Account

Dec. 31, 2014

Account

Balance

(Before

Proration)

(1)

Allocated

Manuf.

Overhead in

Dec. 31, 2014

Balance

(Before

Proration)

(2)

Allocated Manuf.

Overhead in

Dec. 31, 2014

Balance as a

Percent of Total

(3) = (2) ÷ $114,000

Proration of $3,000

Underallocated

Manuf. Overhead

(4) = (3)

$3,000

Dec. 31, 2014

Account

Balance

(After

Proration)

(5) = (1) + (4)

WIP

$ 50,700

$ 10,260a

0.09

0.09

$3,000 = $ 270

$ 50,970

Finished Goods

245,050

29,640b

0.26

0.26

$3,000 = 780

245,830

Cost of Goods Sold

549,250

74,100c

0.65

0.65

$3,000 = 1,950

551,200

Total

$845,000

$114,000

1.00

$3,000

$848,000

a,b,c Overhead allocated = Direct manuf. labor cost

50% = $20,520; $59,280; $148,200

50%

4. Writing off all of the underallocated manufacturing overhead to Cost of Goods Sold (CGS) is

usually warranted when CGS is large relative to Work-in–Process and Finished Goods Inventory

and the underallocated manufacturing overhead is immaterial. Both these conditions apply in this

case. ROW should write off the $3,000 underallocated manufacturing overhead to Cost of Goods

Sold Account.

overhead rate

1. Budgeted manufacturing

=

Budgeted manufacturing overhead cost

Budgeted direct manufacturing labor cost

$125,000 50% of direct manufacturing labor cost

$250,000

==

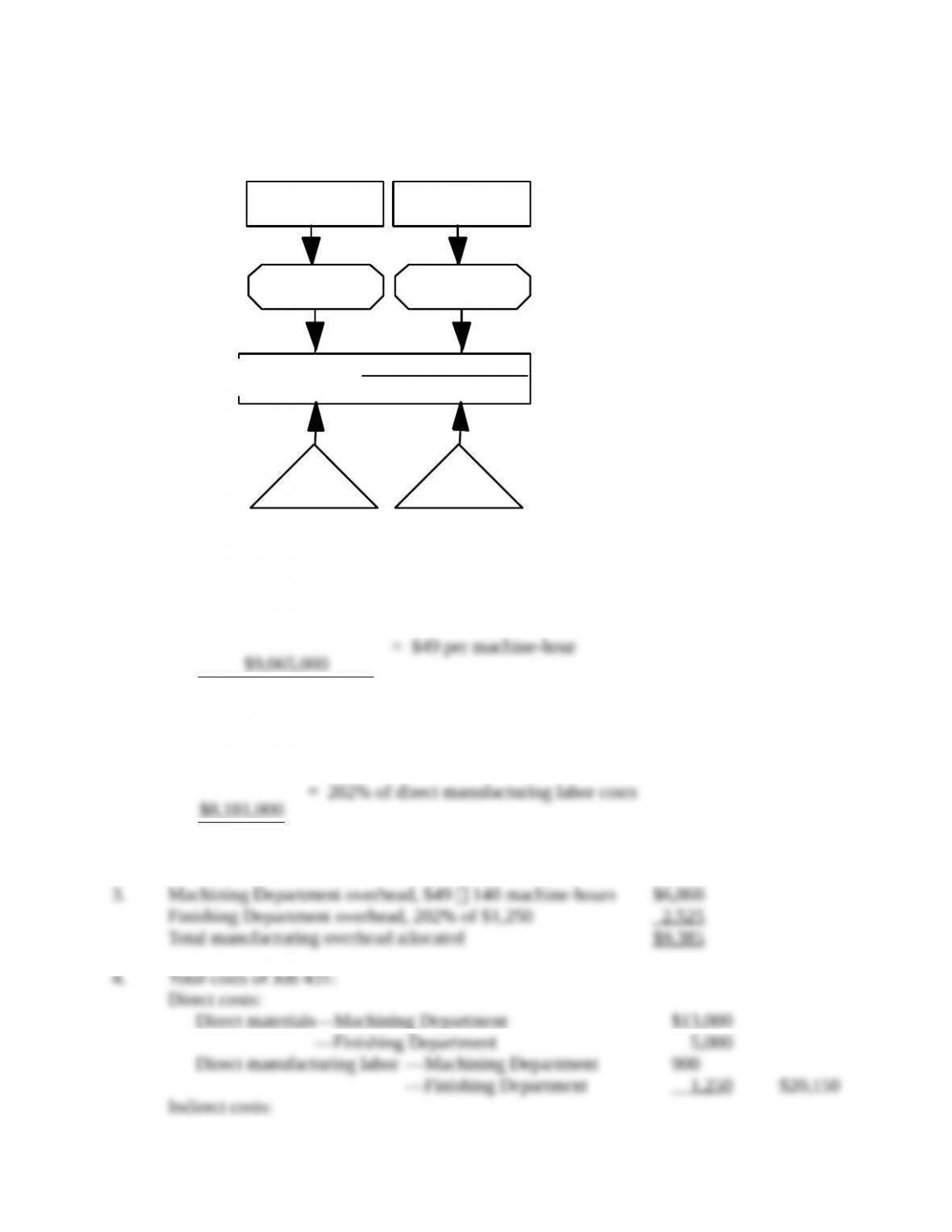

4-31 (20−30 min) Job costing, accounting for manufacturing overhead, budgeted rates.

The Pisano Company uses a job–costing system at its Dover, Delaware, plant. The plant has a

machining department and a finishing department. Pisano uses normal costing with two direct-cost

categories (direct materials and direct manufacturing labor) and two manufacturing overhead cost

pools (the machining department with machine- hours as the allocation base and the finishing

department with direct manufacturing labor costs as the allocation base). The 2014 budget for the

plant is as follows:

Machining Department

Finishing Department

Manufacturing overhead costs

$9,065,000

$8,181,000

Direct manufacturing labor costs

$ 970,000

$4,050,000

Direct manufacturing labor-hours

36,000

155,000

Machine-hours

185,000

37,000

Required:

1. Prepare an overview diagram of Pisano’s job-costing system.

2. What is the budgeted manufacturing overhead rate in the machining department? In the

finishing department?

3. During the month of January, the job-cost record for Job 431 shows the following:

Budgeted total costs in indirect cost pool

Budgeted indirect

Budgeted total costs in indirect cost pool