1) An assumption of the FIFO process-costing method is that ________.

A) the units in beginning inventory are not necessarily assumed to be completed by the

end of the period

B) the units in beginning inventory are assumed to be completed first

C) ending inventory will always be completed in the next accounting period

D) no calculation of conversion costs is possible

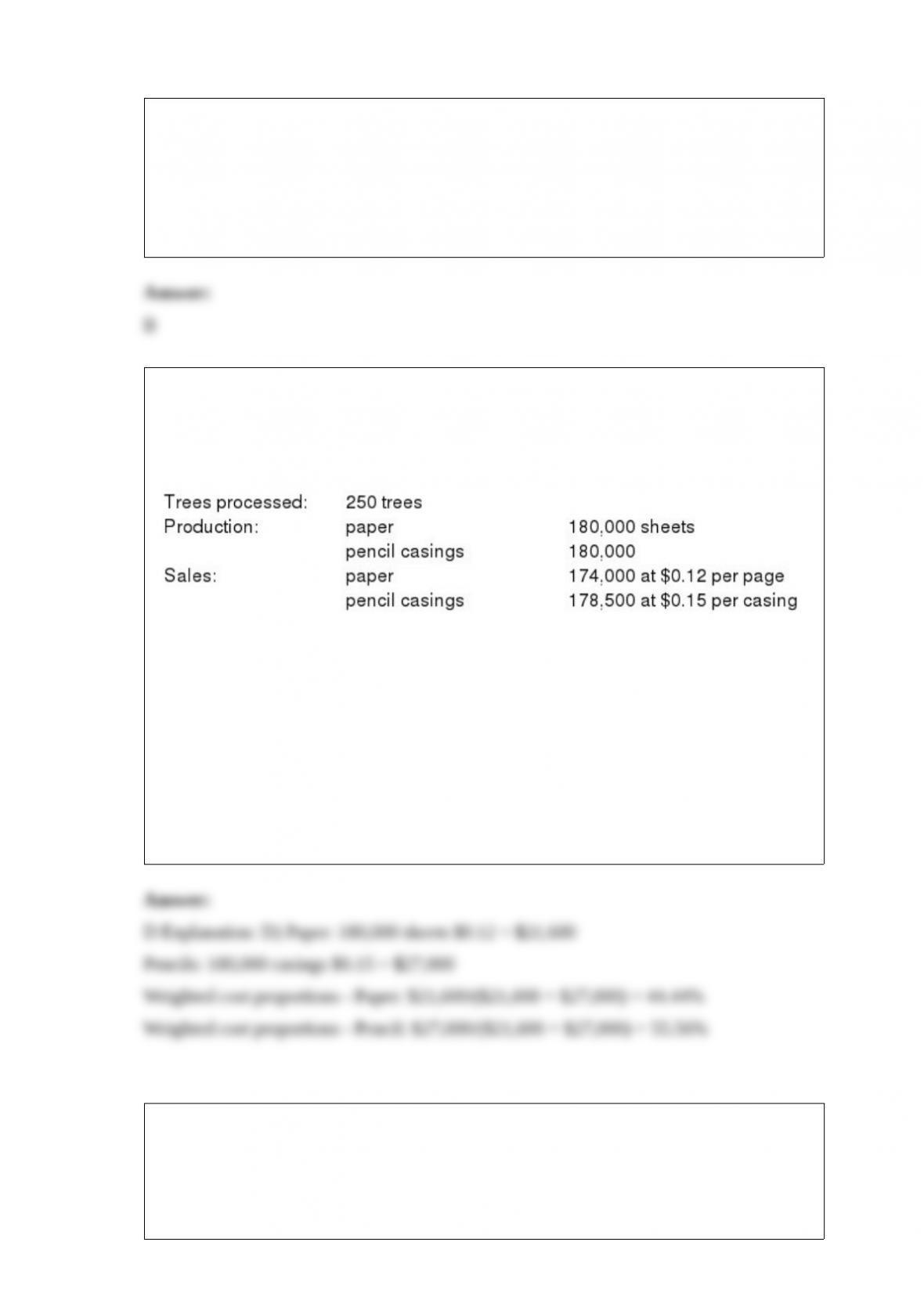

2) Bismite Corporation purchases trees from Cheney lumber and processes them up to

the splitoff point where two products (paper and pencil casings) are obtained. The

products are then sold to an independent company that markets and distributes them to

retail outlets. The following information was collected for the month of October:

The cost of purchasing 250 trees and processing them up to the splitoff point to yield

180,000 sheets of paper and 180,000 pencil casings is $12,500.

Bismite’s accounting department reported no beginning inventory.

What are the paper’s and the pencil’s approximate weighted cost proportions using the

sales value at

splitoff method, respectively?

A) 50.00% and 50.00%

B) 33.33% and 66.67%

C) 31.82% and 68.18%

D) 44.44% and 55.56%

3) The Swivel Chair Company manufacturers a standard recliner. During February, the

firm’s Assembly Department started production of 145,000 chairs. During the month,

the firm completed 175,000 chairs and transferred them to the Finishing Department.

The firm ended the month with 18,000 chairs in ending inventory. All direct materials

costs are added at the beginning of the production cycle. Weighted-average costing is

used by Swivel.

What were the equivalent units for conversion costs for February if the beginning

inventory was 70% complete as to conversion costs and the ending inventory was 40%

complete as to conversion costs?

A) 182,200

B) 152,200

C) 172,200

D) 162,200

4) A transfer-pricing method leads to goal congruence when ________.

A) there is a price difference in different markets due to market inefficiencies

B) managers do no act for their own best interest and work for the long-term best

interest of the manager’s subunit

C) managers act in their own best interest and the decision is in the long-term best

interest of the company

D) there is a low degree of centralization

5) When manufacturing cycle increases, ________.

A) sunk costs will decrease

B) opportunity costs will increase

C) opportunity costs will decrease

D) inventory carrying costs will increase

6) An operating income analysis of Argon Company revealed the following:

Operating income for 2014$1,207,000

Add growth component102,000

Deduct price-recovery component(95,000)

Add productivity component90,000

Operating income for 2015$1,304,000

Argon’s operating income gain is consistent with the ________.

A) product differentiation strategy

B) product leadership strategy

C) cost differentiation strategy

D) cost leadership strategy

7) Which of the following statements is true of benchmarking?

A) It is a systematic approach of optimizing business processes.

B) It fails to help to improve organizational performance as benchmarking data does not

provide insight into why costs or revenues differ across companies.

C) It is difficult to ensure that the benchmark numbers are comparable due to the

existence of differences across companies.

D) It considers four major business aspects such as financial, customer, internal

business processes, and learning and growth.

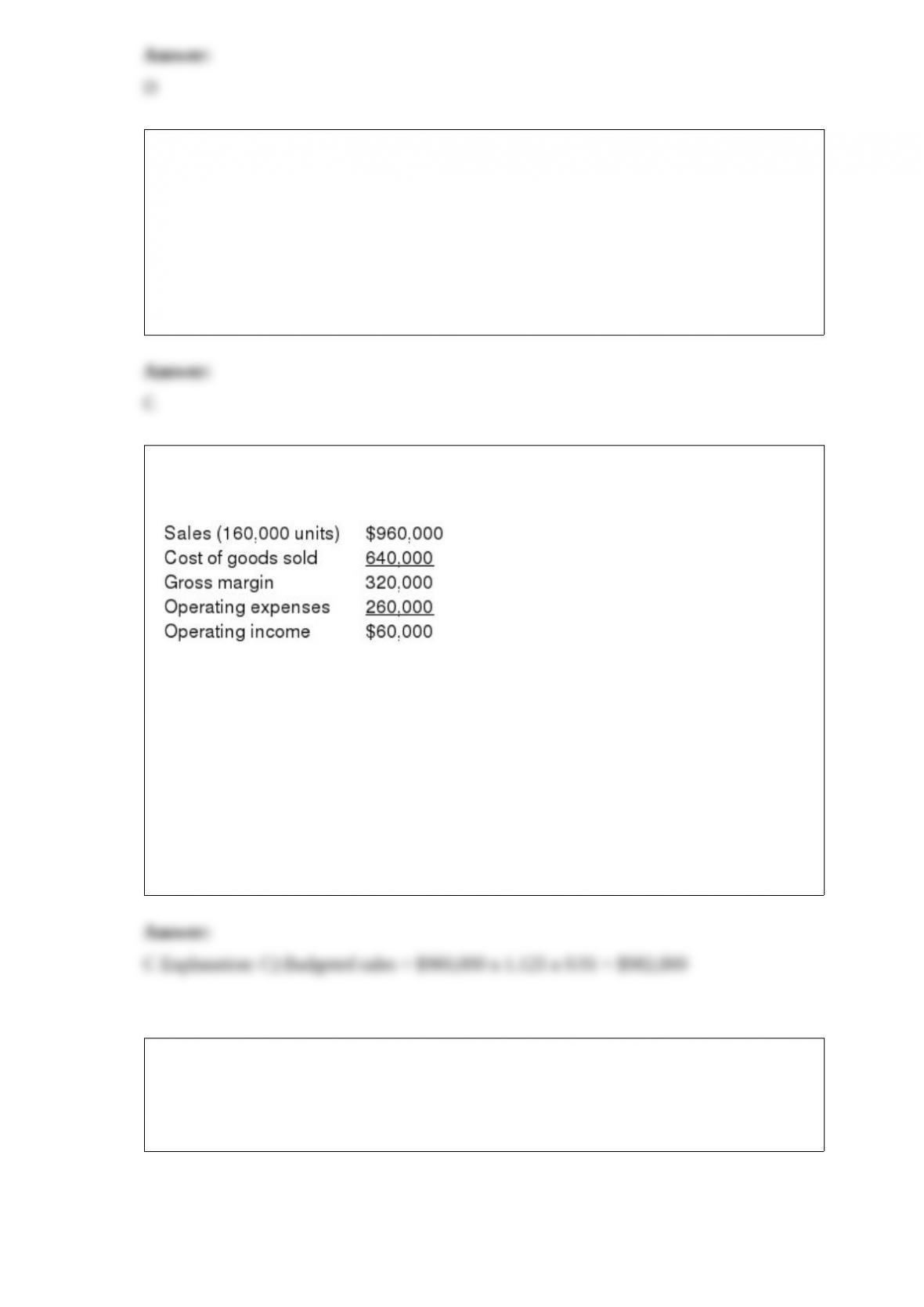

8) Kramer Enterprises reports year-end information from 2015 as follows:

Kramer is developing the 2016 budget. In 2016 the company would like to increase

selling prices by 12.5%, and as a result expects a decrease in sales volume of 9%. All

other operating expenses are expected to remain constant. Assume that cost of goods

sold is a variable cost and that operating expenses are a fixed cost.

What is budgeted sales for 2016?

A) $1,080,000

B) $1,000,000

C) $982,800

D) $873,600

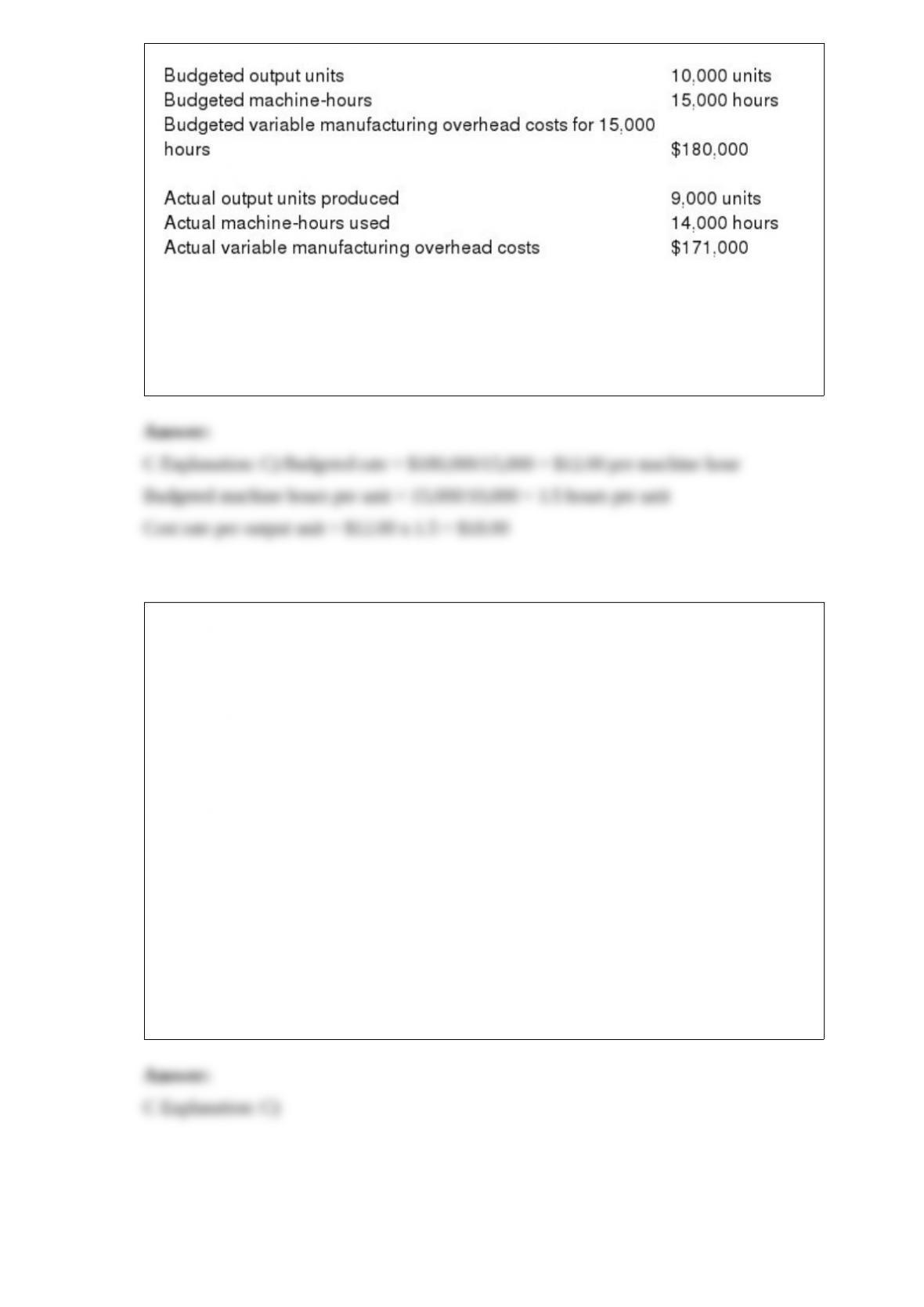

9) Christine Corporation manufactures baseball uniforms and uses budgeted

machine-hours to allocate variable manufacturing overhead. The following information

pertains to the company’s manufacturing overhead data:

What is the budgeted variable overhead cost rate per output unit?

A) $12.00

B) $12.21

C) $18.00

D) $19.00

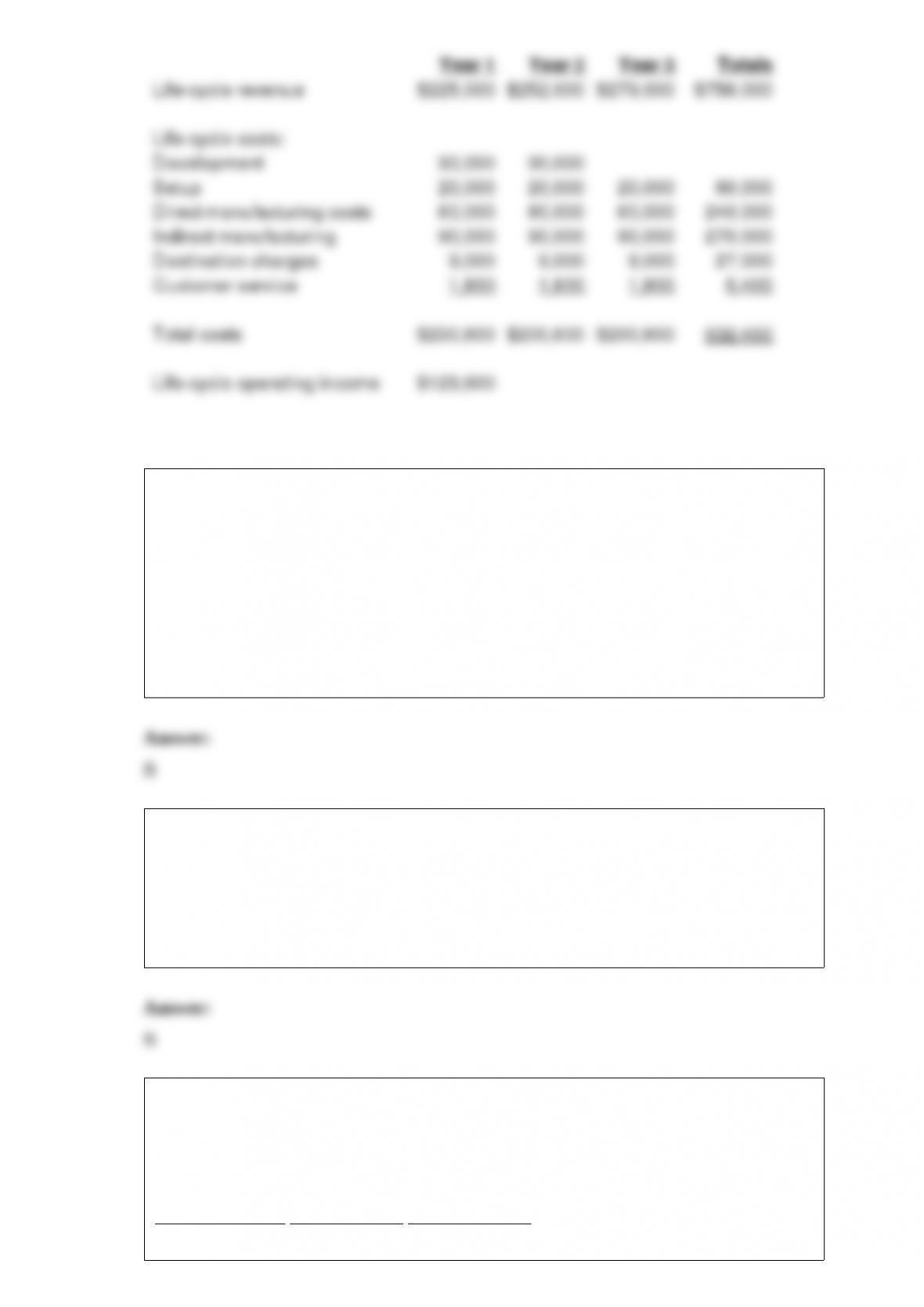

10) Purple Purpose Inc., is in the process of evaluating a new product using the

following information:

A new transformer has two production runs each year, each with $10,000 in setup costs.

The new transformer incurred $30,000 in development costs and is expected to be

produced over the next three years.

Direct costs of producing the transformers are $40,000 per run of 4,500 transformers

each.

Indirect manufacturing costs charged to each run are $45,000.

Destination charges for each transformer average $1.00.

Customer service expenses average $0.20 per transformer.

The transformers are selling for $25 the first year and will increase by $3 each year

thereafter.

Sales units equal production units each year.

What is the estimated life-cycle operating income for the first three years?

A) $63,600

B) $96,600

C) $123,600

D) $150,600

11) Which of the following statements is true of ABC systems?

A) ABC systems provide less insight than traditional systems into the management of

the indirect costs.

B) ABC systems are used by managers for strategic decisions rather than for inventory

valuation in merchandising companies.

C) Service companies find great value from ABC because a vast majority of their cost

structure is composed of direct costs.

D) ABC systems is valuable for pricing decisions but not for understanding, managing,

and reducing costs in government institutions.

12) Which of the following is a stage of the capital budgeting process during which a

plant manager is queried for assembly time?

A) make decisions by choosing among alternatives stage

B) obtain information stage

C) make predictions stage

D) implement the decision, evaluate performance, and learn stage

13) The top management at Groundsource Company, a manufacturer of lawn and

garden equipment, is attempting to recover from a fire that destroyed some of their

accounting records. The main computer system was also severely damaged. The

following information was salvaged:

Tractor Division Tiller Division Digger Division

Sales $10,000,000 (a) $2,400,000

Net operating income $1,000,000 $1,440,000 $600,000

Operating assets (b) (c) $2,000,000

Return on investment 0.2 0.1 (d)

Return on sales (e) 0.12 0.25

Investment turnover (f) (g) 1.2

What is the value of the operating assets belonging to the Tiller Division?

A) $ 10,000,000

B) $ 12,000,000

C) $ 14,400,000

D) $ 15,000,000

14) Relevant total costs in the economic order quantity decision model equal relevant

ordering costs plus relevant ________.

A) carrying costs

B) stockout costs

C) quality costs

D) purchasing costs

15) Which of the following is a disadvantage of using the standards developed by a firm

itself to develop a budget?

A) A firm’s inefficiencies will be part of the data.

B) They are not based on realized benchmarks.

C) The expected future changes are not included in the standards.

D) The flexible-budget amounts are difficult to determine.

16) In an effective balanced scorecard, ________.

A) net income serves as the best indicator for the hard-to measure long-run nonfinancial

performance

B) sales budget serves as one of the leading indicator for the hard-to measure short-run

financial performance

C) sales budget serves as a leading indicator for the hard-to measure short-run

nonfinancial performance

D) customer satisfaction serves as one of the leading indicator for the hard-to measure

long-run financial performance

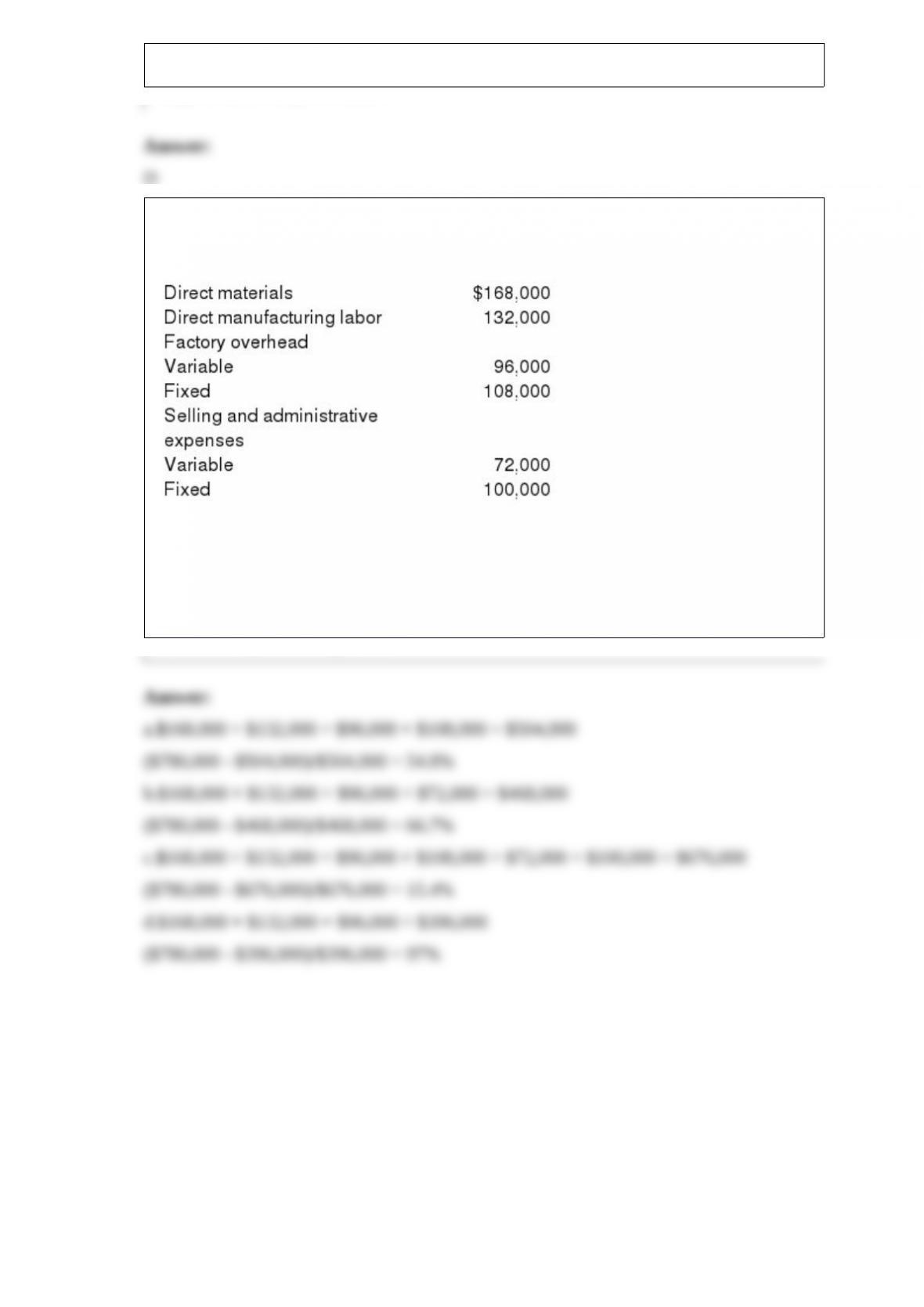

17) Timothy Company has budgeted sales of $780,000 with the following budgeted

costs:

Compute the average markup percentage for setting prices as a percentage of:

a.Total manufacturing costs

b.The variable cost of the product

c.The full cost of the product

d.Variable manufacturing costs