21-1

Difference in after-tax cash flow from terminal disposal of machines:

$23,020 – $14,720 = $8,300 (in favor of new machine)

2. The Frooty Company should retain the old equipment because the net present value of the

incremental cash flows from the new machine is negative. The computations, using the results of

requirement 1, are presented below. In this format, the present value factors appear at the bottom.

All cash flows, year by year, are then converted into present values.

After-Tax Cash Flows

2013a

2014

2015

2016

2017

2018

Initial machine investment

$(190,000)

Current disposal price of old machine

68,000

Tax savings from loss on disposal of

old machine

11,305

Recurring after-tax cash-operating savings

Variable

$18,810

$18,810

$18,810

$18,810

$18,810

Fixed

660

660

660

660

660

Income tax cash savings from difference in

depreciation deductions

5,695

5,695

5,695

5,695

5,695

Additional after-tax cash flow from

terminal disposal of new machine

over old machine

_________

_______

_______

_______

_______

_ 8,300

Net after-tax cash flows

$(110,695)

$25,165

$25,165

$25,165

$25,165

$33,465

Present value discount factors (at 12%)

_ 1.000

0.893

0.797

0.712

0.636

0.567

Present value

$(110,695)

$22,472

$20,057

$17,917

$16,005

$18,975

Net present value

$ (15,269)

a More precisely, January 1, 2014

3. Let $X be the additional recurring after-tax cash operating savings required each year to

make NPV = $0.

The present value of an annuity of $1 per year for 5 years discounted at 12% = 3.605.

To make NPV = 0, Frooty needs to generate cash savings with NPV of $15,269.

That is $X × (3.605) = $15,269

X = $15,269 ÷ 3.605 = $4,235.51

Frooty must generate additional annual after-tax cash operating savings of $4,235.51.

21-35 (35 min.) Recognizing cash flows for capital investment projects.

Johnny Buster owns Entertainment World, a place that combines fast food, innovative beverages,

and arcade games. Worried about the shifting tastes of younger audiences, Johnny contemplates

bringing in new simulators and virtual reality games to maintain customer interest.

As part of this overhaul, Johnny is also looking at replacing his old Guitar Hero equipment with

a Rock Band Pro machine. The Guitar Hero setup was purchased for $25,200 and has accumulated

depreciation of $23,000, with a current trade-in value of $2,700. It currently costs Johnny $600

per month in utilities and another $5,000 a year in maintenance to run the Guitar Hero equipment.

Johnny feels that the equipment could be kept in service for another 11 years, after which it would

have no salvage value.

21-2

The Rock Band Pro machine is more energy-efficient and durable. It would reduce the utilities

costs by 30% and cut the maintenance cost in half. The Rock Band Pro costs $49,000 and has an

expected disposal value of $5,000 at the end of its useful life of 11 years.

Johnny charges an entrance fee of $5 per hour for customers to play an unlimited number of

games. He does not believe that replacing Guitar Hero with Rock Band Pro will have an impact

on this charge or materially change the number of customers who will visit Entertainment World.

Required:

1. Johnny wants to evaluate the Rock Band Pro project using capital budgeting techniques. To

help him, read through the problem and separate the cash flows into four groups: (1) net initial

investment cash flows, (2) cash flow savings from operations, (3) cash flows from terminal

disposal of investment, and (4) cash flows not relevant to the capital budgeting problem.

2. Assuming a tax rate of 40%, a required rate of return of 8%, and straight-line depreciation over

the remaining useful life of equipment, should Johnny purchase Rock Band Pro?

SOLUTION

1. Partitioning relevant cash flows into categories:

(1) Net initial investment cash flows

— The $49,000 cost of the new Rock Band Pro

—The disposal value of Guitar Hero, $2,700, is a cash inflow.

—The book value of Guitar Hero $2,200 ($25,200 − $23,000), relative to the

disposal value of $2,700, yields a taxable gain of $500 ($2,700 − $2,200) that

leads to a cash outflow for taxes of $500 Tax Rate.

(2) Cash flow savings from operations

–—The 30% savings in utilities cost per year of $2,160 (30% × $600 per month ×

12 months) results in cash inflow from operations after tax of $2,160 (1 − Tax

Rate).

–—The savings of half the maintenance costs per year of $2,500 (50% × $5,000)

results in a cash inflow from operations after tax of $2,500 (1 − Tax Rate).

—Annual depreciation of ($49,000 − $5,000) ÷ 11 years = $4,000 on Rock Band

Pro, relative to the ($2,200 − $0) ÷ 11 years = $200 depreciation on current Guitar

Hero leads to additional tax savings of $3,800 × Tax Rate.

(3) Cash flows from terminal disposal of investment

—The $5,000 salvage value of Rock Band Pro minus the $0 salvage value of the

old Guitar Hero equipment is a terminal cash flow at the end of Year 11. There

are no tax effects because both systems are planned to be disposed of at book

value.

21-3

(4) Data not relevant to the capital budgeting decision

—The $5 per hour charge for customers, since it would not change whether or not

Johnny got the new machine

—The $25,200 original cost of the Guitar Hero setup

21-4

2. Net present value of the investment:

Net initial investment

Initial investment in Rock Band Pro

$(49,000)

Current disposal value of Guitar Hero

2,700

Tax on gain on sale of Guitar Hero, 40% × $500

(200)

Net initial investment

$(46,500)

Annual after-tax cash flow from operations (excl. deprn. effects)

After-tax savings in utilities costs, $2,160 × (1−0.40)

$ 1,296

After-tax savings in maintenance costs, $2,500 × (1−0.40)

1,500

Annual after-tax cash flow from operations

$ 2,796

Income-tax cash savings from annual additional depreciation

deductions ($4,000 − $200) × 40%

$ 1,520

After-tax cash flow from terminal disposal of machines

$ 5,000

These four amounts can be combined to determine the NPV at an 8% discount rate.

Present value of net initial investment, $(46,500) × 1.000

$(46,500)

Present value of 11-year annuity of annual after-tax cash flow

from operations (excl. deprcn. effects), $2,796 × 7.139

19,961

Present value of 11-year annuity of income-tax cash savings from

annual depreciation deductions, $1,520 × 7.139

10,851

Present value of after-tax cash flow from terminal disposal of

machines, $5,000 × 0.429

2,145

Net present value

$(13,543)

At the required rate of return of 8%, the net present value of the investment in the Rock Band Pro

machine is substantially negative. Johnny should therefore not make the investment.

21-36 (25 min.) NPV, inflation and taxes.

Cheap-O Foods is considering replacing all 10 of its old cash registers with new ones. The old

registers are fully depreciated and have no disposal value. The new registers cost $899,640 (in

total). Because the new registers are more efficient than the old registers, Cheap-O will have annual

incremental cash savings from using the new registers in the amount of $192,000 per year. The

registers have a 7-year useful life and no terminal disposal value and are depreciated using the

straight-line method. Cheap-O requires an 8% real rate of return.

Required:

1. Given the preceding information, what is the net present value of the project? Ignore taxes.

2. Assume the $192,000 cost savings are in current real dollars and the inflation rate is 5.5%.

Recalculate the NPV of the project.

3. Based on your answers to requirements 1 and 2, should Cheap-O buy the new cash registers?

4. Now assume that the company’s tax rate is 30%. Calculate the NPV of the project assuming

no inflation.

5. Again assuming that the company faces a 30% tax rate, calculate the NPV of the project under

an inflation rate of 5.5%.

6. Based on your answers to requirements 4 and 5, should Cheap-O buy the new cash registers?

SOLUTION

1. Without inflation or taxes, this is a simple net present value problem using an 8%

discount rate

Present value of initial investment, $(899,640) × 1.000

$(899,640)

Present value of 7-year annuity of annual cash savings:

$192,000 × 5.206

999,552

Net present value

$ 99,912

2. With inflation, we adjust each year’s cash flow for the inflation rate to get nominal cash

flows and then discount each cash flow separately using the nominal discount rate.

Nominal rate = (1 + real rate) × (1 + inflation rate) − 1

Nominal rate = (1.08) × (1.055) − 1 = 1.1394 – 1 = 0.1394 or 14% (approx.)

Cash Flow

Cumulative

Cash Inflows

Present Value

Period

(Real Dollars)

Inflation Rate

(Nominal Dollars)

Factor, 14%

Present Value

(1)

(2)

(3) = (1) × (2)

(4)

(5) = (3) × (4)

1

$192,000

1.055

$202,560

0.877

$177,645

2

192,000

1.1131

213,696

0.769

164,332

3

192,000

1.174

225,408

0.675

152,150

4

192,000

1.239

237,888

0.592

140,830

5

192,000

1.307

250,944

0.519

130,240

6

192,000

1.379

264,768

0.456

120,734

7

192,000

1.455

279,360

0.400

111,744

Total present value of annual net cash inflows in nominal dollars

997,675

Present value of initial investment, $(899,640) × 1.000

(899,640)

Net present value

$ 98,035

11.113 = (1.055)2

3. Both the unadjusted and adjusted NPV are positive. Based on financial considerations

alone, Cheap-O Foods should buy the new cash registers. However, the effect of taxes should

also be considered, as well as any pertinent nonfinancial issues, such as potential improvements

in customer response time from moving to the new cash registers.

4.

Initial equipment investment

$(899,640)

Annual cash flow from operations (excl. deprn. effects)

$192,000

Deduct income tax payments (0.30 × $192,000)

57,600

Annual after-tax cash flow from operations (excl. deprn. effects)

$ 134,400

Income tax cash savings from annual depreciation deductions

(0.30 × $128,520)1

$ 38,556

1 Depreciation deductions = ($899,640 – $0) / 7 = $128,520

The terminal disposal price of the equipment is equal to the book value at disposal = $0, so the

above three amounts suffice to determine the NPV at a 8% discount rate.

Present value of net initial investment, $(899,640) × 1.000

$(899,640)

Present value of 7-year annuity annual after-tax cash flow from operations,

$134,400 × 5.206

699,686

Present value of 7-year annuity of income tax cash savings from

annual depreciation deductions, $38,556 × 5.206

200,723

Net present value

$ 769

5. As in the previous section, with inflation, we adjust each year’s cash flow for the

inflation rate to get nominal cash flows and then discount each cash flow separately using the

nominal discount rate.

Nominal rate = (1 + real rate) × (1 + inflation rate) −1

Nominal rate = (1.08)(1.055) −1 = 1.1394 – 1 = .1394 or 14% (approx.)

Cash Flow

Cumulative

Cash Inflows

After Tax

Cash

Present Value

Period

(Real Dollars)

Inflation Rate

(Nominal Dollars)

Flows

Factor, 14%

Present Value

(1)

(2)

(3) = (1) × (2)

(4) = 0.7 × (3)

(5)

(6) = (4) × (5)

21-7

1

$192,000

1.055

$202,560

$141,792

0.877

$124,352

2

192,000

1.113

213,696

149,587

0.769

115,033

3

192,000

1.174

225,408

157,786

0.675

106,505

4

192,000

1.239

237,888

166,522

0.592

98,581

5

192,000

1.307

250,944

175,661

0.519

91,168

6

192,000

1.379

264,768

185,338

0.456

84,514

7

192,000

1.455

279,360

195,552

0.400

78,221

Total present value of annual net cash inflows (excl. depreciation. effects)

$698,374

Present value of 7-year annuity of income-tax cash savings from

annual depreciation deductions, $38,556 × 5.206

200,723

Present value of initial investment $(899,640) × 1.000

(899,640)

Net present value

$ (543)

6. Without inflation, we obtain a positive NPV; however, with inflation NPV is negative,

and Cheap-O Foods would be better off not purchasing the new registers. Negative NPV is

obtained with an inflation estimate of 5.5%. If a careful review of this forecasted inflation rate

results in a lower rate of inflation, Cheap-O Foods should recalculate the NPV to determine

whether the purchase of the registers is in its best interest.

21-37 (60 min.) NPV of information system, income taxes.

Saina Supplies leases and sells materials, tools, and equipment and also provides add-on services

such as ground maintenance and waterproofing to construction and mining sites. The company has

grown rapidly over the past few years. The owner, Saina Torrance, feels that for the company to

continue to scale, it needs to install a professional information system rather than relying on

intuition and Excel analyses. After some research, Saina’s CFO reports back with the following

data about a data warehousing and analytics system that she views as promising:

▪ The system will cost $750,000. For tax purposes, it can be depreciated straight-line to a zero

terminal value over a 5-year useful life. However, the CFO expects that the system will still

be worth $50,000 at that time.

▪ There is an additional $75,000 annual fee for software upgrades and technical support from

the vendor.

▪ The ability to provide better services and to target and reach more clients as a result of the

new system will directly result in a $500,000 increase in revenues for Saina in the first year

after installation. Revenues will grow by 5% each year thereafter. Saina’s contribution

margin is 60%.

▪ Due to greater efficiency in ordering and dispatching supplies, as well as in collecting

receivables, the firm’s working-capital requirements will decrease by $100,000.

▪ Saina will also be able to reduce the amount of warehouse space it currently leases, saving

$40,000 annually in the process.

▪ Saina Supplies pays an income tax of 30% and requires an after-tax rate of return of 12%.

Assume that all cash flows occur at year-end except for initial investment amounts.

21-8

Required:

1. If Saina decides to purchase and install the new information system, what is the expected

incremental after-tax cash flow from operations during each of the 5 years?

2. Compute the net present value of installing the information system at Saina Supplies.

3. In addition to the analysis in requirement 2, what nonfinancial factors you would consider in

making the decision about the information system?

SOLUTION

1. Initial investment (Year 0): $750000

Working-capital investment:

Reduced working capital of $100000 at end of Year 0.

Increased working capital of $100000 at end of Year 5.

Depreciation on initial investment: $750000 5 years = $150000 per year

Income tax cash savings from annual depreciation deductions: $150000 × 0.30 = $45000

After-tax cash flow from disposal of JIT system at end of Year 5: $50000 × (1– 0.30) = $35000

Annual after-tax cash flow from operations:

Year 1

Year 2

Year 3

Year 4

Year 5

Incremental revenues

(5% annual growth)

$500,000

$525,000

$551,250

$578,813

$607,753

Incremental contribution margin

(60%

incremental revenues)

$300,000

$315,000

$330,750

$347,288

$364,652

Rent savings

40,000

40,000

40,000

40,000

40,000

Deduct increase in software

upgrades and tech support costs

(75,000)

(75,000)

(75,000)

(75,000)

(75,000)

Annual pre-tax incremental

cash inflow from operations

265,000

280,000

295,750

312,288

329,652

Deduct income tax payments

(30%)

79,500

84,000

88,725

93,686

98,896

Annual after-tax incremental

cash inflow from operations

$185,500

$196,000

$207,025

$218,602

$230,756

2. Solution Exhibit 21-37 reports the net present value to be $214,506.

3. Saina will have a NPV of $214,506 with the new data warehousing and analytics system.

Based on financial quantitative factors, this is an attractive investment. Qualitative factors could

make the system even more attractive. For example, if a competitor adopts the new information

system but Saina does not, Saina could be at a sizable competitive disadvantage. Not adopting the

information system does not mean the status quo will remain. Saina’s workers can also gain

21-9

additional expertise when using the data warehousing and analytics system that can be beneficially

employed on other projects.

21-10

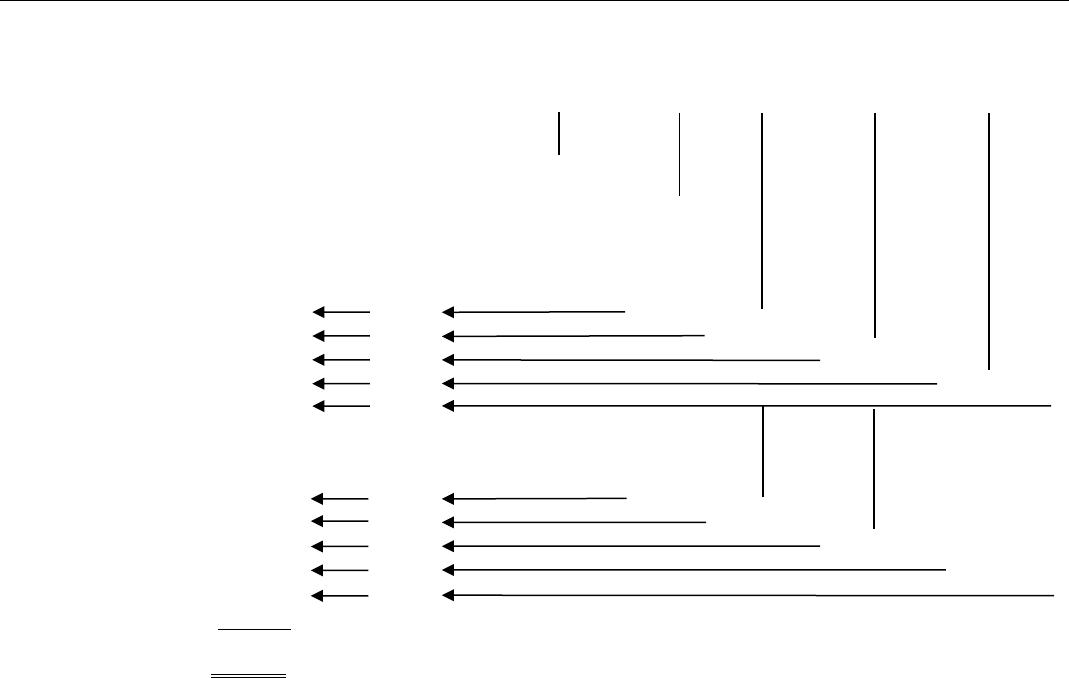

SOLUTION EXHIBIT 21-37

Total

Present

Value

Present

Value

Discount

Factors

at 12%

Sketch of Relevant After-Tax Cash Flows

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

1a. Net initial

investment

$(750000)

1.000

$(750000)

1b. Working

capital decrease

100,000

1.000

$100000

2a. Annual after-

tax cash flow

from operations

Year 1

165,652

0.893

$185,500

Year 2

156,212

0.797

$196000

Year 3

147,402

0.712

$207,025

Year 4

139,031

0.636

$218,602

Year 5

130,839

0.567

$230,756

2b. Income tax cash

savings from annual

depreciation charges

Year 1

40,185

0.893

$45000

Year 2

35,865

0.797

$45000

Year 3

32,040

0.712

$45000

Year 4

28,620

0.636

$45000

Year 5

25,515

0.567

$45000

3. After-tax cash flow from:

a. Terminal

disposal of

machine

19,845

0.567

$35000

b. Increase in

working capital

(56,700)

0.567

$(100000)

Net

present value

$214,506