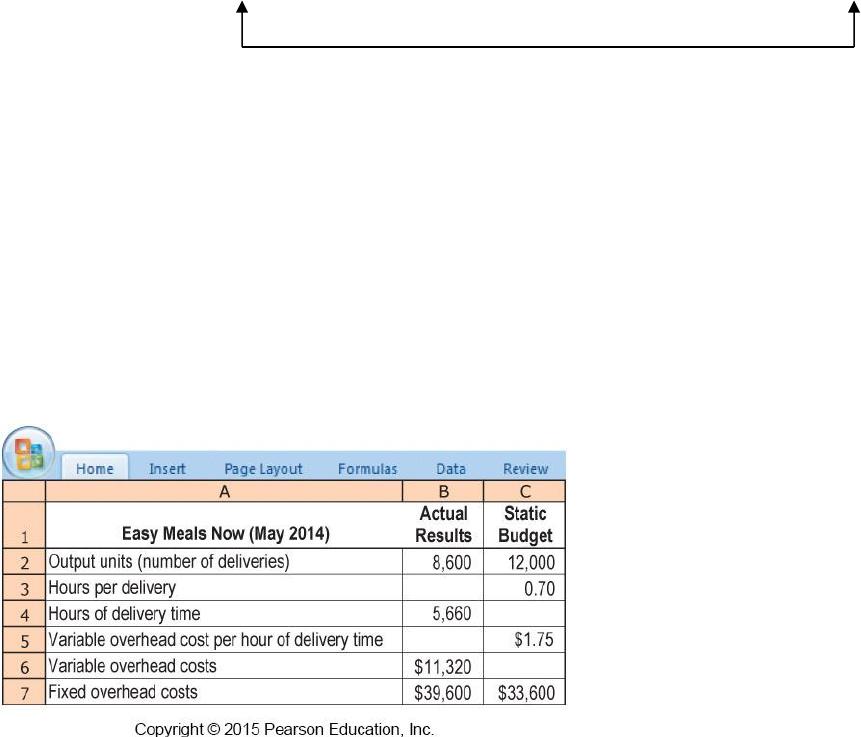

Fixed

MOH

$18,000

$13,400

$13,400

$14,600

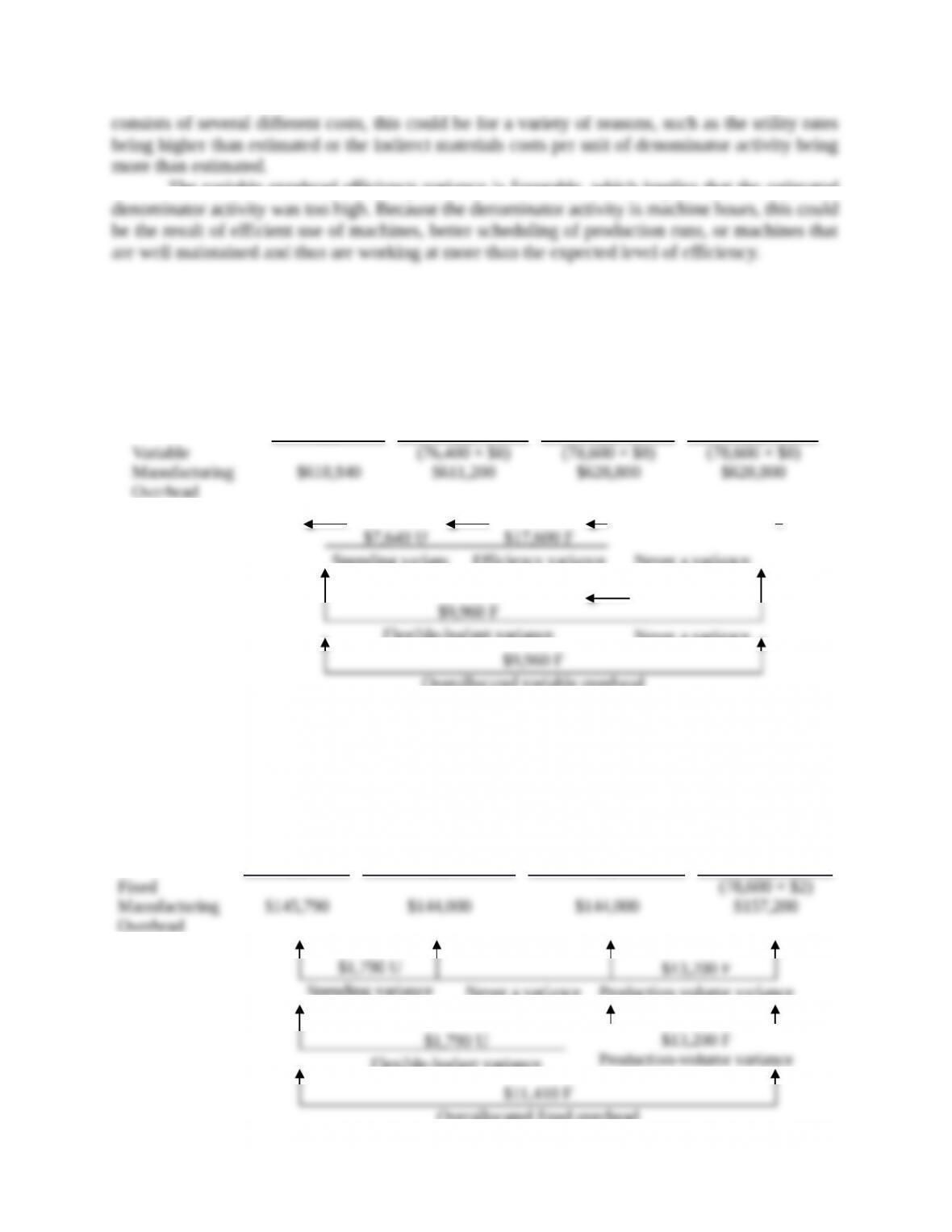

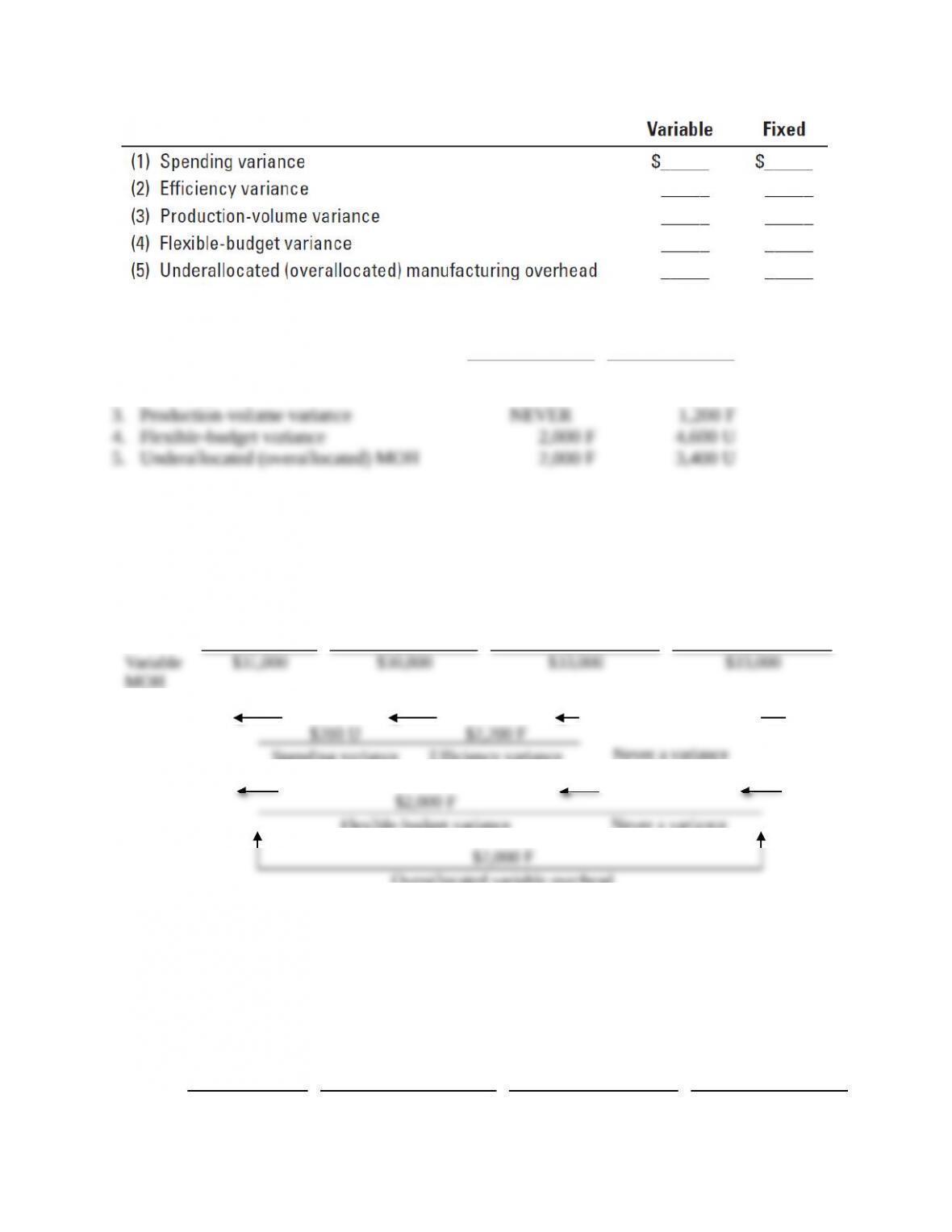

An overview of the four overhead variances is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production–

Volume

Variance

Variable

Overhead

$200 U

$2,200 F

Never a variance

Fixed

Overhead

$4,600 U

Never a variance

$1,200 F

8-22 (20–30 min.) Straightforward 4-variance overhead analysis.

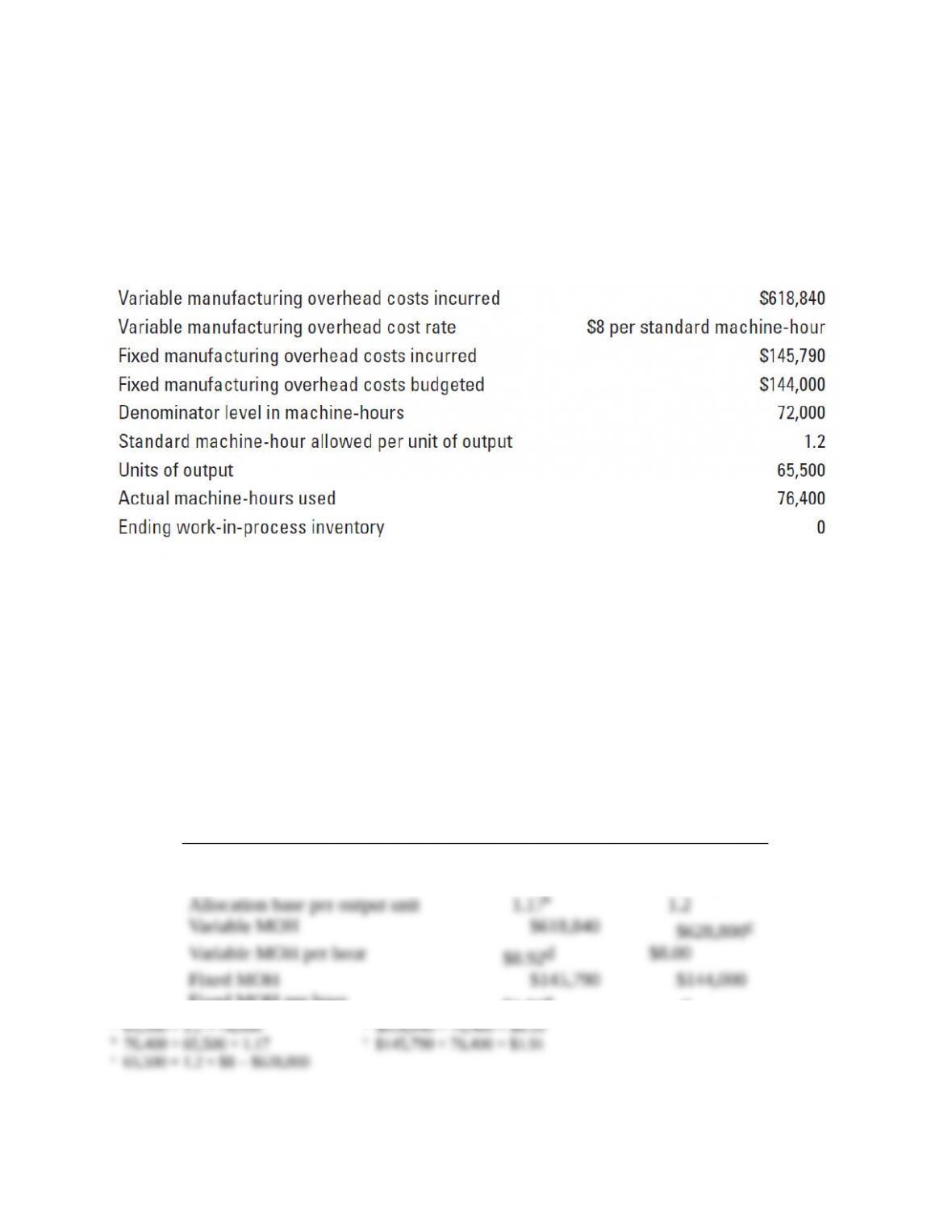

The Lopez Company uses standard costing in its manufacturing plant for auto parts. The standard

cost of a particular auto part, based on a denominator level of 4,000 output units per year, included

6 machine-hours of variable manufacturing overhead at $8 per hour and 6 machine-hours of fixed

manufacturing overhead at $15 per hour. Actual output produced was 4,400 units. Variable

manufacturing overhead incurred was $245,000. Fixed manufacturing overhead incurred was

$373,000. Actual machine-hours were 28,400.

Required:

1. Prepare an analysis of all variable manufacturing overhead and fixed manufacturing overhead

variances, using the 4-variance analysis in Exhibit 8-4 (page 304).

2. Prepare journal entries using the 4-variance analysis.

3. Describe how individual fixed manufacturing overhead items are controlled from day to day.

4. Discuss possible causes of the fixed manufacturing overhead variances.

SOLUTION

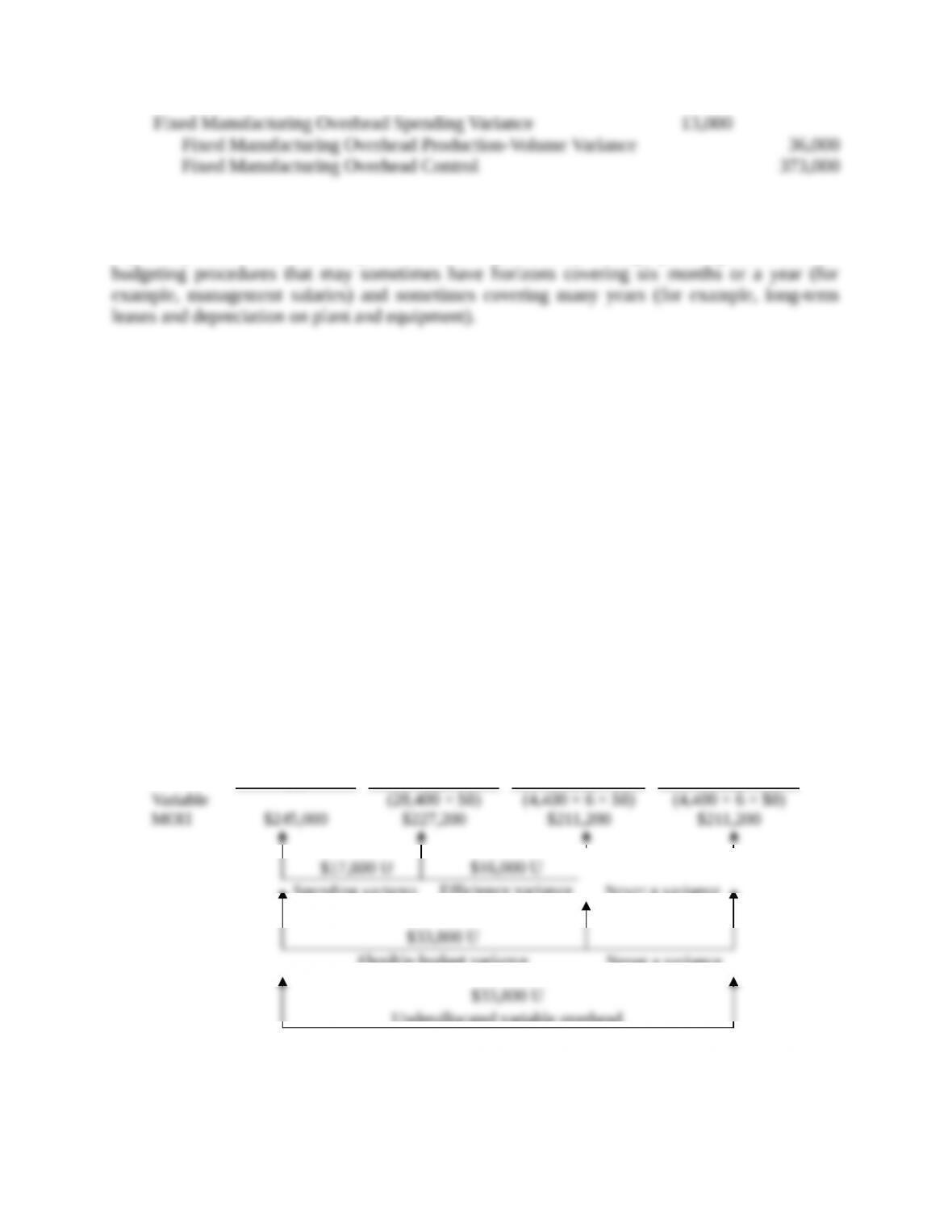

1. The budget for fixed manufacturing overhead is 4,000 units × 6 machine-hours × $15

machine-hours/unit = $360,000.

An overview of the 4-variance analysis is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production–

Volume Variance

$4,600 U

Spending variance

Never a variance

$1,200 F

Production-volume variance

$4,600 U

Flexible-budget variance

$1,200 F

Production-volume variance

$3,400 U

Underallocated fixed overhead

(Total fixed overhead variance)

Variable

Manufacturing

Overhead

$17,800 U

$16,000 U

Never a Variance

Fixed

Manufacturing

Overhead

$13,000 U

Never a Variance

$36,000 F

Solution Exhibit 8-22 has details of these variances.

A detailed comparison of actual and flexible budgeted amounts is:

Actual

Flexible Budget

Output units (auto parts)

4,400

4,400

Allocation base (machine-hours)

28,400

26,400a

Allocation base per output unit

6.45b

6.00

Variable MOH

$245,000

$211,200c

Variable MOH per hour

$8.63d

$8.00

Fixed MOH

$373,000

$360,000e

Fixed MOH per hour

$13.13f

–

a4,400 units × 6.00 machine-hours/unit = 26,400 machine-hours

b28,400 ÷ 4,400 = 6.45 machine-hours per unit

c 4,400 units × 6.00 machine-hours per unit × $8.00 per machine-hour = $211,200

d $245,000 ÷ 28,400 = $8.63

e 4,000 units × 6.00 machine-hours per unit × $15 per machine-hour = $360,000

f $373,000 ÷ 28,400 = $13.13

2. Variable Manufacturing Overhead Control 245,000

Accounts Payable Control and other accounts 245,000

Work-in-Process Control 211,200

Variable Manufacturing Overhead Allocated 211,200

Variable Manufacturing Overhead Allocated 211,200

Variable Manufacturing Overhead Spending Variance 17,800

Variable Manufacturing Overhead Efficiency Variance 16,000

Variable Manufacturing Overhead Control 245,000

Fixed Manufacturing Overhead Control 373,000

Wages Payable Control, Accumulated Depreciation

Control, etc. 373,000

Work-in-Process Control 396,000

Fixed Manufacturing Overhead Allocated 396,000

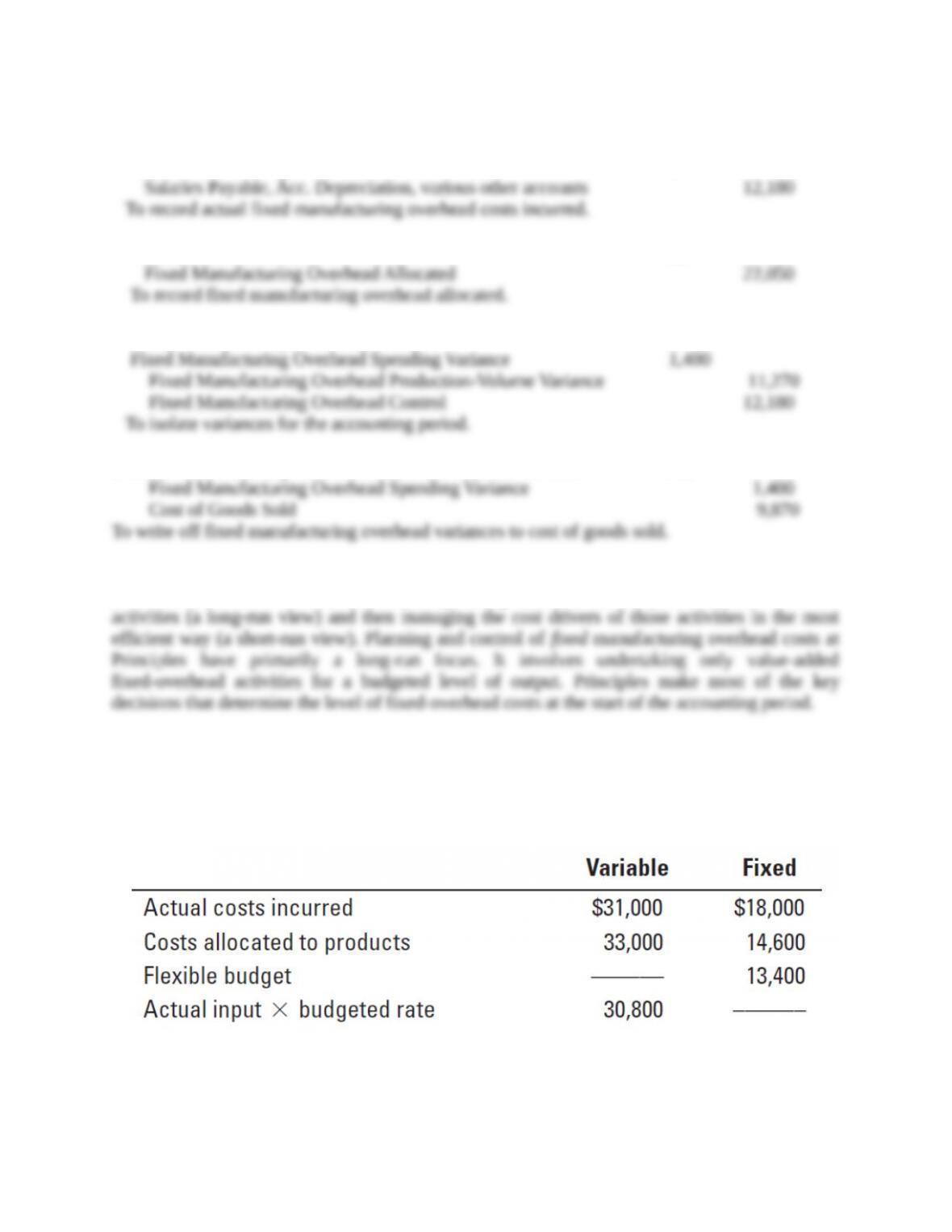

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

Fixed

MOH

$373,000

(4,000 × 6 × $15)

$360,000

(4,000 × 6 × $15)

$360,000

(4,400 × 6 × $15)

$396,000

$13,000 U

Spending variance

Never a variance

$36,000 F

Production-volume

variance

$13,000 U

Flexible-budget variance

$36,000 F

Production-volume

variance

$23,000 F

Overallocated fixed overhead

(Total fixed overhead variance)