11-1

11-27 (20 min.) Relevance of equipment costs.

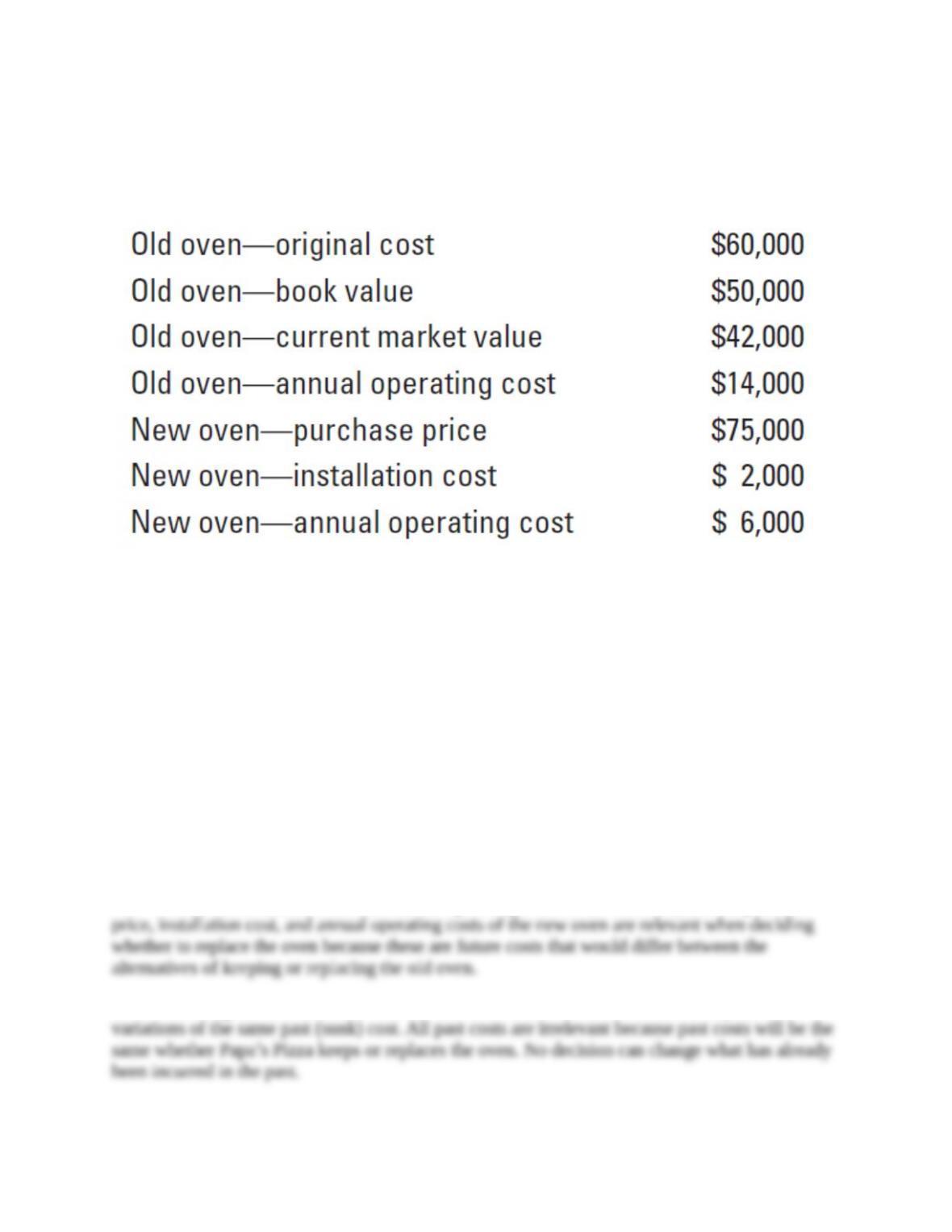

Papa’s Pizza is considering replacement of its pizza oven with a new, more energy-efficient model.

Information related to the old and new pizza ovens follows:

The old oven had been purchased a year ago. Papa’s Pizza estimates that either oven has a

remaining useful life of five years. At the end of five years, either oven would have a zero salvage

value. Ignore the effect of income taxes and the time value of money.

Required:

1. Which of the costs and benefits above are relevant to the decision to replace the oven?

2. What information is irrelevant? Why is it irrelevant?

3. Should Papa’s Pizza purchase the new oven? Provide support for your answer.

4. Is there any conflict between the decision model and the incentives of the manager who has

purchased the “old” oven and is considering replacing it a year later?

5. At what purchase price would Papa’s Pizza be indifferent between purchasing the new oven

and continuing to use the old oven?

SOLUTION

1. The current market value and annual operating costs of the old oven, and the purchase

price, installation cost, and annual operating costs of the new oven are relevant when deciding

whether to replace the oven because these are future costs that would differ between the

alternatives of keeping or replacing the old oven.

2. The original cost and book value of the old oven are irrelevant because they are

variations of the same past (sunk) cost. All past costs are irrelevant because past costs will be the

same whether Papa’s Pizza keeps or replaces the oven. No decision can change what has already

been incurred in the past.

11-2

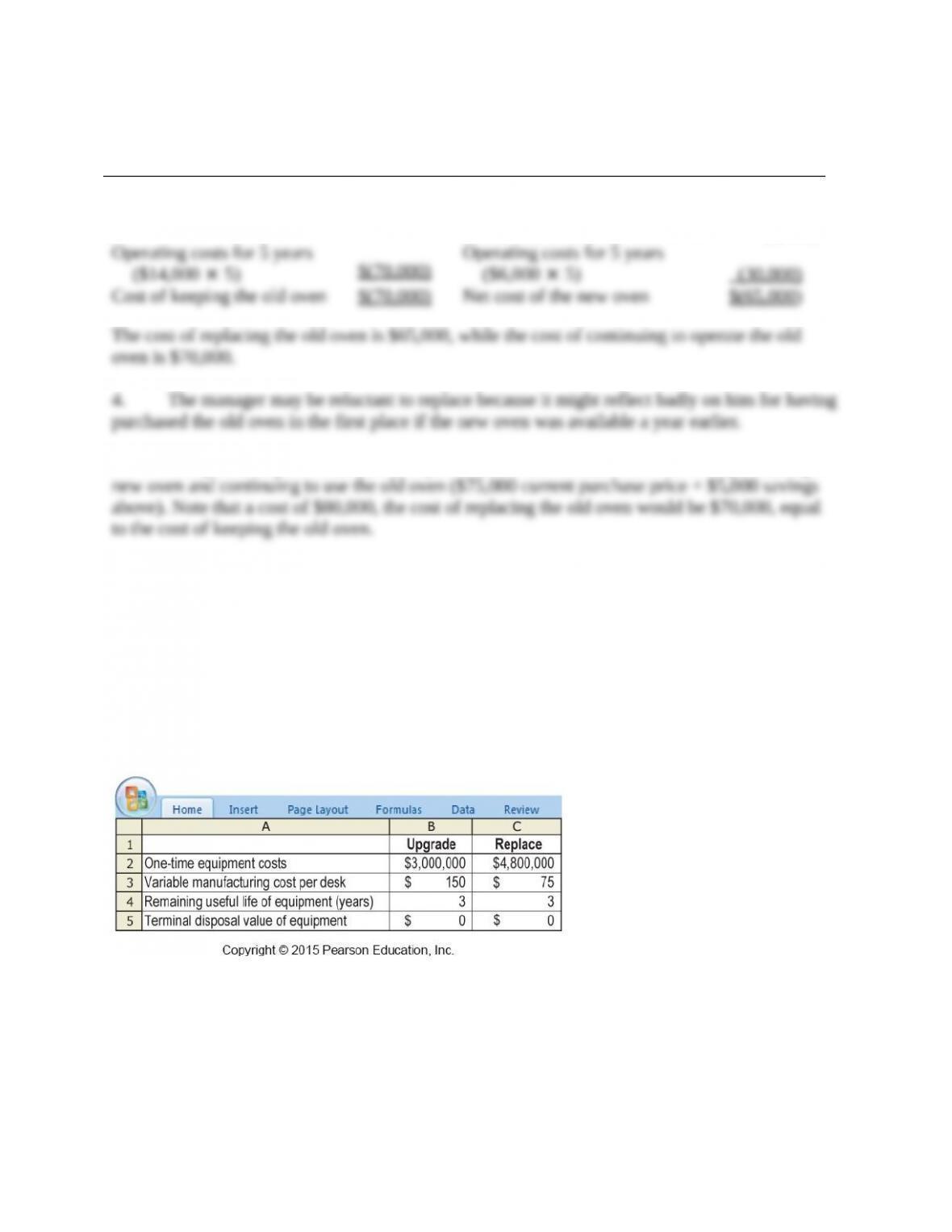

3. Papa’s Pizza should purchase the new oven, based on the following calculations:

Keep the old oven

Replace the old oven

Current market value of old oven

$ 42,000

Purchase price of the new oven

(75,000)

Installation cost of the new oven

(2,000)

Operating costs for 5 years

($14,000 × 5)

$(70,000)

Operating costs for 5 years

($6,000 × 5)

(30,000)

Cost of keeping the old oven

$(70,000)

Net cost of the new oven

$(65,000)

The cost of replacing the old oven is $65,000, while the cost of continuing to operate the old

oven is $70,000.

4. The manager may be reluctant to replace because it might reflect badly on him for having

purchased the old oven in the first place if the new oven was available a year earlier.

5. At a purchase price of $80,000, Papa’s Pizza would be indifferent between purchasing

the new oven and continuing to use the old oven ($75,000 current purchase price + $5,000

savings above). Note that a cost of $80,000, the cost of replacing the old oven would be $70,000,

equal to the cost of keeping the old oven.

11-28 (30 min.) Equipment upgrade versus replacement.

(A. Spero, adapted) The TechGuide Company produces and sells 7,500 modular computer desks

per year at a selling price of $750 each. Its current production equipment, purchased for $1,800,000

and with a five-year useful life, is only two years old. It has a terminal disposal value of $0 and is

depreciated on a straight-line basis. The equipment has a current disposal price of $450,000.

However, the emergence of a new molding technology has led TechGuide to consider either

upgrading or replacing the production equipment. The following table presents data for the two

alternatives:

All equipment costs will continue to be depreciated on a straight-line basis. For simplicity, ignore

income taxes and the time value of money.

Required:

1. Should TechGuide upgrade its production line or replace it? Show your calculations.

11-3

2. Now suppose the one–time equipment cost to replace the production equipment is somewhat

negotiable. All other data are as given previously. What is the maximum one-time equipment

cost that TechGuide would be willing to pay to replace rather than upgrade the old equipment?

3. Assume that the capital expenditures to replace and upgrade the production equipment are as

given in the original exercise, but that the production and sales quantity is not known. For what

production and sales quantity would TechGuide (i) upgrade the equipment or (ii) replace the

equipment?

4. Assume that all data are as given in the original exercise. Dan Doria is TechGuide’s manager,

and his bonus is based on operating income. Because he is likely to relocate after about a year,

his current bonus is his primary concern. Which alternative would Doria choose? Explain.

SOLUTION

1. Based on the analysis in the table below, TechGuide will be better off by $337,500 over

three years if it replaces the current equipment.

Over 3 years

Difference in

Comparing Relevant Costs of Upgrade and

Upgrade

Replace

favor of Replace

Replace Alternatives

(1)

(2)

(3) = (1) – (2)

Cash operating costs

$150; $75 per desk

7,500 desks per yr.

3 yrs.

$3,375,000

$1,687,500

$1,687,5000

Current disposal price

(450,000)

450,000

One time capital costs, written off periodically as

depreciation

3,000,000

4,800,000

(1,800,000)

Total relevant costs

$6,375,000

$6,037,500

$ 337,500

Note that the book value of the current machine, $1,800,000

3

5

= $1,080,000 would either be

written off as depreciation over three years under the upgrade option or all at once in the current

year under the replace option. Its net effect would be the same in both alternatives: to increase

costs by $1,080,000 over three years; hence, it is irrelevant in this analysis.

2. Suppose the capital expenditure to replace the equipment is $X. From requirement 1,

column (2), substituting for the one-time capital cost of replacement, the relevant cost of replacing

is $1,687,500 – $450,000 + $X. From column (1), the relevant cost of upgrading is $6,375,000.

We want to find X such that

$1,687,500 – $450,000 + $X < $6,375,000 (i.e., TechGuide will favor replacing)

Solving the above inequality gives us X < $6,375,000 – $1,237,500 = $5,137,500.

TechGuide would prefer to replace, rather than upgrade, if the replacement cost of the new

equipment does not exceed $5,137,500. Note that this result can also be obtained by taking the

original replacement cost of $4,800,000 and adding to it the $337,500 difference in favor of

replacement calculated in requirement 1.

3. Suppose the units produced and sold over 3 years equal y. Using data from requirement 1,

column (1), the relevant cost of upgrade would be $150y + $3,000,000, and from column (2), the

11-4

relevant cost of replacing the equipment would be $75y – $450,000 + $4,800,000. TechGuide

would want to upgrade when

$150y + $3,000,000 < $75y – $450,000 + $4,800,000

$75y < $1,350,000

y < $1,350,000 $75 = 18,000 units

That is, upgrade when y < 18,000 units (or 6,000 per year for 3 years) and replace when y > 18,000

units over 3 years.

When production and sales volume is low (less than 6,000 per year), the higher operating

costs under the upgrade option are more than offset by the savings in capital costs from upgrading.

When production and sales volume is high, the higher capital costs of replacement are more than

offset by the savings in operating costs in the replace option.

4. Operating income for the first year under the upgrade and replace alternatives are shown

below:

Year 1

Upgrade

Replace

(1)

(2)

Revenues (7,500

$750)

$5,625,000

$5,625,000

Cash operating costs

$150; $75 per desk

7,500 desks per year

1,125,000

562,500

Depreciation ($1,080,000a + $3,000,000)

3; $4,800,000

3

1,360,000

1,600,000

Loss on disposal of old equipment (0; $1,080,000 –

$450,000)

0

630,000

Total costs

2,485,000

2,792,500

Operating Income

$3,140,000

$2,832,500

aThe book value of the current production equipment is $1,800,000

5

3 = $1,080,000; it has a remaining

useful life of 3 years.

First-year operating income is higher by $307,500 ($3,140,000 – $2,832,500) under the upgrade

alternative, and Dan Doria, with his one-year horizon and operating income-based bonus, will

choose the upgrade alternative, even though, as seen in requirement 1, the replace alternative is

better in the long run for TechGuide. This exercise illustrates the possible conflict between the

decision model and the performance evaluation model.

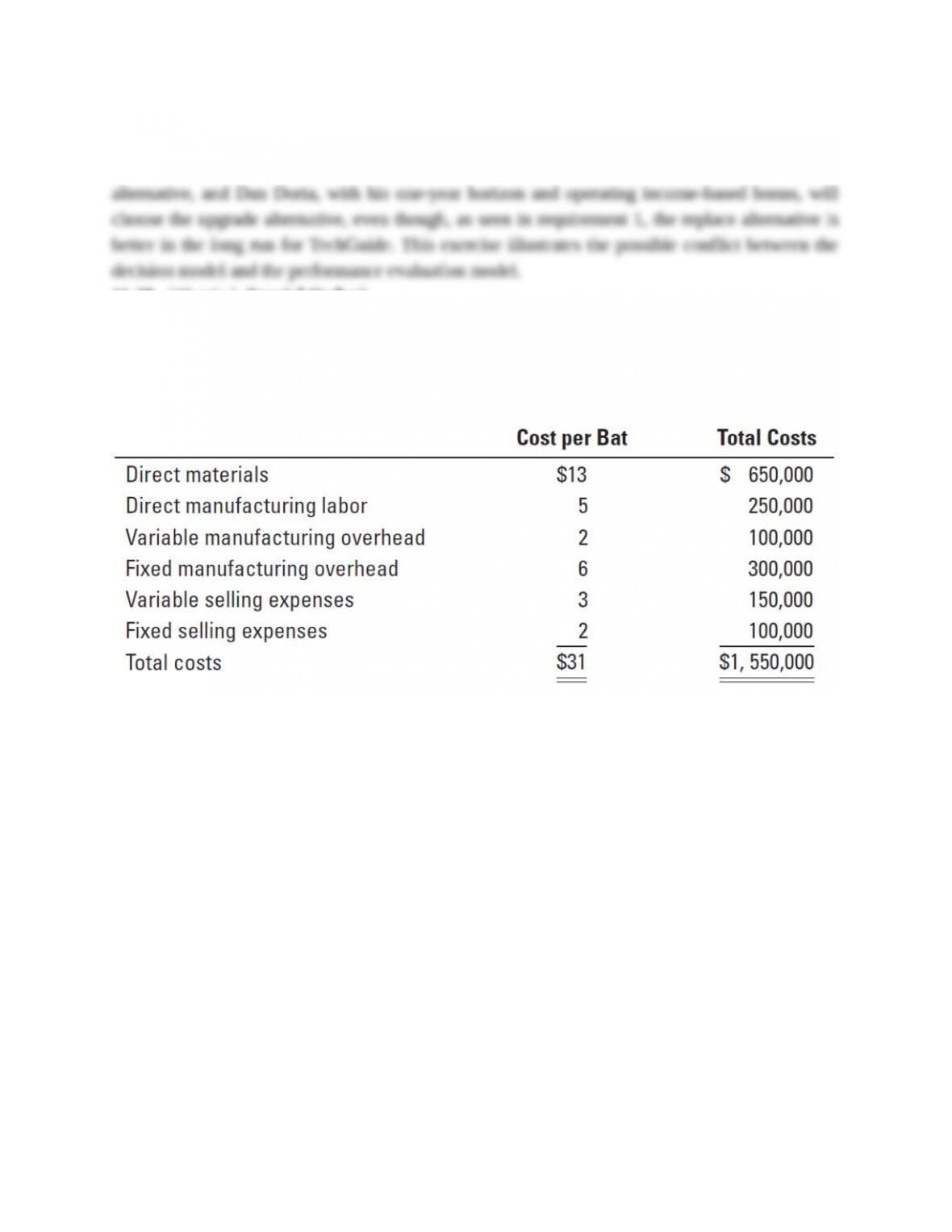

11-29 (20 min.) Special Order3

Slugger Corporation produces baseball bats for kids that it sells for $36 each. At capacity, the

company can produce 50,000 bats a year. The costs of producing and selling 50,000 bats are as

follows:

Required:

1. Suppose Slugger is currently producing and selling 40,000 bats. At this level of production and

sales, its fixed costs are the same as given in the preceding table. Bench Corporation wants to

place a one-time special order for 10,000 bats at $23 each. Slugger will incur no variable selling

costs for this special order. Should Slugger accept this one-time special order? Show your

calculations.

2. Now suppose Slugger is currently producing and selling 50,000 bats. If Slugger accepts

Bench’s offer it will have to sell 10,000 fewer bats to its regular customers. (a) On financial

considerations alone, should Slugger accept this one-time special order? Show your

calculations. (b) On financial considerations alone, at what price would Slugger be indifferent

between accepting the special order and continuing to sell to its regular customers at $36 per

bat. (c) What other factors should Slugger consider in deciding whether to accept the one-time

special order?

SOLUTION

1.

Revenues from special order ($23

10,000 bats)

$230,000

Variable manufacturing costs ($201

10,000 bats)

(200,000)

Increase in operating income if Bench order accepted

$ 30,000

1Direct materials cost per unit + Direct manufacturing labor cost per unit + Variable manufacturing overhead cost per

unit = $13 + $5 + $2 = $20

Slugger should accept Bench’s special order because it increases operating income by $30,000.

Because no variable selling costs will be incurred on this order, this cost is irrelevant. Similarly,

fixed costs are irrelevant because they will be incurred regardless of the decision.

2a. Revenues from special order ($23

10,000 bats)

$230,000

Variable manufacturing costs ($20

10,000 bats)

(200,000)

Contribution margin foregone ([$36─$231]

10,000 bats)

(130,000)

Decrease in operating income if Bench order accepted

$(100,000)

11-6

1Direct materials cost per unit + Direct manufacturing labor cost per unit + Variable manufacturing overhead cost per

unit + Variable selling expense per unit = $13 + $5 + $2 + $3 = $23

Based strictly on financial considerations, Slugger should reject Bench’s special order because it

results in a $100,000 reduction in operating income.

2b. Slugger will be indifferent between the special order and continuing to sell to regular

customers if the special order price is $33. At this price, Slugger recoups the variable

manufacturing costs of $200,000 and the contribution margin given up from regular customers of

$130,000 ([$200,000 + $130,000] ÷ 10,000 units = $33). That is, at the special order price of

$33, Slugger recoups the variable cost per unit of $20 and the contribution margin per unit given

up from regular customers of $13 per unit.

An alternative approach is to recognize that Slugger needs to earn $100,000 more than

the revenues of $230,000 in requirement 2a, so that the decrease in operating income of

$100,000 becomes $0. Slugger will be indifferent between the special order and continuing to

sell to regular customers if revenues from the special order = $230,000 + $100,000 = $330,000

or $33 per bat ($330,000 10,000 bats)

Looked at a different way, Slugger needs to earn the full price of $36 less the $3 saved on

variable selling costs.

2c. Slugger may be willing to accept a loss on this special order if the possibility of future

long-term sales seem likely at a higher price. Moreover, Slugger should also consider the

negative long-term effect on customer relationships of not selling to existing customers. Slugger

cannot afford to sell bats to customers at the special order price for the long term because the $23

price is less than the full manufacturing cost of the product of $26. This means that in the long

term, the contribution margin earned will not cover the fixed costs and result in a loss. Slugger

will then be better off shutting down.

11-30 (15-20 min.) Short-run pricing, capacity constraints.

Ohio Acres Dairy, maker of specialty cheeses, produces a soft cheese from the milk of Holstein

cows raised on a special corn-based diet. One kilogram of soft cheese, which has a contribution

margin of $8, requires 4 liters of milk. A well-known gourmet restaurant has asked Ohio Acres to

produce 2,000 kilograms of a hard cheese from the same milk of Holstein cows. Knowing that the

dairy has sufficient unused capacity, Elise Princiotti, owner of Ohio Acres, calculates the costs of

making one kilogram of the desired hard cheese:

11-7

Required:

1. Suppose Ohio Acres can acquire all the Holstein milk that it needs. What is the minimum price

per kilogram the company should charge for the hard cheese?

2. Now suppose that the Holstein milk is in short supply. Every kilogram of hard cheese Ohio

Acres produces will reduce the quantity of soft cheese that it can make and sell. What is the

minimum price per kilogram the company should charge to produce the hard cheese?

SOLUTION

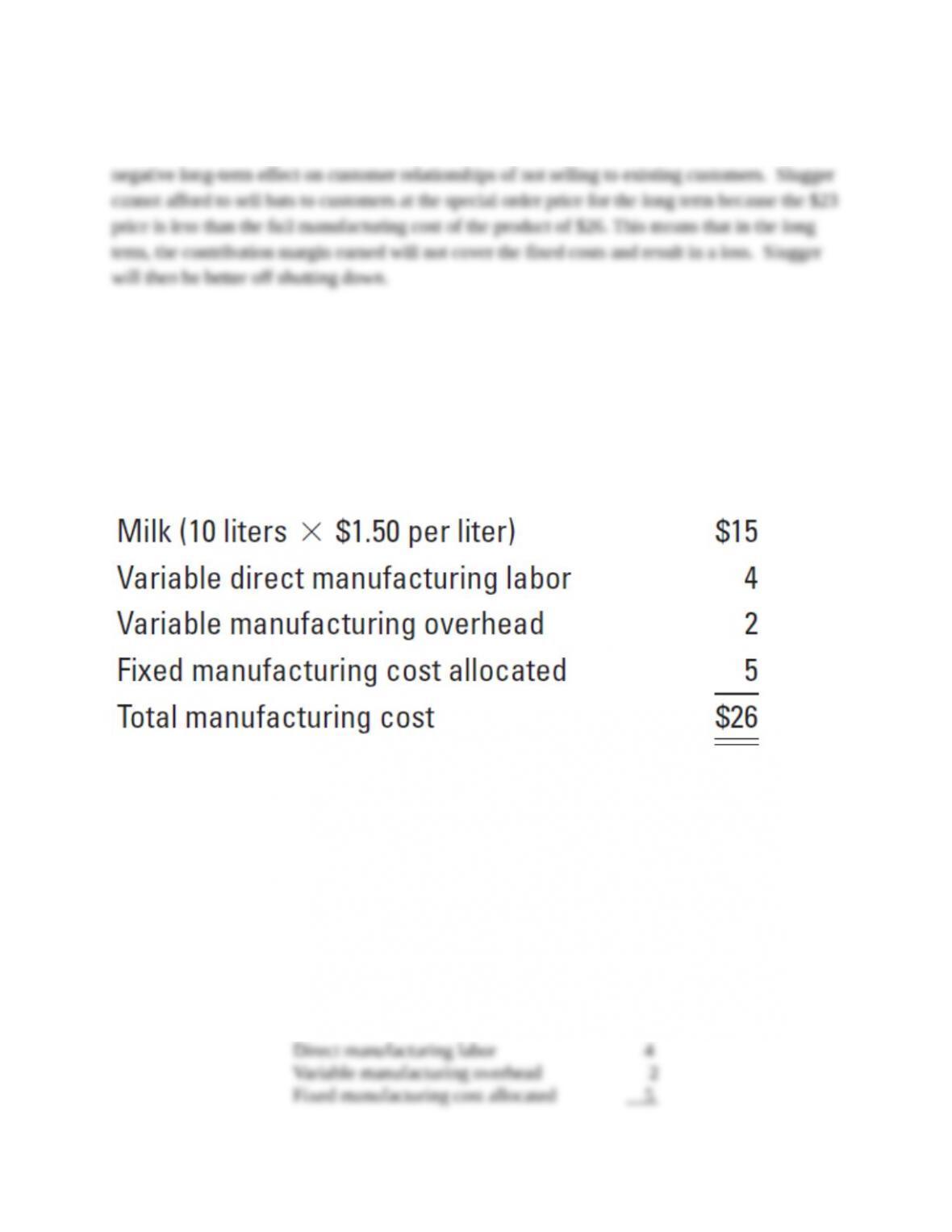

1. Per kilogram of hard cheese:

Milk (10 liters

$1.50 per liter)

$15

Direct manufacturing labor

4

Variable manufacturing overhead

2

Fixed manufacturing cost allocated

5

Total manufacturing cost

$26

If Ohio Acres Dairy can get all the Holstein milk it needs and has sufficient production capacity,

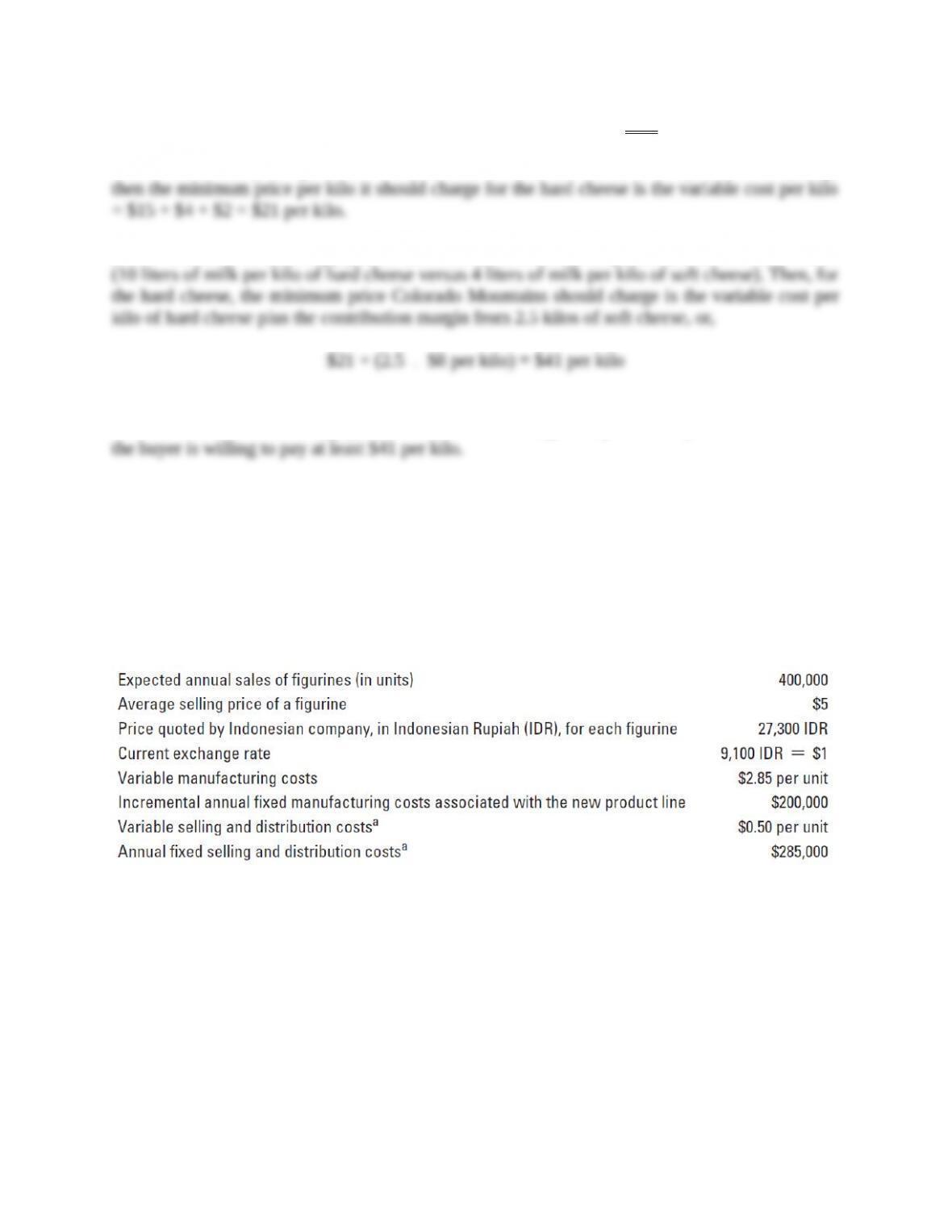

then the minimum price per kilo it should charge for the hard cheese is the variable cost per kilo =

$15 + $4 + $2 = $21 per kilo.

2. If milk is in short supply, then each kilo of hard cheese displaces 2.5 kilos of soft cheese

(10 liters of milk per kilo of hard cheese versus 4 liters of milk per kilo of soft cheese). Then, for

the hard cheese, the minimum price Colorado Mountains should charge is the variable cost per

kilo of hard cheese plus the contribution margin from 2.5 kilos of soft cheese, or,

$21 + (2.5

$8 per kilo) = $41 per kilo

That is, if milk is in short supply, Ohio Acres should not agree to produce any hard cheese unless

the buyer is willing to pay at least $41 per kilo.

11-31 (20 min.) International outsourcing.

Cuddly Critters, Inc., manufactures plush toys in a facility in Cleveland, Ohio. Recently, the

company designed a group of collectible resin figurines to go with the plush toy line. Management

11-8

is trying to decide whether to manufacture the figurines themselves in existing space in the

Cleveland facility or to accept an offer from a manufacturing company in Indonesia. Data

concerning the decision are:

a Selling and distribution costs are the same regardless of whether the figurines are manufactured

in Cleveland or imported.

Required:

1. Should Cuddly Critters manufacture the 400,000 figurines in the Cleveland facility or purchase

them from the Indonesian supplier? Explain.

2. Cuddly Critters believes that the U.S. dollar may weaken in the coming months against the

Indonesian rupiah and does not want to face any currency risk. Assume that Cuddly Critters

can enter into a forward contract today to purchase 27,300 IDRs for $3.40. Should Cuddly

Critters manufacture the 400,000 figurines in the Cleveland facility or purchase them from the

Indonesian supplier? Explain.

3. What are some of the qualitative factors that Cuddly Critters should consider when deciding

whether to outsource the figurine manufacturing to Indonesia?

SOLUTION

1. Cost to purchase each figurine from Indonesian supplier =

27,300 IDR $3.

9,100 IDR/$ =

Cost of purchasing 400,000 figurines from Indonesian supplier = $3 400,000 figurines =

$1,200,000.

Costs of

manufacturing

figurines in

Cleveland

facility

=

Variable

manufacturing

cost per unit

Quantity of

figurines

produced

+

Incremental fixed

manufacturing

costs

= ($2.85 400,000 units) + $200,000

= $1,340,000

11-9

Variable and fixed selling and distribution costs are irrelevant because they do not differ between

the two alternatives of purchasing the figurines from the Indonesian supplier or manufacturing the

figurines in Cleveland.

Cuddly Critters should purchase the figurines from the Indonesian supplier because the

cost of $1,200,000 is less than the relevant cost of $1,340,000 to manufacture the figurines in

Cleveland.

2. If Cuddly Critters enters into a forward contract to purchase 27,300 IDRs for $3.40, each

figurine acquired from the Indonesian supplier will cost $3.40.

Total cost of purchasing 400,000 figurines from Indonesian supplier = $3.40 400,000

figurines = $1,360,000.

Cost of manufacturing 400,000 figurines in Cleveland (see requirement 1) = $1,340,000.

As in requirement 1, selling and distribution costs are irrelevant.

Cuddly Critters should manufacture the figurines in Cleveland because the relevant cost of

$1,340,000 to manufacture the figurines in Cleveland is less than the cost of $1,360,000 to enter

into the forward contract and purchase the figurines from the Indonesian supplier.

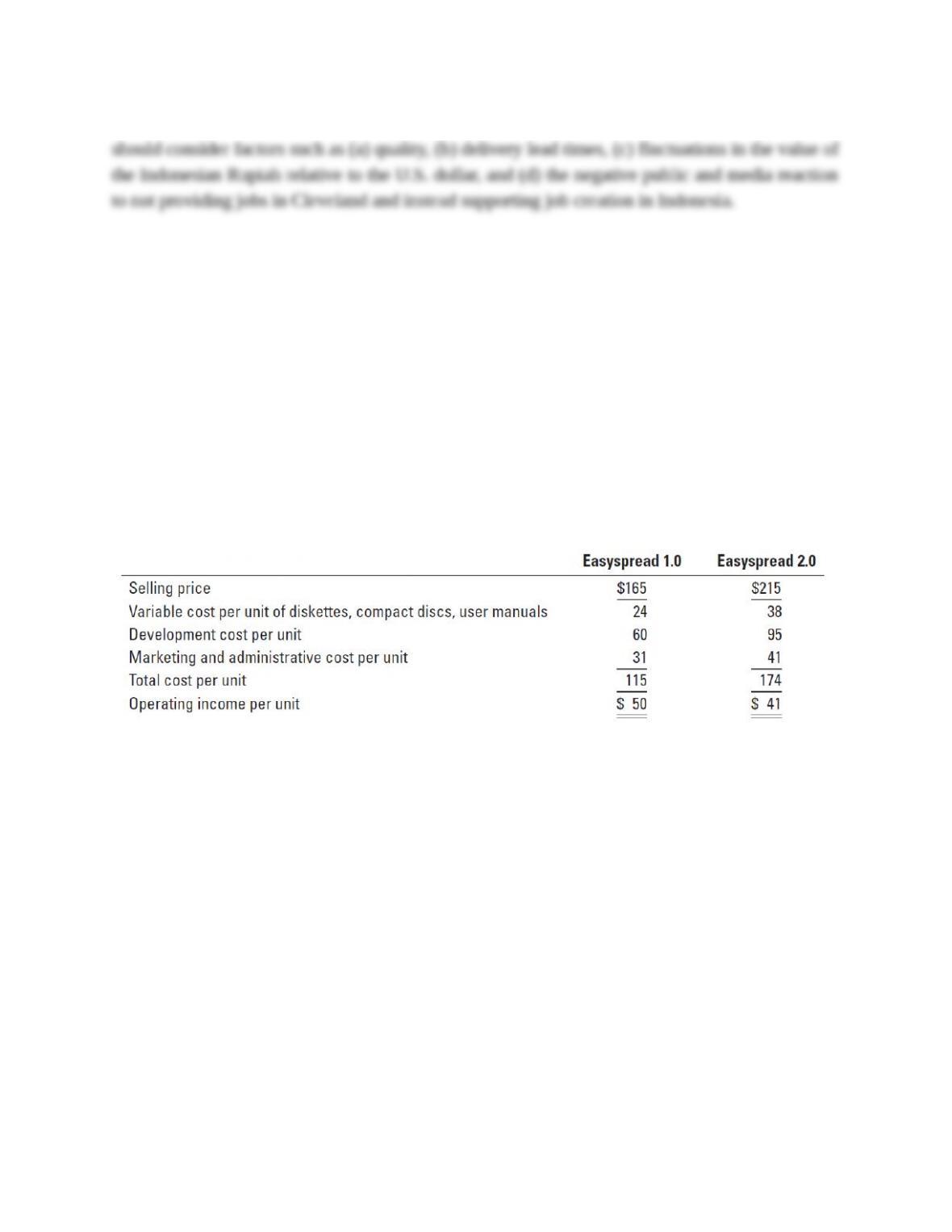

3. In deciding whether to purchase figurines from the Indonesian supplier, Cuddly Critters

should consider factors such as (a) quality, (b) delivery lead times, (c) fluctuations in the value of

the Indonesian Rupiah relative to the U.S. dollar, and (d) the negative public and media reaction

to not providing jobs in Cleveland and instead supporting job creation in Indonesia.

11-32 (30 min.) Relevant costs, opportunity costs.

Gavin Martin, the general manager of Oregano Software, must decide when to release the new

version of Oregano’s spreadsheet package, Easyspread 2.0. Development of Easyspread 2.0 is

complete; however, the diskettes, compact discs, and user manuals have not yet been produced.

The product can be shipped starting July 1, 2014.

The major problem is that Oregano has overstocked the previous version of its spreadsheet

package, Easyspread 1.0. Martin knows that once Easyspread 2.0 is introduced, Oregano will not

be able to sell any more units of Easyspread 1.0. Rather than just throwing away the inventory of

Easyspread 1.0, Martin is wondering if it might be better to continue to sell Easyspread 1.0 for the

next three months and introduce Easyspread 2.0 on October 1, 2014, when the inventory of

Easyspread 1.0 will be sold out.

The following information is available:

11-10

Development cost per unit for each product equals the total costs of developing the software

product divided by the anticipated unit sales over the life of the product. Marketing and

administrative costs are fixed costs in 2014, incurred to support all marketing and administrative

activities of Oregano Software. Marketing and administrative costs are allocated to products on

the basis of the budgeted revenues of each product. The preceding unit costs assume Easyspread

2.0 will be introduced on October 1, 2014.

Required:

1. On the basis of financial considerations alone, should Martin introduce Easyspread 2.0 on July

1, 2014, or wait until October 1, 2014? Show your calculations, clearly identifying relevant

and irrelevant revenues and costs.

2. What other factors might Gavin Martin consider in making a decision?