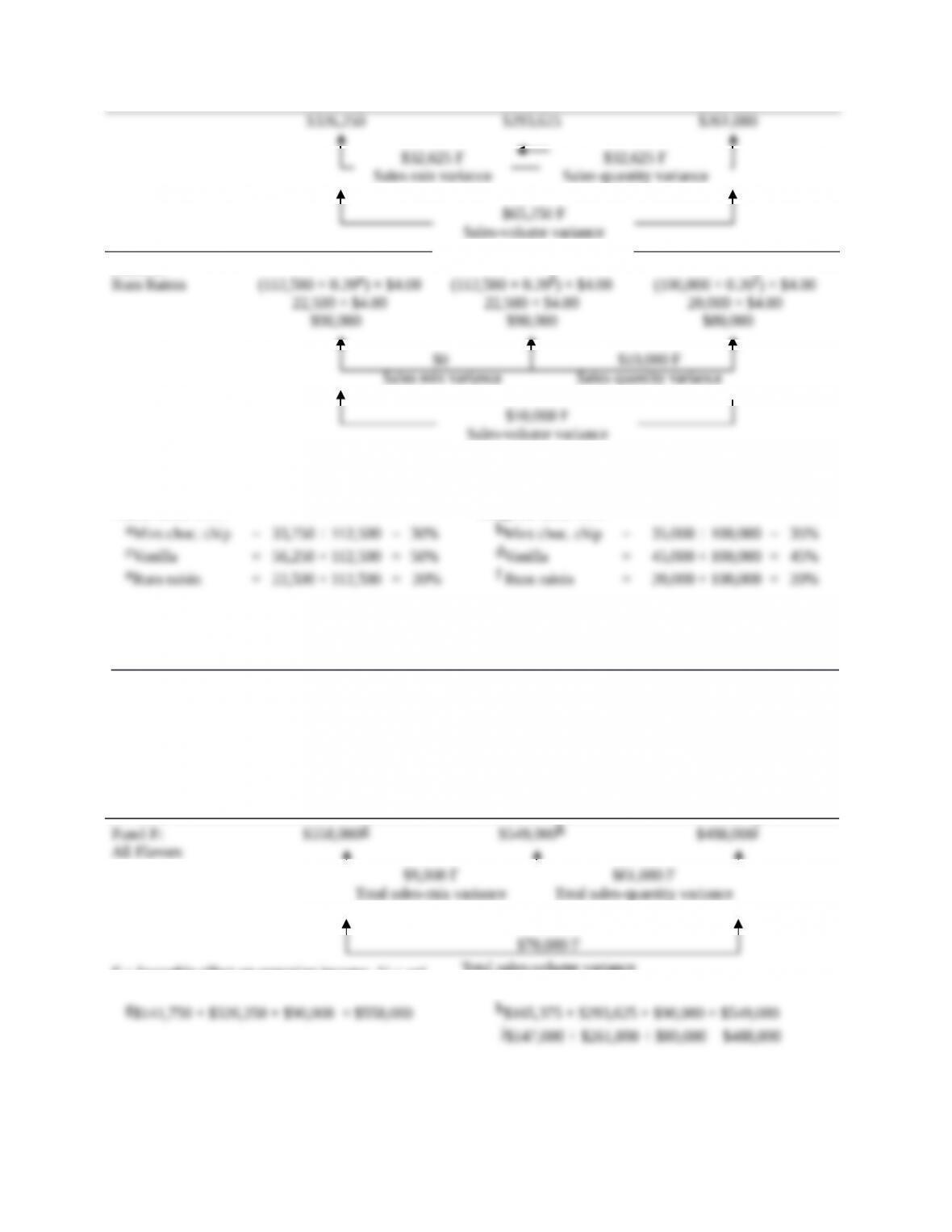

Panel F: $558,000g $549,000h $488,000j

All Flavors

F = favorable effect on operating income; U = unfavorable effect on operating income.

g$141,750 + $326,250 + $90,000 = $558,000

h$165,375 + $293,625 + $90,000 = $549,000

j$147,000 + $261,000 + $80,000 = $488,000

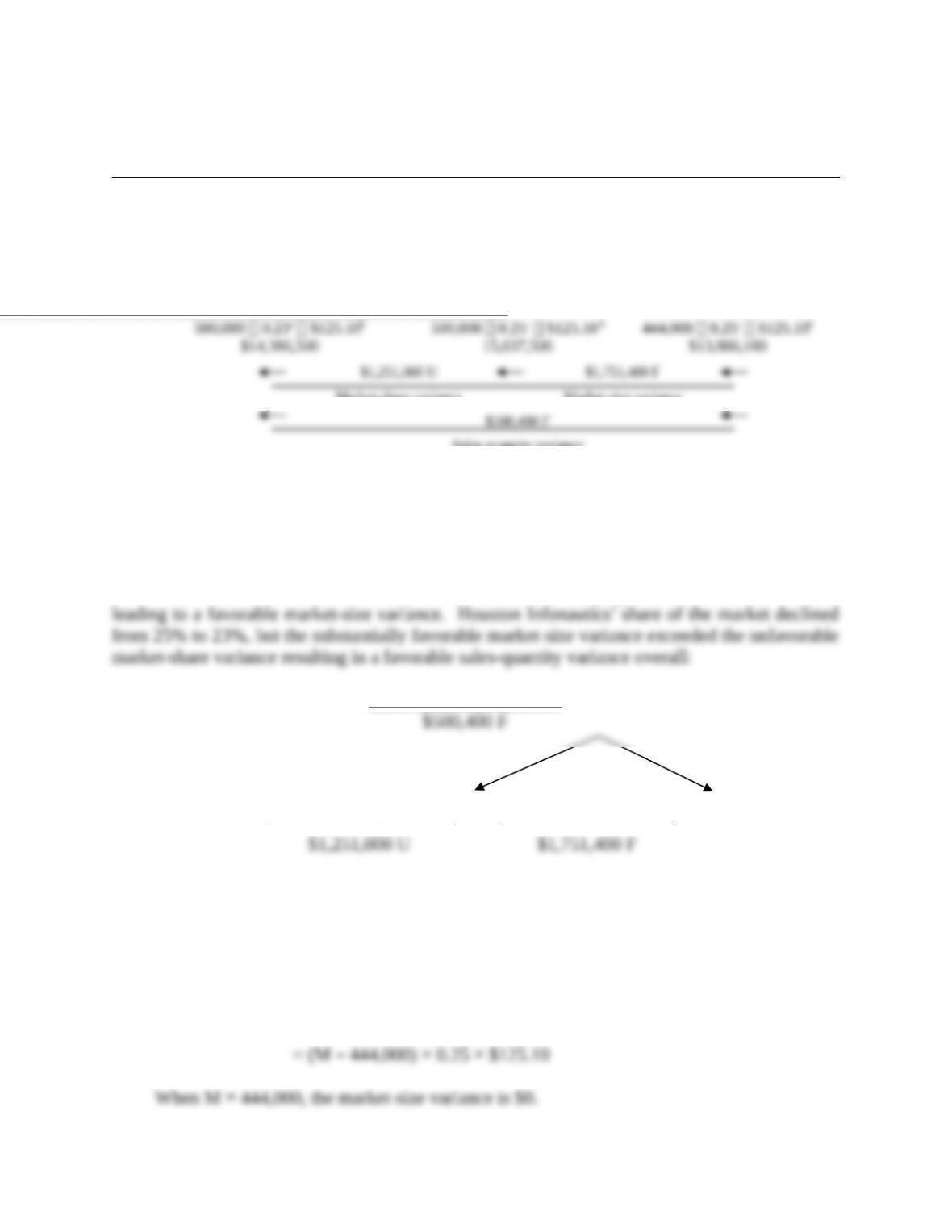

$32,625 F

Sales-mix variance

$32,625 F

Sales-quantity variance

$65,250 F

Sales-volume variance

$10,000 F

Sales-quantity variance

$0

Sales-mix variance

$10,000 F

Sales-volume variance

$70,000 F

Total sales-volume variance

$61,000 F

Total sales-quantity variance

$9,000 F

Total sales-mix variance

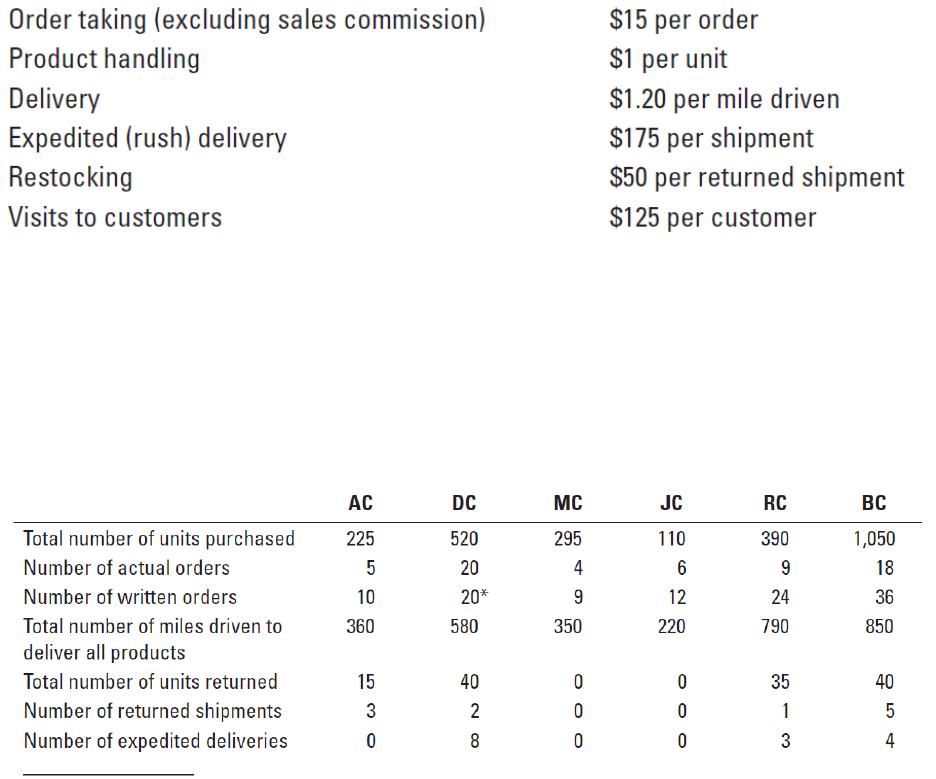

Visits to customers

125

125

125

125

125

125

Sales commissions

$10× 10; 20; 9; 12; 24; 36

100

200

90

120

240

360

Total customer-level operating costs

1,182

3,341

1,065

799

2,638

4,045

Customer-level operating income

$1,338

$ 2,419

$2,475

$ 521

$ 1,622

$ 8,075

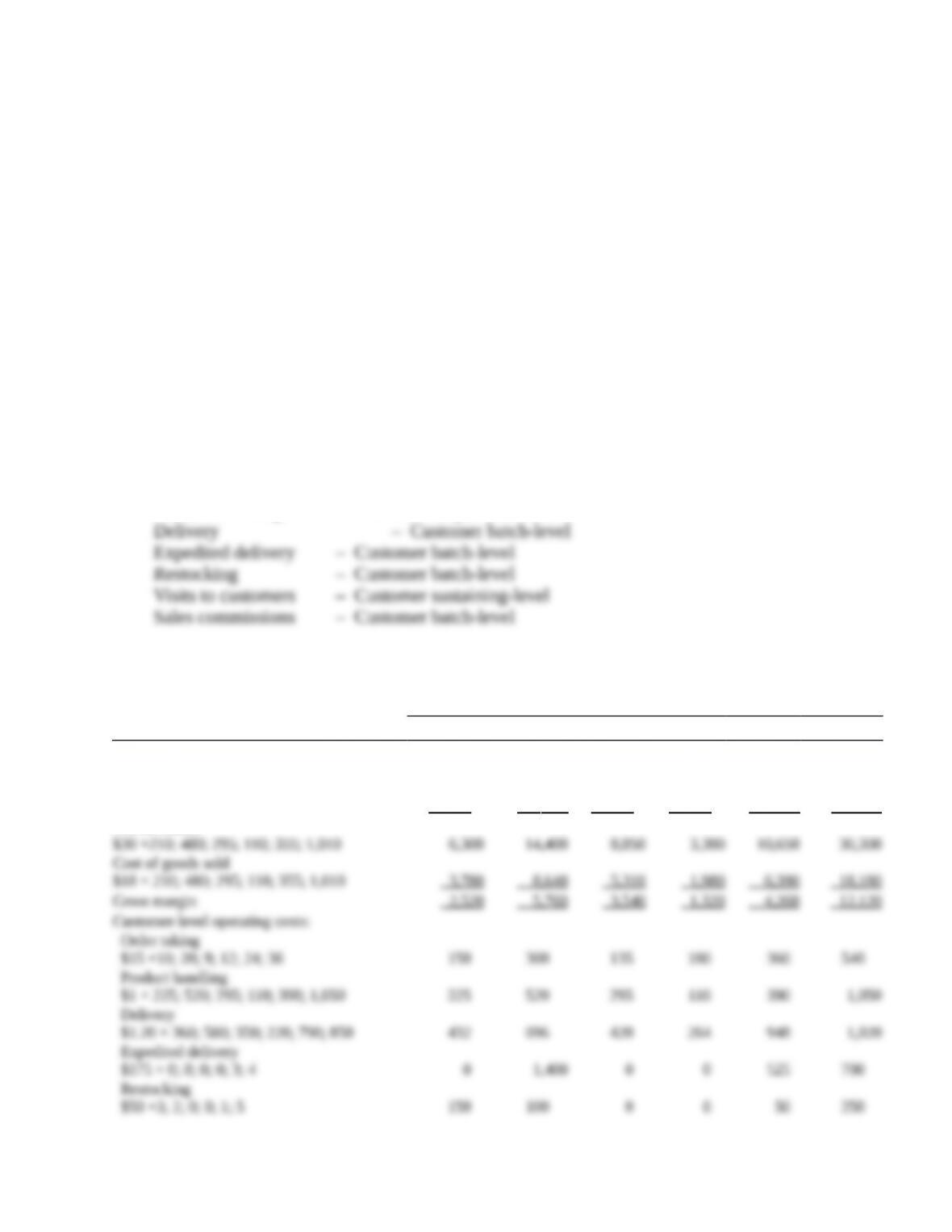

3. Customer level operating income based on actual order costs:

Customers

AC

DC

MC

JC

RC

BC

Revenues

$30 × 225; 520; 295; 110; 390; 1,050

$6,750

$15,600

$8,850

$3,300

$11,700

$31,500

Less: Returns

$30 ×15; 40; 0; 0; 35; 40

450

1,200

0

0

1,050

1,200

Net Revenues

$30 ×210; 480; 295; 110; 355; 1,010

6,300

14,400

8,850

3,300

10,650

30,300

Cost of goods sold

$18 × 210; 480; 295; 110; 355; 1,010

3,780

8,640

5,310

1,980

6,390

18,180

Gross margin

2,520

5,760

3,540

1,320

4,260

12,120

Customer-level operating costs:

Order taking

$8 ×10; $15 × 20; $8 × 9; $8 × 12; $8 × 24;

$8 × 36

80

300

72

96

192

288

Product handling

$1 × 225; 520; 295; 110; 390; 1,050

225

520

295

110

390

1,050

Delivery

$1.20 × 360; 580; 350; 220; 790; 850

432

696

420

264

948

1,020

Expedited delivery

$175 × 0; 8; 0; 0; 3; 4

0

1,400

0

0

525

700

Restocking

$50 ×3; 2; 0; 0; 1; 5

150

100

0

0

50

250

Visits to customers

125

125

125

125

125

125

Sales commissions

$10× 10; 20; 9; 12; 24; 36

100

200

90

120

240

360

Total customer-level operating costs

1,112

3,341

1,002

715

2,470

3,793

Customer-level operating income

$1,408

$ 2,419

$2,538

$ 605

$ 1,790

$ 8,327

Comparing the answers in requirements 2 and 3, it appears that operating income is higher than

expected, so the management of KC Corporation would be very pleased with the performance of

the salespeople for reducing order costs. Except for DC, all of the customers are more profitable

than originally reported.

Customer-level operating income based on actual orders and adjusted commissions

Customers

AC

DC

MC

JC

RC

BC

Revenues

$30 × 225; 520; 295; 110; 390; 1,050

$6,750

$15,600

$8,850

$3,300

$11,700

$31,500

Less: Returns

450

1,200

0

0

1,050

1,200

$30 ×15; 40; 0; 0; 35; 40

Net Revenues

$30 ×210; 480; 295; 110; 355; 1,010

6,300

14,400

8,850

3,300

10,650

30,300

Cost of goods sold

$18 × 210; 480; 295; 110; 355; 1,010

3,780

8,640

5,310

1,980

6,390

18,180

Gross margin

2,520

5,760

3,540

1,320

4,260

12,120

Customer-level operating costs:

Order taking

$15 ×5; 20; 4; 6; 9; 18

75

300

60

90

135

270

Product handling

$1 × 225; 520; 295; 110; 390; 1,050

225

520

295

110

390

1,050

Delivery

$1.20 × 360; 580; 350; 220; 790; 850

432

696

420

264

948

1,020

Expedited delivery

$175 × 0; 8; 0; 0; 3; 4

0

1,400

0

0

525

700

Restocking

$50 ×3; 2; 0; 0; 1; 5

150

100

0

0

50

250

Visits to customers

125

125

125

125

125

125

Sales commissions

$10× 5; 20; 4; 6; 9; 18

50

200

40

60

90

180

Total customer-level operating costs

1,057

3,341

940

649

2,263

3,595

Customer-level operating income

$1,463

$ 2,419

$2,600

$ 671

$ 1,997

$ 8,525

5. The behavior of the salespeople is costing KC Corporation $588 in profit (the difference

between the incomes in requirements 3 and 4.) Although management thinks the salespeople

are saving money based on the budgeted order costs, in reality they are costing the firm money

by increasing the costs of orders ($1,028 in requirement 3 versus $930 in requirement 4) and

at the same time increasing their sales commissions ($1,110 in requirement 3 versus $620 in

requirement 4). This is not ethical.

KC Corporation needs to change the structure of the sales commission, possibly linking

commissions to the overall units sold rather than on number of orders.

Some students might argue that the amount is not material, but in matters of ethics be wary of

the slippery slope. Most organizations do not stand for any deviation from ethical principles,

regardless of the amount involved. Students can engage in an interesting debate around this

point.