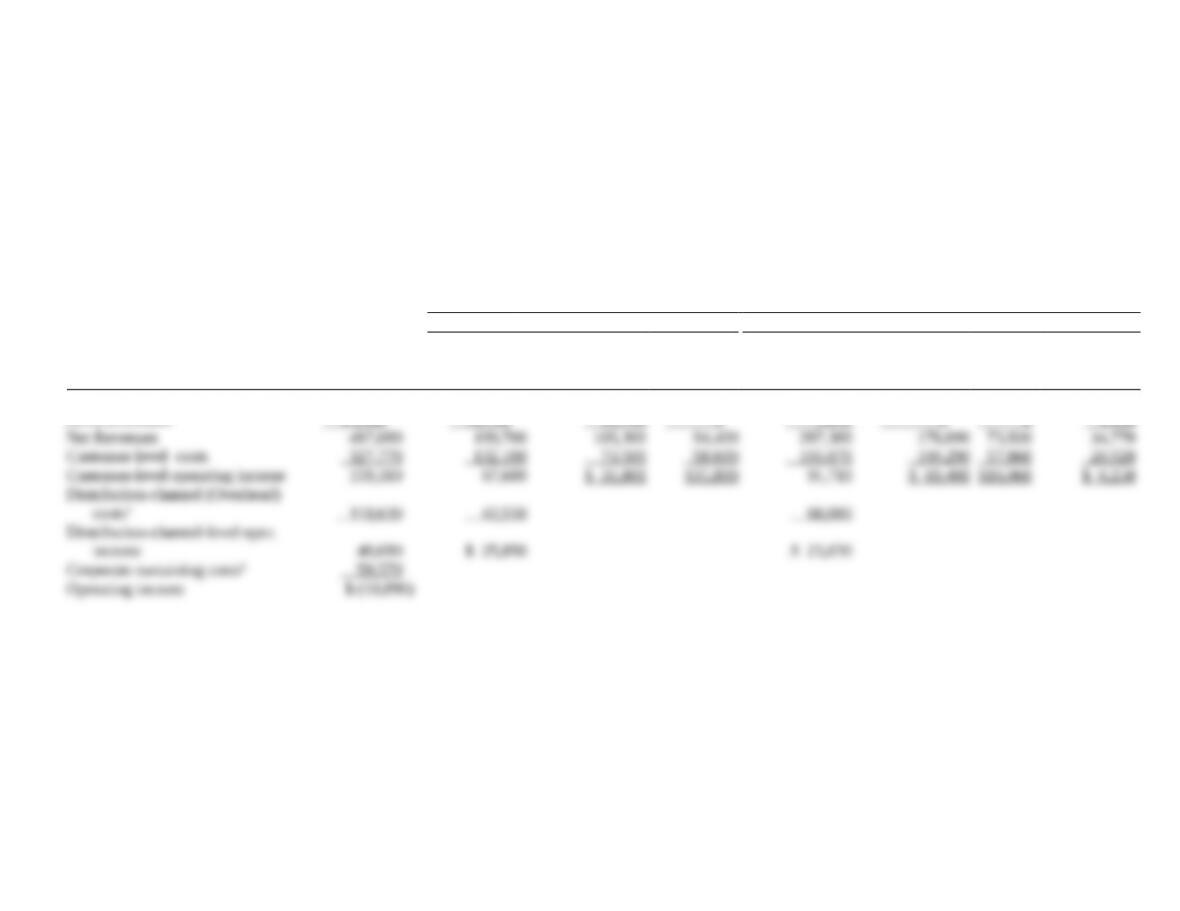

(Dollar amounts in millions)

Oil & Gas

Upstream

Oil & Gas

Downstream

Chemical

Products

Copper

Mining

Total

Revenues

$8,000.00

$16,000.00

$4,800.00

$3,200.00

$32,000

Operating Costs

3,000.00

15,000.00

3,800.00

3,500.00

25,300

Operating Income

5,000.00

1,000.00

1,000.00

(300.00)

6,700

Cost Pool 1 Allocation ((1)

$2,000)

1,120.00

480.00

240.00

160.00

2,000

Cost Pool 2 Allocation ((2)

$800)

200.00

400.00

120.00

80.00

800

Cost Pool 3 Allocation ((3)

$203)

145.00

29.00

29.00

0.00

203

Cost Pool 4 Allocation ((4)

$225)

67.50

9

0.00

45.00

22.50

225

Division Income

$3,467.50

$ 1.00

$ 566.00

$ (562.50)

$ 3,472

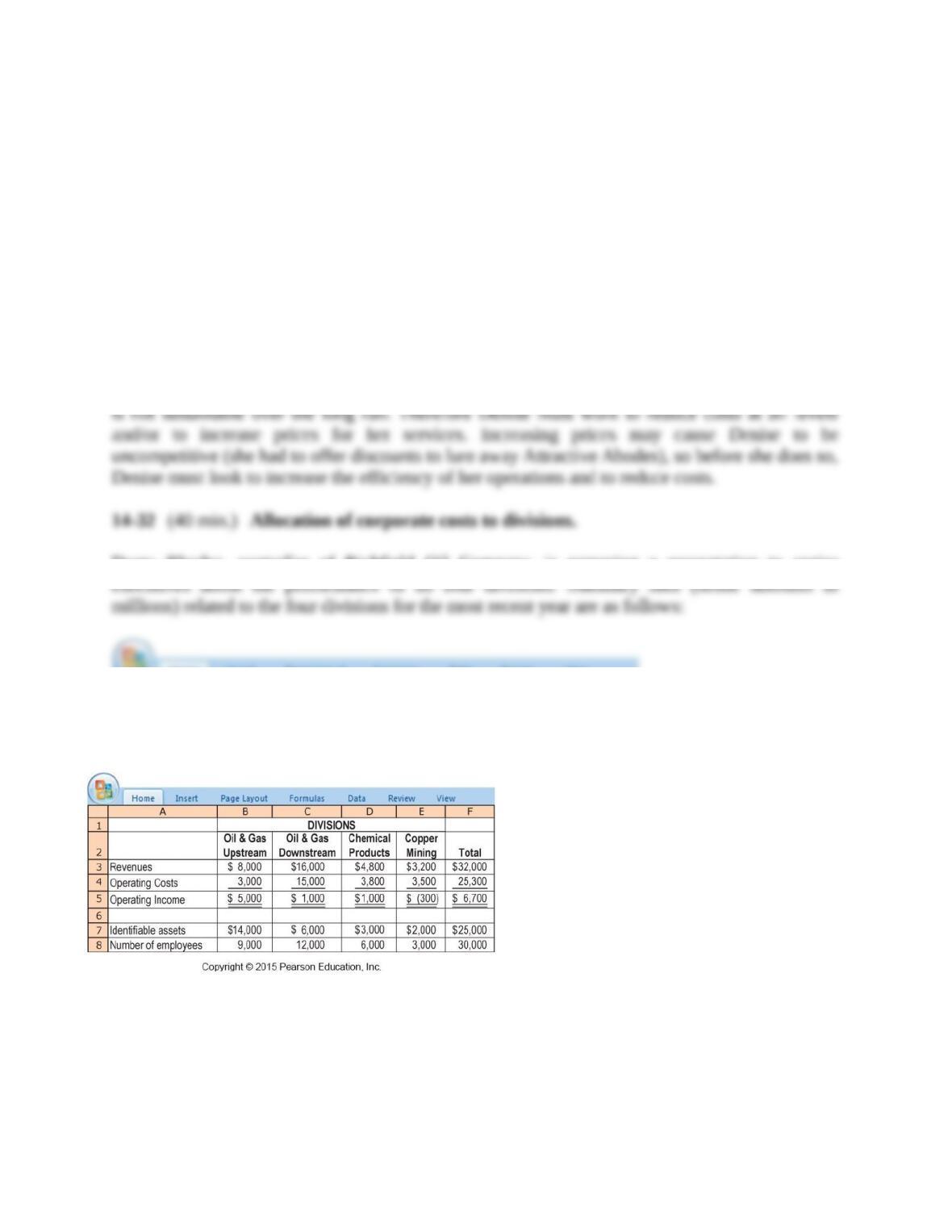

4. The table below compares the reported income of each division under the original revenue-

based allocation scheme and the new four-pool-based allocation scheme. Oil & Gas Upstream

seems 17% less profitable than before ($3,467.5

$4,193 = 83%) and may resist the new

allocation, but each of the other divisions seem more profitable (or less loss-making) than before,

and they will probably welcome it. In this setting, corporate costs are relatively large [about 13%

($3,228 ÷ $25,300) of total operating costs], and division incomes are sensitive to the corporate

cost allocation method.

(Dollar amounts in millions)

Oil & Gas

Upstream

Oil & Gas

Downstream

Chemical

Products

Copper

Mining

Total

Operating Income

(before corp. cost allocation)

$5,000.00

$1,000.00

$1,000.00

$(300.00)

$6,700

Division income under revenue-based

allocation of corporate costs

$4,193.00

$ (614.00)

$ 516.00

$(623.00)

$3,472

Division income under four-cost-pool

allocation of corporate costs

$3,467.50

$ 1.00

$ 566.00

$(562.50)

$3,472

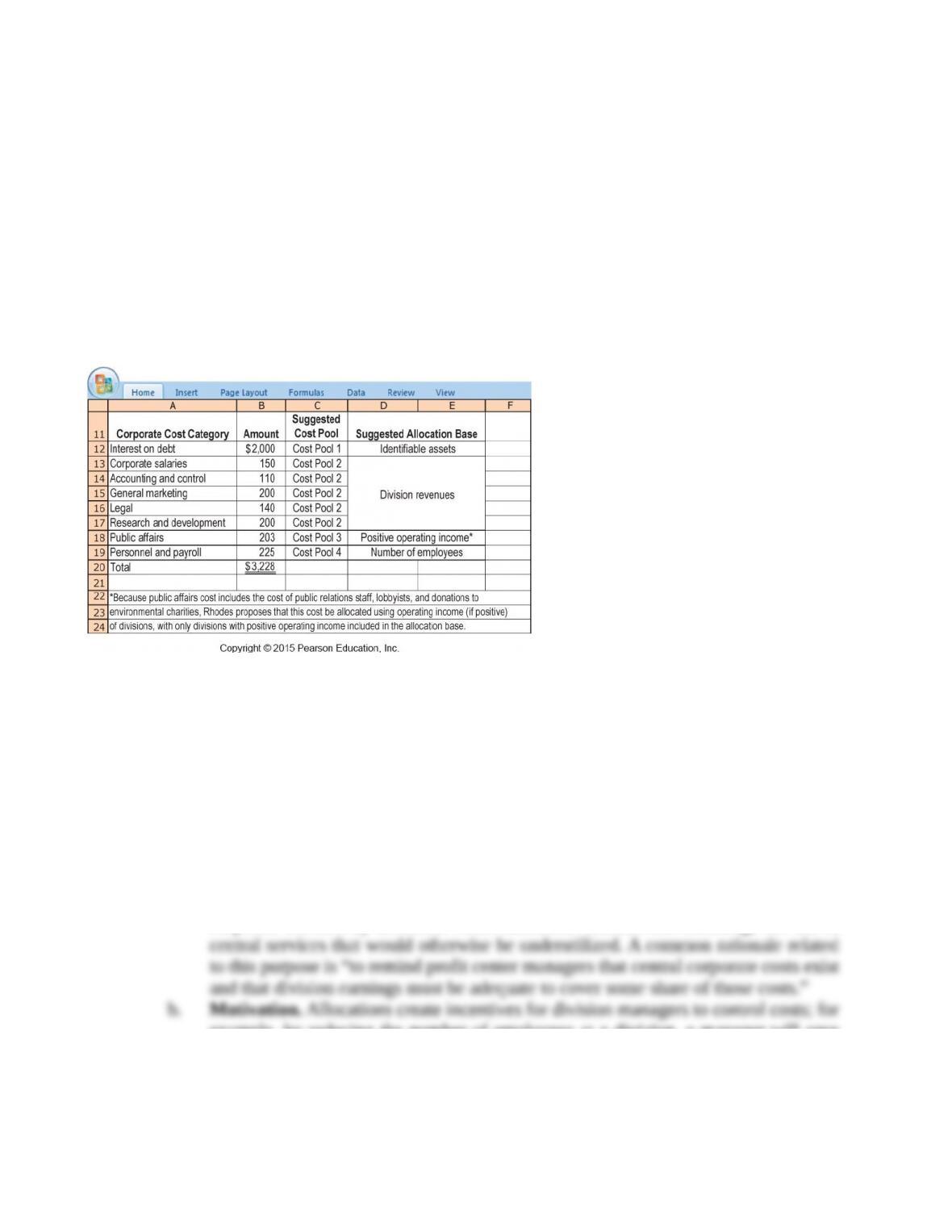

Strengths of Rhodes’ proposal relative to existing single-cost pool method:

a. Better able to capture cause-and-effect relationships. Interest on debt is more likely caused

by the financing of assets than by revenues. Personnel and payroll costs are more likely

caused by the number of employees than by revenues.

b. Relatively simple. No extra information need be collected beyond what is already

available. (Some students will list the extra costs of Rhodes’ proposal as a weakness.

However, for a company with $30 billion in revenues, those extra costs are minimal.)

Weaknesses of Rhodes’ proposal relative to existing single–cost pool method:

a. May promote dysfunctional decision making. May encourage division managers to lease

or rent assets rather than to purchase assets, even where it is economical for Richfield Oil

to purchase them. This off-balance sheet financing will reduce the “identifiable assets” of

the division and thus will reduce the interest on debt costs allocated to the division.

(Richfield Oil could counteract this problem by incorporating leased and rented assets in

the “identifiable assets” base.)

Total

2,504,600

839,900

1,755,500

5,100,000

Operating income

$3,895,400

$ 460,100

$4,394,500

$ 8,750,000

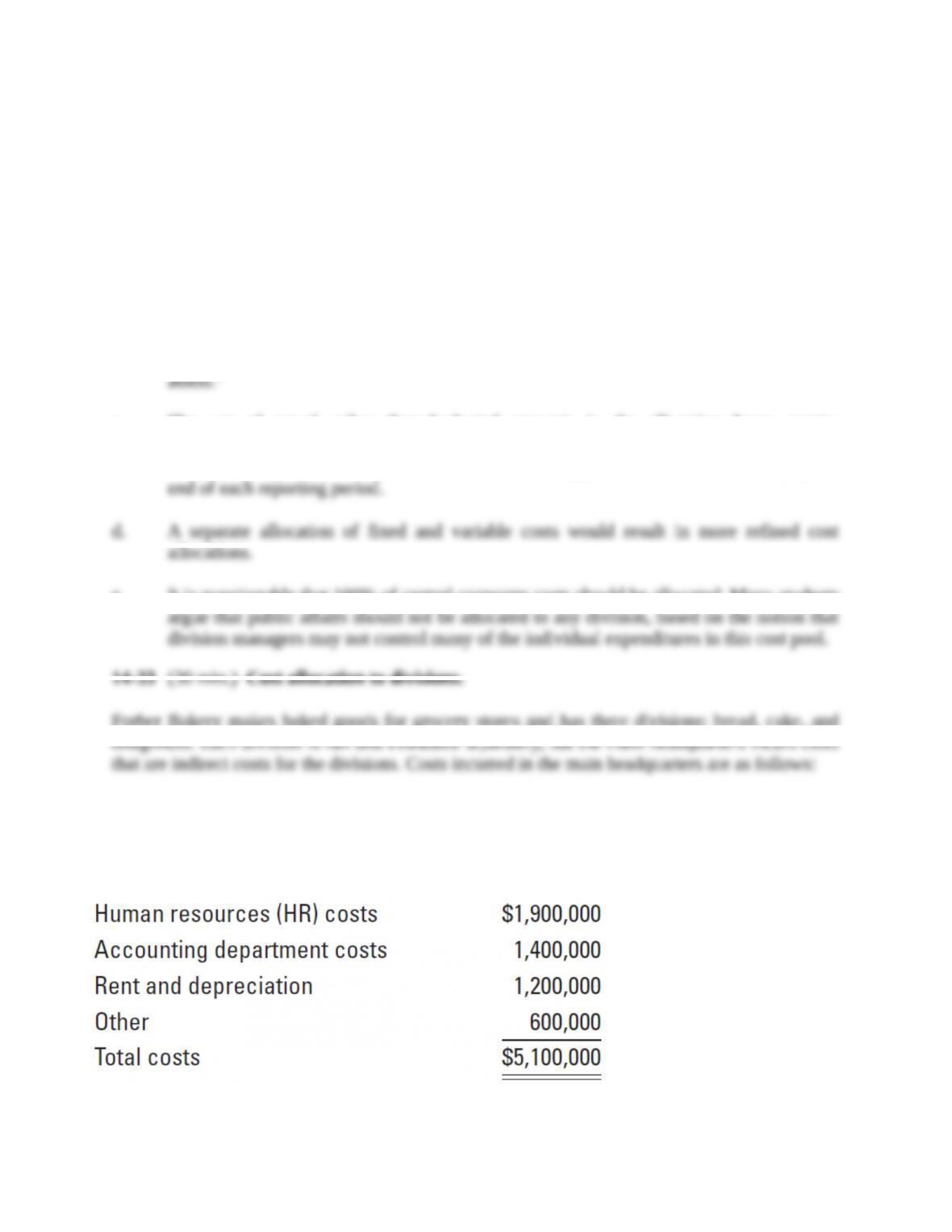

1HR costs: 400 ÷ 800 = 50%; 100 ÷ 800 = 12.5%; 300 ÷ 800 = 37.5%

2Accounting: $20,900,000 ÷ $38,800,000 = 53.9%; $4,500,000 ÷ $38,800,000 = 11.6%;

$13,400,000 ÷ $38,800,000 = 34.5%

3Rent and depreciation: 10,000 ÷ 20,000 = 50%; 4,000 ÷ 20,000 = 20%; 6,000 ÷ 20,000 = 30%

A cause-and-effect relationship may exist between Human Resources costs and the number of

employees at each division. Rent and depreciation costs may be related to square feet, except

that very expensive machines may require little square footage, which is inconsistent with this

choice of allocation base. The Accounting Department costs are probably related to the revenues

earned by each division—higher revenues mean more transactions and more accounting. Other

overhead costs are allocated arbitrarily.

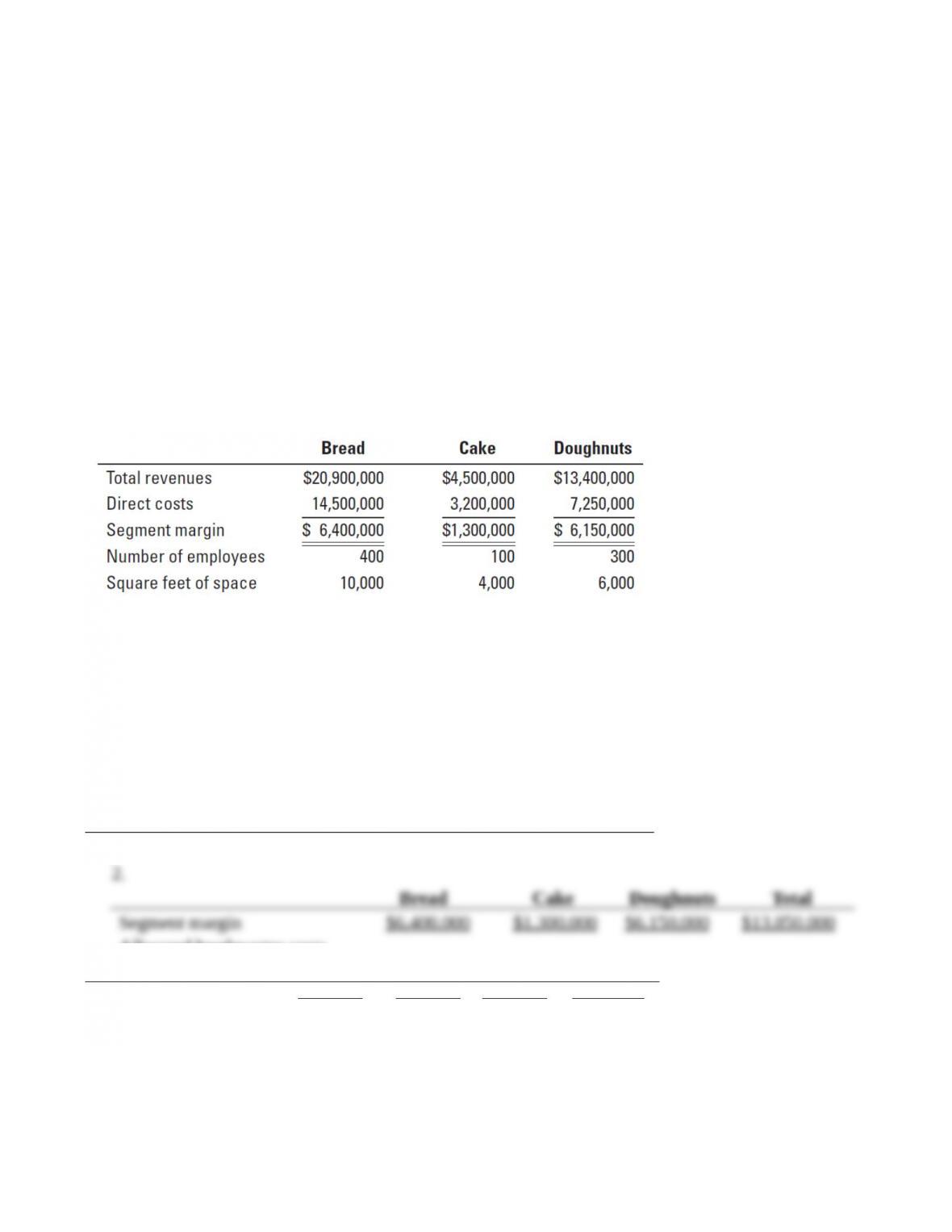

3. The manager who suggested the new allocation bases probably works in the Cake

Division. Under the old scheme, the Cake Division shows an operating loss after allocating

headquarter costs because it is smaller, yet was charged an equal amount (a third) of headquarter

costs. The new allocation scheme shows an operating profit in the Cake Division, even after

allocating headquarter costs. The ABC method is a better way to allocate headquarter costs

because it uses cost allocation bases that, by and large, represent cause-and-effect relationships

between various categories of headquarter costs and the demands that different divisions place

on these costs.

14-34 (30 min.) Cost-hierarchy income statement and allocation of corporate, division, and

channel costs to customers.

Rod Manufacturing Company produces metal rods for their customers. Its wholesale division is

the focus of our analysis.

Management of the company wishes to analyze the profitability of the three key customers in

the division and has gathered the following information.

The company allocates wholesale channel costs to customers based on one cost pool and division

costs based on two cost pools as follows. Customer actions do not influence these costs.