Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Gross margin

$217,000

$592,000

$809,000

Gross margin percentage

51%

53%

52%

2. Sandra Dashel probably performed the analysis shown below to arrive at the net loss of

$2,435 from marketing the stock:

PANEL A: Allocation of Joint Costs using

Sales Value at Splitoff

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen

Stock

Total

Sales value of total production at splitoff point

(20,000 tons

$5 per ton; 28,000

$20 per

ton; 6,000

$4 per ton)

$100,000

$560,000

$24,000

$684,000

Weighting

($100,000; $560,000; $24,000 ÷ $684,000)

14.6199%

81.8713%

3.5088%

100%

Joint costs allocated

(0.146199; 0.818713; 0.035088

$400,000)

$58,480

$327,485

$14,035

$400,000

PANEL B: Product-Line Income Statement

for June 2014

Special B

Special S

Stock

Total

Revenues

(25,000 tons

$17 per ton; 34,000

$33 per

ton; 6,000

$4 per ton)

$425,000

$1,122,000

$24,000

$1,571,000

Separable processing costs

100,000

238,000

0

338,000

Joint costs allocated (from Panel A)

58,480

327,485

14,035

400,000

Gross margin

$266,520

$556,515

$9,965

$833,000

Deduct marketing costs

12,400

12,400

Operating income

$ (2,435)

$820,600

In this (misleading) analysis, the $400,000 of joint costs are reallocated between Special B, Special

S, and the stock. Irrespective of the method of allocation, this analysis is wrong. Joint costs are

always irrelevant in a process-further decision. Only incremental costs and revenues past the

splitoff point are relevant. In this case, the correct analysis is much simpler: The incremental

revenues from selling the stock are $24,000, and the incremental costs are the marketing costs of

$12,400. So, Fancy Foods should sell the stock—this will increase its operating income by $11,600

($24,000 – $12,400).

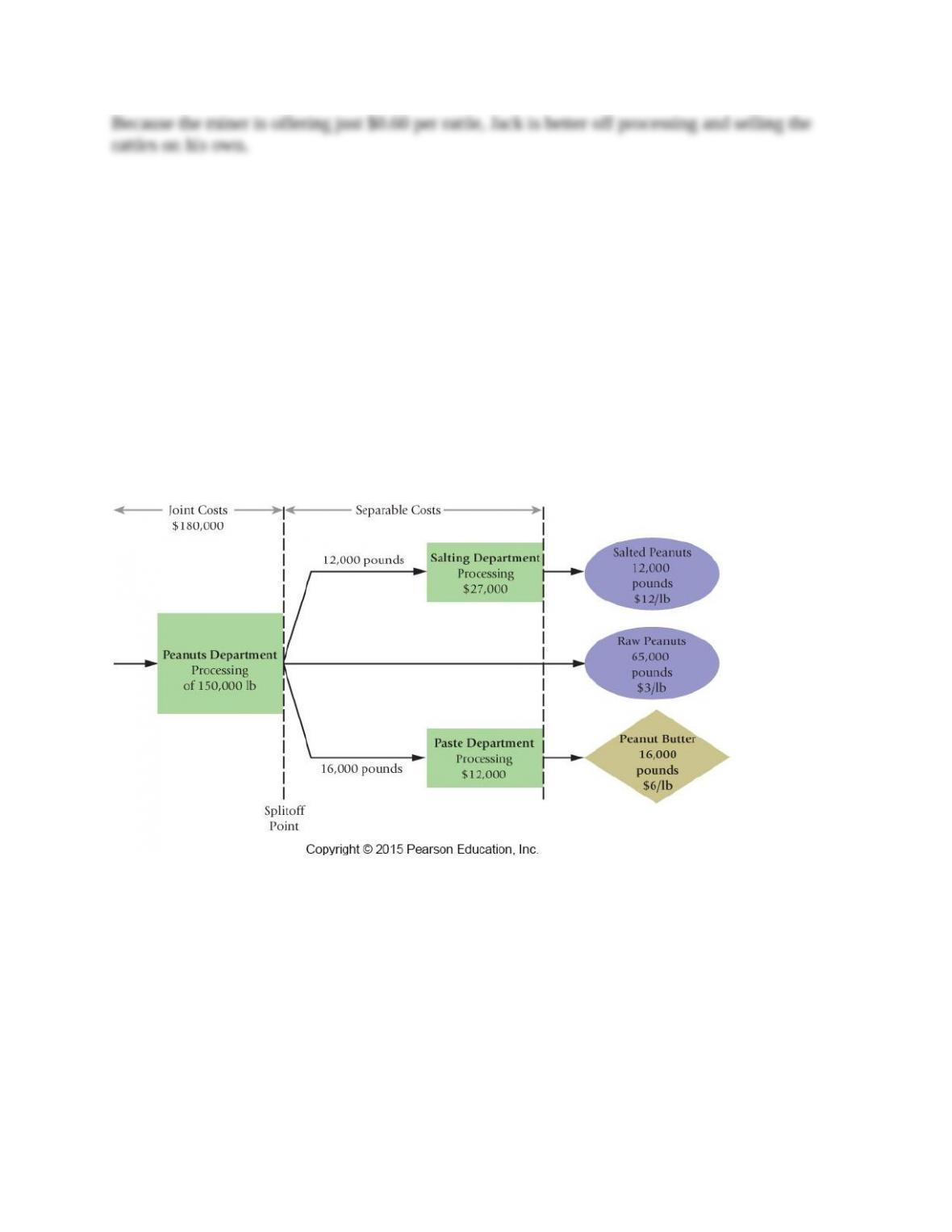

16-23 (20 min.) Joint cost allocation: sell immediately or process further.

Illinois Soy Products (ISP) buys soybeans and processes them into other soy products. Each ton

of soybeans that ISP purchases for $340 can be converted for an additional $190 into 575 pounds

of soy meal and 160 gallons of soy oil. A pound of soy meal can be sold at splitoff for $1.24 and

soy oil can be sold in bulk for $4.25 per gallon.

ISP can process the 575 pounds of soy meal into 725 pounds of soy cookies at an additional

cost of $380. Each pound of soy cookies can be sold for $2.24 per pound. The 160 gallons of soy

oil can be packaged at a cost of $240 and made into 640 quarts of Soyola. Each quart of Soyola

can be sold for $1.35.

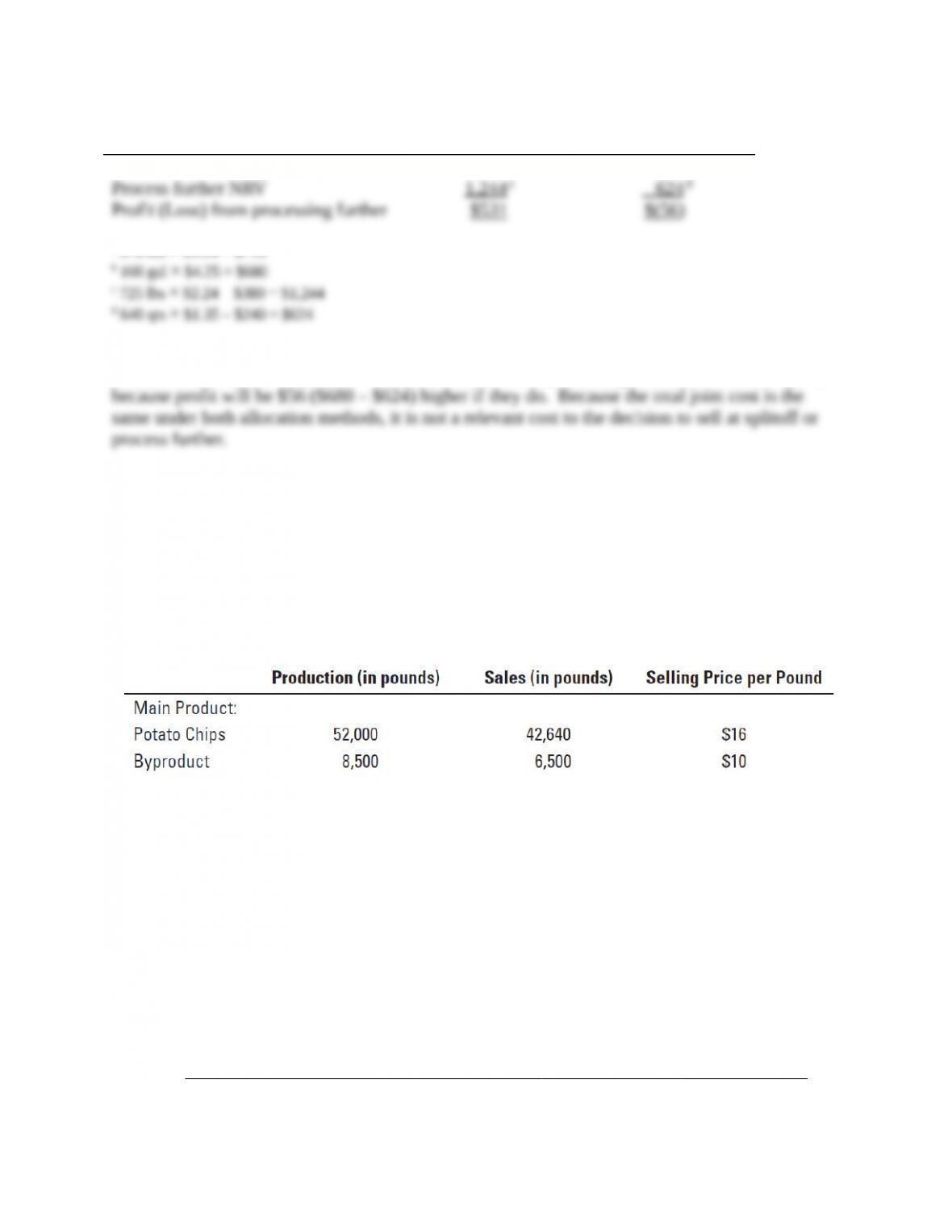

Required:

Byproduct

20,000a

0

a Ending inventory shown at unrealized selling price.

BI + Production – Sales = EI

0 + 8,500 – 6,500 = 2,000 pounds

Ending inventory = 2,000 pounds $10 per pound = $20,000

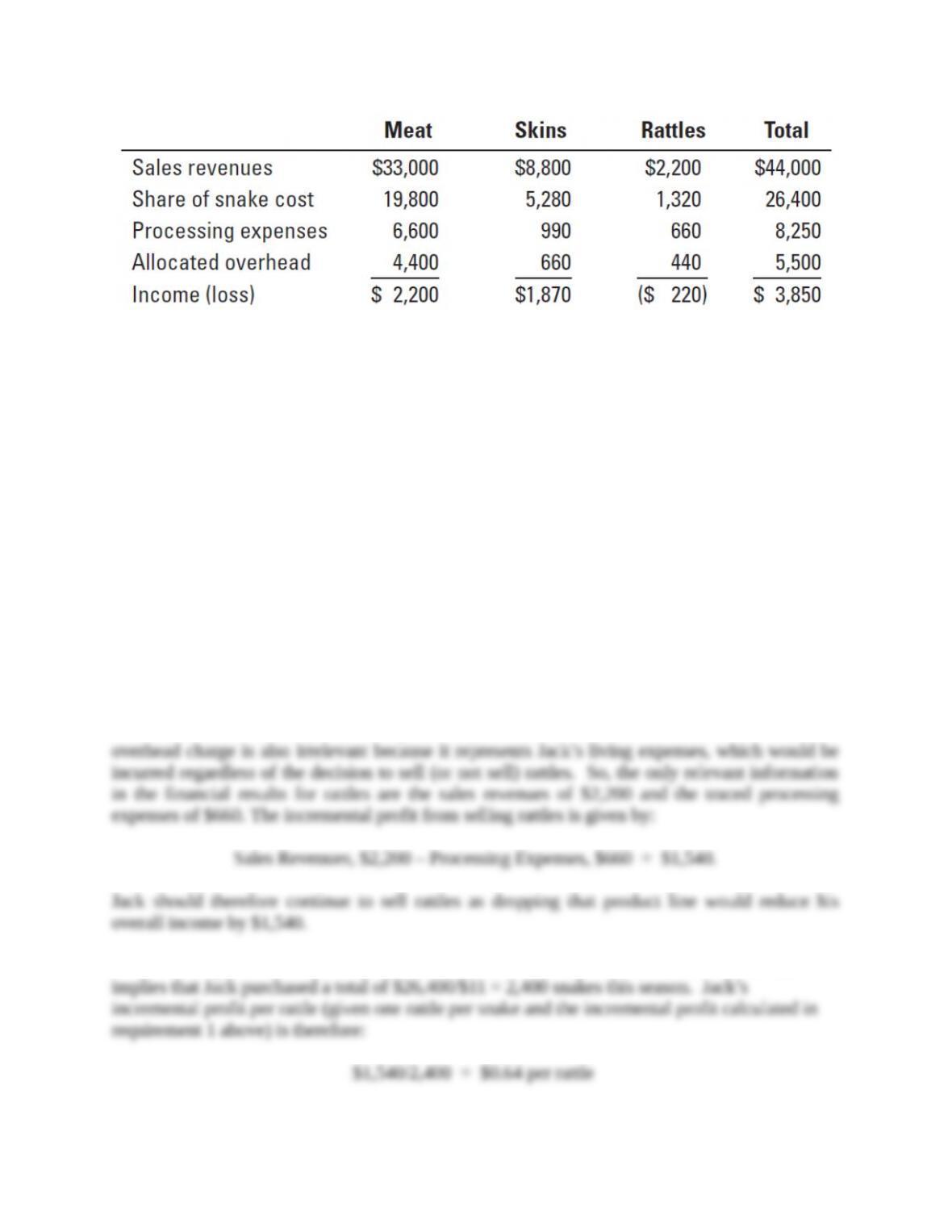

16-25 (20 min.) Joint costs and decision making.

Jack Bibby is a prospector in the Texas Panhandle. He has also been running a side business for

the past couple of years. Based on the popularity of shows such as “Rattlesnake Nation,” there has

been a surge of interest from professionals and amateurs to visit the northern counties of Texas to

capture snakes in the wild. Jack has set himself up as a purchaser of these captured snakes.

Jack purchases rattlesnakes in good condition from “snake hunters” for an average of $11 per

snake. Jack produces canned snake meat, cured skins, and souvenir rattles, although he views

snake meat as his primary product. At the end of the recent season, Jack Bibby evaluated his

financial results:

The cost of snakes is assigned to each product line using the relative sales value of meat, skins,

and rattles (i.e., the percentage of total sales generated by each product). Processing expenses are

directly traced to each product line. Overhead costs represent Jack’s basic living expenses. These

are allocated to each product line on the basis of processing expenses.

Jack has a philosophy of every product line paying for itself and is determined to cut his losses

on rattles.

Required:

1. Should Jack Bibby drop rattles from his product offerings? Support your answer with

computations.

2. An old miner has offered to buy every rattle “as is” for $0.60 per rattle (note: “as is” refers to

the situation where Jack only removes the rattle from the snake and no processing costs are

incurred). Assume that Jack expects to process the same number of snakes each season. Should

he sell rattles to the miner? Support your answer with computations.

SOLUTION