1) A revenue driver is a variable, such as volume, that causally affects revenues.

2) Machine depreciation can be a cost-driver for a manufacturing company under ABC

system.

3) Fixed overhead has no production-volume variance.

4) The dual cost-allocation method classifies costs into two pools, a budgeted cost pool

and an actual cost pool.

5) The use of activity-based cost drivers gives rise to zero-based budgeting.

6) The constant gross-margin percentage NRV method is the only method of allocating

joint costs under which products may receive negative allocations.

7) The constant gross-margin percentage NRV method is the only method whereby

products can receive negative allocations.

8) Manufacturing lead time is the sum of waiting time and manufacturing time for an

order.

9) Direct tracing of costs reduces the amount of costs classified as indirect costs.

10) Engineering and human resource factors are both important when estimating

theoretical or practical capacity.

11) The productivity component measures the amount by which operating income

increases by using inputs efficiently to lower costs.

12) Under variable costing, lease charges paid on the factory building is an

inventoriable cost.

13) The two most common methods of costing inventories in manufacturing companies

are variable costing and absorption costing.

14) Acquisition costs of direct materials include freight-in charges, sales taxes, and

custom duties.

15) Net initial investment in the project includes the acquisition of assets and any

associated additions to working capital, minus the after-tax cash flow from the disposal

of existing assets.

16) Product costs used for external reporting generally include ________.

A) manufacturing costs only

B) design costs plus manufacturing costs

C) all costs incurred along the value chain

D) research and development costs along with production costs

17) Which of the following capacity levels should a company choose, from a long-run

product costing perspective, to allocate budgeted fixed manufacturing costs to

products?

A) master-budget capacity utilization to highlight unused capacity

B) normal capacity utilization for benchmarking purposes

C) practical capacity for pricing decisions

D) theoretical capacity for performance evaluation

18) The reason to have a post-investment audit is ________.

A) they encourage mid-level managers to make overly optimistic estimates during the

early stages of the capital budgeting process

B) they help alert senior management to problems in the implementation of projects

C) they analyze by calculating contribution-margin

D) they help in calculating present value

19) Under absorption costing, if a manager’s bonus is tied to operating income, then

increasing inventory levels compared to last year would result in ________.

A) increasing the manager’s bonus

B) decreasing the manager’s bonus

C) not affecting the manager’s bonus

D) being unable to determine the manager’s bonus using only the above information

20) Strykerz Corp expects to spend $800,000 in 2015 in appraisal costs if it does not

change its incoming materials inspection method. If it decides to implement a new

receiving method, it will save $60,000 in fixed appraisal costs and variable costs of

$0.50 per unit of finished product. The new method involves $140,000 in training costs

and an additional $150,000 in annual equipment rental.

Internal failure costs average $160 per failed unit of finished goods. During 2014, 5%

of all completed items had to be reworked. External failure costs average $400 per

failed unit. The company’s average external failures are 1% of units sold. The company

carries no ending inventories, because all jobs are on a per order basis and a just-in-time

inventory ordering method is used.

How much will external failure costs change assuming 800,000 units of materials are

received and that product failures with customers are cut in half with the new receiving

method?

A) $20,000 increase

B) $400,000 decrease

C) $640,000 decrease

D) $800,000 decrease

21) Using the high-low method, the estimate of the variable component of inspection

cost per unit produced is closest to:

A) $10.57

B) $0.11

C) $17.89

D) $9.33

22) In a normal costing system, the Manufacturing Overhead Control account

________.

A) is increased by allocated manufacturing overhead

B) is credited with amounts transferred to Work-in-Process

C) is decreased by allocated manufacturing overhead

D) is debited with actual overhead costs

23) Charlie Chairs Inc., manufactures plastic moldings for car seats. Its costing system

utilizes two cost categories, direct materials and conversion costs. Each product must

pass through Department A and Department B. Direct materials are added at the

beginning of production. Conversion costs are allocated evenly throughout production.

Data for Department A for February 2015 are:

Costs for Department A for February 2015 are:

How many units were completed and transferred out of Department A during February?

A) 300 units

B) 800 units

C) 900 units

D) 1,000 units

24) Linking rewards to performance ________.

A) helps to motivate managers

B) allows companies to charge premium prices

C) should only be based on financial information

D) enhances agency costs

25) Customer response time involves ________.

A) the speed it takes a customer to respond to an advertisement and place an order

B) the speed at which an organization responds to customer requests

C) the speed it takes to develop a new product

D) the speed it takes an organization to develop a Total Quality Management (TQM)

program

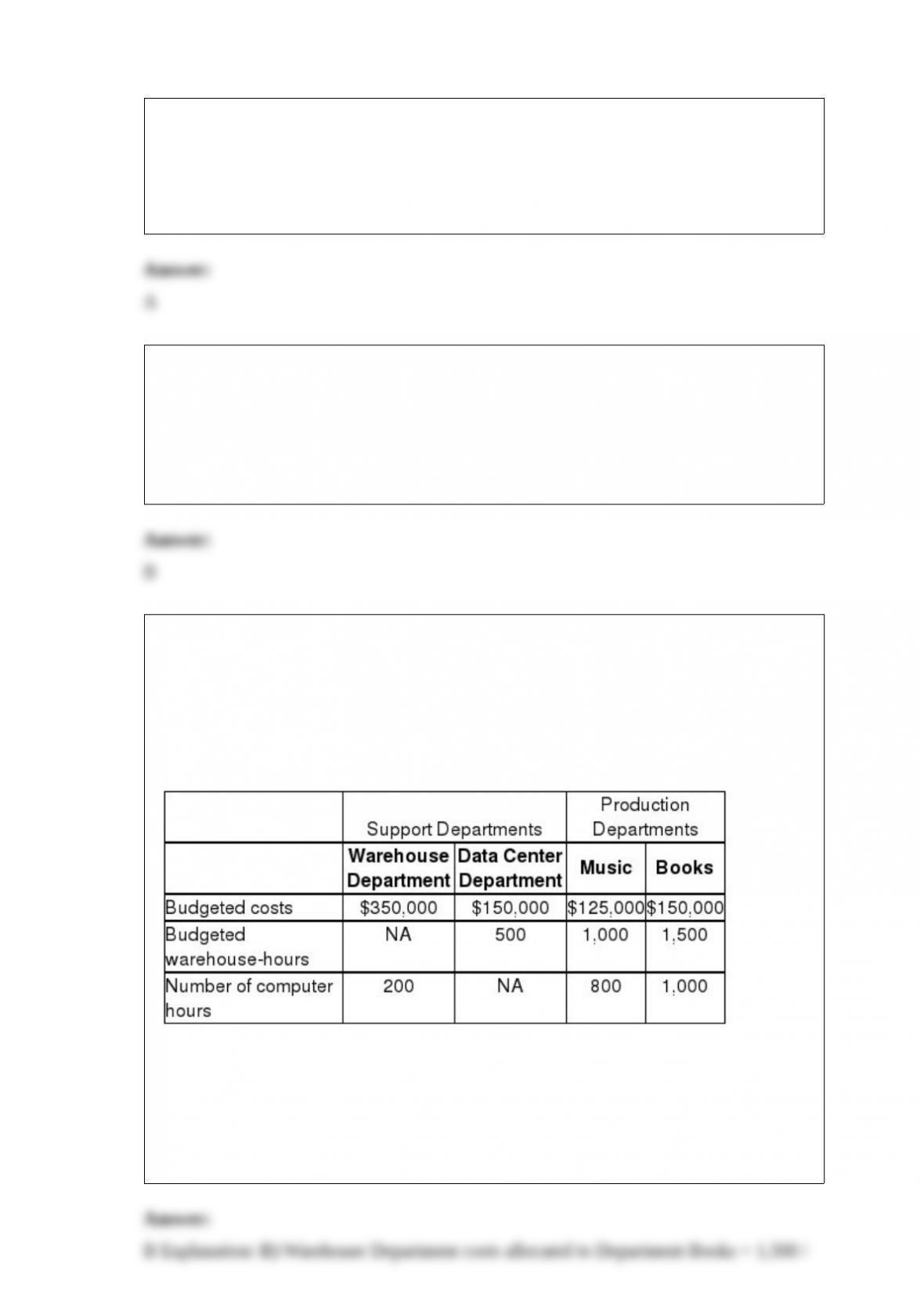

26) Goldfarb’s Book and Music Store has two service departments, Warehouse and Data

Center. Warehouse Department costs of $350,000 are allocated on the basis of budgeted

warehouse-hours. Data Center Department costs of $150,000 are allocated based on the

number of computer log-on hours. The costs of operating departments Music and Books

are $250,000 and $300,000, respectively. Data on budgeted warehouse-hours and

number of computer log-on hours are as follows:

Using the direct method, what amount of Warehouse Department costs will be allocated

to Department Books?

A) $140,000

B) $210,000

C) $150,000

D) $175,000

27) What is throughput costing? What advantages is it purported to have over variable

and absorption costing?

28) How does the capacity level chosen to compute the budgeted fixed overhead cost

rate affect the production-volume variance?

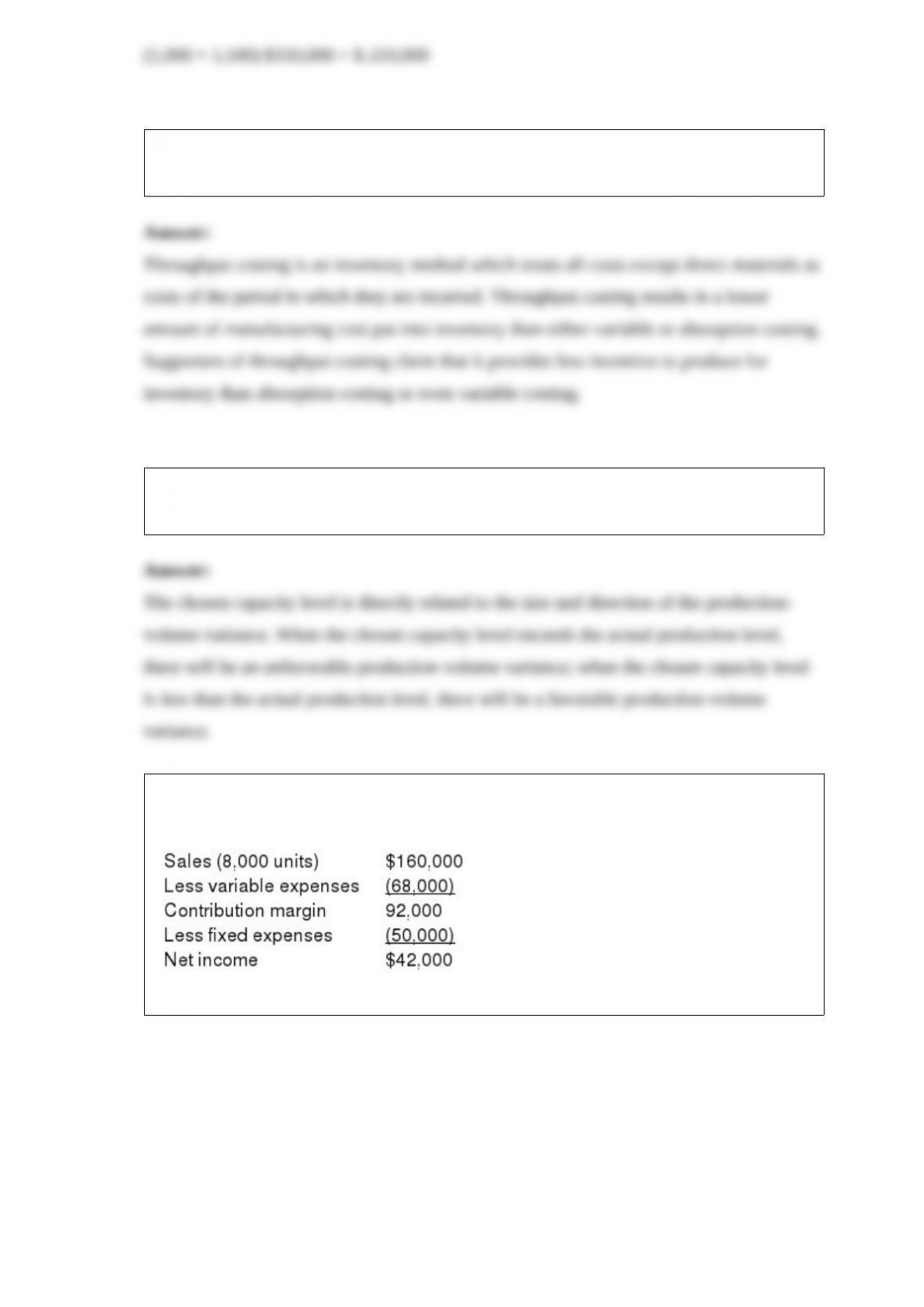

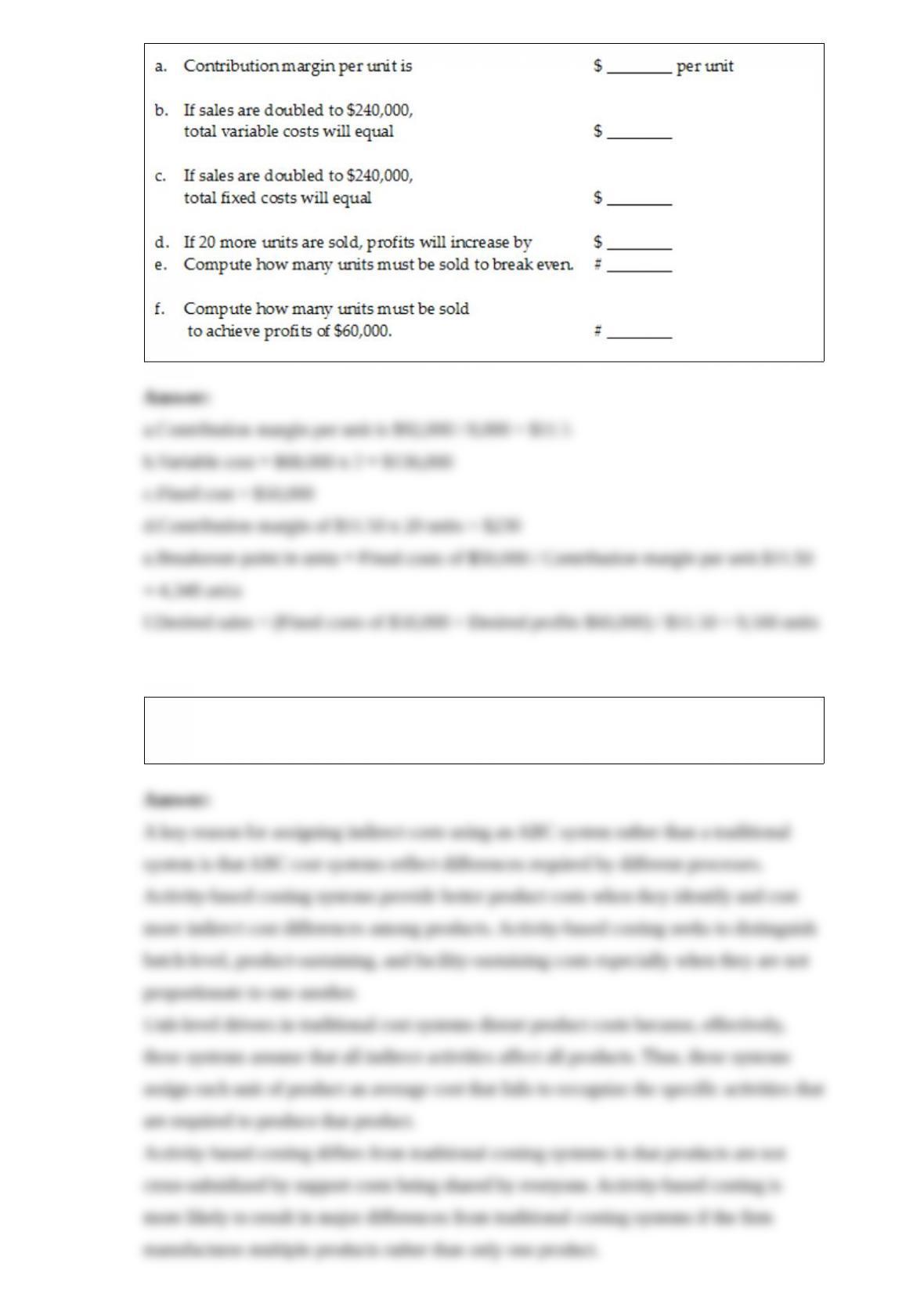

29) Zeta Corp’s most recent income statement is given below.

Required:

30) Explain how activity-based costing systems can provide more accurate product

costs than traditional cost systems.

31) What are the reasons for allocating joint costs to individual products or services?

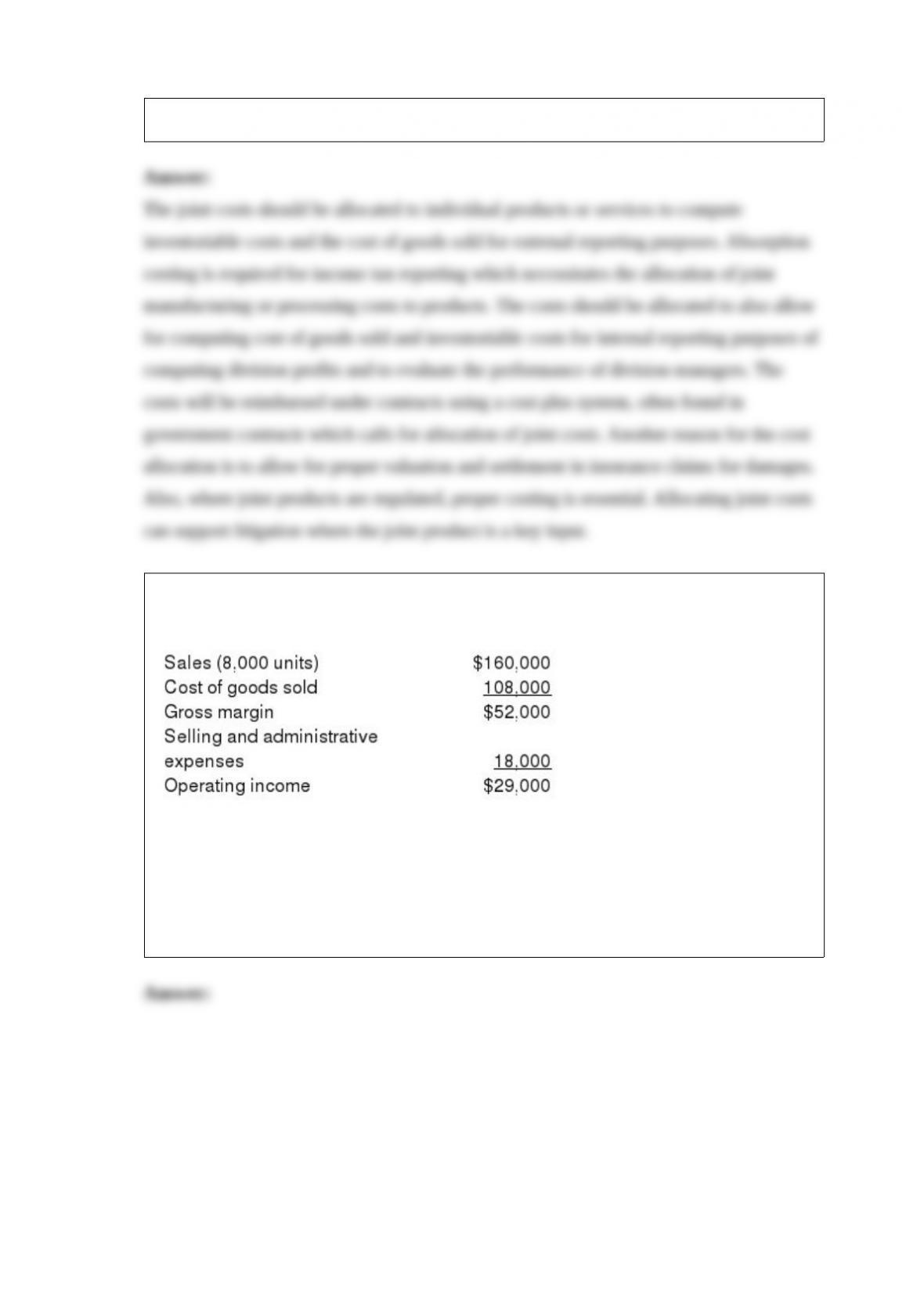

32) Aspen Popular Company prepared the following absorption-costing income

statement for the year ended May 31, 2015.

Additional information follows:

Selling and administrative expenses include $1.50 of variable cost per unit sold. There

was no beginning inventory, and 8,750 units were produced. Variable manufacturing

costs were $11 per unit. Actual fixed costs were equal to budgeted fixed costs

Required:

Prepare a variable-costing income statement for the same period.

33) Discuss the methods used to identify quality problems.

34) Explain how are the fixed manufacturing overhead costs treated under Generally

Accepted Accounting Principles?

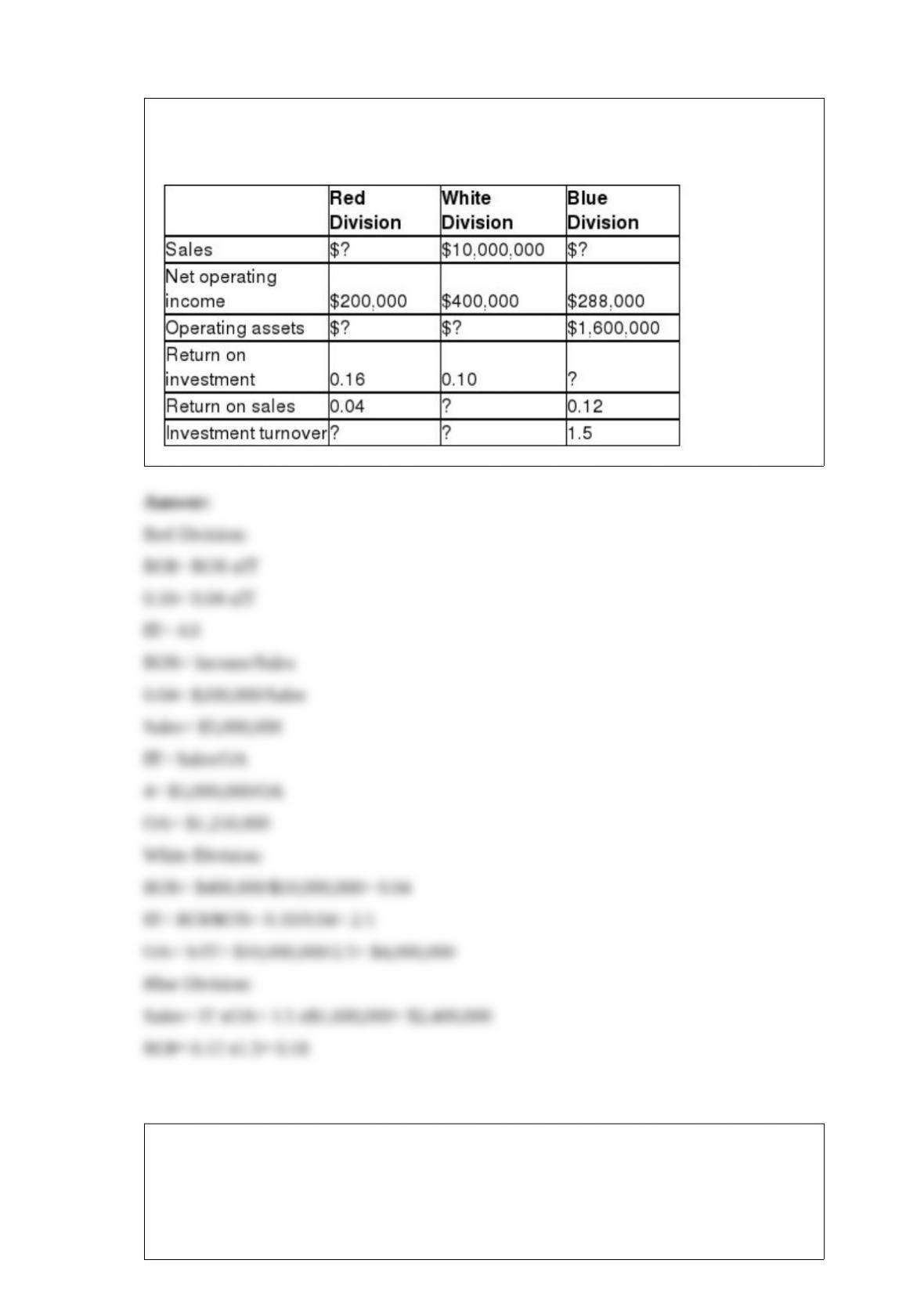

35) Provide the missing data for the following situations:

36) Super Shoes Company manufactures sneakers. The Athletic Division sells its socks

for $18 a pair to outsiders. Sneakers have manufacturing costs of $6.00 each for

variable and $6.00 for fixed. The division’s total fixed manufacturing costs are

$315,000 at the normal volume of 70,000 units.

The European Division has offered to buy 15,000 Sneakers at the full cost of $12. The

Athletic Division has excess capacity and the 15,000 units can be produced without

interfering with the current outside sales of 70,000. The 85,000 volume is within the

division’s relevant operating range.

Explain whether the Athletic Division should accept the offer.