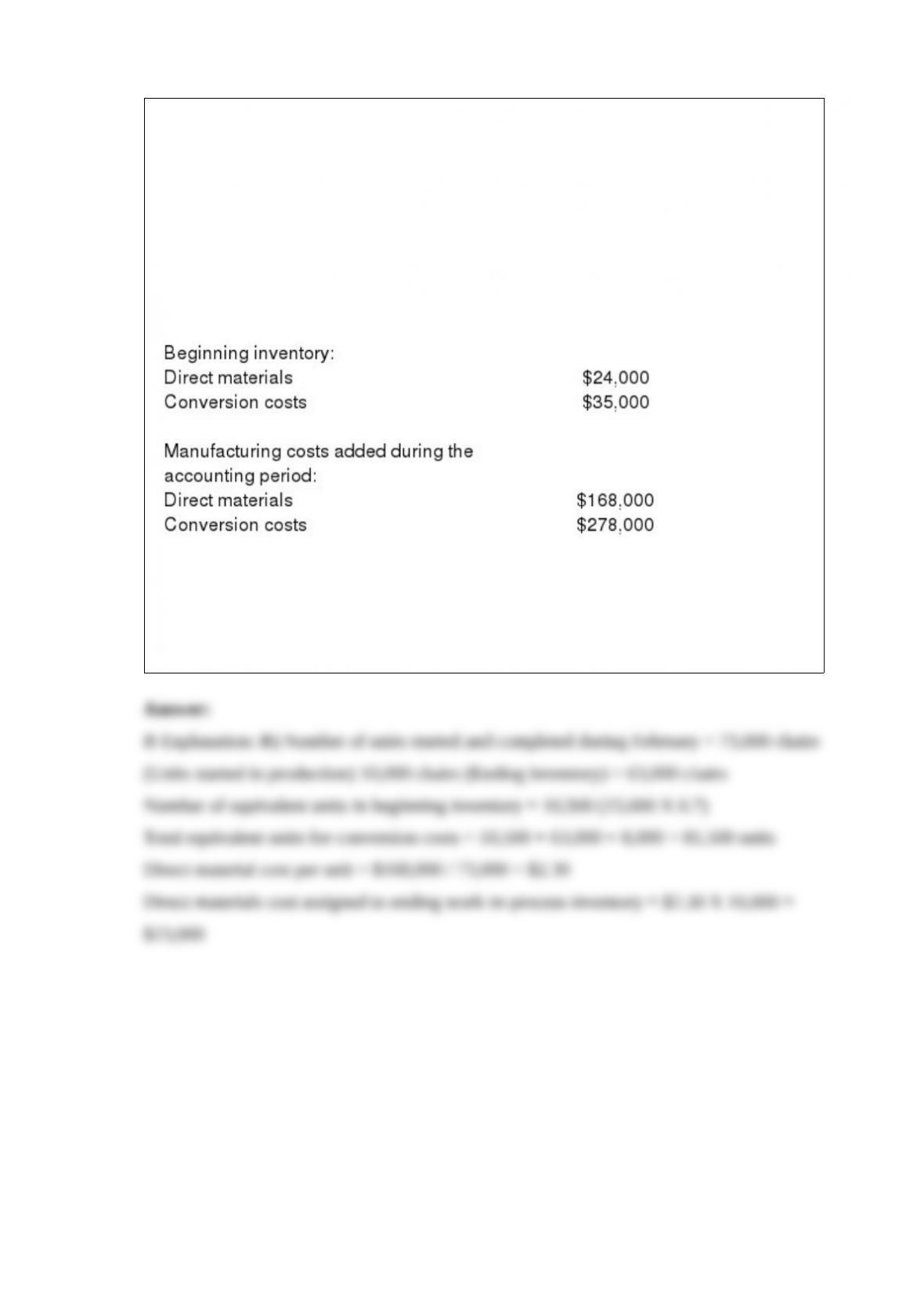

1) Comfort chair company manufacturers a standard recliner. During February, the

firm’s Assembly Department started production of 73,000 chairs. During the month, the

firm completed 78,000 chairs, and transferred them to the Finishing Department. The

firm ended the month with 10,000 chairs in ending inventory. There were 15,000 chairs

in beginning inventory. All direct materials costs are added at the beginning of the

production cycle and conversion costs are added uniformly throughout the production

process. The FIFO method of process costing is used by Comfort. Beginning work in

process was 30% complete as to conversion costs, while ending work in process was

80% complete as to conversion costs.

What is the cost of the goods transferred out during February?

A) $417,750.5

B) $454,694.8

C) $476,750.6

D) $505,000 .2

2) Which of the following statements is true of the cost of producing a product?

A) It controls pricing in highly competitive markets.

B) It affects the willingness of a company to supply a product.

C) It includes manufacturing costs, but not product design costs for pricing decisions.

D) It is not a factor to be taken into account while pricing a product.

3) In the service sector, to achieve timely reporting on the profitability of an

engagement, a company will use ________.

A) budgeted rates for all direct costs

B) budgeted rates for indirect costs

C) actual costing

D) budgeted rates for some direct costs and indirect costs

4) Fixed overhead costs ________.

A) never have any unused capacity

B) have no spending variance

C) have no efficiency variance

D) have no production-volume variance

5) Short-run prices should at least recover ________.

A) full cost of producing a product

B) fixed manufacturing overhead

C) variable cost of producing a product

D) variable and fixed manufacturing overhead

6) Chess Woods Limited produces two products: wooden chess pieces and wooden

inlaid chess boards. Under their traditional cost system using one cost driver (direct

manufacturing labor hours), the cost of a set of wooden chess pieces is $325.00. An

analysis of the activities and their costs revealed that three cost drivers would be used

under a new ABC system. These cost drivers would be equipment usage, storage area

for the material, and type of woods used. The new cost of a set of chess pieces was

determined to be $298.00 per set.

Given this change in the cost structure ________.

A) The costing results for chess pieces under the new system depend on the adequacy

and quality of the estimated cost drivers and costs used by the system.

B) Chess pieces have benefited from the new system.

C) Chess pieces are definitely more accurately costed.

D) Chess will now have a lower sales price.

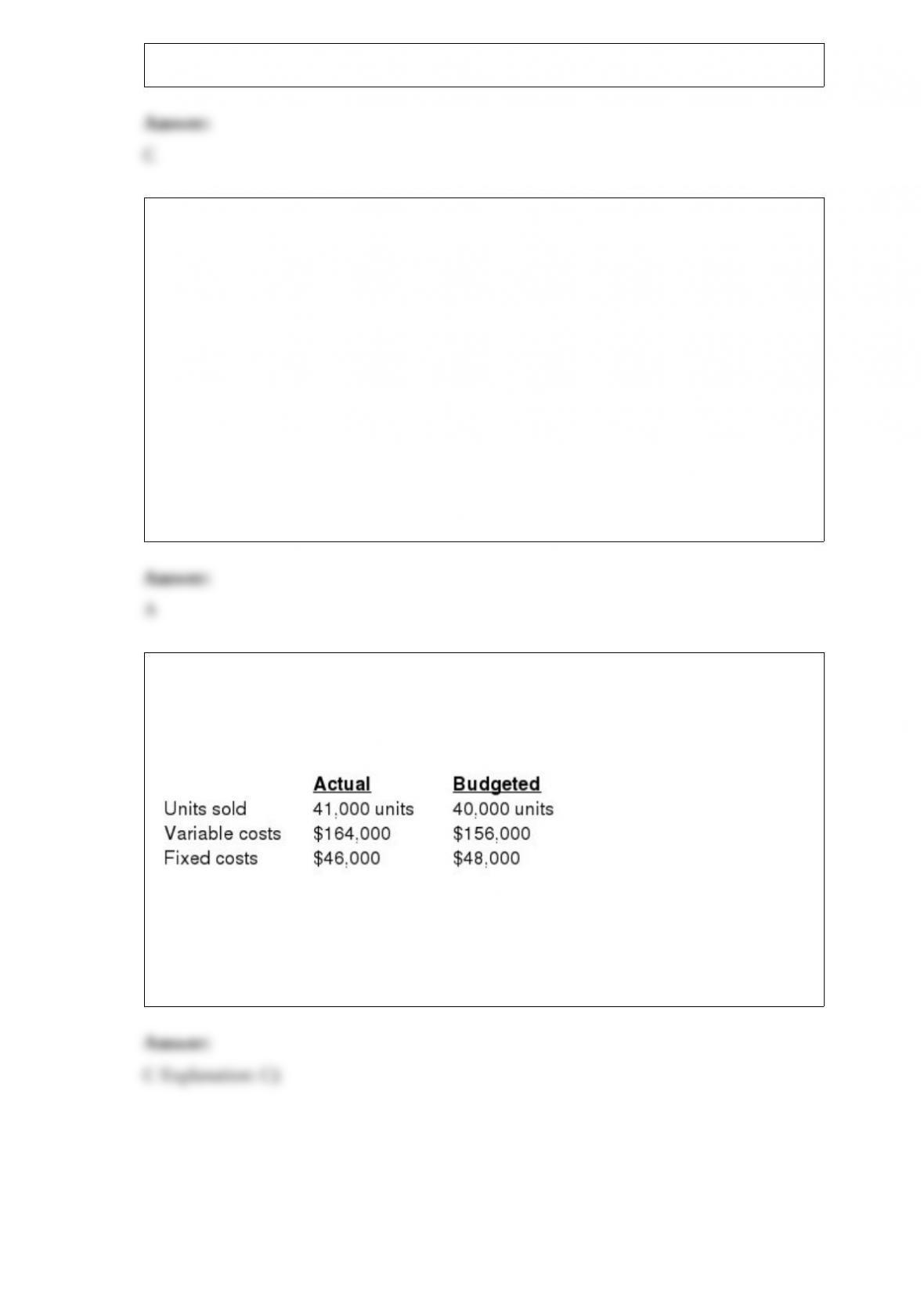

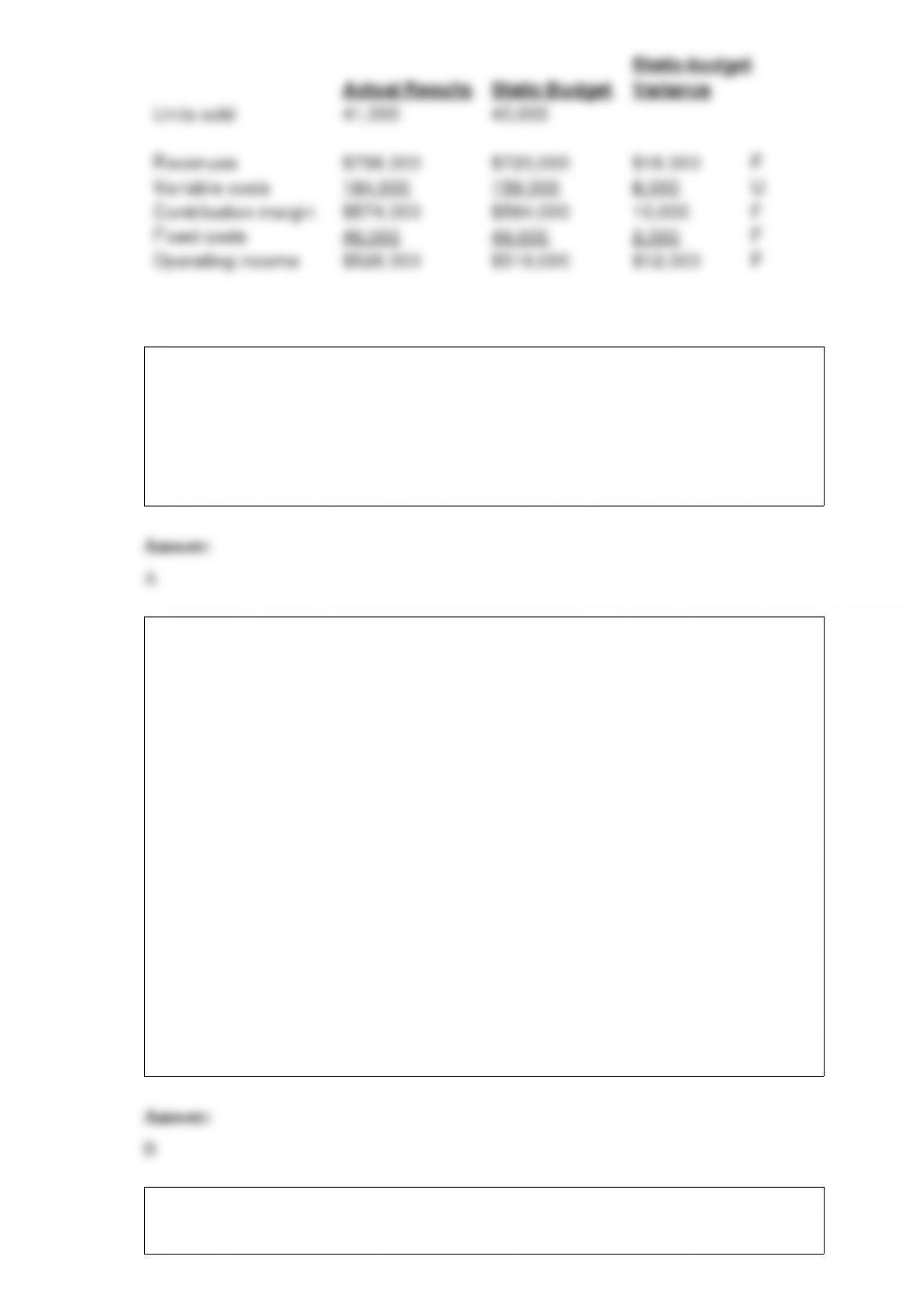

7) Lander Corporation used the following data to evaluate their current operating

system. The company sells items for $18 each and used a budgeted selling price of $18

per unit.

What is the static-budget variance of operating income?

A) $10,000 favorable

B) $10,000 unfavorable

C) $12,000 favorable

D) $12,000 unfavorable

8) Which of the following companies is part of the manufacturing sector of our

economy?

A) Nike

B) Barnes & Noble

C) Corvette Law Firm

D) Sears, Roebuck, and Company

9) Games R Us manufactures various games. For March, there were no beginning

inventories of direct materials and no beginning or ending work in process. Conversion

costs is the only indirect manufacturing cost category currently used. Journal entries are

recorded when materials are purchased and when conversion costs are allocated under

backflush costing.

Conversion costs March$ 400,000

Direct materials purchased March$1,070,000

Units produced March58,800

Units sold March41,800

Which of the following journal entries properly records the purchase of direct

materials?

A) Accounts Payable Control 1,070,000

Inventory: Raw and In-Process Control 1,070,000

B) Inventory: Raw and In-Process Control 1,070,000

Accounts Payable Control 1,070,000

C) Inventory: Raw and In-Process Control 1,070,000

Conversion Costs 1,070,000

D) Conversion Costs 1,070,000

Inventory: Raw and In-Process Control 1,070,000

10) Outputs with a negative sales value are ________.

A) added to cost of goods sold

B) added to joint production costs and allocated to joint or main products

C) added to joint production costs and allocated to byproducts and scrap

D) subtracted from product revenue

11) Which of the following statements is of true engineered costs?

A) They arise from periodic (usually annual) decisions regarding the maximum amount

to be incurred.

B) They have a detailed, physically observable, and repetitive relationship with output.

C) They include advertising, executive training, and R&D.

D) They have high level of uncertainty.

12) Using master-budget capacity to set selling prices ________.

A) avoids the recalculation of unit costs when expected demand levels change

B) spreads fixed costs over available capacity

C) can result in a downward demand spiral

D) uses the perspective of long-run product pricing