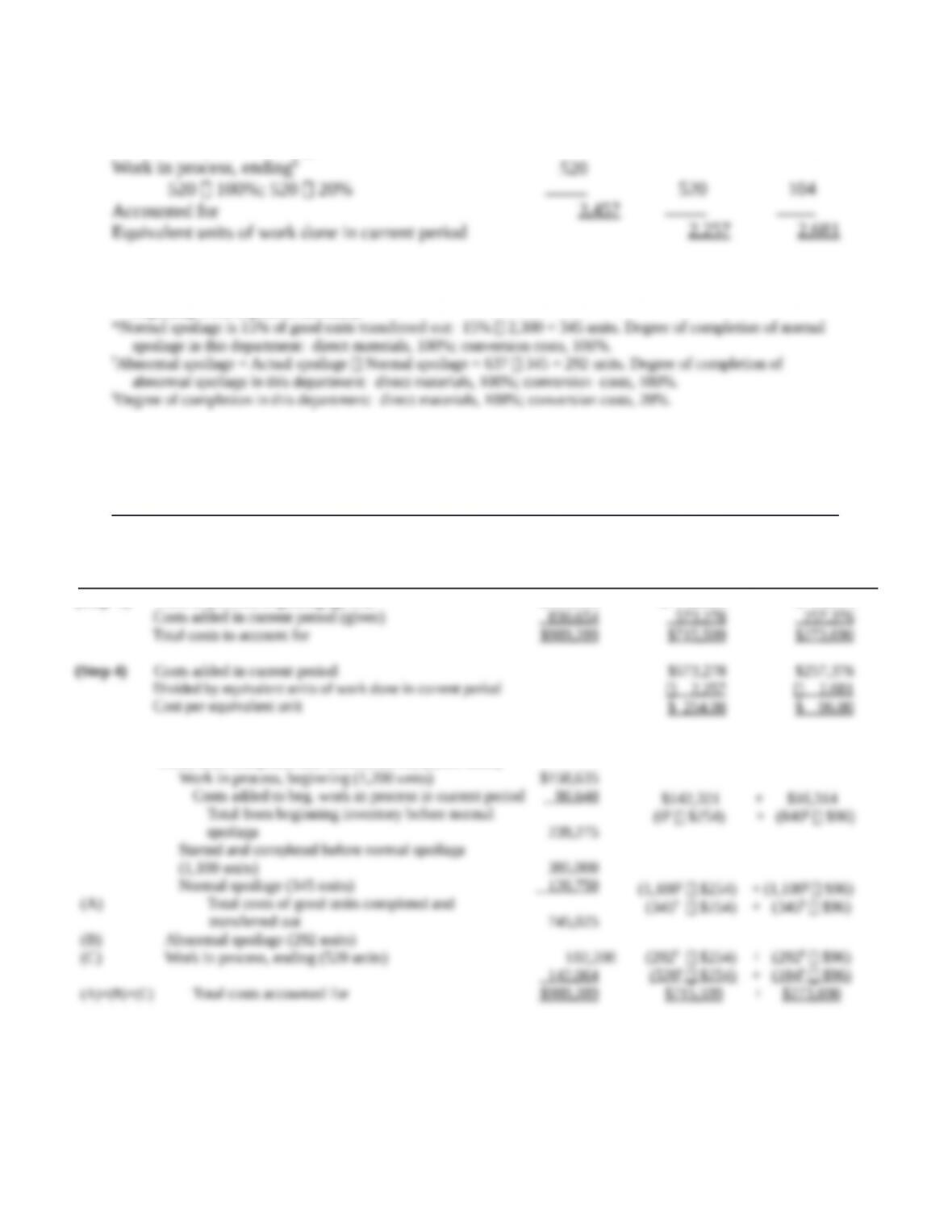

(A) Total cost of good units completed and

transferred out

(B) Abnormal spoilage (292 units)

(C) Work-in-process, ending (520 units)

785,565

86,724

117,000

(292# $207) + (292# $90)

(520# $207) + (104# $90)

(A)+(B)+(C) Total costs accounted for

$989,289

$715,599

$273,690

# Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

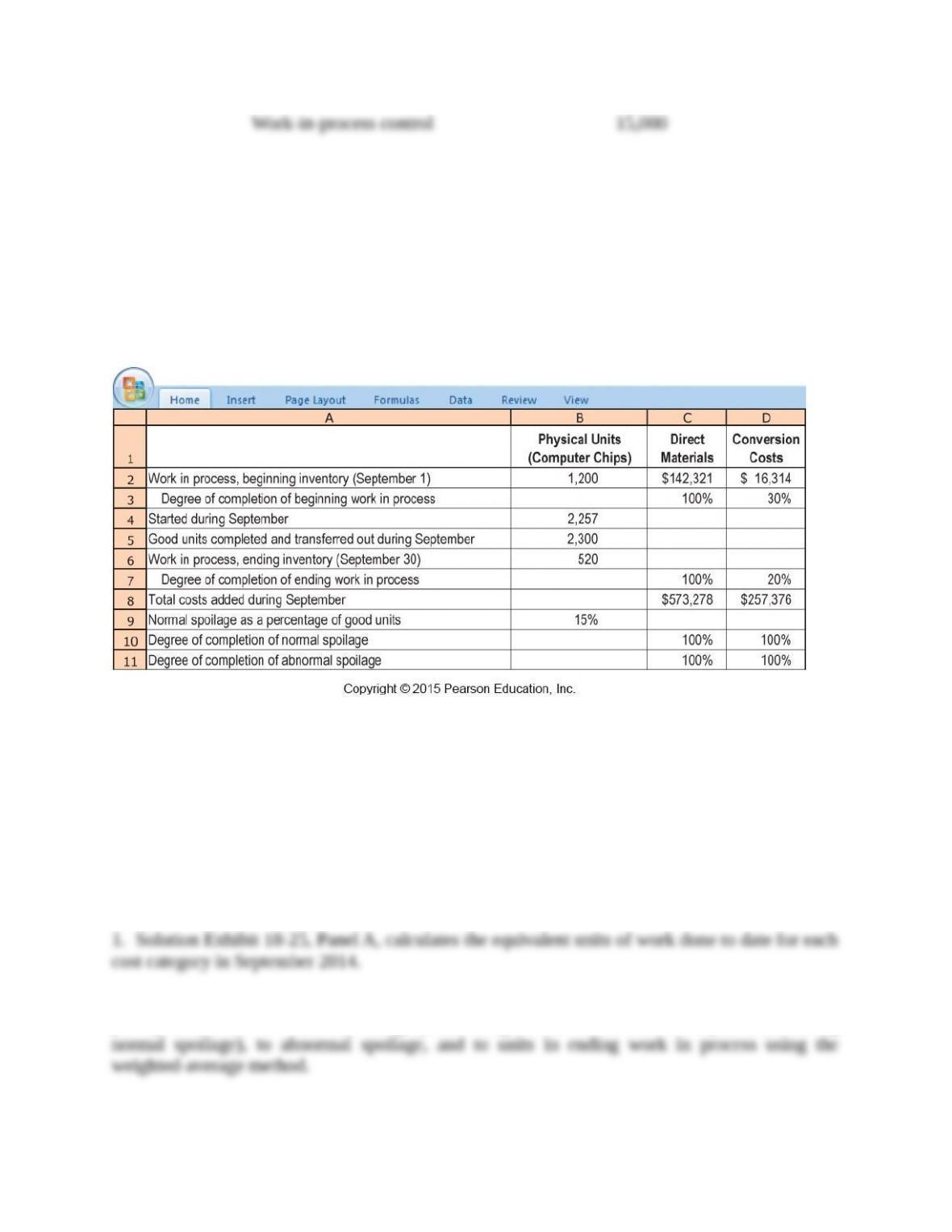

18-26 (25 min.) FIFO method, spoilage.

Refer to the information in Exercise 18-25.

Required:

1. Do Exercise 18-25 using the FIFO method of process costing.

2. Should WaferCo’s managers choose the weighted-average method or the FIFO method?

Explain briefly.

SOLUTION

1. Solution Exhibit 18-26, Panel A, calculates the equivalent units of work done in the current

period for each cost category in September 2014.

Solution Exhibit 18-26, Panel B, summarizes WaferCo’s production costs for September

2014, calculates the costs per equivalent unit for each cost category, and assigns total costs to units

completed and transferred out (including normal spoilage) to abnormal spoilage and to units in

ending work in process under the FIFO method.

SOLUTION EXHIBIT 18-26

First-in, First-out (FIFO) Method of Process Costing with Spoilage,

WaferCo for September 2014

PANEL A: Summarize the Flow of Physical Units and Compute Output in Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

From beginning work in process||

1,200 (100% −100%); 1,200 (100% − 30%)

Started and completed

1,100 100%; 1,100 100%

Normal spoilage*

1,200

2,557

3,457

1,200

1,100#

345

0

1,100

345

840

1,100

345

345 100%; 345 100%

Abnormal spoilage†

292 100%; 292 100%

Work in process, ending‡

520 100%; 520 20%

Accounted for

Equivalent units of work done in current period

292

520

3,457

292

520

2,257

292

104

2,681

||Degree of completion in this department: direct materials, 100%; conversion costs, 30%.

#2,300 physical units completed and transferred out minus 1,200 physical units completed and transferred out from

beginning work in process inventory.

*Normal spoilage is 15% of good units transferred out: 15% 2,300 = 345 units. Degree of completion of normal

spoilage in this department: direct materials, 100%; conversion costs, 100%.

†Abnormal spoilage = Actual spoilage − Normal spoilage = 637 − 345 = 292 units. Degree of completion of

abnormal spoilage in this department: direct materials, 100%; conversion costs, 100%.

‡Degree of completion in this department: direct materials, 100%; conversion costs, 20%.

PANEL B: Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in–Process

Inventory

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs added in current period

Divided by equivalent units of work done in current period

Cost per equivalent unit

(Step 5) Assignment of costs:

Good units completed and transferred out (2,300 units)

$158,635

830,654

$989,289

$ 142,321

573,278

$715,599

$573,278

2,257

$ 254.00

$ 16,314

257,376

$273,690

$257,376

2,681

$ 96.00

Work in process, beginning (1,200 units)

Costs added to beg. work in process in current period

Total from beginning inventory before normal

spoilage

Started and completed before normal spoilage

(1,100 units)

Normal spoilage (345 units)

(A) Total costs of good units completed and

transferred out

(B) Abnormal spoilage (292 units)

(C) Work in process, ending (520 units)

$158,635

80,640

239,275

385,000

120,750

745,025

102,200

142,064

$142,321 + $16,314

(0§ $254) + (840§ $96)

(1,100§ $254) + (1,100§ $96)

(345§ $254) + (345§ $96)

(292§ $254) + (292§ $96)

(520§ $254) + (104§ $96)

(A)+(B)+(C) Total costs accounted for

$989,289

$715,599

+ $273,690

§Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A.

Beginning

Inventory

Work Done in

Current Period

Direct materials

Conversion costs

Total cost per unit

$118.60 ($142,321 1,200 equiv. units)

45.32 ($ 16,314 360 equiv. units)

$163.92

$254.00

96.00

$350.00

Direct

Materials

Conversion

Costs

Cost per equivalent unit (weighted-average)

$207*

$90*

Cost per equivalent unit (FIFO)

$254**

$96**

* from Solution Exhibit 18-25, Panel B

**from Solution Exhibit 18-26, Panel B

The cost per equivalent unit differs between the two methods because each method uses different

costs as the numerator of the calculation. FIFO uses only the costs added during the current period

whereas weighted-average uses the costs from the beginning work–in–process as well as costs

added during the current period. Both methods also use different equivalent units in the

denominator.

The following table summarizes the costs assigned to units completed and those still in

process under the weighted-average and FIFO process-costing methods for our example.

FIFO

(Solution

Exhibit 18-26B)

Wtd.-Avg.

(Solution

Exhibit 18-25B)

Difference

Cost of units completed and transferred out

Abnormal spoilage

Work in process, ending

Total costs accounted for

$745,025

102,200

142,064

$989,289

$785,565

86,724

117,000

$989,289

− $40,540

+ $15,476

+ $25,064

The FIFO ending inventory is higher than the weighted-average ending inventory by $25,064. This

is because FIFO assumes that all the lower-cost prior-period units in work in process are the first

to be completed and transferred out while ending work in process consists of only the higher-cost

current-period units. The weighted-average method, in contrast, smoothes the cost per equivalent

unit by assuming that more of the higher-cost units are completed and transferred out, while some

lower-cost units in beginning work in process are placed in ending work in process. It similarly

costs the abnormal spoilage incurred during the period using a blended cost rate rather than the

higher current-period cost (as in the FIFO method, which assigns $15,476 more in costs to that

spoilage). As a result, the FIFO method results in a relatively lower cost of units completed and

transferred out and a higher ending work-in-process inventory.

WaferCo’s managers should consider the weighted-average method because it leads to a

higher cost of goods completed and transferred (and sold), thereby lowering taxes. The managers

may have an incentive, however, to use the FIFO method and show a higher level of current

income if their compensation increases with higher operating income or if there are debt

covenants that would be violated by showing lower income. WaferCo’s managers may also

consider advantage of the FIFO method, which is that it provides better information for

spoilage

Started and completed before normal spoilage

(1,100 units)

Normal spoilage (345 units)

(A) Total costs of good units completed and

transferred out

(B) Abnormal spoilage (292 units)

(C) Work in process, ending (520 units)

(A)+(B)+(C) Total costs accounted for

374,000

117,300

899,300

99,280

135,200

$1,133,780

(1,100§ $240) + (1,100§ $100)

(345§ $240) + (345§ $100)

(292§ $240) + (292§ $100)

(520§ $240) + (104§ $100)

$829,680 + $304,100

*Work in process, beginning has 1,200 equivalent units (1,200 physical units 100%) of direct materials and 360

equivalent units (1,200 physical units 30%) of conversion costs.

§Equivalent units of direct materials and conversion costs calculated in Step 2 in Solution Exhibit 18-25, Panel A.

2. To show better performance, a department supervisor might report a higher degree of

completion resulting in understated cost per equivalent unit and overstated operating income. If

performance for the period is very good, the department supervisor may be tempted to report a

lower degree of completion reducing income in the current period. This has the effect of

reducing the costs carried in ending inventory and the costs carried to the following year in

beginning inventory. In other words, estimates of degree of completion can help to smooth

earnings from one period to the next.

To guard against the possibility of bias, managers should ask supervisors specific

questions about the process they followed to prepare estimates. Top management should always

emphasize obtaining the correct answer, regardless of how it affects reported performance. This

emphasis drives ethical actions throughout the organization.

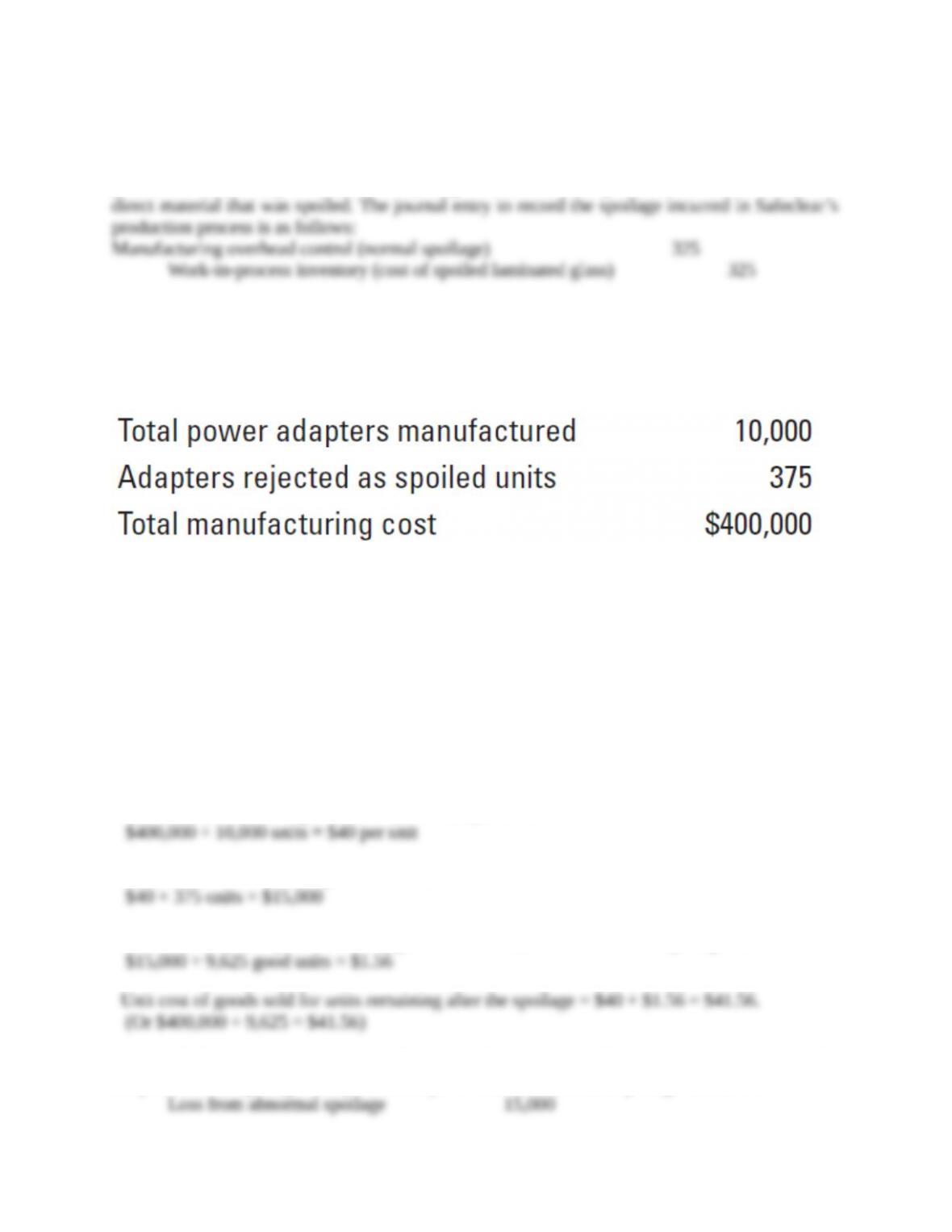

18-28 (20–30 min.) Spoilage and job costing.

(L. Bamber) Barrett Kitchens produces a variety of items in accordance with special job orders

from hospitals, plant cafeterias, and university dormitories. An order for 2,100 cases of mixed

vegetables costs $9 per case: direct materials, $4; direct manufacturing labor, $3; and

manufacturing overhead allocated, $2. The manufacturing overhead rate includes a provision for

normal spoilage. Consider each requirement independently.

Required:

1. Assume that a laborer dropped 420 cases. Suppose part of the 420 cases could be sold to a

nearby prison for $420 cash. Prepare a journal entry to record this event. Calculate and explain

briefly the unit cost of the remaining 1,680 cases.

2. Refer to the original data. Tasters at the company reject 420 of the 2,100 cases. The 420 cases

are disposed of for $840. Assume that this rejection rate is considered normal. Prepare a journal

entry to record this event, and do the following:

a. Calculate the unit cost if the rejection is attributable to exacting specifications of this

particular job.

b. Calculate the unit cost if the rejection is characteristic of the production process and is not

attributable to this specific job.

c. Are unit costs the same in requirements 2a and 2b? Explain your reasoning briefly.

3. Refer to the original data. Tasters rejected 420 cases that had insufficient salt. The product can