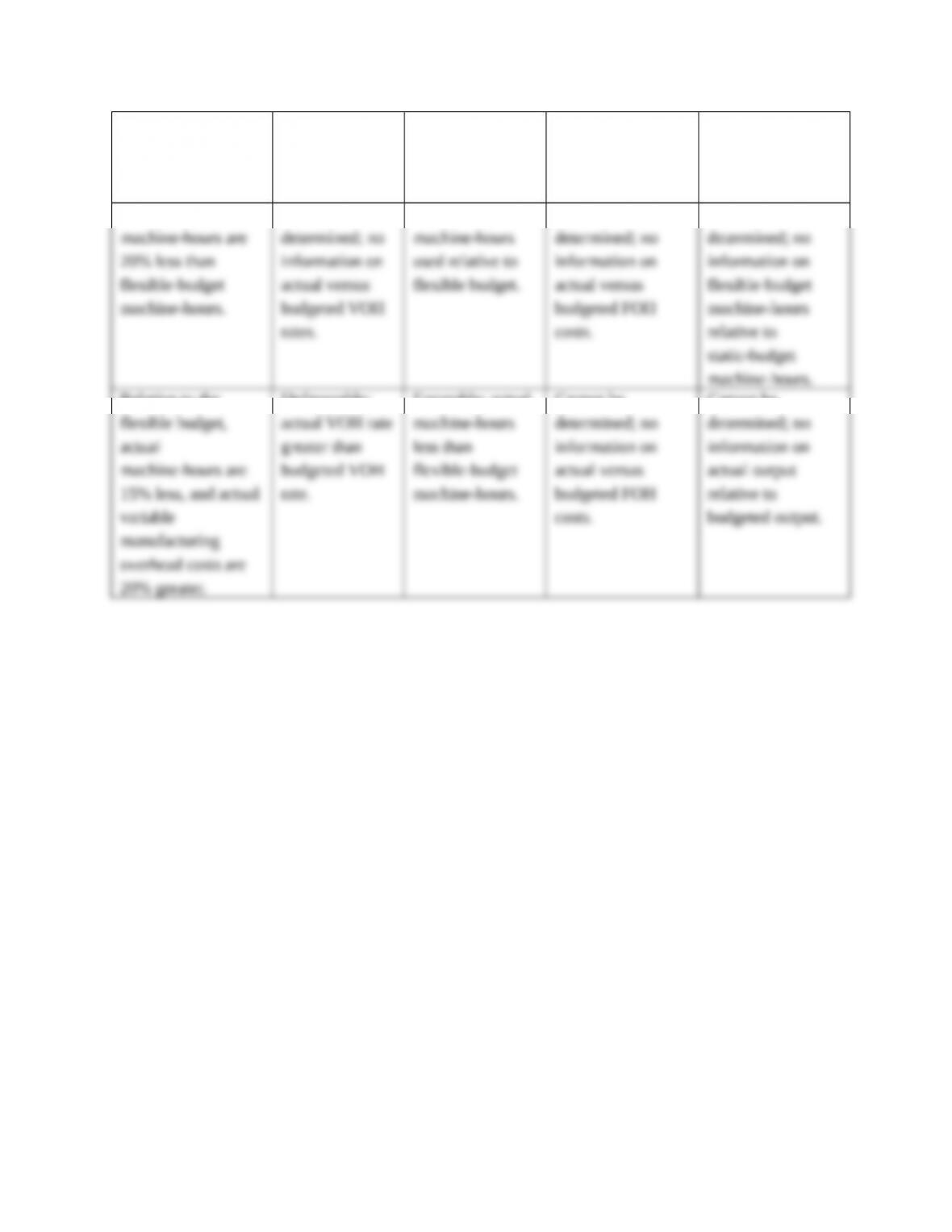

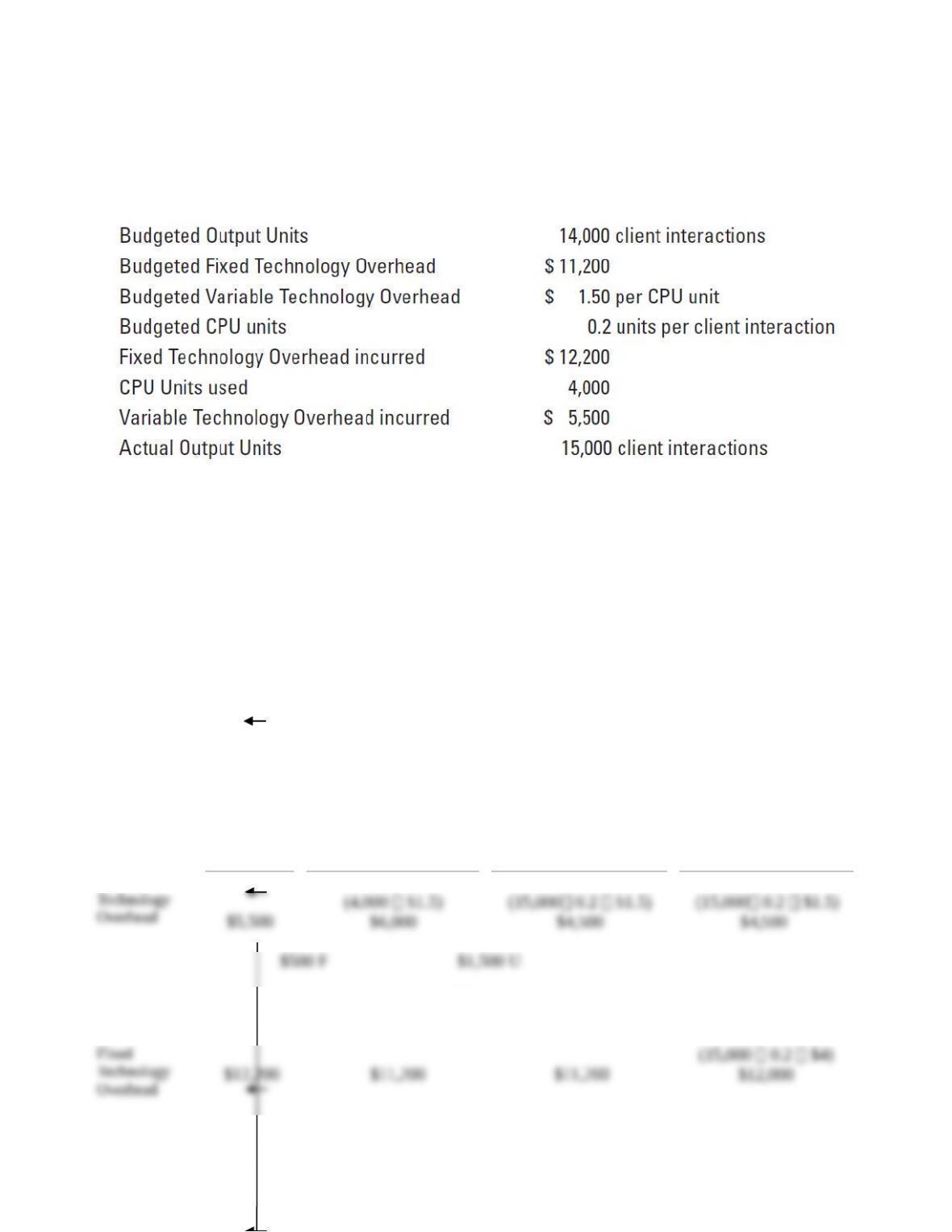

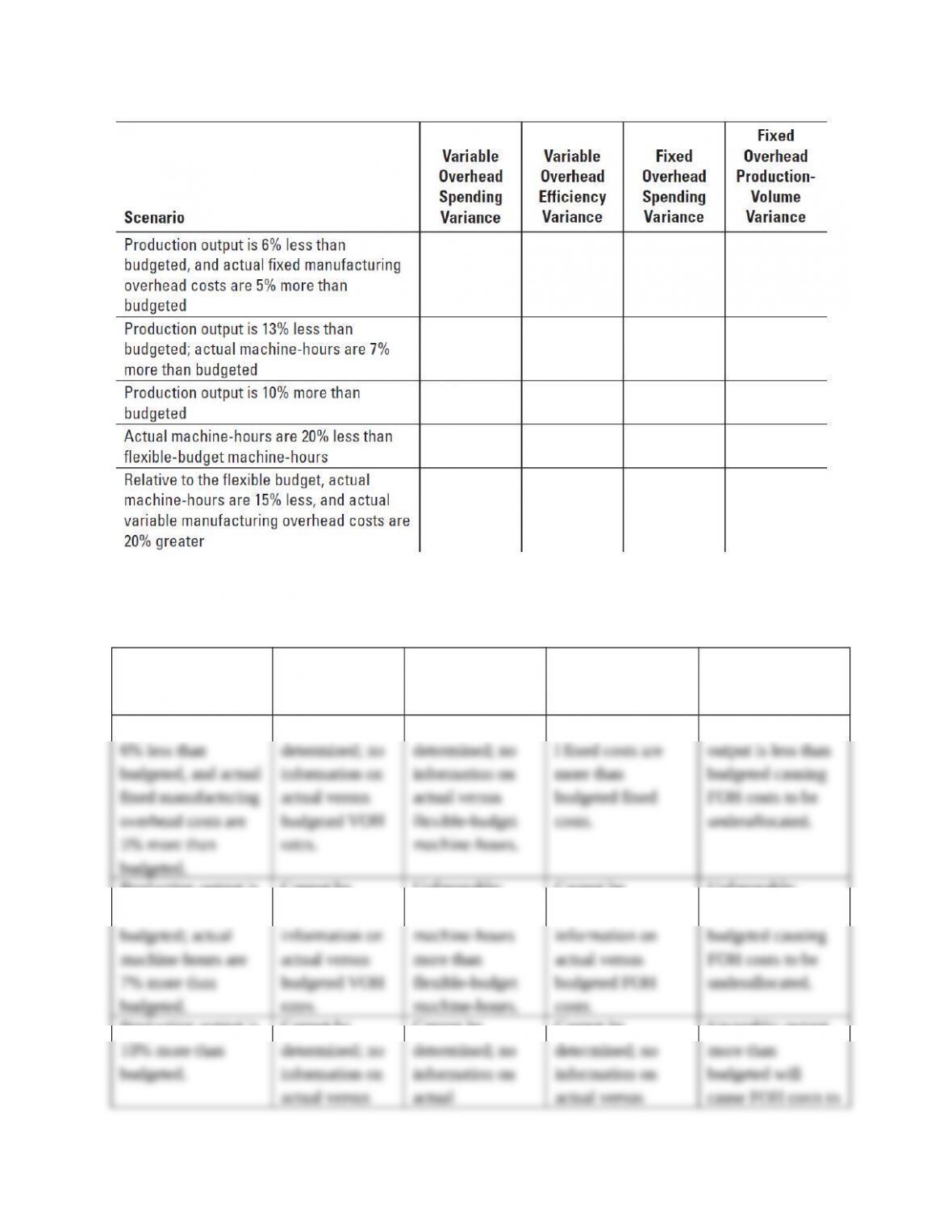

Production output is

13% less than

budgeted; actual

machine-hours are

7% more than

budgeted.

Cannot be

determined; no

information on

actual versus

budgeted VOH

rates.

Unfavorable;

actual machine-

hours more than

flexible-budget

machine-hours.

Cannot be

determined; no

information on

actual versus

budgeted FOH

costs.

Unfavorable;

output is less than

budgeted causing

FOH costs to be

underallocated.

Production output is

10% more than

budgeted.

Cannot be

determined; no

information on

actual versus

budgeted VOH

rates.

Cannot be

determined; no

information on

actual machine-

hours versus

flexible-budget

machine-hours.

Cannot be

determined; no

information on

actual versus

budgeted FOH

costs.

Favorable; output

more than

budgeted will

cause FOH costs to

be overallocated.

Actual machine-

hours are 20% less

than flexible-budget

machine-hours.

Cannot be

determined; no

information on

actual versus

budgeted VOH

rates.

Favorable; less

machine-hours

used relative to

flexible budget.

Cannot be

determined; no

information on

actual versus

budgeted FOH

costs.

Cannot be

determined; no

information on

flexible-budget

machine-hours

relative to static-

budget machine-

hours.

Relative to the

flexible budget,

actual machine-

hours are 15% less,

and actual variable

manufacturing

overhead costs are

20% greater.

Unfavorable;

actual VOH rate

greater than

budgeted VOH

rate.

Favorable; actual

machine-hours

less than flexible-

budget machine-

hours.

Cannot be

determined; no

information on

actual versus

budgeted FOH

costs.

Cannot be

determined; no

information on

actual output

relative to

budgeted output.