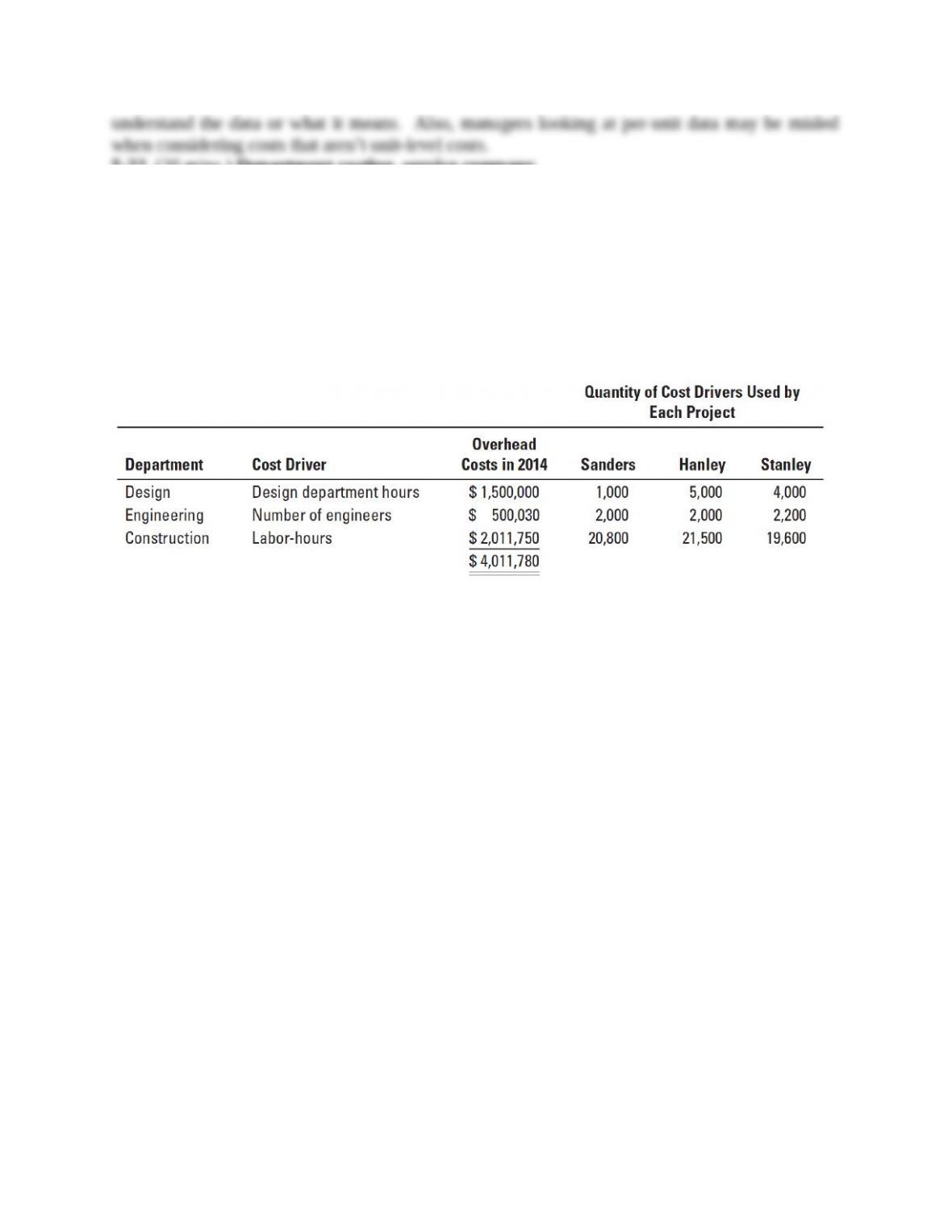

Design

Engineering

Production

CAD-design hours

Engineering hours

Machine hours

28%

19

3

51%

16

70

21%

65

27

The United Motors contract uses only 3% of total machines hours in 2011, yet uses 28%

of CAD design-hours and 19% of engineering hours. The result is that the plantwide rate, based

on machine hours, will greatly underestimate the cost of resources used on the United Motors

contract. This explains the 157% increase in indirect costs assigned to the United Motors contract

when department rates are used. The Leland Auto contract also uses far fewer machine-hours than

engineering-hours and is also undercosted.

In contrast, the Holden Motors contract uses less of design (51%) and engineering (16%)

than of machine-hours (70%). Hence, the use of department rates will report lower indirect costs

for Holden Motors than does a plantwide rate.

Holden Motors was probably complaining under the use of the simple system because its

contract was being overcosted relative to its consumption of MOH resources. United and Leland,

on the other hand, were having their contracts undercosted and underpriced by the simple

system. Assuming that AP is an efficient and competitive supplier, if the new department-based

rates are used to price contracts, United and Leland will be unhappy. AP should explain to United

and Leland how the calculation was done, and point out United’s high use of design and

engineering resources and Leland’s high use of engineering resources relative to production

machine hours. Discuss ways of reducing the consumption of those resources, if possible, and

show willingness to partner with them to do so. If the price rise is going to be steep, perhaps offer

to phase in the new prices.

4. Other than for pricing, AP can also use the information from the department-based system

to examine and streamline its own operations so that there is maximum value-added from all

indirect resources. It might set targets over time to reduce both the consumption of each indirect

resource and the unit costs of the resources. The department-based system gives AP more

opportunities for targeted cost management.

5. It would not be worthwhile to further refine the cost system into an ABC system if (1) a

single activity accounts for a sizable proportion of the department’s costs or (2) significant costs

are incurred on different activities within a department, but each activity has the same cost driver

or (3) there wasn’t much variation among contracts in the consumption of activities within a

department. If, for example, most activities within the design department were, in fact, driven by

CAD-design hours, then the more refined system would be more costly and no more accurate than

the department-based cost system. Even if there was sufficient variation, considering the relative

sizes of the three department cost pools, it may only be cost-effective to further analyze the

engineering cost pool, which consumes 78% ($240,000

$308,600) of the manufacturing

overhead.

5-20 (50 min.) Plantwide, department, and activity-cost rates.

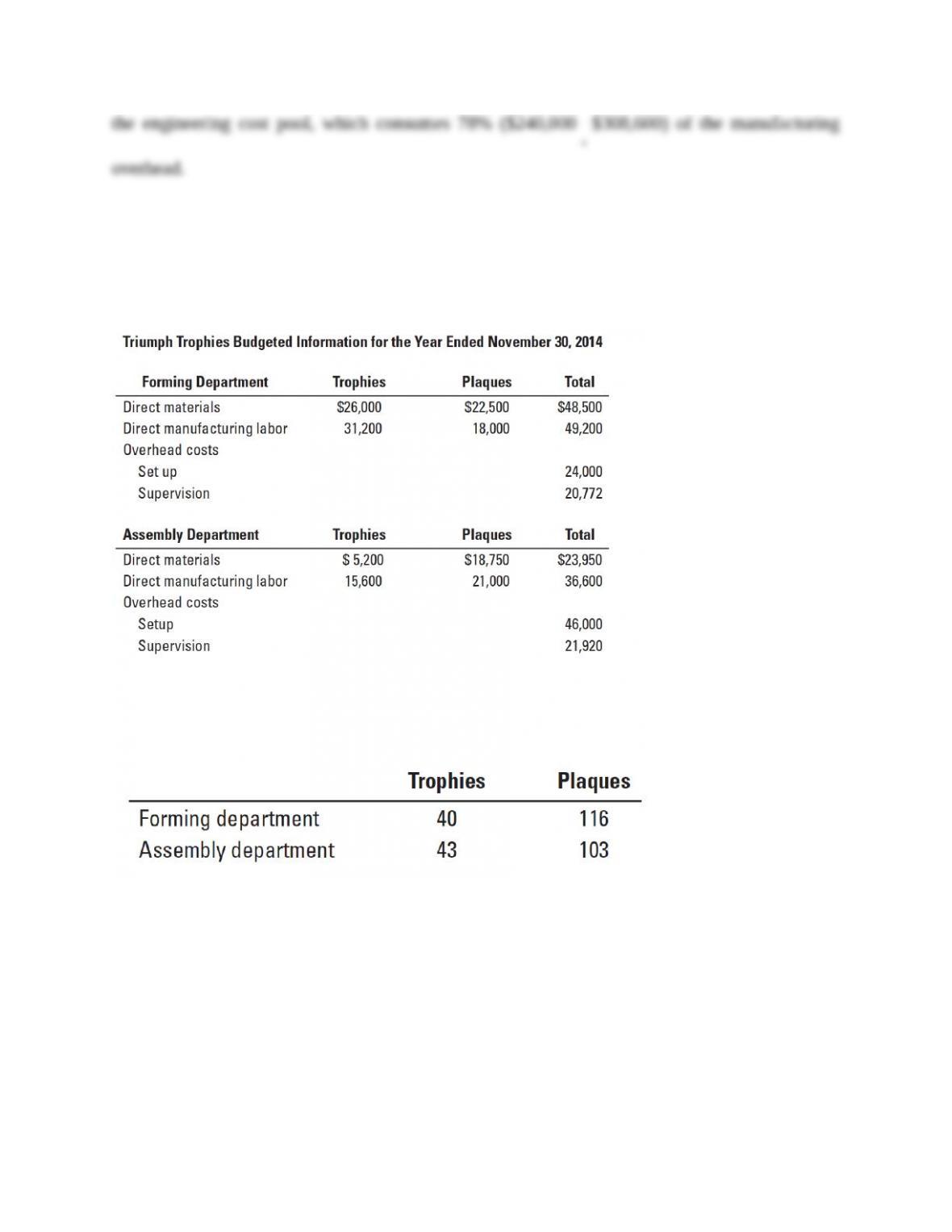

Triumph Trophies makes trophies and plaques and operates at capacity. Triumph does large

custom orders, such as the participant trophies for the Minnetonka Little League. The controller

has asked you to compare plant-wide, department, and activity- based cost allocation.

Forming

$26,000

$22,500

Assembly

5,200

18,750

Total

31,200

41,250

Direct manufacturing labor

Forming

31,200

18,000

Assembly

15,600

21,000

Total

46,800

39,000

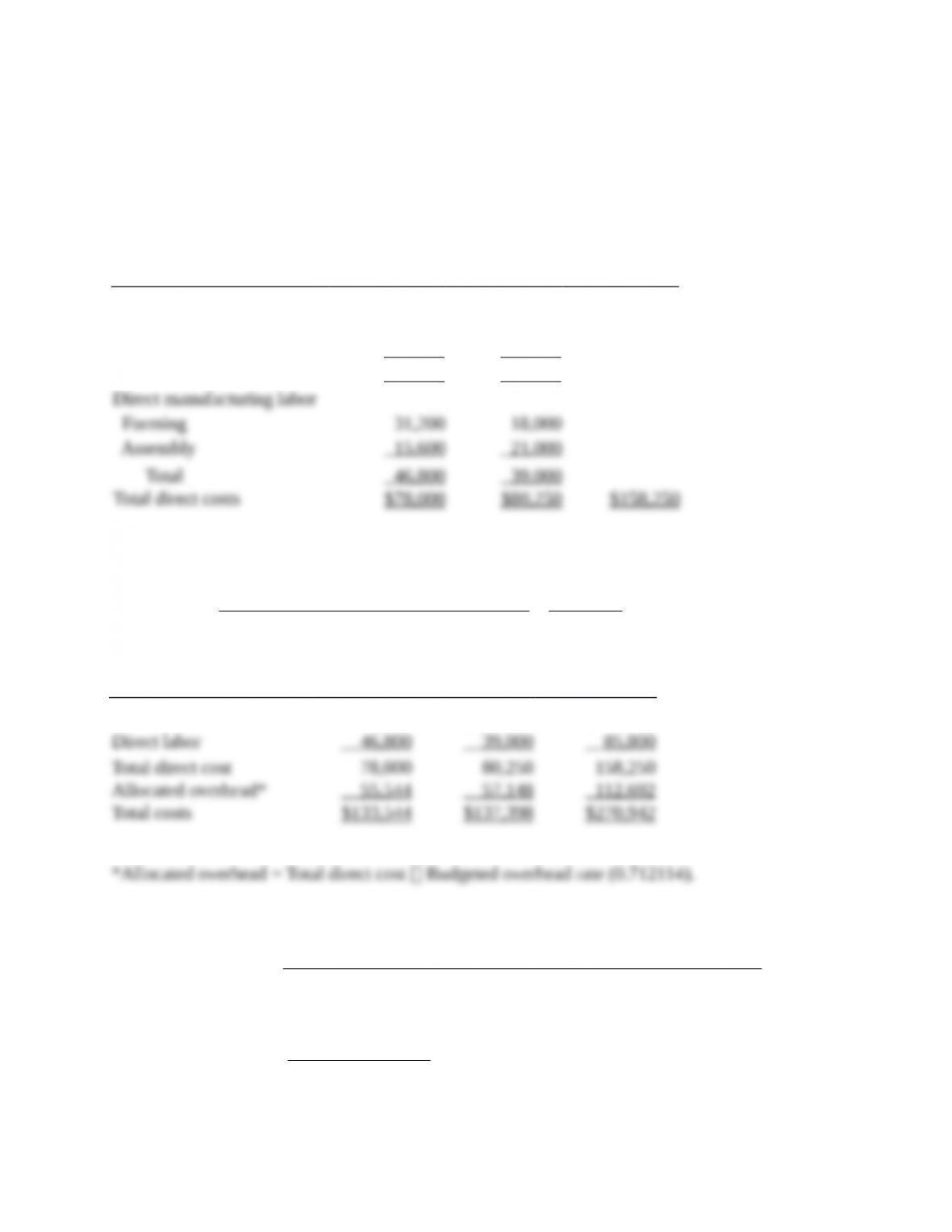

Total direct costs

$78,000

$80,250

$158,250

Budgeted

overhead rate

=

($24,000 $20,772 $46,000 $21,920) $112,692

$158,250 $158,250

+++ =

=

$0.712114

per dollar of direct cost

Trophies

Plaques

Total

Direct materials

$ 31,200

$ 41,250

$ 72,450

Direct labor

46,800

39,000

85,800

Total direct cost

78,000

80,250

158,250

Allocated overhead*

55,544

57,148

112,692

Total costs

$133,544

$137,398

$270,942

*Allocated overhead = Total direct cost Budgeted overhead rate (0.712114).

2.

Budgeted

overhead rate

Forming Dept.

—

=

Budgeted Forming Department overhead costs

Budgeted Forming Department direct manufacturing labor costs

=

$24,000 $20,772

$31,200 $18,000

+

+

=

$44,772

$49,200 =

$0.91 per Forming Department direct manuf.-labor dollar

Budgeted

overhead rate

Assembly Dept.

—

=

Budgeted Assembly Department overhead costs

Budgeted Assembly Department direct costs

=

$46,000 $21,920

($5,200 $18,750 $15,600 $21,000)

+

+++

=

$67,920

$60,550 =

$1.121718 per Assembly Department direct cost dollar

Trophies

Plaques

Total

Direct materials

$ 31,200

$ 41,250

$ 72,450

Direct labor

46,800

39,000

85,800

Total direct cost

78,000

80,250

158,250

Allocated overhead

Forming Dept.a

28,392

16,380

44,772

Assembly Dept.b

23,332

44,588

67,920

Total costs

$129,724

$141,218

$270,942

Trophies

Plaques

Total

a Forming Dept.

Direct manufacturing labor costs

$31,200

$18,000

$49,200

Allocated overhead

(0.91 × $31,200; $18,000)

$28,392

$16,380

$44,772

b Assembly Dept.

Total direct costs

($5,200 + $15,600; $18,750 + $21,000)

$20,800

$39,750

$60,550

Allocated overhead

(1.121718 $20,800; $39,750)

$11,666

$22,294

$33,960

3.

Forming Department

Budgeted setup rate

=

$24,000

156 batches

= $153.84615 per batch

Budgeted supervision rate

=

$20,772

$49,200

= $0.422195 per direct-labor dollar

Assembly Department

Budgeted set up rate

=

$46,000

146 batches

= $315.06849 per batch

Budgeted supervision rate

=

$21,920

$36,600

= $0.598907 per direct manuf.-labor dollar

Trophies

Plaques

Total

Direct material costs

$ 31,200

$ 41,250

$ 72,450

Direct labor costs

46,800

39,000

85,800

Total direct costs

78,000

80,250

158,250

Forming Dept. overhead

Set up

$153.84615 40; 116

6,154

17,846

24,000

Supervision

0.422195

$31,200; $18,000

13,172

7,600

20,772

Assembly Department overhead

Set up

$315.06849

43; 103

13,548

32,452

46,000

Supervision

0.598907

$15,600; $21,000

9,343

12,577

21,920

Total costs

$120,217

$150,725

$270,942

4. As Triumph uses more refined cost pools, the costs of trophies decreases, and costs of

plaques increases. This is because plaques use a higher proportion of cost drivers (batches of

set ups and direct manufacturing labor costs) than trophies, whereas the direct costs (the

allocation base used in the simple costing system) are slightly smaller for plaques compared to

trophies. This results in plaques being undercosted and trophies overcosted in the simple

costing system.

Department costing systems increase the costs of plaques relative to trophies because

the forming department costs are allocated based on direct manufacturing labor costs in the

forming department and plaques use more direct manufacturing labor in this department

compared to trophies.

Disaggregated information can improve decisions by allowing managers to see the

details that help them understand how different aspects of cost influence total cost per unit.

Managers can also understand the drivers of different cost categories and use this information

for pricing and product-mix decisions, cost reduction and process-improvement decisions,

design decisions, and to plan and manage activities. However, too much detail can overload

managers who don’t understand the data or what it means. Also, managers looking at per-unit

data may be misled when considering costs that aren’t unit-level costs.

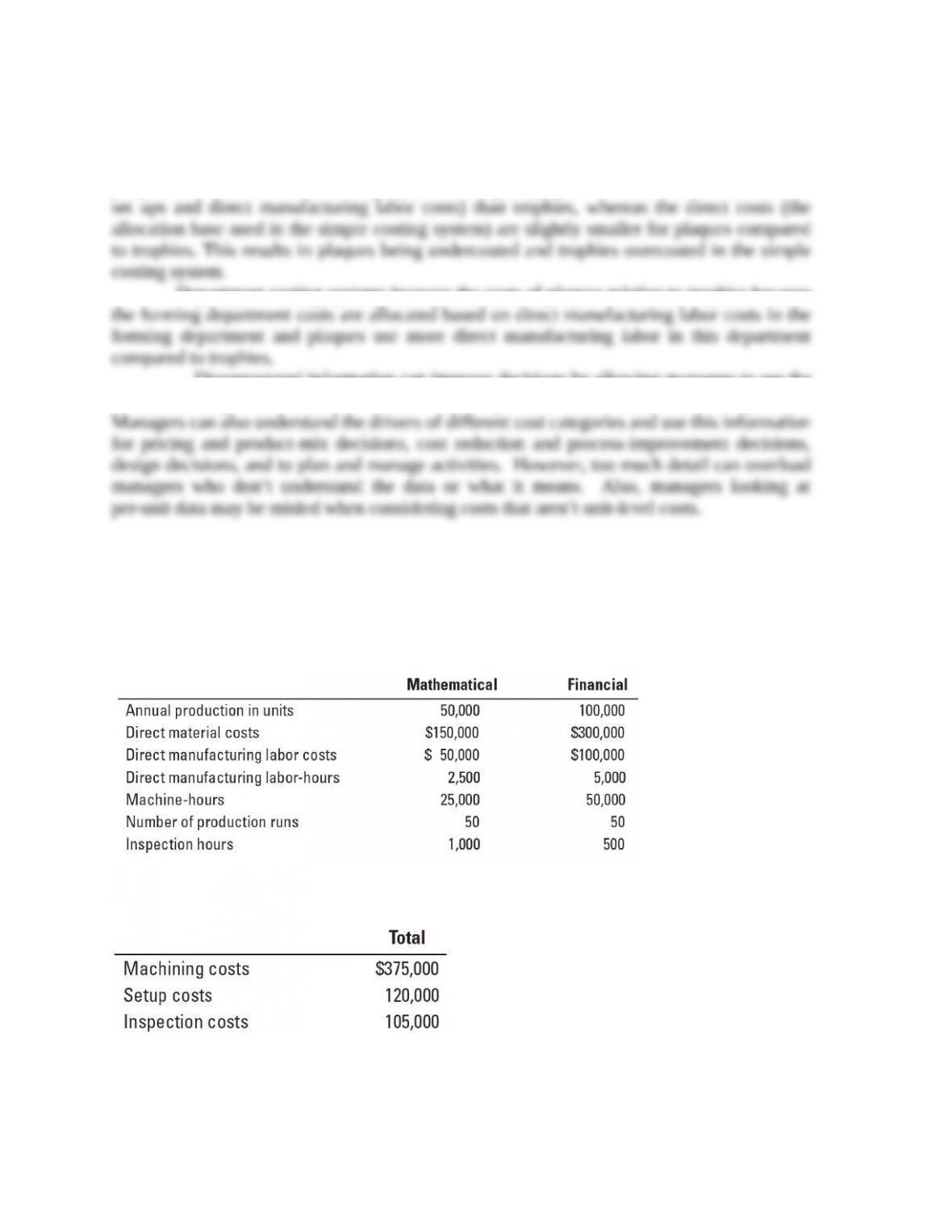

5-21 (10–15 min.) ABC, process costing.

Parker Company produces mathematical and financial calculators and operates at capacity. Data

related to the two products are presented here: