Direct materials

Direct labor

Job 11

$4,870

$5,100

Job 12

$5,910

$6,800

InStep Company has no finished goods inventories because all printing jobs are transferred to cost

of goods sold when completed.

Required:

1. Compute the overhead allocation rate.

2. Calculate the balance in ending work in process and cost of goods sold before any adjustments

for under- or overallocated overhead.

3. Calculate under- or overallocated overhead.

4. Calculate the ending balances in work in process and cost of goods sold if the under- or

overallocated overhead amount is as follows:

a. Written off to cost of goods sold

b. Prorated using the overhead allocated in 2014 (before proration) in the ending balances of

cost of goods sold and work-in-process control accounts

5. Which of the methods in requirement 4 would you choose? Explain.

SOLUTION

1. Budgeted overhead rate = Budgeted overhead costs ÷ Budgeted labor costs

= $315,000 ÷ $225,000 = 140% of labor cost

2. Ending work in process

Job 11

Job 12

Total

Direct material costs

$ 4,870

$ 5,910

$10,780

Direct labor costs

5,100

6,800

11,900

Overhead

(1.40 × Direct labor costs)

7,140

9,520

16,660

Total costs

$17,110

$22,230

$39,340

Cost of goods sold = Beginning WIP + Manufacturing costs – Ending WIP

= $0 + $148,500 + $213,500 + ($213,500 × 1.40) – $39,340 = $621,560

3. Overhead allocated = 1.40 × $213,500 = $298,900

Underallocated overhead = Actual overhead – Allocated overhead

= $302,100 – $298,900 = $3,200 underallocated

4a. All underallocated overhead is written off to cost of goods sold.

WIP inventory remains unchanged.

Account

(1)

Dec. 31, 2014

Account Balance

(Before Proration)

(2)

Write-off of $3,200

Underallocated

overhead

(3)

Dec. 31, 2014

Account Balance

(After Proration)

(4) = (2) + (3)

Work in Process

$ 39,340

$ 0

$ 39,340

Cost of goods sold

621,560

3,200

624,760

$660,900

$3,200

$664,100

4b. Underallocated overhead prorated based on overhead allocated before proration.

Account

(1)

Dec. 31, 2014

Account

Balance

(Before

Proration)

(2)

Allocated Overhead

Included in

Dec. 31, 2014

Account Balance

(Before Proration)

(3) (4)

Proration of $3,200

Underallocated

Manufacturing Overhead

(5)

Dec. 31, 2014

Account

Balance

(After

Proration)

(6) = (2) + (5)

Work in Process

$ 39,340

$ 16,660a (5.57%)

0.0557 $3,200 = $ 178

$ 39,518

Cost of Goods Sold

621,560

282,240b (94.43%)

0.9443 $3,200 = 3,022

624,582

Total

$660,900

$298,900 100%

$3,200

$664,100

a$11,900 1.40; b($213,500 – $11,900) 1.40

5. Writing off all of the underallocated overhead to Cost of Goods Sold (CGS) is warranted when

CGS is large relative to Work–in-Process Inventory and Finished Goods Inventory and the

underallocated overhead is immaterial. Both these conditions apply in this case. InStep Company

should write off the $3,200 underallocated overhead to Cost of Goods Sold account.

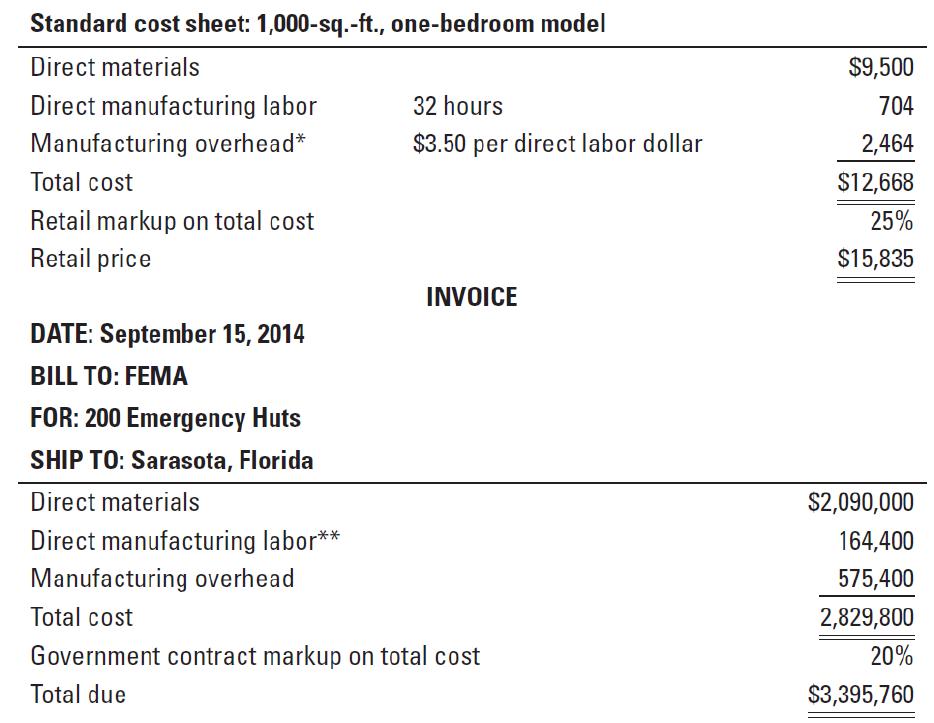

4-40 (25-30 min.) Job costing, contracting, ethics.

Rand Company manufactures modular homes. The company has two main products that it sells

commercially: a 1,000-square-foot, one-bedroom model and a 1,500-square-foot, two-bedroom

model. The company recently began providing emergency housing (huts) to the Federal

Emergency Management Agency (FEMA). The emergency housing is similar to the 1,000-square-

foot model.

FEMA has requested Rand to create a bid for 150 emergency huts to be sent for wildfire

victims in the West. Your manager has asked that you prepare this bid. In preparing the bid, you

find a recent invoice to FEMA for 200 huts provided during the most recent hurricane season in

the South. You also have a standard cost sheet for the 1,000-square-foot model sold commercially.

Both are provided as follows:

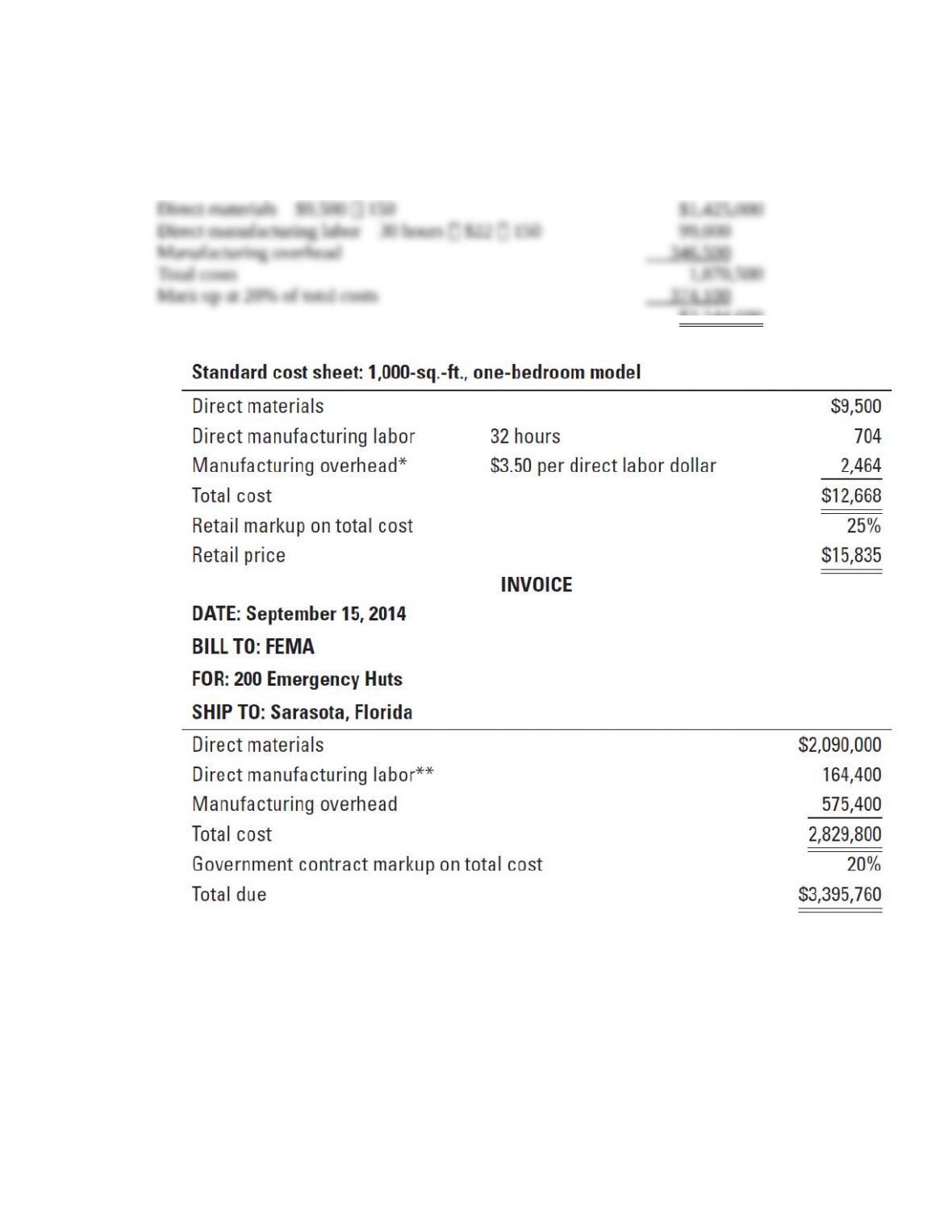

1.

Direct manufacturing costs:

Direct materials ($9,500 150 huts)

Direct manufacturing labor ($704 150 huts)

Manufacturing overhead (3.50 $105,600)

Total costs

Markup (20% $1,900,200)

Total bid price

$1,425,000

105,600

369,600

$1,900,200

380,040

$2,280,240

2.

Direct manufacturing costs:

Direct materials

Direct manufacturing labor

Manufacturing overhead

Total costs

Markup (20% of $2,122,350)

Total bid price

$1,567,500

123,300

431,550

$2,122,350

424,470

$2,546,820

Direct materials = ($2,090,000/200) 150 = $1,567,500

Direct manufacturing labor

$164,400 150 huts = $123,300

200 huts

=

Manufacturing overhead = (3.50 $123,300) = $431,550

3. The main discrepancies in costs (before the mark up) in requirements 1 and 2 are as follows:

a. Materials are marked up by 10% in the Sept. 15, 2014, invoice.

($1,567,500 – $1,425,000)/$1,425,000 = 10%.

b. Costs are double-counted based on the Sept. 15, 2014, invoice (inspection and setup

costs are included as both a direct cost as part of direct manufacturing labor and in

manufacturing overhead allocated at 3.5 times direct manufacturing labor cost).

c. The standard cost sheet includes 32 direct manufacturing labor hours, while the

Sept. 15, 2014, invoice includes 30 hours of production labor.

4. According to the IMA Standards of Ethical Conduct for Practitioners of Management

Accounting and Financial Management, the following principles should guide your decision

to present the bid based on the retail cost of producing the huts:

a. Competence—responsibility to provide information that is accurate.

b. Integrity—refraining from engaging in any conduct that would prejudice carrying out

duties ethically or that would discredit the profession.

c. Credibility—disclose all relevant information.

I would go to my boss with the bid in requirement 1 after checking

(a) If any direct material savings is possible and