Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

21-1

SOLUTION

1. The after-tax cash inflow per year is $24,400 ($19,600 + $4,800), as shown below:

Annual cash flow from operations ($43,000 – $15,000)

$28,000

Deduct income tax payments (0.30 $28,000)

8,400

Annual after-tax cash flow from operations

$19,600

Annual depreciation on upgrades ($80,000 5 years)

$16,000

Income tax cash savings from annual depreciation deductions

(0.30 $16,000)

$ 4,800

The expected increase in net annual income is $8,400, the difference between the after-

tax cash inflow of $24,400 and the annual depreciation of $16,000. This can also be

computed directly as follows:

Incremental margins

$43,000

Deduct incremental cash expenses

15,000

Deduct depreciation on upgrades

16,000

Pre-tax incremental income

$12,000

Incremental tax (0.30 $12,000)

3,600

After-tax incremental income

$ 8,400

2. The average level of investment in the project is

$100,000 $20,000

2

+

= $60,000.

The after-tax incremental income from the project (from requirement 1) is $8,400.

The accrual accounting rate of return on average investment is therefore

$8,400

$60,000

= 14%.

1. The project is not worth investing in from an NPV standpoint. Its NPV is $(698),

calculated as follows:

Present value of 5-year annuity of $24,400 at 12%

$24,400 3.605 $ 87,962

Present value of $20,000 disposal value at end of 5 years

$20,000 0.567 11,340

Present value of cash outlays, $100,000 1.000 (100,000)

Net present value $ (698)

21-2

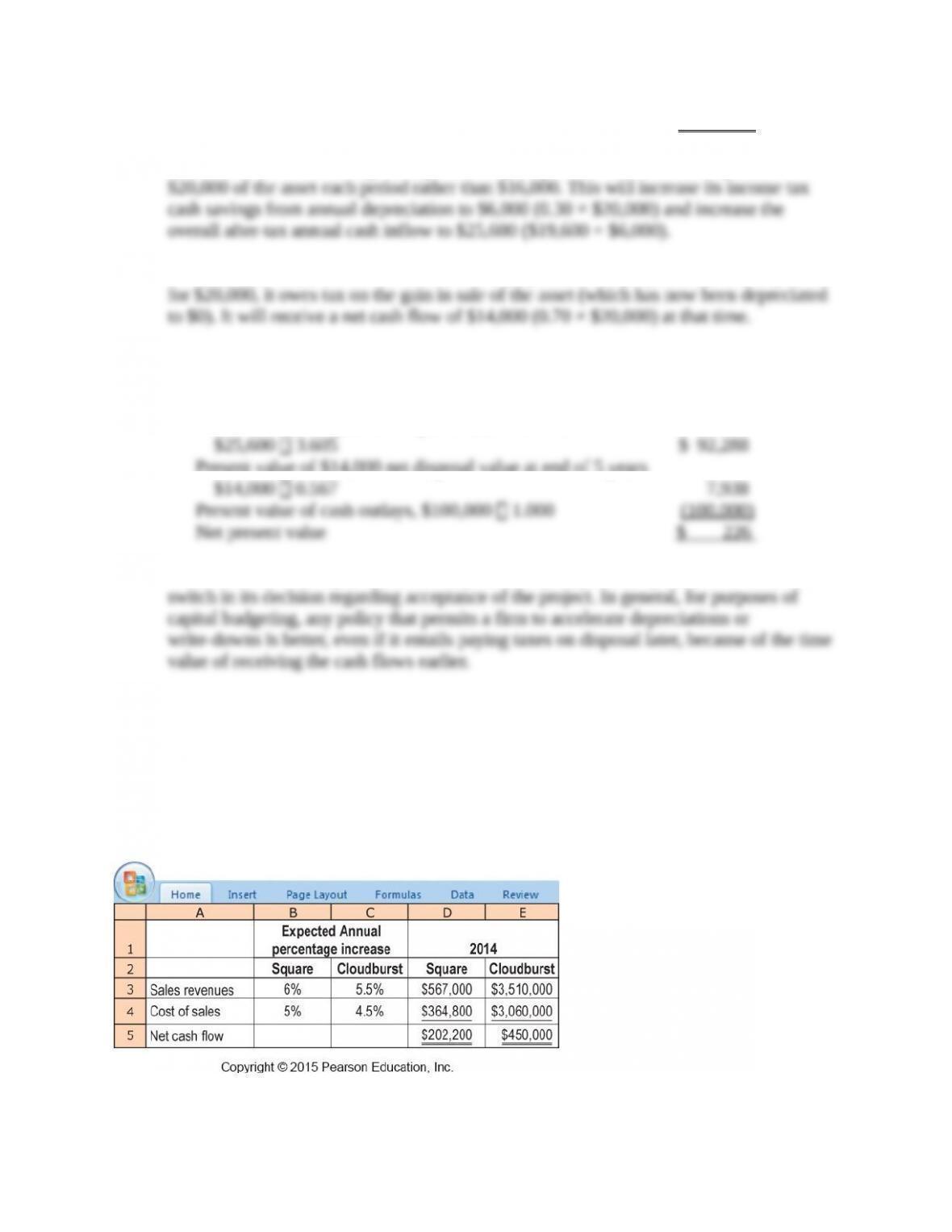

4. The first effect of the change in depreciation policy is that Harrison can depreciate

$20,000 of the asset each period rather than $16,000. This will increase its income tax

cash savings from annual depreciation to $6,000 (0.30 × $20,000) and increase the

overall after-tax annual cash inflow to $25,600 ($19,600 + $6,000).

The second effect is that now when Harrison disposes of the project at the end of year 5

for $20,000, it owes tax on the gain in sale of the asset (which has now been depreciated

to $0). It will receive a net cash flow of $14,000 (0.70 × $20,000) at that time.

The project is now worth investing in from an NPV standpoint. Its NPV is $226,

calculated as follows:

Present value of 5-year annuity of $25,600 at 12%

$25,600 3.605 $ 92,288

Present value of $14,000 net disposal value at end of 5 years

$14,000 0.567 7,938

Present value of cash outlays, $100,000 1.000 (100,000)

Net present value $ 226

From Harrison’s standpoint, the new depreciation policy is clearly better and leads to a

switch in its decision regarding acceptance of the project. In general, for purposes of

capital budgeting, any policy that permits a firm to accelerate depreciations or write-

downs is better, even if it entails paying taxes on disposal later, because of the time value

of receiving the cash flows earlier.

21-27 (40 min.) Customer value.

Ortel Telecom sells telecommunication products and services to a variety of small businesses. Two

of Ortel’s key clients are Square and Cloudburst, both fast-growing technology start- ups located

in New York City. Ortel has compiled information regarding its transactions with Square and

Cloudburst for 2014, as well as its expectations regarding their interactions for the next 3 years:

Ortel’s transactions with Square and Cloudburst are in cash. Assume that they occur at year-end.

Ortel is headquartered in the Cayman Islands and pays no income taxes. The owners of Ortel insist

on a required rate of return of 12%.

21-3

Required:

1. What is the expected net cash flow from Square and Cloudburst for the next 3 years?

2. Based on the net present value from cash flows over the next 3 years, is Cloudburst or Square

a more valuable customer for Ortel?

3. Cloudburst threatens to switch to another supplier unless Ortel gives a 10% price reduction on

all sales starting in 2015. Calculate the 3-year NPV of Cloudburst after incorporating the 10%

discount. Should Ortel continue to transact with Cloudburst? What other factors should it

consider before making its final decision?

SOLUTION

1.

Square

Annual

Increases*

2014

2015

2016

2017

Cash Revenues

6%

$567,000

$601,020

$637,081

$675,306

Cash Expenses

5%

364,800

383,040

402,192

422,302

Net Cash Flows

$202,200

$217,980

$234,889

$ 253,004

Cloudburst

Annual

Increases*

2014

2015

2016

2017

Cash Revenues

5.5%

$3,510,000

$3,703,050

$3,906,718

$4,121,587

Cash Expenses

4.5%

3,060,000

3,197,700

3,341,597

3,491,968

Net Cash Flows

$ 450,000

$ 505,350

$ 565,121

$ 629,619

*Given in the problem.

2.

Square

Cloudburst

Year

PV Factor

for 12%

Net Cash

Flows

Present

Value

Net Cash

Flows

Present

Value

2015

0.893

$217,980

$194,625

$505,350

$451,205

2016

0.797

234,889

187,252

565,121

450,511

2017

0.712

253,004

180,084

629,619

448,150

$561,961

$1,349,867

Based on NPV at 12%, Cloudburst is the more valuable customer.

3. Assuming a 10% discount on the revenues for Cloudburst calculated in requirement 1, we

have

Cloudburst

Annual

Increases

2014

2015

2016

2017

Cash Revenues*

5.5%

$3,510,000

$3,332,745

$3,516,046

$3,709,428

Cash Expenses

4.5%

3,060,000

3,197,700

3,341,597

3,491,968

Net Cash Flows

$ 450,000

$ 135,045

$ 174,449

$ 217,460

* Cloudburst’s revenue from requirement 1 reduced by 10% each year from 2015 onwards.

Net present value if revenues are reduced by 10% each year relative to original estimates:

Cloudburst

Year

PV Factor

for 12%

Net Cash

Flows

Present

Value

2015

0.893

$135,045

$120,576

2016

0.797

174,449

139,070

2017

0.712

217,460

154,784

$513,430

21-5

The 10% discount and reduced subsequent annual revenue reduces the NPV substantially

from $1,349,867 to $513,430. The NPV is still positive, and so Ortel should continue to sell to

Cloudburst. However, this is a little over 60% drop in NPV from Cloudburst, and it makes Square

the more profitable customer.

Ortel should consider whether the price discount demanded by Cloudburst needs to be met

in its entirety to keep the account. The implication of meeting the full demand is that the account is

minimally profitable. A serious concern is whether Square will also demand comparable price

discounts if Cloudburst’s demands are met. This could result in large reductions in the NPVs of all

of Ortel’s customers.

Ortel should also consider the reliability of the growth estimates used in computing the

NPVs. Are the predicted differences in revenue growth rates based on reliable information? Many

revenue growth estimates by salespeople turn out to be overestimates or occur over a longer time

period than initially predicted.

21-28 (60 min.) Selling a plant, income taxes.

(CMA, adapted) The Lucky Seven Company is an international clothing manufacturer. Its

Redmond plant will become idle on December 31, 2014. Peter Laney, the corporate controller, has

been asked to look at three options regarding the plant:

▪ Option 1: The plant, which has been fully depreciated for tax purposes, can be sold

immediately for $900,000.

▪ Option 2: The plant can be leased to the Preston Corporation, one of Lucky Seven’s

suppliers, for 4 years. Under the lease terms, Preston would pay Lucky Seven $220,000 rent

per year (payable at year-end) and would grant Lucky Seven a $40,000 annual discount off

the normal price of fabric purchased by Lucky Seven. (Assume that the discount is received

at year-end for each of the 4 years.) Preston would bear all of the plant’s ownership costs.

Lucky Seven expects to sell this plant for $150,000 at the end of the 4-year lease.

▪ Option 3: The plant could be used for 4 years to make souvenir jackets for the Olympics.

Fixed over- head costs (a cash outflow) before any equipment upgrades are estimated to be

$20,000 annually for the 4-year period. The jackets are expected to sell for $55 each. Variable

cost per unit is expected to be $43. The following production and sales of jackets are

expected: 2015, 18,000 units; 2016, 26,000 units; 2017, 30,000 units; 2018, 10,000 units. In

order to manufacture the jackets, some of the plant equipment would need to be upgraded at

an immediate cost of $160,000. The equipment would be depreciated using the straight-line

depreciation method and zero terminal disposal value over the 4 years it would be in use.

Because of the equipment upgrades, Lucky Seven could sell the plant for $270,000 at the

end of 4 years. No change in working capital would be required.

Lucky Seven treats all cash flows as if they occur at the end of the year, and it uses an after-tax

required rate of return of 10%. Lucky Seven is subject to a 35% tax rate on all income, including

capital gains.

21-6

Required:

1. Calculate net present value of each of the options and determine which option Lucky Seven

should select using the NPV criterion.

2. What nonfinancial factors should Lucky Seven consider before making its choice?

SOLUTION

1. Option 1

Current disposal price $900,000

Deduct current book value 0

Gain on disposal 900,000

Deduct 35% tax payments 315,000

Net present value $585,000

Option 2

Lucky Seven receives three sources of cash inflows:

a. Rent. Four annual payments of $220,000. The after-tax cash inflow is:

$220,000 × (1 – 0.35) = $143,000 per year

b. Discount on material purchases, payable at year-end for each of the four years: $40,000

The after-tax cash inflow is: $40,000 × (1 – 0.35) = $26,000

c. Sale of plant at year-end 2018. The after-tax cash inflow is:

$150,000 × (1 – 0.35) = $97,500

Present Value

Total Discount

Present Factors at

Value 10% Sketch of Relevant After-Tax Cash Flows

0 1 2 3 4

1. Rent

$129,987 0.909 $143,000

118,118 0.826 $143,000

107,393 0.751 $143,000

97,669 0.683 $143,000

2. Discount on

Purchases $23,634 0.909 $26,000

21,476 0.826 $26,000

19,526 0.751 $26,000

17,758 0.683 $26,000

3. Sale of plant $ 66,593 0.683 $97,500

Net present value $602,154

21-7

Option 3

Contribution margin per jacket:

Selling price $55.00

Variable costs 43.00

Contribution margin $12.00

2015 2016 2017 2018

Contribution margin

$12.00 × 18,000; 26,000;

30,000; 10,000 $216,000 $312,000 $360,000 $120,000

Fixed overhead (cash) costs 20,000 20,000 20,000 20,000

Annual cash flow from operations 196,000 292,000 340,000 100,000

Income tax payments (35%) 68,600 102,200 119,000 35,000

After-tax cash flow from

operations (excl. depcn.) $127,400 $189,800 $221,000 $65,000

Depreciation: $160,000 ÷ 4 = $40,000 per year

Income tax cash savings from depreciation deduction: $40,000 × 0.35 = $14,000 per year

Sale of plant at end of 2018: $270,000 × (1 – 0.35) = $175,500

Solution Exhibit 21-28 presents the NPV calculations: NPV = $487,181

21-8

SOLUTION EXHIBIT 21-28

Total

Present

Value

Present Value

Discount

Factors at

10%

Sketch of Relevant After-Tax Cash Flows

2014

2015

2016

2017

2018

1a. Initial plant equipment

upgrade investment

$(160,000)

1.000

$(160,000)

1b. Initial working capital

investment

0

1.000

$0

2a. Annual after-tax cash

flow from operations

(excluding depreciation

effects)

Year 1

115,807

0.909

$127,400

Year 2

156,775

0.826

$189,800

Year 3

165,971

0.751

$221,000

Year 4

44,395

0.683

$65,000

2b. Income tax cash savings

from annual depreciation

deductions

Year 1

12,726

0.909

$14,000

Year 2

11,564

0.826

$14,000

Year 3

10,514

0.751

$14,000

Year 4

9,562

0.683

$14,000

3. After-tax cash flow

From

a. Terminal disposal

of plant

119,867

0.683

$175,500

b. Recovery of working

capital

0

0.683

$0

Net present value

$487,181

Option 2 has the highest NPV:

NPV

Option 1 $585,000

Option 2 $602,154

Option 3 $487,181

2. Nonfinancial factors that Lucky Seven should consider include the following:

• Option 1 gives Lucky Seven immediate liquidity that it can use for other projects.

• Option 2 has the advantage of Lucky Seven having a closer relationship with the

supplier. However, it limits Lucky Seven’s flexibility if Preston Corporation’s quality

is not comparable to that of competitors.

• Option 3 has Lucky Seven entering a new line of business. If this line of business is

successful, it could be expanded to cover souvenir jackets for other major events. The

risks of selling the predicted number of jackets should also be considered.

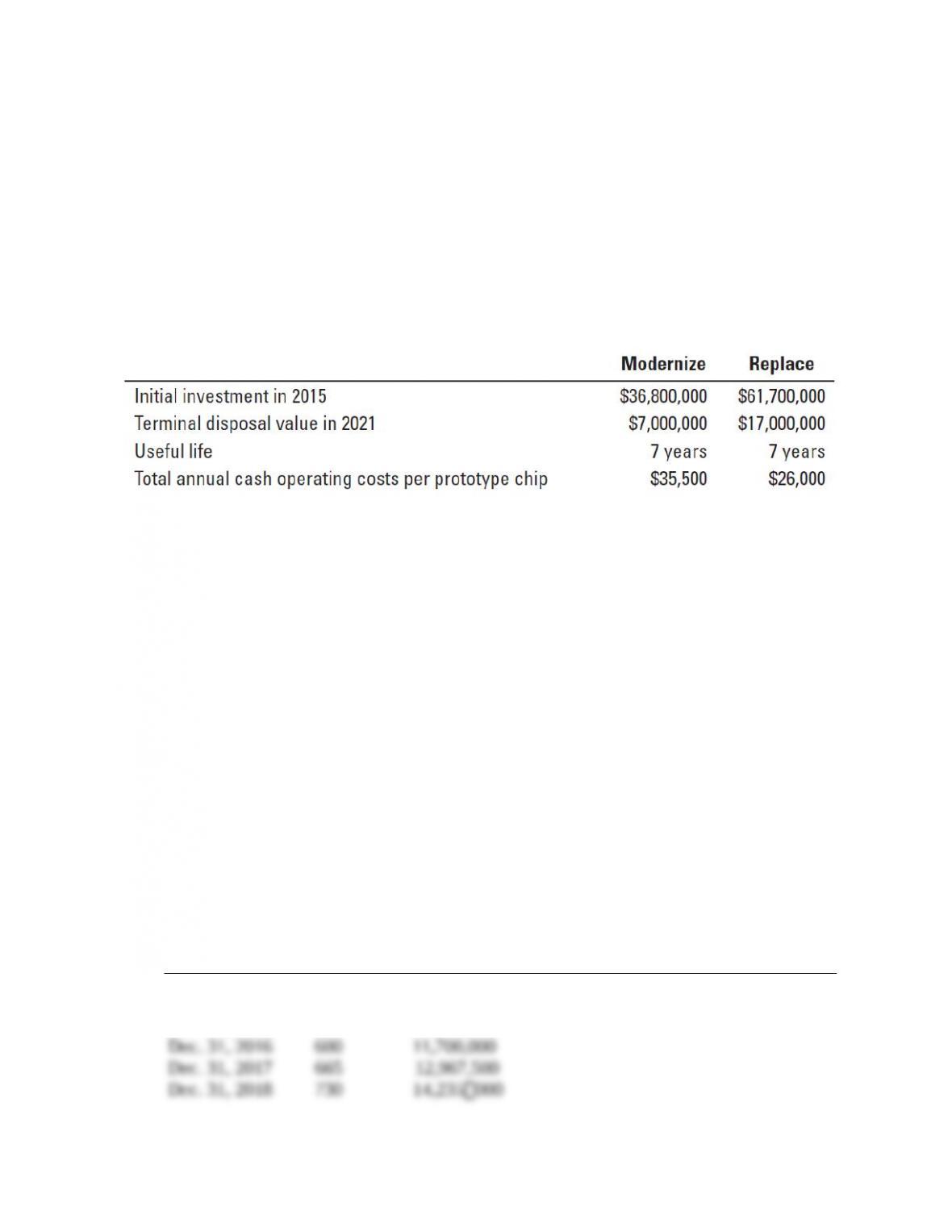

21-29 (60 min.) Equipment replacement, no income taxes.

21-9

Clean Chips is a manufacturer of prototype chips based in Dublin, Ireland. Next year, in 2015,

Clean Chips expects to deliver 535 prototype chips at an average price of $55,000. Clean Chips’

marketing vice president forecasts growth of 65 prototype chips per year through 2021. That is,

demand will be 535 in 2015, 600 in 2016, 665 in 2017, and so on.

The plant cannot produce more than 525 prototype chips annually. To meet future demand,

Clean Chips must either modernize the plant or replace it. The old equipment is fully depreciated

and can be sold for $4,300,000 if the plant is replaced. If the plant is modernized, the costs to

modernize it are to be capitalized and depreciated over the useful life of the updated plant. The old

equipment is retained as part of the modernize alternative. The following data on the two options

are available:

Clean Chips uses straight-line depreciation, assuming zero terminal disposal value. For simplicity,

we assume no change in prices or costs in future years. The investment will be made at the

beginning of 2015, and all transactions thereafter occur on the last day of the year. Clean Chips’

required rate of return is 10%.

There is no difference between the modernize and replace alternatives in terms of required

working capital. Clean Chips has a special waiver on income taxes until 2021.

Required:

1. Sketch the cash inflows and outflows of the modernize and replace alternatives over the 2015–

2021 period.

2. Calculate payback period for the modernize and replace alternatives.

3. Calculate net present value of the modernize and replace alternatives.

4. What factors should Clean Chips consider in choosing between the alternatives?

SOLUTION

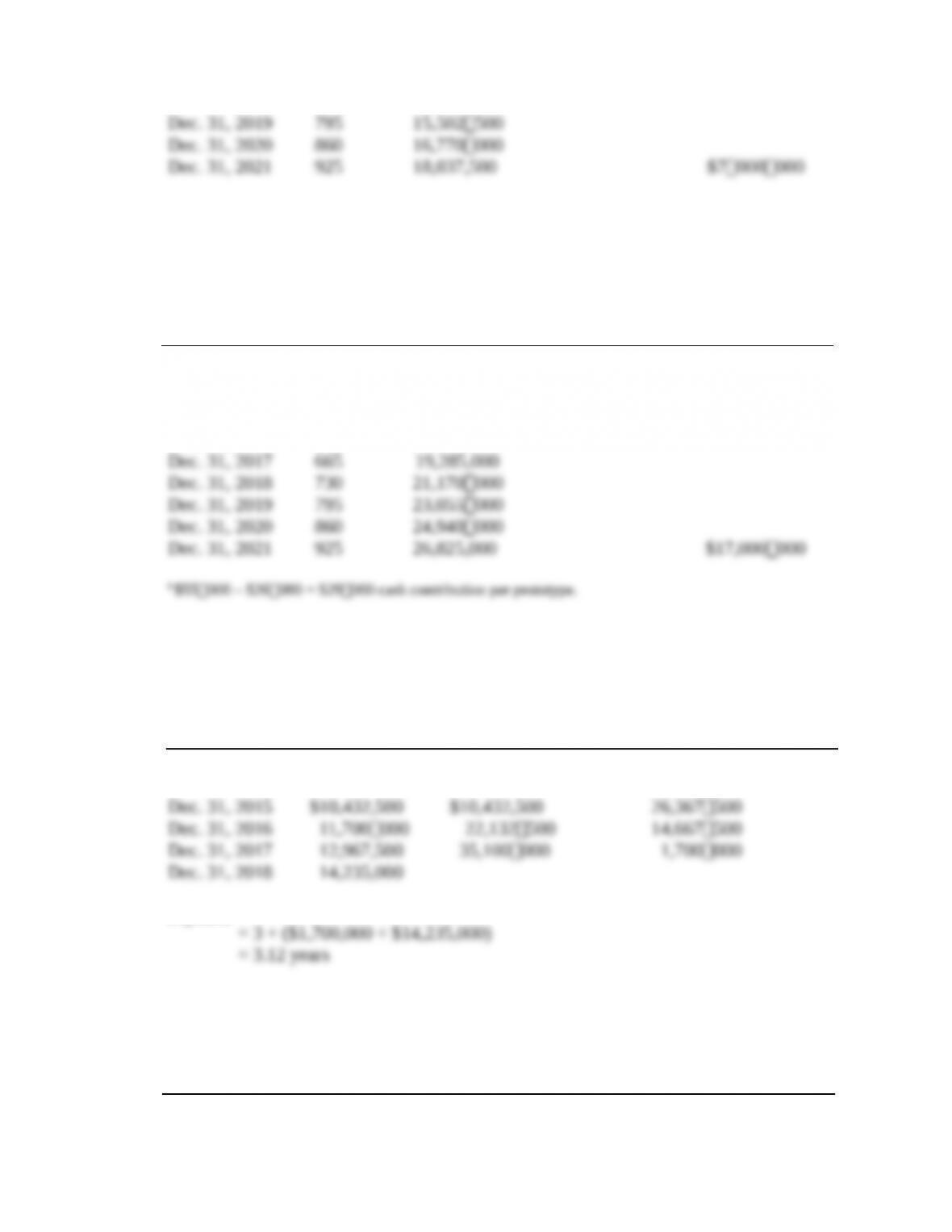

1. Cash flows for modernizing alternative:

Net Cash Initial Sale of Equip.

Year Units Sold Contributions Investments at Termination

(1) (2) (3) = (2) × $19,500a (4) (5)

Jan. 1, 2015 –– –– $(36,800,000) ––

Dec. 31, 2015 535 $10,432,500

Dec. 31, 2016 600 11,700,000

Dec. 31, 2017 665 12,967,500

Dec. 31, 2018 730 14,235000

21-10

Dec. 31, 2019 795 15,502500

Dec. 31, 2020 860 16,770000

Dec. 31, 2021 925 18,037,500 $7000000

a $55000 – $35,500 = $19,500 cash contribution per prototype.

Cash flows for replacement alternative:

Net Cash Initial Sale of Equip.

Year Units Sold Contributions Investments

(1) (2) (3) = (2) × $29,000b (4) (5)

Jan. 1, 2015 –– –– $(61,700,000) $4,300000

Dec. 31, 2015 535 $15,515,000

Dec. 31, 2016 600 17,400,000

Dec. 31, 2017 665 19,285,000

Dec. 31, 2018 730 21,170000

Dec. 31, 2019 795 23,055000

Dec. 31, 2020 860 24,940000

Dec. 31, 2021 925 26,825,000 $17,000000

b $55000 – $26000 = $29000 cash contribution per prototype.

Payback period calculations for modernizing alternative:

Cumulative Net Initial Investment

Year Cash Inflow Cash Inflow Unrecovered at End of Year

(1) (2) (3) (4)

Jan. 1, 2015 –– –– $36,800,000

Dec. 31, 2015 $10,432,500 $10,432,500 26,367500

Dec. 31, 2016 11,700000 22,132500 14,667500

Dec. 31, 2017 12,967,500 35,100000 1,700000

Dec. 31, 2018 14,235,000

Payback = 3 + ($1,700,000 ÷ $14,235,000)

= 3.12 years

Payback period calculations for replace alternative:

Cumulative Net Initial Investment

Year Cash Inflow Cash Inflow Unrecovered at End of Year

(1) (2) (3) (4)

Jan. 1, 2015 –– –– $57,400,000

21-11

Dec. 31, 2015 $15,515000 $15,515000 41,885000

Dec. 31, 2016 17,400000 32,915000 24,485000

Dec. 31, 2017 19,285000 52,200000 5,200000

Dec. 31, 2018 21,170000

Payback = 3 + ($5,200,000 ÷ $21,170,000)

= 3.25 years