6-1

6-38 (30 min.) Cash budgeting, chapter appendix.

Retail outlets purchase snowboards from Skulas, Inc., throughout the year. However, in

anticipation of late summer and early fall purchases, outlets ramp up inventories from May through

August. Outlets are billed when boards are ordered. Invoices are payable within 60 days. From

past experience, Skulas’ accountant projects 40% of invoices will be paid in the month invoiced,

45% will be paid in the following month, and 15% of invoices will be paid two months after the

month of invoice. The average selling price per snowboard is $650.

To meet demand, Skulas increases production from April through July because the snowboards

are produced a month prior to their projected sale. Direct materials are purchased in the month of

production and are paid for during the following month (terms are payment in full within 30 days

of the invoice date). During this period there is no production for inventory and no materials are

purchased for inventory.

Direct manufacturing labor and manufacturing overhead are paid monthly. Variable

manufacturing overhead is incurred at the rate of $7 per direct manufacturing labor-hour. Variable

marketing costs are driven by the number of sales visits. However, there are no sales visits during

the months studied. Skulas, Inc., also incurs fixed manufacturing overhead costs of $7,500 per

month and fixed nonmanufacturing overhead costs of $4,500 per month.

The beginning cash balance for July 1, 2015, is $14,000. On October 1, 2014, Skulas had a cash

crunch and borrowed $60,000 on a 12% one-year note with interest payable monthly. The note is

due October 1, 2015.

Required:

1. Prepare a cash budget for the months of July through September 2015. Show supporting

schedules for the calculation of receivables and payables.

2. Will Skulas be in a position to pay off the $60,000 one-year note that is due on October 1,

2015? If not, what actions would you recommend to Skulas’ management?

3. Suppose Skulas is interested in maintaining a minimum cash balance of $14,000. Will the

company be able to maintain such a balance during all three months analyzed? If not, suggest

a suitable cash management strategy.

4. Why do Skulas’ managers prepare a cash budget in addition to the revenue, expenses, and

operating income budget?

SOLUTION

Note: This problem is independent of the previous Problem 6-37. All the information needed

to solve Problem 6-38 is given in Problem 6-38. There is no connection between Problem 6–

37 and Problem 6-38.

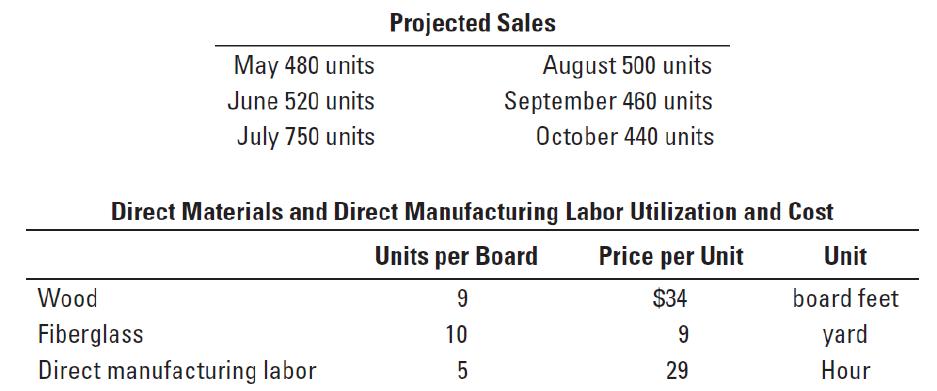

1. Projected Sales

May

June

July

August

September

October

Sales in units

480

520

750

500

460

440

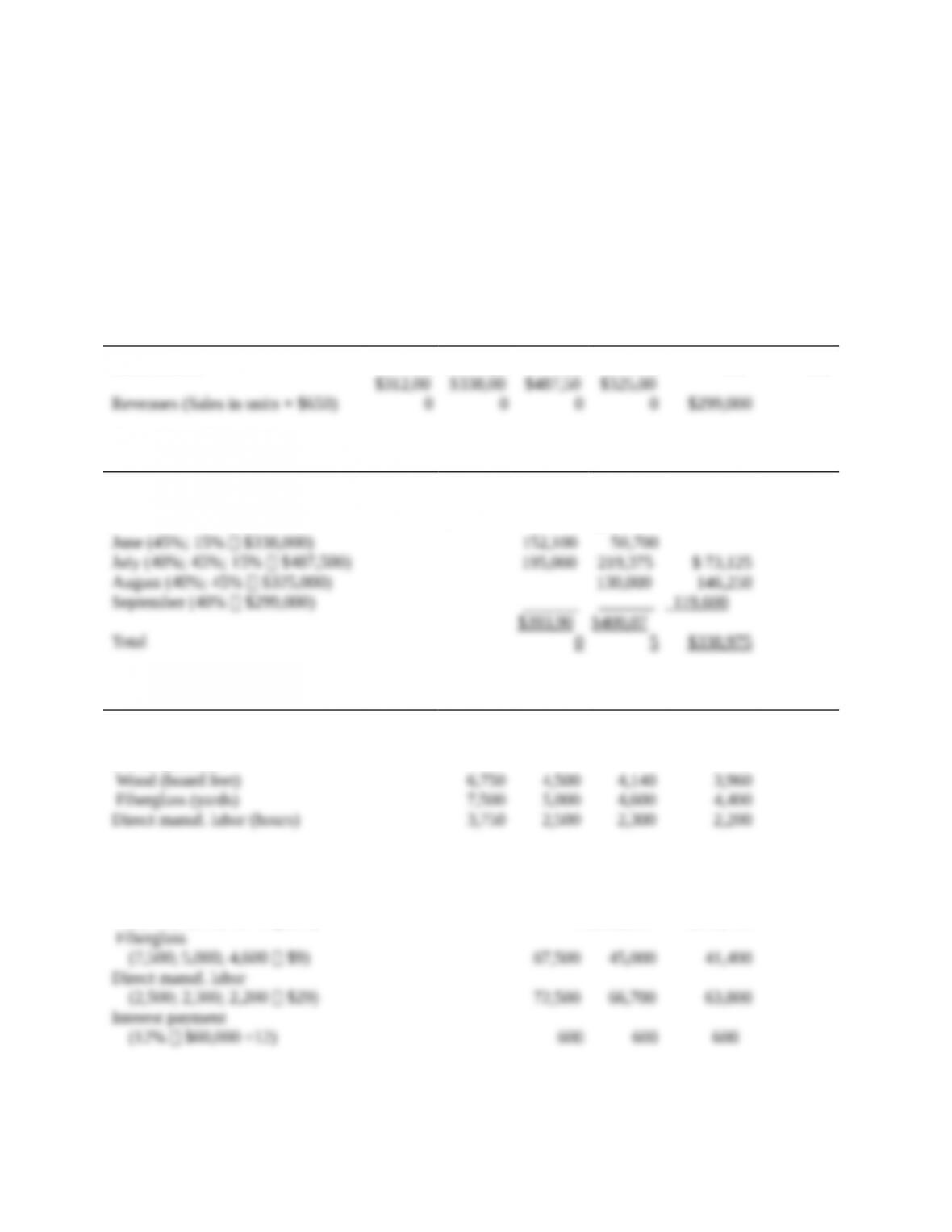

Revenues (Sales in units × $650)

$312,00

0

$338,00

0

$487,50

0

$325,00

0

$299,000

Collections of Receivables

May

June

July

August

September

October

From sales in:

May (15% $312,000)

$ 46,800

June (45%; 15% $338,000)

152,100

$

50,700

July (40%; 45%; 15% $487,500)

195,000

219,375

$ 73,125

August (40%; 45% $325,000)

130,000

146,250

September (40% $299,000)

119,600

Total

$393,90

0

$400,07

5

$338,975

Calculation of Payables

May

June

July

August

September

October

Material and Labor Use, Units

Budgeted production

750

500

460

440

Direct materials

Wood (board feet)

6,750

4,500

4,140

3,960

Fiberglass (yards)

7,500

5,000

4,600

4,400

Direct manuf. labor (hours)

3,750

2,500

2,300

2,200

Disbursement of Payments

Direct materials

Wood

(6,750; 4,500; 4,140 $34)

$229,50

0

$153,000

$140,760

Fiberglass

(7,500; 5,000; 4,600 $9)

67,500

45,000

41,400

Direct manuf. labor

(2,500; 2,300; 2,200 $29)

72,500

66,700

63,800

Interest payment

(12% $60,000 ÷12)

600

600

600

Variable Overhead Calculation

Variable overhead rate

$ 7

$ 7

$ 7

6-3

Overhead driver

(direct manuf. labor-hours)

2,500

2,300

2,200

Variable overhead expense

$

17,500

$

16,100

$ 15,400

Cash Budget for the months of July, August, September 2015

July

August

September

Beginning cash balance

$ 14,000

$ 8,300

$114,975

Add receipts: Collection of receivables

393,900

400,075

338,975

Total cash available

$407,900

$408,375

$453,950

Deduct disbursements:

Material purchases

$297,000

$198,000

$182,160

Direct manufacturing labor

72,500

66,700

63,800

Variable costs

17,500

16,100

15,400

Fixed manuf. and nonmanuf. costs

12,000

12,000

12,000

Interest payments

600

600

600

Total disbursements

399,600

293,400

273,960

Ending cash balance

$ 8,300

$114,975

$179,990

2. Yes. Skulas has a budgeted cash balance of $179,990 on 9/30/2015, and so it will be in a

position to pay off the $60,000 1-year note on October 1, 2015.

3. No. Skulas does not maintain a $14,000 minimum cash balance in July. To maintain a

$14,000 cash balance in each of the three months, it could perhaps encourage its customers to pay

earlier by offering a discount. Alternatively, Skulas could seek short-term credit from a bank.

4. Skulas’ managers prepare a cash budget in addition to the operating income budget to plan

cash flows to ensure that the company has adequate cash to pay vendors, meet payroll, and pay

operating expenses as these payments come due. Skulas could be very profitable on an accrual

accounting basis, but the pattern of cash receipts from revenues might be delayed and result in

insufficient cash being available to make scheduled payments for its expenses. Skulas’ managers

may then need to initiate a plan to borrow money to finance any shortfall. Building a profitable

operating plan does not guarantee that adequate cash will be available, so Skulas’ managers need

to prepare a cash budget in addition to an operating income budget.

6-39 (40–50 min.) Cash budgeting.

On December 1, 2014, the Iaia Wholesale Co. is attempting to project cash receipts and

disbursements through January 31, 2015. On this latter date, a note will be payable in the amount

of $107,000. This amount was borrowed in September to carry the company through the seasonal

peak in November and December.

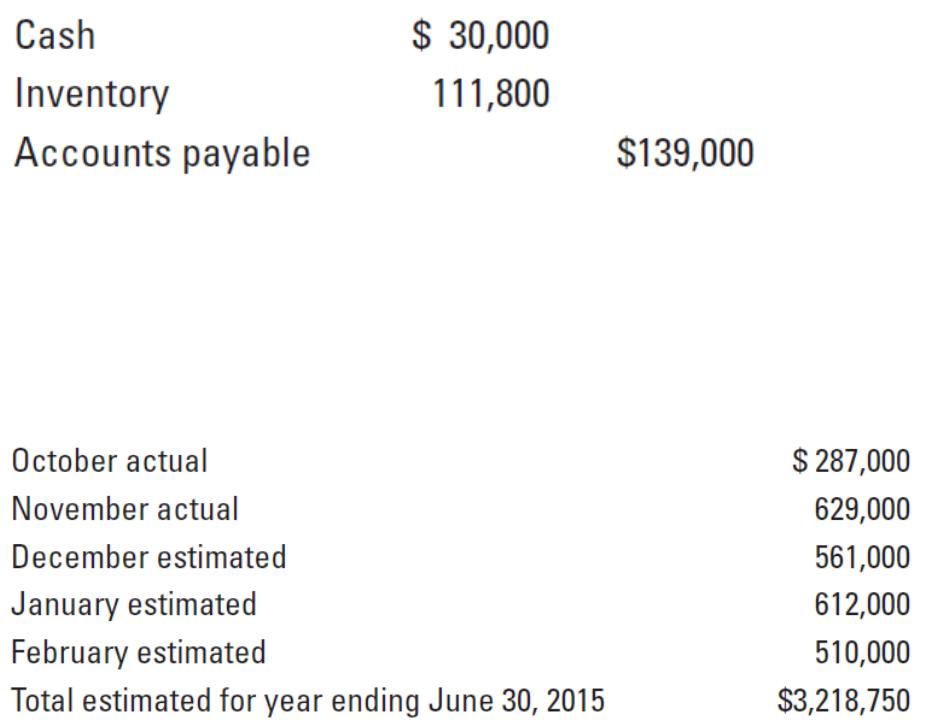

Selected general ledger balances on December 1 are:

6-4

Sales terms call for a 3% discount if payment is made within the first 10 days of the month after

sale, with the balance due by the end of the month after sale. Experience has shown that 50% of

the billings will be collected within the discount period, 30% by the end of the month after

purchase, and 15% in the following month. The remaining 5% will be uncollectible. There are no

cash sales.

The average selling price of the company’s products is $170 per unit. Actual and projected

sales are:

All purchases are payable within 15 days. Approximately 60% of the purchases in a month are

paid that month and the rest the following month. The average unit purchase cost is $130. Target

ending inventories are 570 units plus 20% of the next month’s unit sales.

Total budgeted marketing, distribution, and customer-service costs for the year are $670,000.

Of this amount, $155,000 are considered fixed (and include depreciation of $43,400). The

remainder varies with sales. Both fixed and variable marketing, distribution, and customer-service

costs are paid as incurred.

Required:

1. Prepare a cash budget for December 2014 and January 2015. Supply supporting schedules for

collections of receivables; payments for merchandise; and marketing, distribution, and

customer-service costs.

2. Why do Iaia’s managers prepare a cash budget in addition to the operating income budget?

SOLUTION

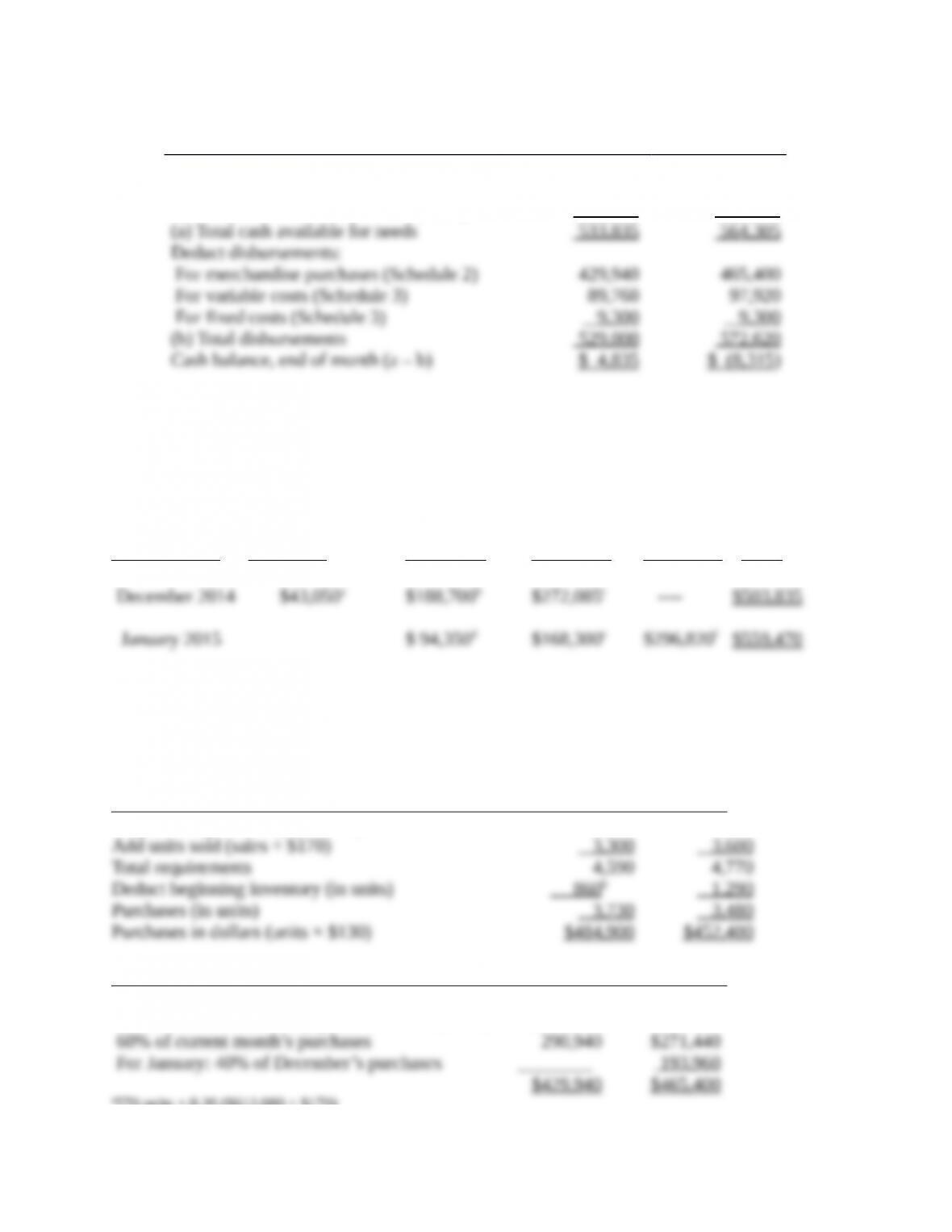

Iaia Wholesale Co.

Statement of Budgeted Cash Receipts and Disbursements

For the Months of December 2014 and January 2015

6-5

December 2014

January 2015

Cash balance, beginning

$ 30,000

$ 4,835

Add receipts:

Collections of receivables (Schedule 1)

503,835

559,470

(a) Total cash available for needs

533,835

564,305

Deduct disbursements:

For merchandise purchases (Schedule 2)

429,940

465,400

For variable costs (Schedule 3)

89,760

97,920

For fixed costs (Schedule 3)

9,300

9,300

(b) Total disbursements

529,000

572,620

Cash balance, end of month (a – b)

$ 4,835

$ (8,315)

Under the current projections, the cash balance as of January 31, 2015, is $(8,315), which is not

sufficient to enable repayment of the $107,000 note.

Schedule 1: Collections of Receivables

Collections in Oct. Sales Nov. Sales Dec. Sales Jan. Sales Total

December 2014 $43,050a $188,700b $272,085c —- $503,835

January 2015 $ 94,350d $168,300e $296,820f $559,470

a0.15 × $287,000 b0.30 × $629,000 c0.50 × $561,000 × 0.97

d0.15 × $629,000 e0.30 × $561,000 f0.50 × $612,000 × 0.97

Schedule 2: Payments for Merchandise

December January

Target ending inventory (in units) 1,290a 1,170c

Add units sold (sales ÷ $170) 3,300 3,600

Total requirements 4,590 4,770

Deduct beginning inventory (in units) 860b 1,290

Purchases (in units) 3,730 3,480

Purchases in dollars (units × $130) $484,900 $452,400

December January

Cash disbursements:

For December: accounts payable on Dec. 1, 2014; $139,000

60% of current month’s purchases 290,940 $271,440

For January: 40% of December’s purchases ________ 193,960

$429,940 $465,400

6-6

a570 units + 0.20 ($612,000 ÷ $170)

b$111,800 ÷ $130

c570 units + 0.20($510,000 ÷ $170)

Schedule 3: Marketing, Distribution, and Customer-Service Costs

Total annual fixed costs, $155,000, minus $43,400 depreciation $111,600

Monthly fixed cost requiring cash outlay $ 9,300

Variable cost ratio to sales =

$670,000 $155,000

$3,218,750

−

= 0.16

December variable costs: 0.16 × $561,000 sales $89,760

January variable costs: 0.16 × $612,000 sales $97,920

2. Iaia’s managers prepare a cash budget in addition to the operating income budget to plan

cash flows to ensure that the company has adequate cash to pay vendors, meet payroll, and pay

operating expenses as these payments come due. Iaia could be very profitable on an accrual

accounting basis, but the pattern of cash receipts from revenues might be delayed and result in

insufficient cash being available to make scheduled payments for its expenses. Iaia’s managers

may then need to initiate a plan to borrow money to finance any shortfall. Building a profitable

operating plan does not guarantee that adequate cash will be available, so Iaia’s managers need to

prepare a cash budget in addition to an operating income budget. For example, the cash budget

helps Iaia’s managers recognize that Iaia will not be able to repay the note in the amount of

$107,000 when it comes due on January 15, 2015. The cash budget prompts Iaia’s managers to

start making other arrangements for this loan, either by extending its terms or borrowing cash from

elsewhere to pay it back.

6-7

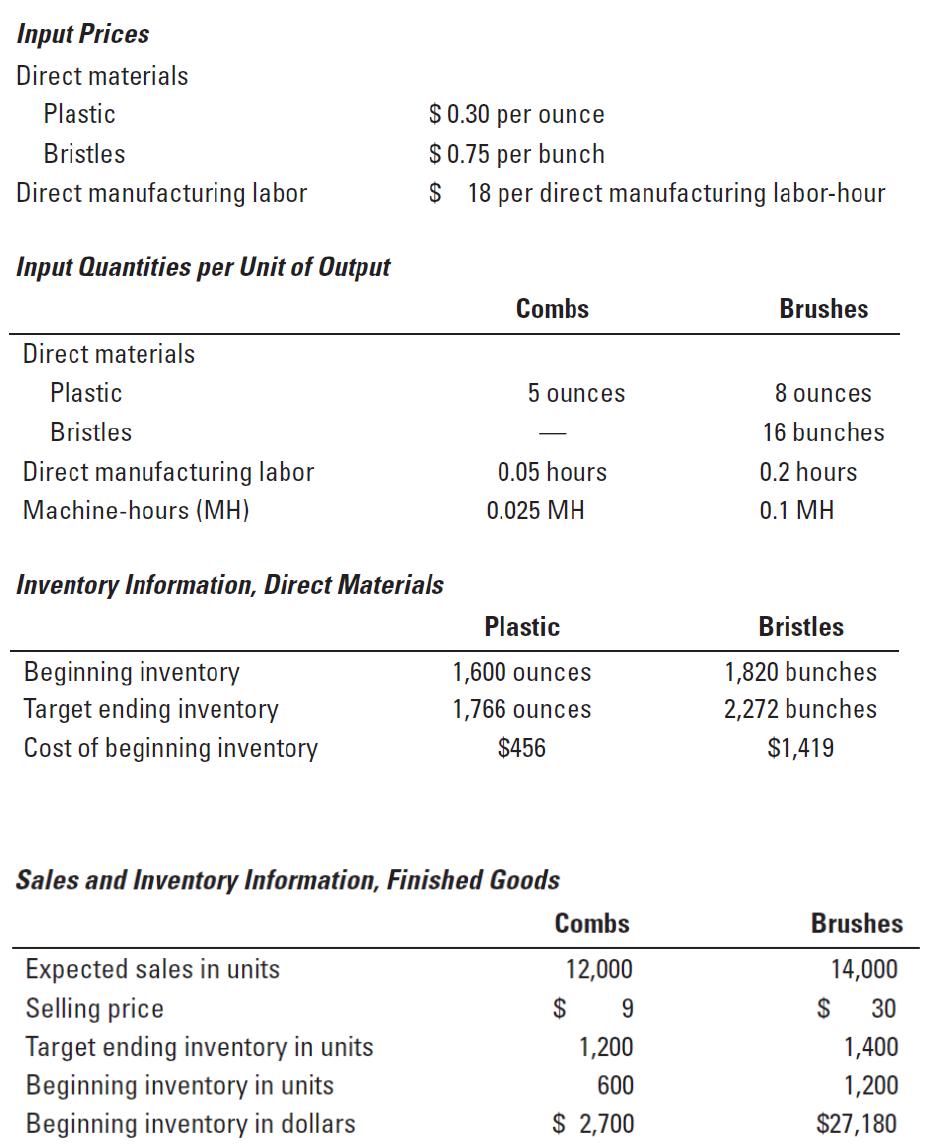

6-40 (60 min.) Comprehensive problem; ABC manufacturing, two products.

Hazlett, Inc., operates at capacity and makes plastic combs and hairbrushes. Although the combs

and brushes are a matching set, they are sold individually and so the sales mix is not 1:1. Hazlett’s

management is planning its annual budget for fiscal year 2015. Here is information for 2015:

Hazlett accounts for direct materials using a FIFO cost flow.

6-8

Hazlett uses a FIFO cost flow assumption for finished goods inventory.

Combs are manufactured in batches of 200, and brushes are manufactured in batches of 100. It

takes 20 minutes to set up for a batch of combs and 1 hour to set up for a batch of brushes.

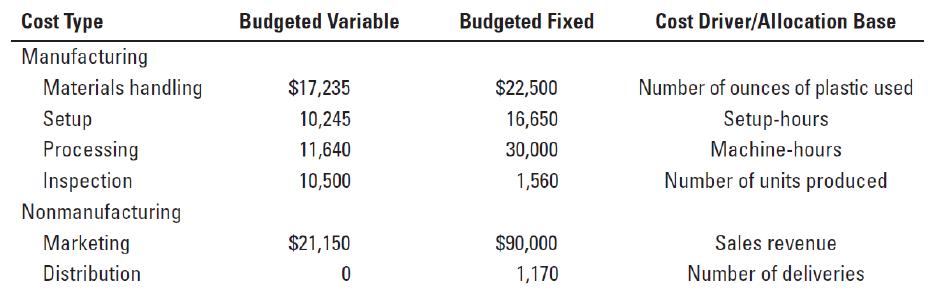

Hazlett uses activity-based costing and has classified all overhead costs as shown in the

following table. Budgeted fixed overhead costs vary with capacity. Hazlett operates at capacity so

budgeted fixed overhead cost per unit equals the budgeted fixed overhead costs divided by the

budgeted quantities of the cost allocation base.

Delivery trucks transport units sold in delivery sizes of 1,000 combs or 1,000 brushes.

Required:

Do the following for the year 2015:

1. Prepare the revenues budget.

2. Use the revenues budget to:

a. Find the budgeted allocation rate for marketing costs.

b. Find the budgeted number of deliveries and allocation rate for distribution costs.

3. Prepare the production budget in units.

4. Use the production budget to:

a. Find the budgeted number of setups and setup-hours and the allocation rate for setup costs.

b. Find the budgeted total machine-hours and the allocation rate for processing costs.

c. Find the budgeted total units produced and the allocation rate for inspection costs.

5. Prepare the direct material usage budget and the direct material purchases budgets in both units

and dollars; round to whole dollars.

6. Use the direct material usage budget to find the budgeted allocation rate for materials-handling

costs.

7. Prepare the direct manufacturing labor cost budget.

8. Prepare the manufacturing overhead cost budget for materials handling, setup, processing, and

inspection costs.

9. Prepare the budgeted unit cost of ending finished goods inventory and ending inventories

budget.

10. Prepare the cost of goods sold budget.

11. Prepare the nonmanufacturing overhead costs budget for marketing and distribution.

12. Prepare a budgeted income statement (ignore income taxes).

13. How does preparing the budget help Hazlett’s management team better manage the company?

6-9

SOLUTION

1.

Revenues Budget

For the Year Ending December 31, 2015

Units

Selling

Price

Total Revenues

Combs

12,000

$ 9

$108,000

Brushes

14,000

$30

420,000

Total

$528,000

2a.

Total budgeted marketing costs = Budgeted variable marketing costs + Budgeted fixed marketing costs

= $21,150 + $90,000 = $111,150

Marketing allocation rate = $111,150 ÷ $528,000 = $0.2105 per sales dollar

2b.

Total budgeted distribution costs = Budgeted variable distribn. costs + Budgeted fixed distribn. costs

= $0 + $1,170 = $1,170

Combs:

12,000 units ÷ 1,000 units per delivery

12 deliveries

Brushes:

14,000 units ÷ 1,000 units per delivery

14 deliveries

Total

26 deliveries

Delivery allocation rate = $1,170 ÷ 26 deliveries = $45 per delivery

3.

Production Budget (in Units)

For the Year Ending December 31, 2015

Product

Combs

Brushes

Budgeted unit sales

12,000

14,000

Add target ending finished goods inventory

1,200

1,400

Total required units

13,200

15,400

Deduct beginning finished goods inventory

600

1,200

Units of finished goods to be produced

12,600

14,200

6-10

4a.

Combs

Brushes

Total

Machine setup overhead

Units to be produced

12,600

14,200

Units per batch

÷200

÷100

Number of setups

63

142

Hours to setup per batch

×1/3

×1

Total setup hours

21

142

163

Total budgeted setup costs = Budgeted variable setup costs + Budgeted fixed setup costs

= $10,245 + $16,650 = $26,895

Machine setup

allocation rate

= $26,895 ÷ 163 setup hours = $165 per setup hour

b.

Combs:

12,600 units × 0.025 MH per unit

315 MH

Brushes:

14,200 units × 0.1 MH per unit

1,420 MH

Total

1,735 MH

Total budgeted processing costs = Budgeted variable processing costs + Budgeted fixed processing costs

= $11,640 + $30,000 = $41,640

Processing allocation rate = $41,640 ÷ 1,735 MH = $24 per MH

c.

Total budgeted inspection costs = Budgeted variable inspection costs + Budgeted fixed inspection costs

= $10,500 + $1,560 = $12,060

Inspection allocation rate = $12,060 ÷ 26,800 units = $0.45 per unit

6-11