Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

21-1

1. Modernizing alternative:

Present Value

Discount Factors Net Cash Present

Year At 10% Flow Value

Jan. 1, 2015 1.000 $(36,800000) $(36,800,000)

Dec. 31, 2015 0.909 10,432,500 9,483,143

Dec. 31, 2016 0.826 11,700000 9,664,200

Dec. 31, 2017 0.751 12,967,500 9,738,593

Dec. 31, 2018 0.683 14,235,000 9,722,505

Dec. 31, 2019 0.621 15,502,500 9,627,053

Dec. 31, 2020 0.564 16,770000 9,458,280

Dec. 31, 2021 0.513 25,037,500 12,844,238

Total $33,738,010

Replace Alternative:

Present Value

Discount Factors Net Cash Present

Year At 10% Flow Value

Jan. 1, 2015 1.000 $(57,400000) $(57,400,000)

Dec. 31, 2015 0.909 15,515000 14,103,135

Dec. 31, 2016 0.826 17,400000 14,372,400

Dec. 31, 2017 0.751 19,285000 14,483,035

Dec. 31, 2018 0.683 21,170000 14,459,110

Dec. 31, 2019 0.621 23,055000 14,317,155

Dec. 31, 2020 0.564 24,940000 14,066,160

Dec. 31, 2021 0.513 43,825,000 22,482,225

Total $50,883,220

4. Using the payback period, the modernize alternative is preferred to the replace alternative.

On the other hand, the replace alternative has a significantly higher NPV than the modernize

alternative and so should be preferred. Of course, the NPV amounts are based on best estimates of

cash flows going out into the future. Clean Chips should examine the sensitivity of the NPV

amounts to variations in the estimates.

Nonfinancial qualitative factors should be considered. These could include the quality of

the prototypes produced by the modernize and replace alternatives. These alternatives may differ

in capacity and their ability to meet surges in demand beyond the estimated amounts. The

alternatives may also differ in how workers increase their shop floor-capabilities. Such differences

could provide labor force externalities that can be the source of future benefits to Clean Chips.

21-2

21-30 (40 min.) Equipment replacement, income taxes (continuation of 21-29).

Assume the same facts as in Problem 21-29, except that the plant is located in Austin, Texas. Clean

Chips has no special waiver on income taxes. It pays a 30% tax rate on all income. Proceeds from

sales of equipment above book value are taxed at the same 30% rate.

Required:

1. Sketch the after-tax cash inflows and outflows of the modernize and replace alternatives over

the 2015–2021 period.

2. Calculate the net present value of the modernize and replace alternatives.

3. Suppose Clean Chips is planning to build several more plants. It wants to have the most

advantageous tax position possible. Clean Chips has been approached by Spain, Malaysia, and

Australia to construct plants in their countries. Use the data in Problem 21-29 and this problem

to briefly describe in qualitative terms the income tax features that would be advantageous to

Clean Chips.

SOLUTION

1. & 2. Income tax rate = 30%

Modernize Alternative

Annual depreciation:

$36,800000 7 years = $5257143 a year.

Income tax cash savings from annual depreciation deductions:

$5257143 0.3 = $1577143 a year.

Terminal disposal of equipment = $7000000.

After-tax cash flow from terminal disposal of equipment:

$7000000 0.70 = $4,900000.

The NPV components are:

a. Initial investment: NPV

Jan. 1, 2015 $(36,800000) 1.000 $(36,800000)

b. Annual after-tax cash flow from operations

(excluding depreciation):

Dec. 31, 2015 10,432500 0.70 0.909 $6,638,200

2016 11,700000 0.70 0.826 6,764,940

2017 12,967,500 0.70 0.751 6,817,015

2018 14,235000 0.70 0.683 6,805,754

2019 15,502000 0.70 0.621 6,738,937

2020 16,770000 0.70 0.564 6,620,796

2021 18,037000 0.70 0.513 6,477,266

21-3

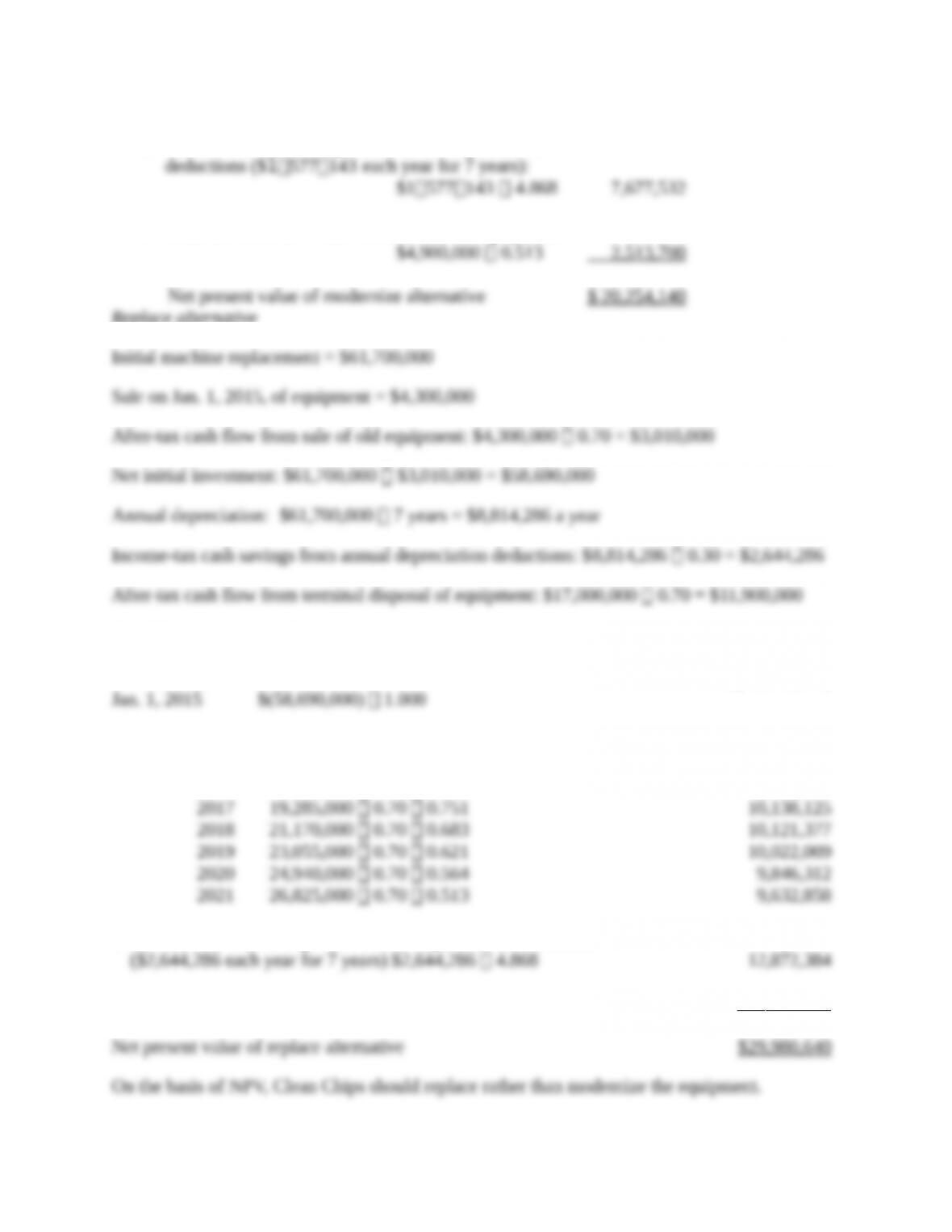

c. Income tax cash savings from annual depreciation

deductions ($1577143 each year for 7 years):

$1577143 4.868 7,677,532

d. After-tax cash flow from terminal sale of equipment:

$4,900,000 0.513 2,513,700

Net present value of modernize alternative $ 20,254,140

Replace alternative

Initial machine replacement = $61,700,000

Sale on Jan. 1, 2015, of equipment = $4,300,000

After-tax cash flow from sale of old equipment: $4,300,000 0.70 = $3,010,000

Net initial investment: $61,700,000 − $3,010,000 = $58,690,000

Annual depreciation: $61,700,000 7 years = $8,814,286 a year

Income-tax cash savings from annual depreciation deductions: $8,814,286 0.30 = $2,644,286

After-tax cash flow from terminal disposal of equipment: $17,000,000 0.70 = $11,900,000

The NPV components of the replace alternative are:

a. Net initial investment

Jan. 1, 2015 $(58,690,000) 1.000

$(58,690,000)

b. Annual after-tax cash flow from operations (excluding depreciation)

Dec. 31,

2015

$15,515,000 0.70 0.909

$ 9,872,195

2016

17,400,000 0.70 0.826

10,060,680

2017

19,285,000 0.70 0.751

10,138,125

2018

21,170,000 0.70 0.683

10,121,377

2019

23,055,000 0.70 0.621

10,022,009

2020

24,940,000 0.70 0.564

9,846,312

2021

26,825,000 0.70 0.513

9,632,858

c. Income tax cash savings from annual depreciation deductions

($2,644,286 each year for 7 years) $2,644,286 4.868

12,872,384

d. After-tax cash flow from terminal sale of equipment, $11,900,000 0.513

6,104,700

Net present value of replace alternative

$29,980,640

On the basis of NPV, Clean Chips should replace rather than modernize the equipment.

21-4

3. Clean Chips would prefer to:

a. have lower tax rates,

b. have revenue exempt from taxation,

c. recognize taxable revenues in later years rather than earlier years,

d. recognize taxable cost deductions greater than actual outlay costs, and

e. recognize cost deductions in earlier years rather than later years (including

accelerated amounts in earlier years).

21-31 (20 min.) DCF, sensitivity analysis, no income taxes.

(CMA, adapted) Invigor Corporation is an international manufacturer of fragrances for women.

Management at Invigor is considering expanding the product line to men’s fragrances. From the

best estimates of the marketing and production managers, annual sales (all for cash) for this new

line are 1,200,000 units at $50 per unit; cash variable cost is $20 per unit; and cash fixed costs are

$8,000,000 per year. The investment project requires $70,000,000 of cash outflow and has a

project life of 8 years.

At the end of the 8-year useful life, there will be no terminal disposal value. Assume all cash

flows occur at year-end except for initial investment amounts.

Men’s fragrance is a new market for Invigor, and management is concerned about the reliability

of the estimates. The controller has proposed applying sensitivity analysis to selected factors.

Ignore income taxes in your computations. Invigor’s required rate of return on this project is 12%.

Required:

1. Calculate the net present value of this investment proposal.

2. Calculate the effect on the net present value of the following two changes in assumptions.

(Treat each item independently of the other.)

a. 10% reduction in the selling price

b. 10% increase in the variable cost per unit

3. Discuss how management would use the data developed in requirements 1 and 2 in its

consideration of the proposed capital investment.

SOLUTION

The present value of an annuity of $1 per year for 8 years discounted at 12% = 4.968.

1. Revenues, $50 × 1,200,000 $60,000,000

Variable cash costs, $20 × 1,200,000 24,000,000

Cash contribution margin 36,000,000

Fixed cash costs 8,000,000

Cash inflow from operations $28,000,000

Net present value:

Cash inflow from operations: $28,000,000 × 4.968 $139,104,000

Cash outflow for initial investment (70,000,000)

Net present value $ 69,104,000

2a. 10% reduction in selling prices:

21-5

Revenues, $45 × 1,200,000 $54,000,000

Variable cash costs, $20 × 1,200,000 24,000,000

Cash contribution margin 30,000,000

Fixed cash costs 8,000,000

Cash inflow from operation $22,000,000

Net present value:

Cash inflow from operations: $22,000,000 × 4.968 $109,296,000

Cash outflow for initial investment (70,000,000)

Net present value $ 39,296,000

b. 10% increase in the variable cost per unit:

Revenues, $50 × 1,200,000 $60,000,000

Variable cash costs, $22 × 1,200,000 26,400,000

Cash contribution margin 33,600,000

Fixed cash costs 8,000,000

Cash inflow from operations $25,600,000

Net present value:

Cash inflow from operations: $25,600,000 × 4.968 $127,180,800

Cash outflow for initial investment (70,000,000)

Net present value $ 57,180,800

3. Sensitivity analysis enables management to see those assumptions for which input

variations have sizable impact on NPV. Extra resources could be devoted to getting more informed

estimates of those inputs with the greatest impact on NPV, in this case the potential reduction in

selling prices.

Sensitivity analysis also enables management to have contingency plans in place if

assumptions are not met.

21-32 (30–35 min.) NPV and AARR, goal-congruence issues.

Eric Ishton, a manager of the Plate Division for the Stone Ware Manufacturing company, has the

opportunity to expand the division by investing in additional machinery costing $430,000. He

would depreciate the equipment using the straight-line method and expects it to have no residual

value. It has a useful life of 8 years. The firm mandates a required after-tax rate of return of 12%

on investments. Eric estimates annual net cash inflows for this investment of $110,000 before taxes

and an investment in working capital of $7,500. The tax rate is 30%.

Required:

1. Calculate the net present value of this investment.

2. Calculate the accrual accounting rate of return based on net initial investment for this project.

3. Should Eric accept the project? Will Eric accept the project if his bonus depends on achieving

an accrual accounting rate of return of 12%? How can this conflict be resolved?

SOLUTION

21-6

1.

Annual cash flow from operations

$110,000

Income tax payments (30%)

33,000

Annual after-tax cash flow from operations (excl. deprn.)

$ 77,000

Depreciation: $430,000 ÷ 8 = $53,750 per year

Income-tax cash savings from depreciation deduction: $53,750 × 0.30 = $16,125 per year

The present value of an annuity of $1 per year for 8 years discounted at 12% = 4.968.

So, present value of annual cash flows = ($77,000 + $16,125) × 4.968 = $462,645

Net initial investment = $(430,000) + $(7,500) = $(437,500)

Present value of working capital recovery = $7,500 × 0.404 = $3,030

Net present value of project = $(437,500) + $462,645 + $3,030 = $28,175

2. Accrual accounting rate of return (AARR): The accrual accounting rate of return takes

the annual accrual net income after tax and divides by the initial investment to get a return.

Incremental net operating income excluding depreciation $110,000

Less: Depreciation expense ($430,000 ÷ 8) 53,750

Income before tax 56,250

Income tax expense (at 30%) 16,875

Net income per period $ 39,375

AARR = $39,375 ÷ $437,500 = 9.00%.

3. Eric will not accept the project if he is being evaluated on the basis of accrual accounting

rate of return because the project does not meet the 12% threshold above which Eric earns a

bonus. Eric should accept the project if he wants to act in the firm’s best interest because the

NPV is positive, implying that, based on the cash flows generated, the project exceeds the firm’s

required 12% rate of return. Thus, Eric will turn down an acceptable long-run project to avoid a

poor evaluation based on the measure used to evaluate his performance. To remedy this, the firm

could evaluate Eric instead on a project-by-project basis and by looking at how well he achieves

the cash flows forecasted when he chose to accept a given project.

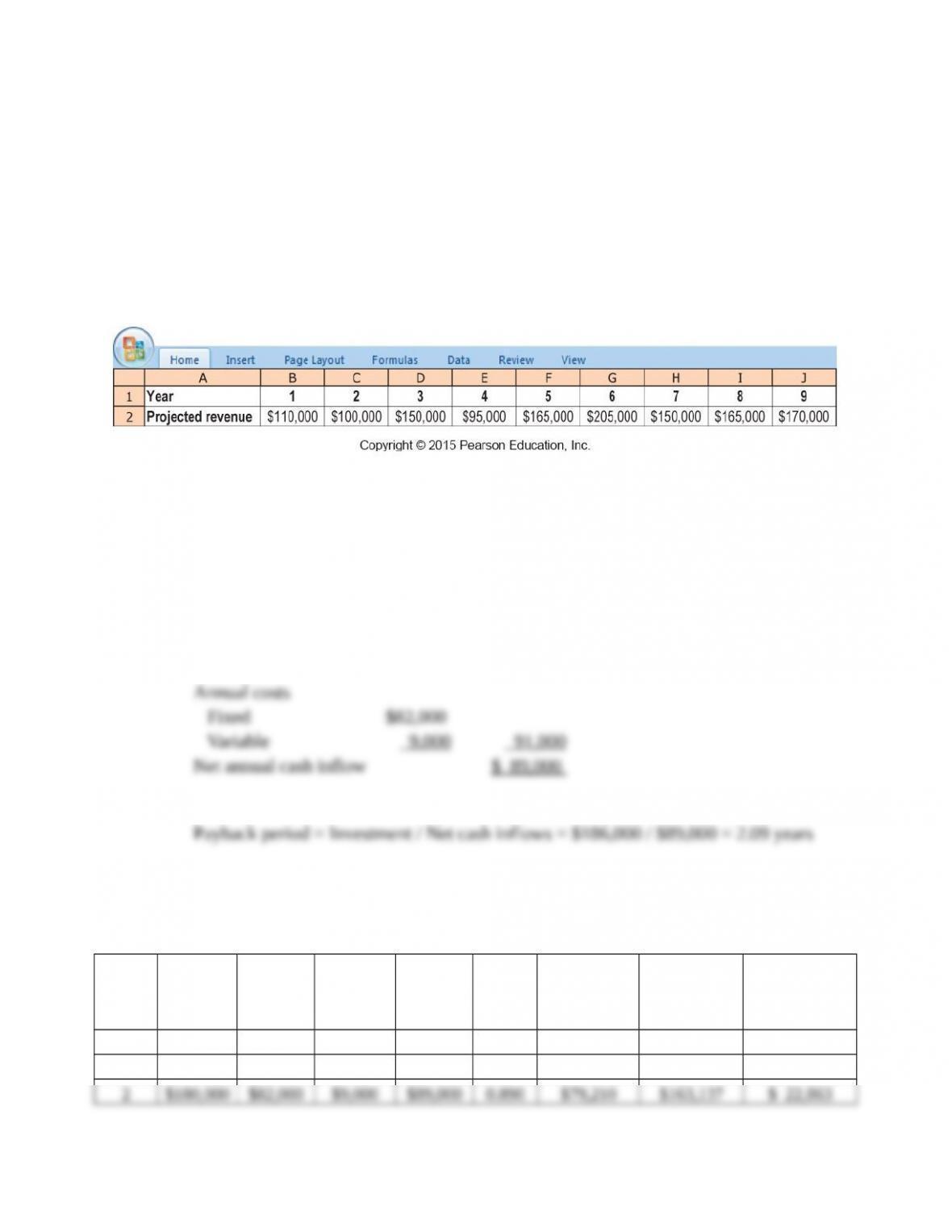

21-33 (30 min.) Payback methods, even and uneven cash flows.

Cardinal Laundromat is trying to enhance the services it provides to customers, mostly college

students. It is looking into the purchase of new high- efficiency washing machines that will allow

for the laundry’s status to be checked via smartphone.

Cardinal estimates the cost of the new equipment at $186,000. The equipment has a useful life

of 9 years. Cardinal expects cash fixed costs of $82,000 per year to operate the new machines, as

well as cash variable costs in the amount of 5% of revenues. Cardinal evaluates investments using

a cost of capital of 6%.

Required:

1. Calculate the payback period and the discounted payback period for this investment, assuming

Cardinal expects to generate $180,000 in revenues every year from the new machines.

2. Assume instead that Cardinal expects the following uneven stream of cash revenues from

installing the new washing machines:

Based on this estimated revenue stream, what are the payback and discounted payback periods for

the investment?

SOLUTION

Payback problem:

1.

Annual revenue

$180,000

Annual costs

Fixed

$82,000

Variable

9,000

91,000

Net annual cash inflow

$ 89,000

Payback period = Investment / Net cash inflows = $186,000 / $89,000 = 2.09 years

Discounted Payback Period with even cash flows:

$22,863/$74,760 = 0.31

Discounted Payback Period = 2.31 years

2.

Year

Revenue

(1)

Cash Fixed

Costs

(2)

Cash

Variable Costs

(3)

Net Cash Inflows

(4) = (1) − (2) − (3)

Cumulative

Amounts

1

$110,000

$ 82,000

$ 5,500

$ 22,500

$ 22,500

2

100,000

82,000

5,000

13,000

35,500

3

150,000

82,000

7,500

60,500

96,000

4

95,000

82,000

4,750

8,250

104,250

5

165,000

82,000

8,250

74,750

179,000

6

205,000

82,000

10,250

112,750

291,750

7

150,000

82,000

7,500

60,500

352,250

8

165,000

82,000

8,250

74,750

427,000

9

170,000

82,000

8,500

79,500

506,500

The cumulative amount exceeds the initial $186,000 investment for the first time at the end of year

6. So, payback happens in year 6.

Using linear interpolation, a more precise measure is that payback happens at:

5 years + ($186,000 – $179,000)/$112,750 = 5.06 years

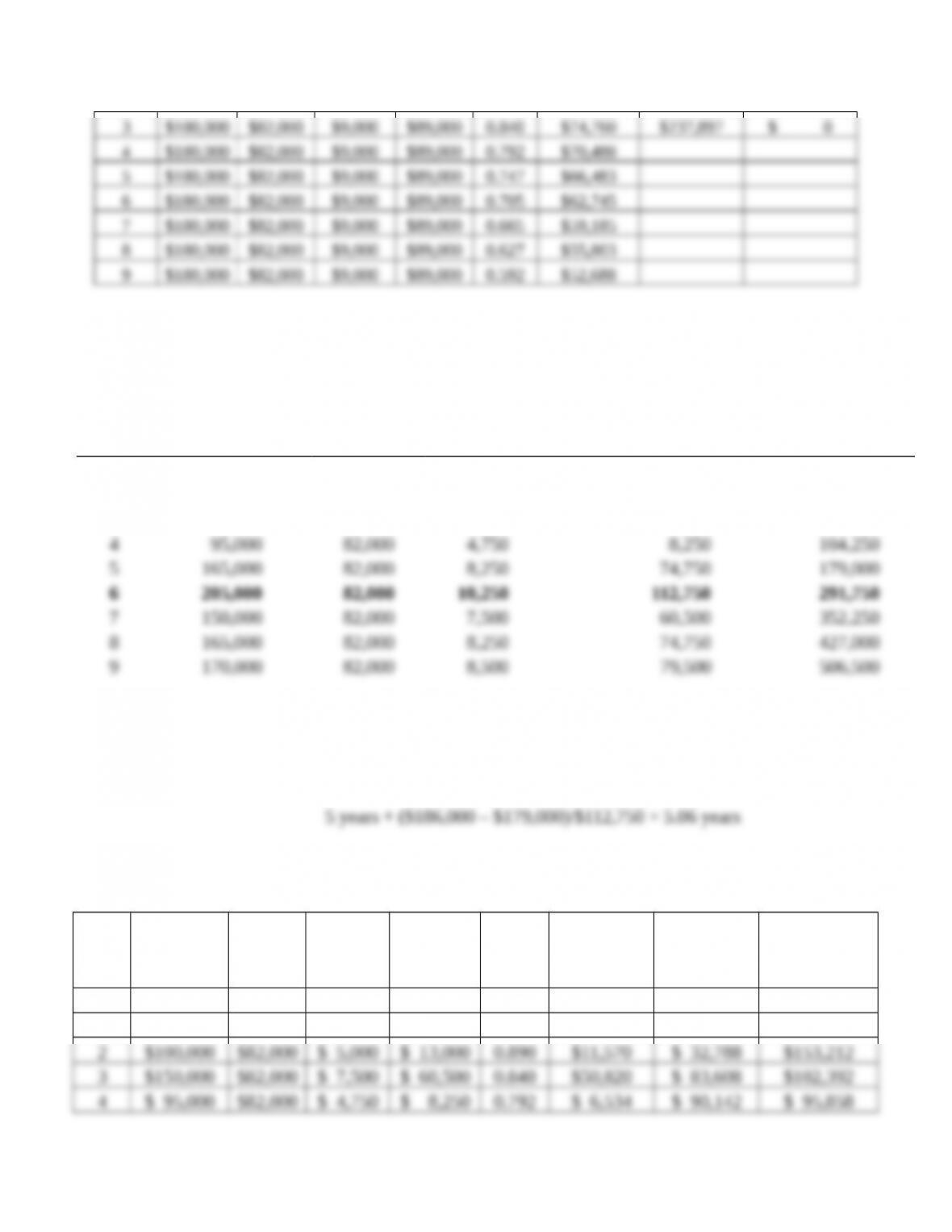

Discounted Payback Period with uneven cash flows:

Period

Year

Cash

Revenues

Fixed

Costs

Variable

Costs

Net Cash

Inflows

Disc

Factor

(6%)

Discounted

Cash Savings

Cumulative

Disc. Cash

Savings

Unrecovered

Investment

0

$186,000

1

$180,000

$82,000

$9,000

$89,000

0.943

$83,927

$ 83,927

$102,073

2

$180,000

$82,000

$9,000

$89,000

0.890

$79,210

$163,137

$ 22,863

3

$180,000

$82,000

$9,000

$89,000

0.840

$74,760

$237,897

$ 0

4

$180,000

$82,000

$9,000

$89,000

0.792

$70,488

5

$180,000

$82,000

$9,000

$89,000

0.747

$66,483

6

$180,000

$82,000

$9,000

$89,000

0.705

$62,745

7

$180,000

$82,000

$9,000

$89,000

0.665

$59,185

8

$180,000

$82,000

$9,000

$89,000

0.627

$55,803

9

$180,000

$82,000

$9,000

$89,000

0.592

$52,688

21-9

Year

Cash

Revenues

Fixed

Costs

Variable

Costs

Net Cash

Inflows

Disc

Factor

(6%)

Discounted

Cash

Savings

Cumulative

Disc. Cash

Savings

Unrecovered

Investment

0

$186,000

1

$110,000

$82,000

$ 5,500

$ 22,500

0.943

$21,218

$ 21,218

$164,782

2

$100,000

$82,000

$ 5,000

$ 13,000

0.890

$11,570

$ 32,788

$153,212

3

$150,000

$82,000

$ 7,500

$ 60,500

0.840

$50,820

$ 83,608

$102,392

4

$ 95,000

$82,000

$ 4,750

$ 8,250

0.792

$ 6,534

$ 90,142

$ 95,858

5

$165,000

$82,000

$ 8,250

$ 74,750

0.747

$55,838

$145,980

$ 40,020

6

$205,000

$82,000

$10,250

$112,750

0.705

$79,489

$225,469

$ 0

7

$150,000

$82,000

$ 7,500

$ 60,500

0.665

$40,233

$265,702

8

$165,000

$82,000

$ 8,250

$ 74,750

0.627

$46,868

$312,570

9

$170,000

$82,000

$ 8,500

$ 79,500

0.592

$47,064

$359,634

Discounted payback period = 5 years + ($186,000 – $145,980)/$79,489 = 5.50 years

21-34 (40 min.) Replacement of a machine, income taxes, sensitivity.

(CMA, adapted) The Frooty Company is a family-owned business that produces fruit jam. The

company has a grinding machine that has been in use for 3 years. On January 1, 2014, Frooty is

considering the purchase of a new grinding machine. Frooty has two options: (1) continue using

the old machine or (2) sell the old machine and purchase a new machine. The seller of the new

machine isn’t offering a trade-in. The following information has been obtained:

A

Frooty is subject to a 34% income tax rate. Assume that any gain or loss on the sale of machines

is treated as an ordinary tax item and will affect the taxes paid by Frooty in the year in which it

21-10

occurs. Frooty’s after-tax required rate of return is 12%. Assume all cash flows occur at year-end

except for initial investment amounts.

Required:

1. A manager at Frooty asks you whether it should buy the new machine. To help in your analysis,

calculate the following:

a. One-time after-tax cash effect of disposing of the old machine on January 1, 2014

b. Annual recurring after-tax cash operating savings from using the new machine (variable

and fixed)

c. Cash tax savings due to differences in annual depreciation of the old machine and the new

machine

d. Difference in after-tax cash flow from terminal disposal of new machine and old machine

2. Use your calculations in requirement 1 and the net present value method to determine whether

Frooty should use the old machine or acquire the new machine.

3. How much more or less would the recurring after-tax cash operating savings of the new

machine need to be for Frooty to earn exactly the 12% after-tax required rate of return? Assume

that all other data about the investment do not change.

SOLUTION

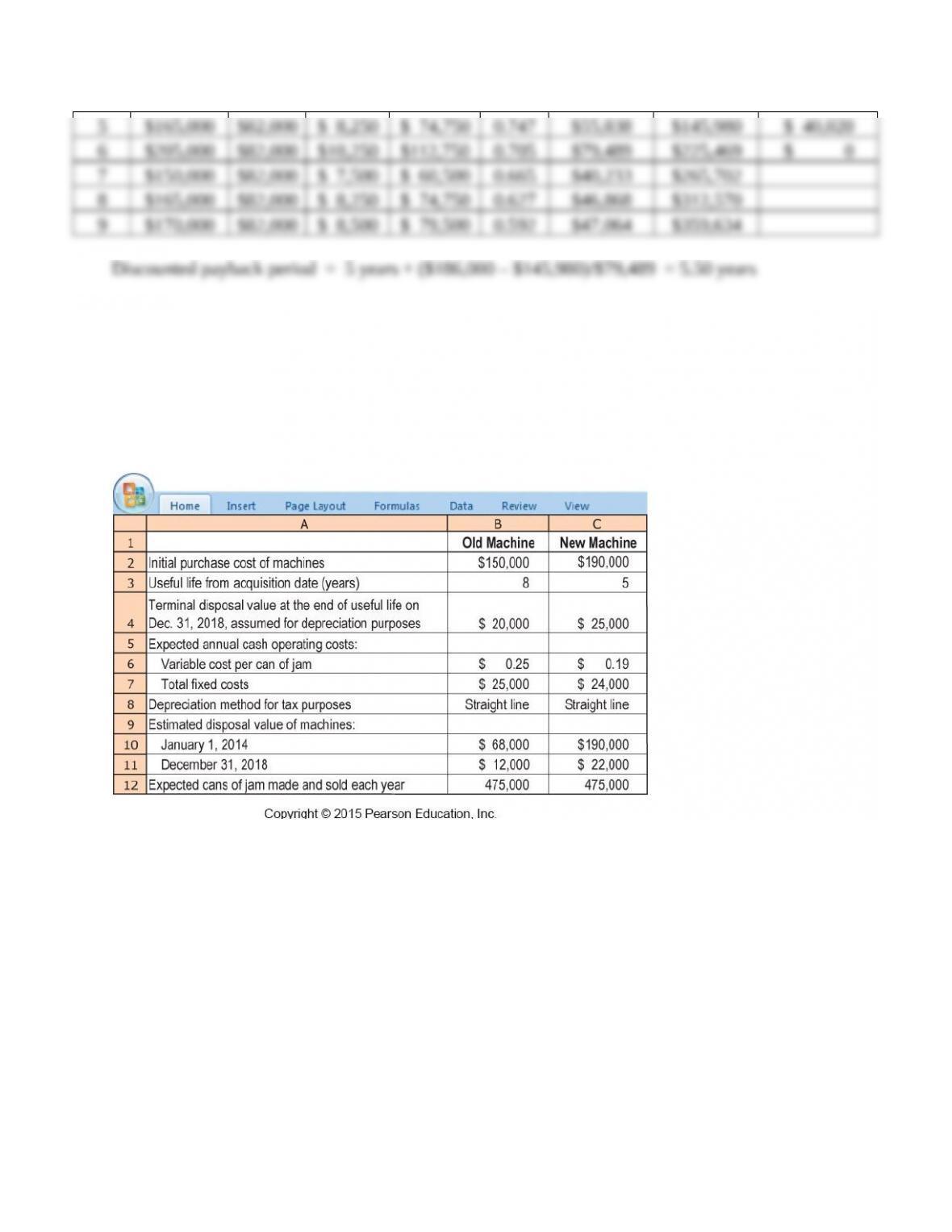

1a. Original cost of old machine: $150,000

Depreciation taken during the first 3 years

{[($150,000 – $20,000) ÷ 8] 3} 48,750

Book value 101,250

Current disposal price: 68,000

Loss on disposal $ 33,250

Tax rate × 0.34

Tax savings from loss on current disposal of old machine $ 11,305

Total after-tax cash effect of disposal = $68,000 + $11,305 = $79,305

1b. Difference in recurring after-tax variable cash-operating savings, with 34% tax rate:

($0.25 – $0.19) (475,000) (1– 0.34) = $18,810 (in favor of new machine)

Difference in after-tax fixed cost savings, with 34% tax rate:

($25,000 – $24,000) (1 – 0.34) = $660 (in favor of new machine)

1c.

Old Machine

New Machine

Initial machine investment $150,000 $190,000

Terminal disposal price at end of useful life 20,000 25,000

Depreciable base $130,000 $165,000

Annual depreciation using

straight-line (8-year life) $ 16,250

Annual depreciation using straight-line (5-year life): $ 33,000

21-11

Annual income tax cash savings from difference in depreciation deduction:

($33,000 – $16,250) 0.34 = $5,695 (in favor of new machine)

1d.

Old Machine

New Machine

Original cost $150,000 $190,000

Total depreciation 130,000 165,000

Book value of machines on Dec. 31, 2018 20,000 25,000

Terminal disposal price of machines on Dec. 31, 2018 12,000 22,000

Loss on disposal of machines 8,000 3,000

Add tax savings on loss (34% of $8,000; 34% of $3,000) 2,720 1,020

After-tax cash flow from terminal disposal of

machines ($12,000 + $2,720; $22,000 + $1,020) $ 14,720 $ 23,020