1) Job costing system is an example of absorption costing.

2) When calculating the equivalent units, we should only focus on dollar amounts of

inventory.

3) Discretionary costs are not easily controllable compared to engineered costs.

4) There is a direct cause-and effect relationship between division-sustaining costs and

customer or sales manager’s actions.

5) When making decisions for product mix or and pricing, the focus should be on total

costs and not unit costs.

6) Managers track the costs incurred in each value-chain category is to reduce costs and

to improve efficiency.

7) If companies increase market share in a given product line because their reported

costs are less than their actual costs, they will become more profitable in the long run.

8) The cost leadership strategy is best for a company if the engineering staff is more

skilled at creatively designing new products than at making process improvements.

9) The net realizable value (NRV) method allocates joint costs to joint products

produced during the accounting period on the basis of their relative NRVfinal sales

value plus separable costs.

10) A production cost worksheet is used to summarize total costs to account for,

compute cost per equivalent unit, and assign total costs to units completed and to units

in ending work-in-process.

11) Breakeven point is the point at which operating income is zero.

12) Gathering information before making a decision leads to a wastage of time and is

not helpful.

13) As cash flows and time value of money are central to capital budgeting decisions,

the AARR method is regarded as better than the IRR method.

14) Reverse engineering is a systematic evaluation of all aspects of the value chain with

the objective of reducing costs.

15) The contribution-margin format of the income statement is used with absorption

costing.

16) Antique Brass Company has budgeted sales volume of 120,000 units and budgeted

production of 108,000 units, while 20,000 units are in beginning finished goods

inventory. How many units are targeted for ending finished goods inventory?

A) 20,000 units

B) 32,000 units

C) 12,000 units

D) 8,000 units

17) ________ describes when a resource is consumed or benefit forgone to meet a

specific objective.

A) Cost incurrence

B) Locked-in cost

C) Resource utilization

D) Designed-in cost

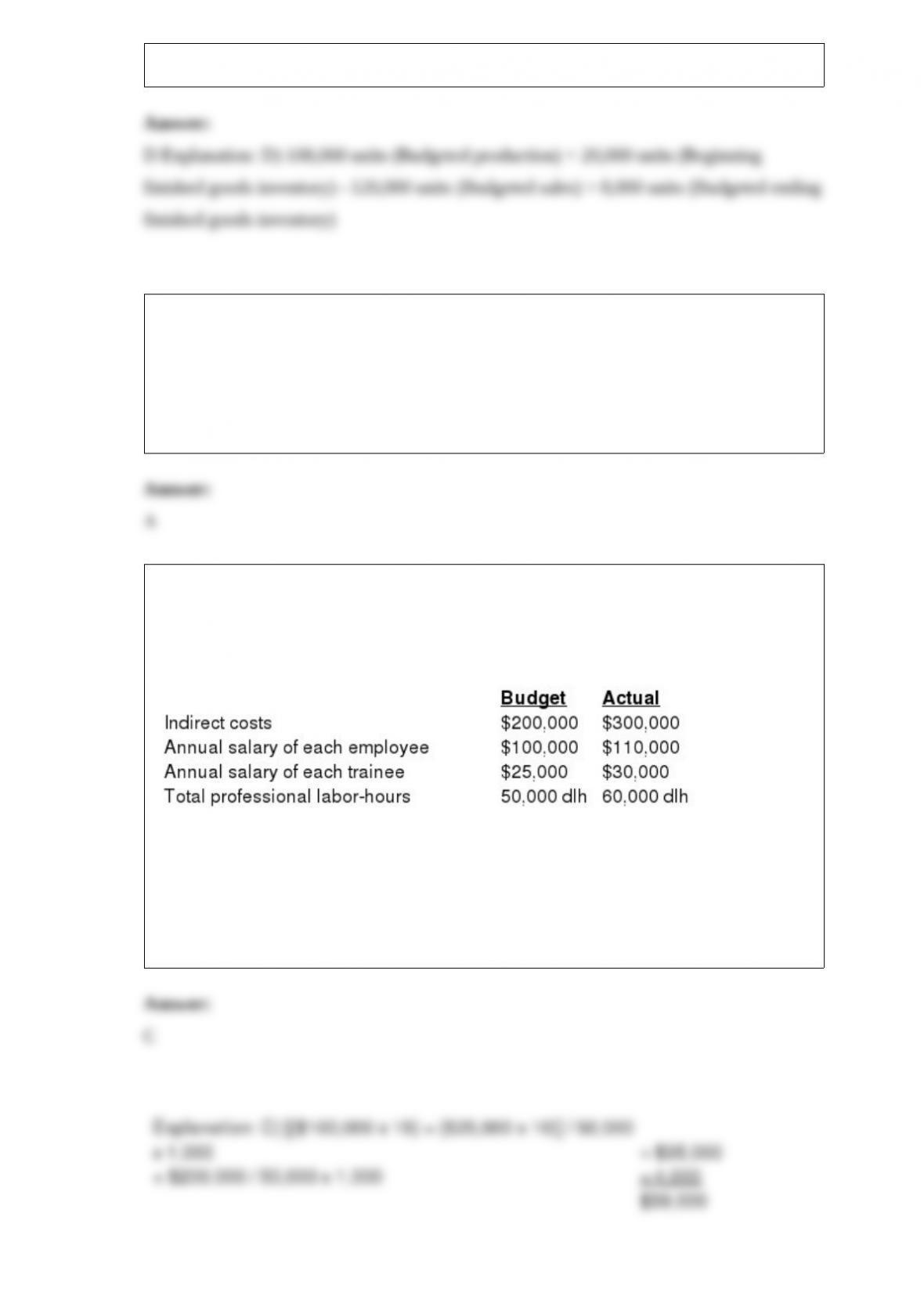

18) Mark Papers employs 15 full-time employees and 10 trainees. Direct and indirect

costs are applied on a professional labor-hour basis that includes both employee and

trainee hours. Following is information for 2014:

How much should a client be billed in a normal costing system when 1,000 professional

labor-hours are used?

A) $33,600

B) $29,800

C) $39,000

D) $41,000

19) Which of the following is a limitation of AARR method?

A) It is difficult to compare projects as its result is expressed in dollars and not in

percentage terms.

B) It does not consider income earned throughout a project’s expected useful life.

C) It does not track initial investment.

D) It does not consider time value of money.

20) The Materials Control account is increased when ________.

A) direct materials are purchased

B) indirect materials are sold

C) materials are requisitioned for production

D) materials are converted to finished goods

21) ________ occurs when revenues are related to a particular revenue object but

cannot be traced to it in an economically feasible (cost-effective) way.

A) Revenue estimation

B) Revenue allocation

C) Resource allocation

D) Revenue optimization

22) Luke employs 20 professional cleaners. Budgeted costs total $1,800,000 of which

$1,550,000 is direct costs. Budgeted indirect costs are $750,000 and actual indirect

costs were $795,800. Budgeted professional labor-hours are 1,000,000 and actual hours

were 1,218,000. What is the budgeted direct cost-allocation rate?

A) $1.80 per hour

B) $1.7857 per hour

C) $0.75 per hour

D) $1.55 per hour

23) ________ are the subdivisions of income that management accountants use for the

strategic analysis of operating income.

A) Growth, price-recovery and cost leadership components

B) Growth, price-recovery and productivity components

C) Cost leadership, price-recovery and productivity components

D) Growth, cost leadership and productivity components

24) For a company which produce its products in batches, the CEO’s salary is a(n)

________ cost.

A) batch-level

B) output unit-level

C) facility-sustaining

D) product-sustaining

25) Which of the following statements is true of the methods for allocating joint costs?

A) The sales value at splitoff method lacks a common basis for allocating joint costs to

products.

B) The complexity of the sales value at splitoff method increases when managers make

frequent changes to the sequence of post-splitoff processing decisions.

C) The NRV method assumes that none of the markup is attributable to the separable

costs.

D) The NRV method treats the joint products as though they comprise a single product.

26) Eliminating excess capacity is an initiative to achieve the ________ perspective

under a balanced scorecard.

A) marketing

B) customer

C) learning and growth

D) internal-business-process

27) Which of the following is a benefit of budgeting?

A) It helps investors to value stocks.

B) It helps managers gather information for improving future performance.

C) It helps managers to take marketing decisions.

D) It helps in increasing market capitalization of the company.