1) In markets with little or no competition, the key factor affecting price is the cost of

production to the company.

2) One of the steps in planning is evaluating the performance and taking corrective

measures.

3) The accounting for 3-variance analysis is simpler than the 4-variance analysis, but

some

information is lost because the variable and fixed overhead spending variances are

combined

into a single total overhead spending variance.

4) For critical items such as product defects, a small variance may prompt investigation.

5) Markups tend to be higher in more competitive markets.

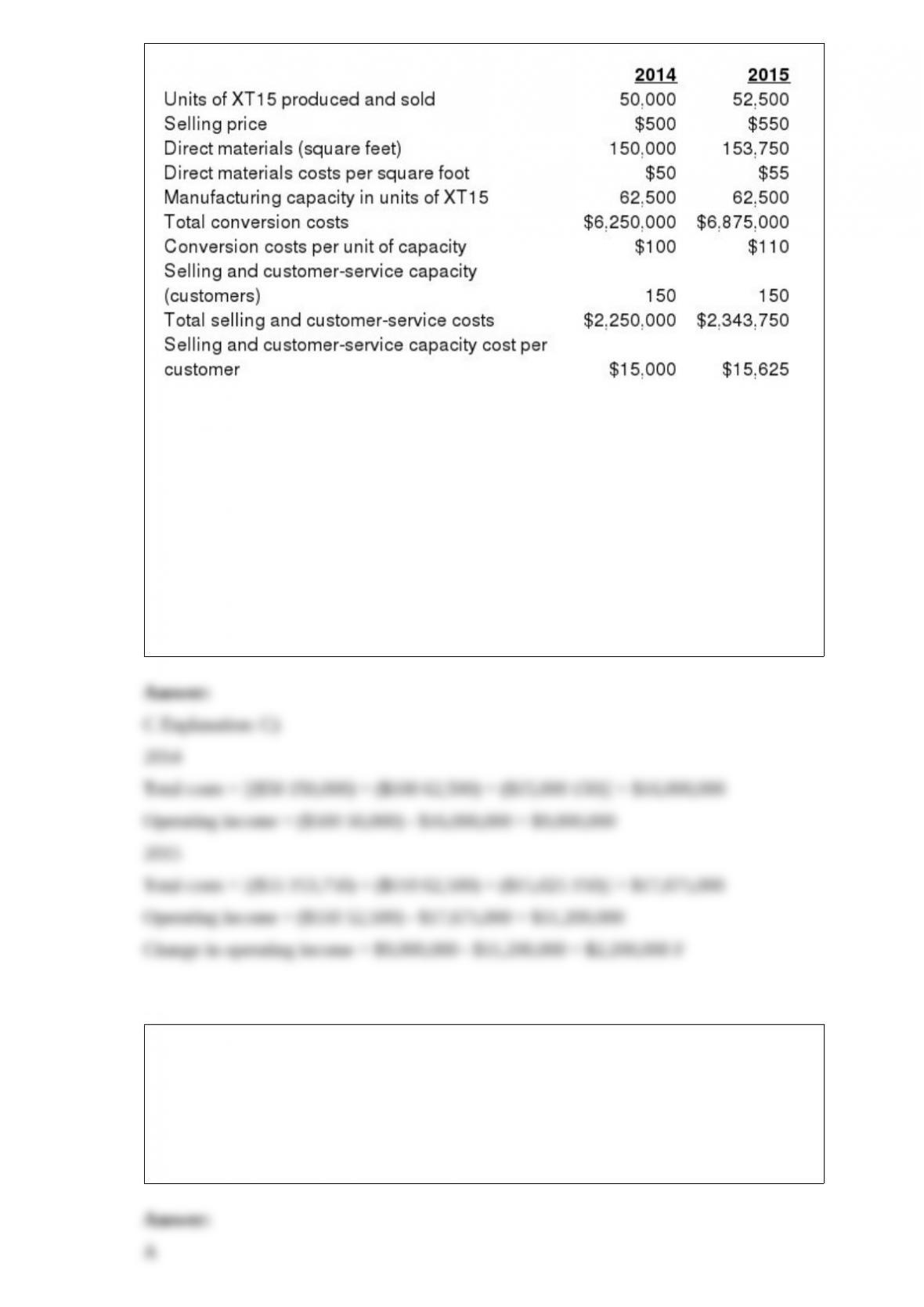

6) Following a strategy of product differentiation, Arseniq Company makes a high-end

Appliance, XT15. Arseniq presents the following data for the years 2014 and 2015:

Arseniq produces no defective units but it wants to reduce direct materials usage per

unit of XT15. Manufacturing conversion costs in each year depend on production

capacity defined in terms of XT15 units that can be produced. Selling and

customer-service costs depend on the number of customers that the customer and

service functions are designed to support. Arseniq had 140 customers in 2014 and 145

customers in 2015.

What is the change in operating income from 2014 to 2015?

A) $2,200,000 U

B) $3,875,000 F

C) $2,200,000 F

D) $3,875,000 U

7) A limitation of using past performance as a basis for judging actual results is that

________.

A) future conditions can be different from the past

B) any undervaluation of profits in the past period is likely to continue

C) any subsequent change in accounting treatment will distort performance evaluation

D) they tend to distort results when current and past conditions are similar

8) The actual indirect-cost rate is calculated by ________.

A) dividing actual total indirect costs by the actual total quantity of the cost-allocation

base

B) multiplying actual total indirect costs by the actual total quantity of the

cost-allocation base

C) dividing the actual total quantity of the cost allocation base by actual total indirect

costs

D) multiplying the actual total quantity of the cost allocation base by actual total

indirect costs

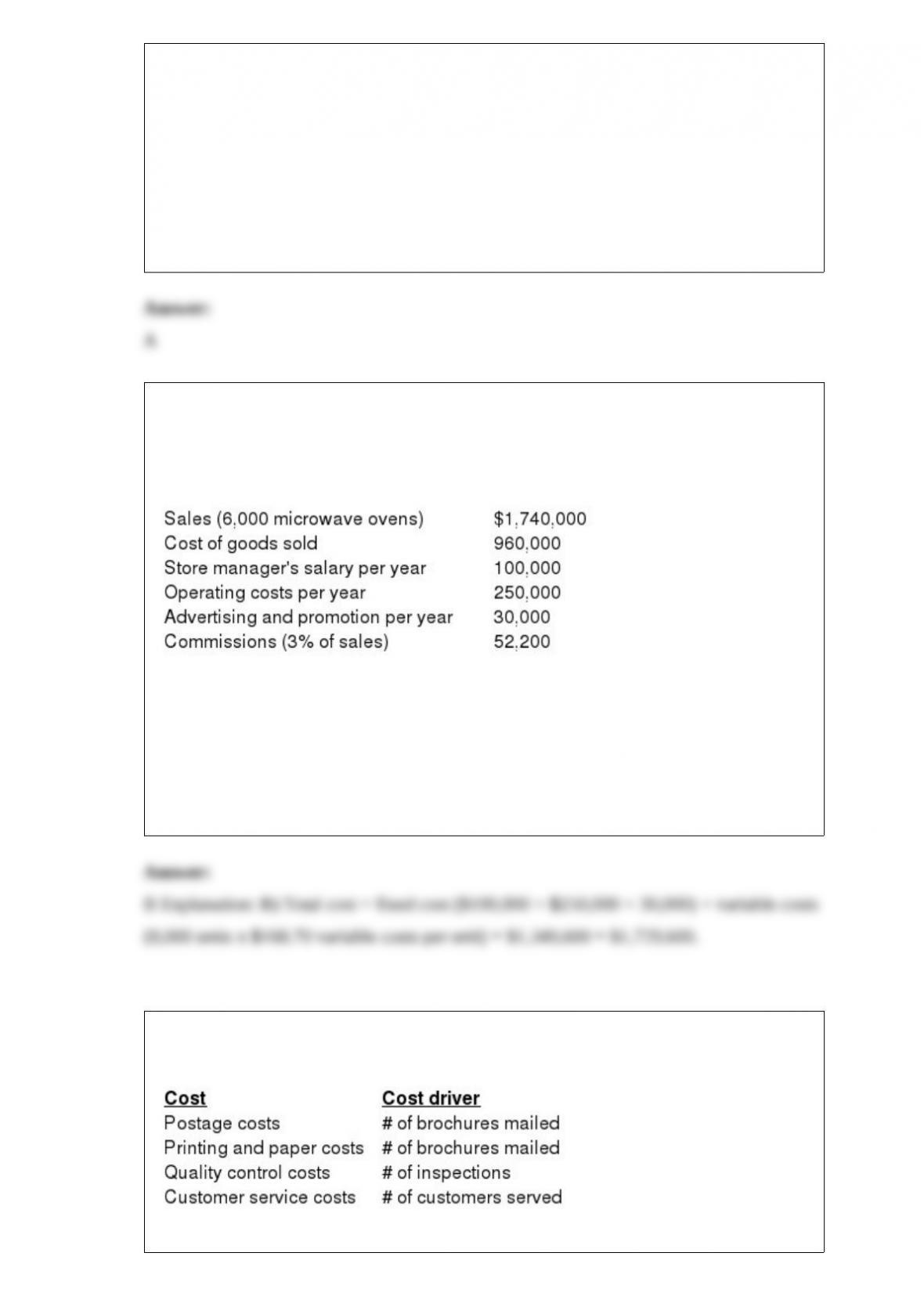

9) Genend’s Good Value Appliance Store is a small company that has hired you to

perform some management advisory services. The following information pertains to

2015 operations.

What are the estimated total costs if Genend’s store expects to sell 8,000 units next

year?

A) $812,117

B) $1,729,600

C) $1,952,200

D) $380,450

10) How many separate cost pools should be formed given the following information?

A) 1 cost pool

B) 2 cost pools

C) 3 cost pools

D) 4 cost pools

11) The Allianz Company produces a specialty wood furniture product, and has the

following information available concerning its inventory items:

Relevant ordering costs per purchase order$450

Relevant carrying costs per year for each package:

Required annual return on investment15%

Required other costs per year$4

Annual demand is 30,000 packages per year. The purchase price per package is $48.

Assuming each order was made at the economic order quantity amount, what is the cost

of placing an order?

A) $322 per order

B) $200 per order

C) $231 per order

D) $417 per order

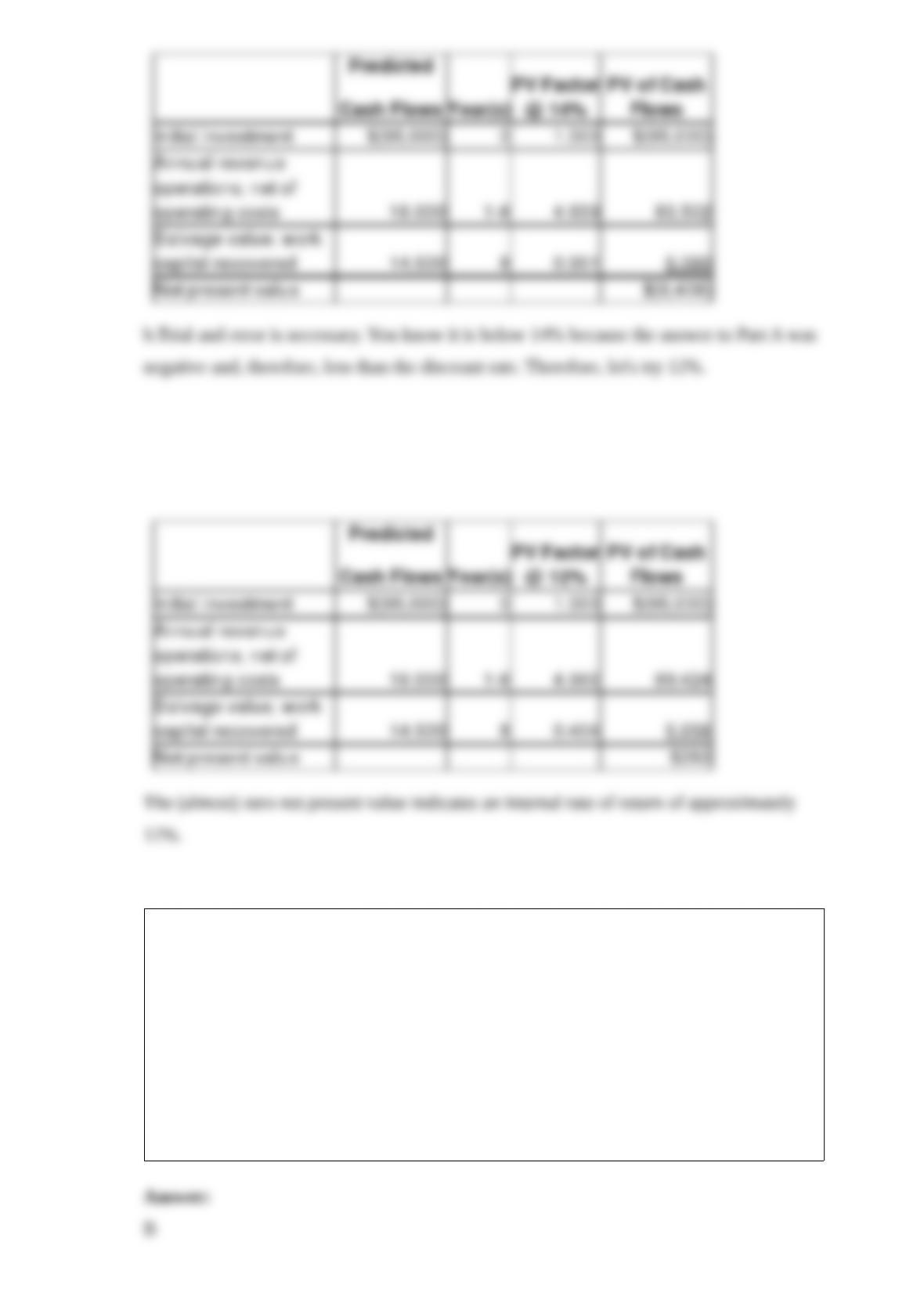

12) Network Service Center is considering purchasing a new computer network for

$82,000. It will require additional working capital of $13,000. Its anticipated eight-year

life will generate additional client revenue of $33,000 annually with operating costs,

excluding depreciation, of $15,000. At the end of eight years, it will have a salvage

value of $9,500 and return $5,000 in working capital. Taxes are not considered.

Required:

a.If the company has a required rate of return of 14%, what is the net present value of

the proposed investment?

b.What is the internal rate of return?

13) The variable overhead efficiency variance measures the difference between the

________, multiplied by the budgeted variable overhead cost per unit of the

cost-allocation base.

A) budgeted quantity of the cost-allocation base used and the budgeted quantity of the

cost-allocation base that should have been used to produce the actual output

B) actual quantity of the cost-allocation base used and the budgeted quantity of the

cost-allocation base that should have been used to produce the actual output

C) actual cost incurred and the budgeted quantity of the cost-allocation base that should

have been used to produce the actual output

D) budgeted cost and the actual cost used to produce the actual output

14) In a long-run, it is worthwhile to sell a product only if the selling price exceeds

________.

A) direct costs of the product

B) manufacturing costs of the product

C) fixed cost of the product

D) full cost of the product and a markup

15) To guide cost allocation decisions, the cause-and-effect criterion ________.

A) is used less frequently than the other criteria

B) is the primary criterion used in activity-based costing

C) considers fairness as a matter of judgment rather than an operational criterion

D) advocates allocating costs in proportion to the cost object’s ability to bear costs

allocated to it

16) What factor most often drives joint cost allocation?

A) performance evaluation

B) manager compensation

C) selling prices

D) simplicity of the method

17) Roberto Inc., operates a chain of luxury hotels in the Asia-Pacific region. It charges

$150 for one night stay. However when 90% of the rooms are occupied, Roberto

charges a premium of 20% on room tariff for the remaining rooms. What pricing

method has Roberto Inc. adopted?

A) customer-preference pricing

B) seasonal-load pricing

C) peak-load pricing

D) capacity pricing

18) Match each of the following items with one or more of the denominator-level

capacity concepts by putting the appropriate letter(s) by each item:

a.Theoretical capacity

b.Practical capacity

c.Normal capacity utilization

d.Master-budget capacity utilization

1>Reduces theoretical capacity by considering unavoidable operating interruptions

2>Producing at full efficiency all the time

3>Measures capacity levels in terms of demand

4>

5>Does not allow for plant maintenance

6>Engineering and human resource factors are important when estimating capacity

7>

8>Ideal goal of capacity utilization

9>Takes into account seasonal, cyclical, and trend factors

10>Measures capacity levels in terms of what a plant can supply