1) The NPV method is the preferred method over IRR for selecting projects because

________.

A) its use leads to shareholder value maximization

B) it accounts for the time value of money

C) it assumes that cash flows are reinvested at the internal rate of return

D) it gives a project ranking consistent with that of IRR

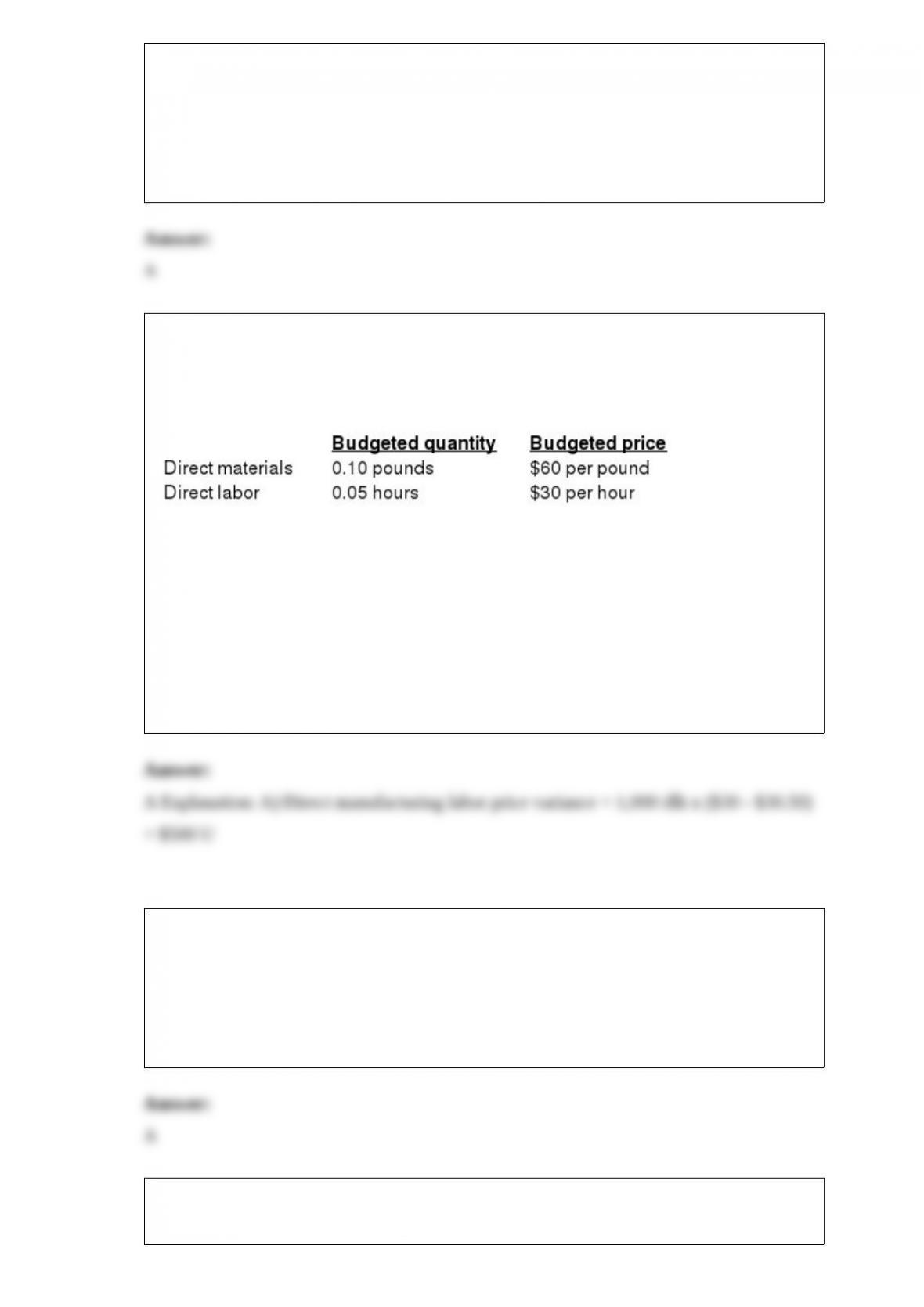

2) Animent Industries, Inc. (AII), developed standard costs for direct material and direct

labor. In 2015, AII estimated the following standard costs for one of their major

products, the 10-gallon plastic container.

During June, AII produced and sold 20,000 containers using 1,900 pounds of direct

materials at an average cost per pound of $64 and 1,000 direct manufacturing

labor-hours at an average wage of $30.50 per hour.

The direct manufacturing labor price variance during June is ________.

A) $500 unfavorable

B) $500 favorable

C) $7,600 unfavorable

D) 1,600 unfavorable

3) The slope of the line of regression is the ________.

A) rate at which the dependent variable varies

B) rate at which the independent variable varies

C) difference between the fixed cost and variable cost associated with the cost driver

D) difference between actual cost and estimated cost for each observation of the cost

driver

4) To complete the first setup on a new machine took an employee 300 minutes. Using

an 85% cumulative average-time learning curve indicates that the second setup on the

new machine is expected to take ________.

A) 127.50 minutes

B) 210 minutes

C) 277.50 minutes

D) 255 minutes

5) Managers who feel that top management does not believe in the budget are most

likely to ________.

A) pick up the slack and participate in the budgeting process

B) to face little interference in the day-to-day aspects of running the business

C) be inactive participants in the budgeting process

D) convert the budget to a shorter more reasonable time period

6) LaCrosse Products has a budget of $900,000 in 2015 for prevention costs. If it

decides to automate a portion of its prevention activities, it will save $80,000 in

variable costs. The new method will require $40,000 in training costs and $100,000 in

annual equipment costs. Management is willing to adjust the budget for an amount up

to the cost of the new equipment. The budgeted production level is 150,000 units.

Appraisal costs for the year are budgeted at $600,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $15 per failed unit of

finished goods. The internal failure rate is expected to be 3% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $54 per failed unit. The company’s

average external failures average 3% of units sold. The new proposal will reduce this

rate by 50%. Assume all units produced are sold and there are no ending inventories.

What is the net change in the budget for prevention costs if the procedures are

automated in 2015? Will management agree with the changes?

A) $60,000 decrease, yes

B) $60,000 increase, yes

C) $140,000 increase, no

D) $80,000 decrease, yes

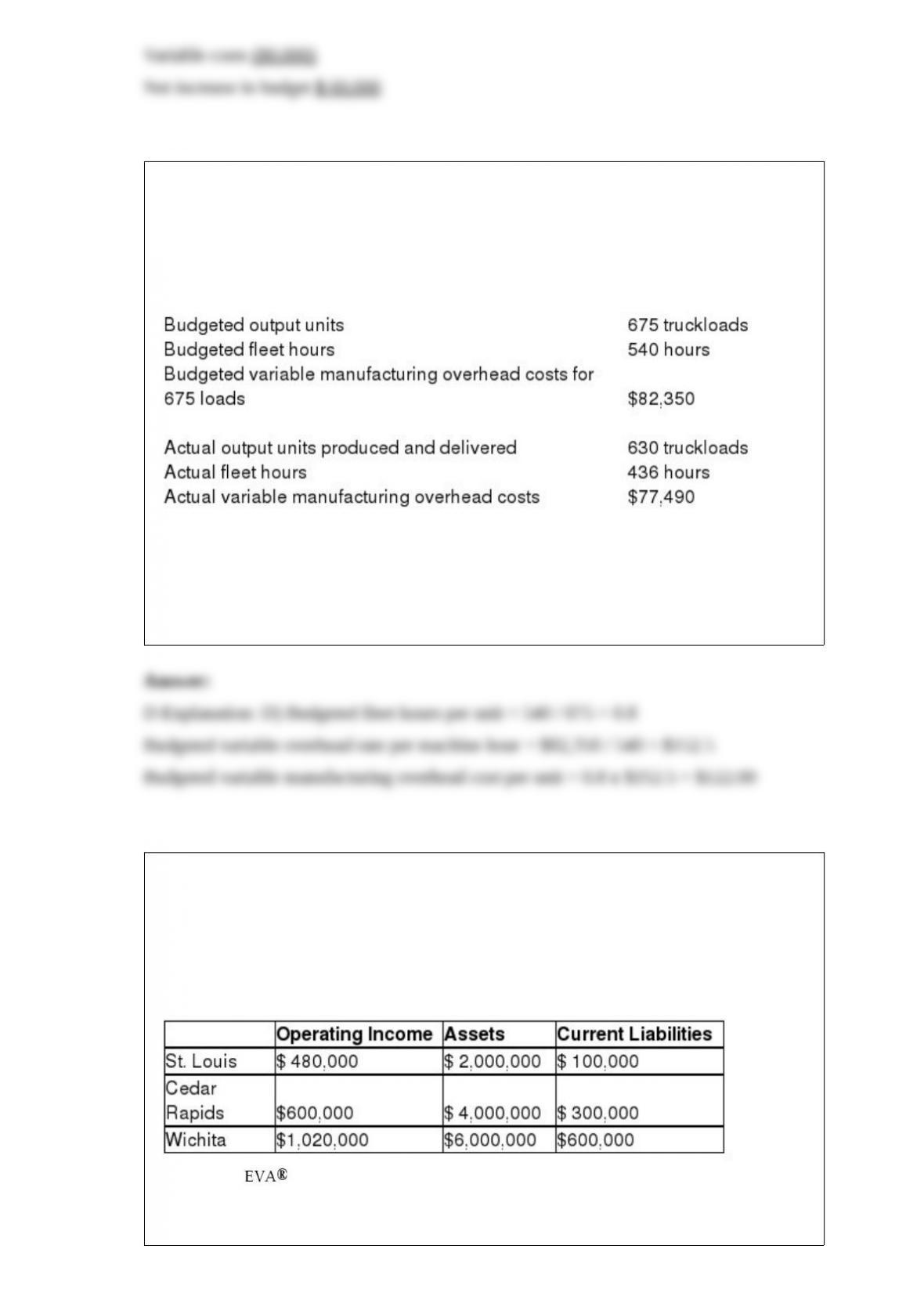

7) Mynarc Corporation produces fertilizer and distributes the product by using his

tanker trucks. Mynarc

uses budgeted fleet hours to allocate variable manufacturing overhead. The following

information pertains to the company’s manufacturing overhead data:

What is the budgeted variable manufacturing overhead cost per unit?

A) $183.00 per unit

B) $178.89 per unit

C) $119.25 per unit

D) $122.00 per unit

8) Waldorf Company has two sources of funds: long-term debt with a market and book

value of $5 million issued at an interest rate of 12%, and equity capital that has a

market value of $4 million (book value of $2 million). Waldorf Company has profit

centers in the following locations with the following operating incomes, total assets,

and current liabilities. The cost of equity capital is 12%, while the tax rate is 25%.

What is the for Wichita?

A) $225,000

B) $765,000

C) $207,180

D) $557,820

9) The approach often used when dealing with small amounts of underallocated or

overallocated overhead is the ________.

A) adjusted allocation-rate approach

B) proration approach

C) write-off to cost of goods sold approach

D) adjusted write-off approach

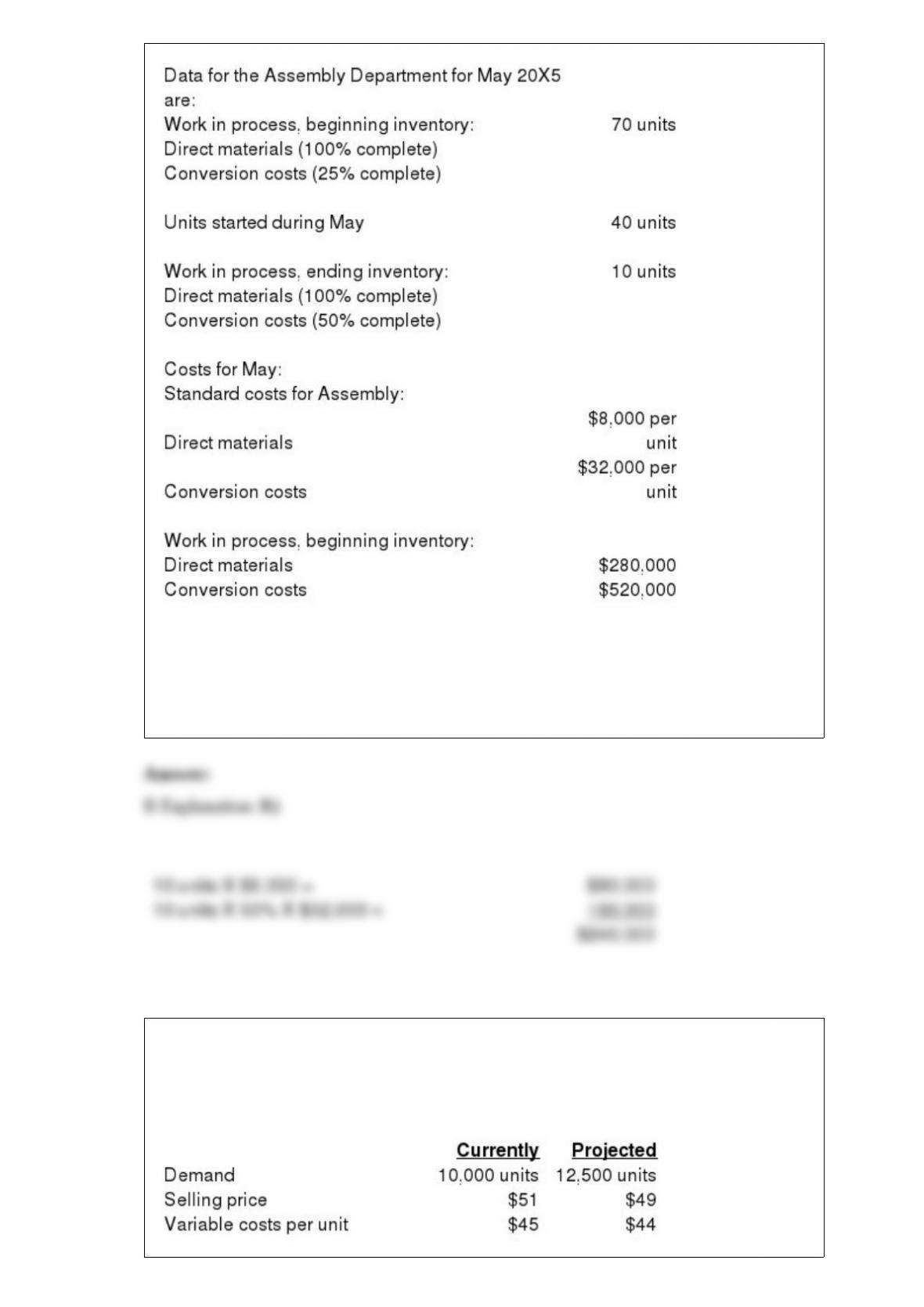

10) Emerging Dock Company manufactures boat docks on an assembly line. Its

standard costing system uses two cost categories, direct materials and conversion costs.

Each product must pass through the Assembly Department and the Finishing

Department. Direct materials are added at the beginning of the production process.

Conversion costs are allocated evenly throughout production.

What is the balance in ending work-in-process inventory?

A) $164,000

B) $240,000

C) $310,000

D) $340,000

11) Velim Electronics manufactures electric shavers and is considering decreasing the

price by $2 a unit for the coming year. With a $2 price decrease, the unit demand is

expected to increase by 25%, and a high volume materials discount is expected to

decrease the variable costs per unit by $1 per unit.

Would you recommend the $2 price decrease?

A) Yes, because demand decreases.

B) No, because the selling price decreases.

C) Yes, because operating income increases.

D) No, because contribution margin per unit increases.

12) Aurous Incorporated planned to use $35 of material per unit but actually used $34

of material per unit, and planned to make 1,500 units but actually made 1,300 units.

The flexible-budget variance for materials is ________.

A) $1,500 favorable

B) $1,500 unfavorable

C) $1,300 unfavorable

D) $1,300 favorable

13) The cost of factory machinery purchased last year is:

A) an opportunity cost.

B) a differential cost.

C) a direct materials cost.

D) a sunk cost.