1) Budgeted production equals ________.

A) beginning finished goods inventory + budgeted unit sales – targeted ending finished

goods inventory

B) targeted ending finished goods inventory + beginning finished goods inventory –

budgeted unit sales

C) budgeted unit sales + targeted ending finished goods inventory – beginning finished

goods inventory

D) budgeted unit sales + targeted ending finished goods inventory + beginning finished

goods inventory

2) The following information pertains to the January operating budget for Casey

Corporation.

Budgeted sales for January $200,000 and February $100,000.

Collections for sales are 60% in the month of sale and 40% the next month.

Gross margin is 30% of sales.

Administrative costs are $10,000 each month.

Beginning accounts receivable is $20,000.

Beginning inventory is $14,000.

Beginning accounts payable is $65,000. (All from inventory purchases.)

Purchases are paid in full the following month.

Desired ending inventory is 20% of next month’s cost of goods sold (COGS).

At the end of January, budgeted accounts receivable is ________.

A) $40,000

B) $80,000

C) $120,000

D) $160,000

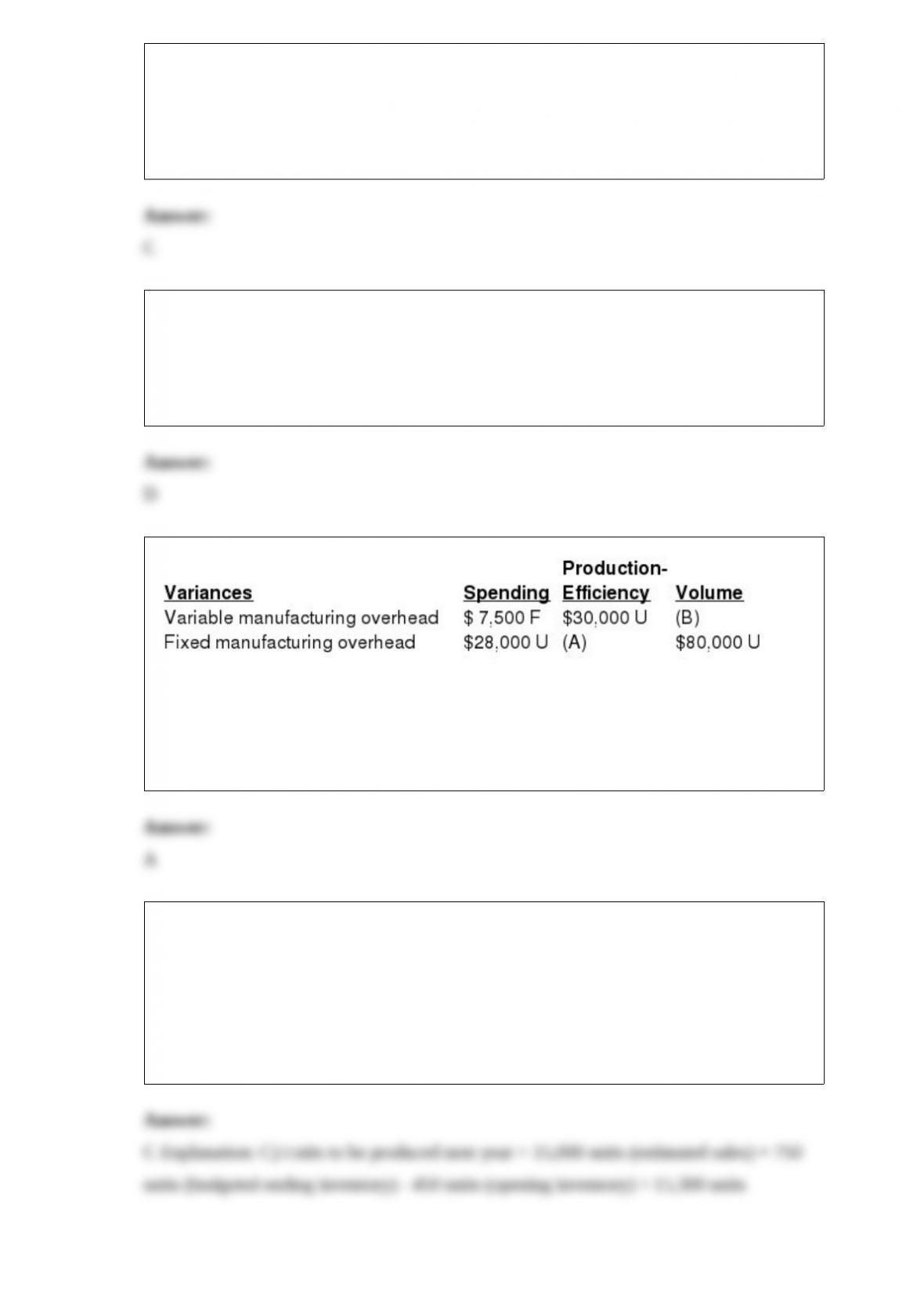

3) The fixed overhead cost variance can be further subdivided into the ________.

A) price variance and the efficiency variance

B) spending variance and flexible-budget variance

C) production-volume variance and the efficiency variance

D) flexible-budget variance and the production-volume variance

4) During February the Lungren Manufacturing Company’s costing system reported

several variances that the production manager was surprised to see. Most of the

company’s monthly variances are under $125, even though they may be either favorable

or unfavorable. The following information is for the manufacture of garden gates, its

only product:

1.Direct materials price variance, $800 unfavorable.

2.Direct materials efficiency variance, $1,800 favorable.

3.Direct manufacturing labor price variance, $4,000 favorable.

4.Direct manufacturing labor efficiency variance, $600 unfavorable.

Required:

a.Provide the manager with some ideas as to what may have caused the price variances.

b.What may have caused the efficiency variances?

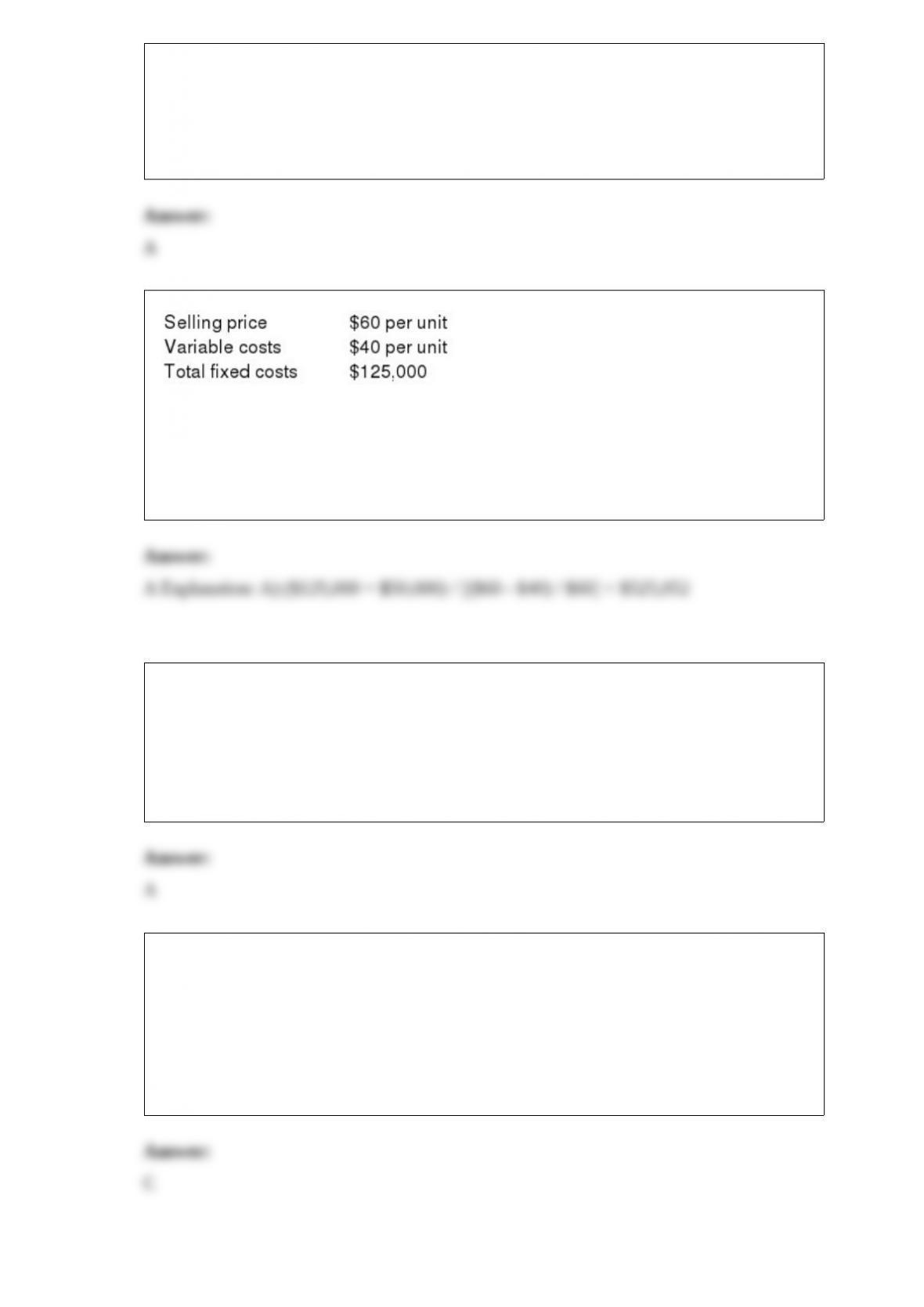

5) The margin of safety is the difference between ________.

A) budgeted expenses and breakeven expenses

B) budgeted revenues and breakeven revenues

C) actual operating income and budgeted operating income

D) actual sales margin and budgeted sales margin

6) Job costing information is used ________.

A) to determine target customers

B) to calculate the percentage of completion

C) for internal financial reporting

D) to enhance public relations

7) Which of the following is a manufacturing overhead cost?

A) cost of conversion of direct materials to finished goods

B) labor cost that can be traced to individual products

C) cost of materials that can be traced to individual products

D) overtime premiums paid to plant workers

8) The above table is a ________.

A) 4-variance analysis

B) 3-variance analysis

C) 2-variance analysis

D) 1-variance analysis

9) For next year, Roberto, Inc., has budgeted sales of 15,000 units, targeted ending

finished goods inventory of 750 units, and beginning finished goods inventory of 450

units. All other inventories are zero. How many units should be produced next year?

A) 14,700 units

B) 15,000 units

C) 15,300 units

D) 16,200 units

10) Which of the following is an opportunity cost?

A) lost sales

B) cost of production

C) marginal cost

D) cost of sales

11) If targeted operating income is $50,000, then targeted sales revenue is ________.

A) $525,052

B) $533,333

C) $498,133

D) $517,072

12) The scenario that resources should be spent if the expected benefits to the company

exceed the expected costs describes ________.

A) cost-benefit approach

B) behavioral and technical considerations

C) balanced scorecard

D) different costs for different purposes

13) The approaches and activities of managers in short-run and long-run planning and

control decisions that increase value for customers and lower costs of products and

services are known as ________.

A) value chain management

B) enterprise resource planning

C) cost management

D) customer value management