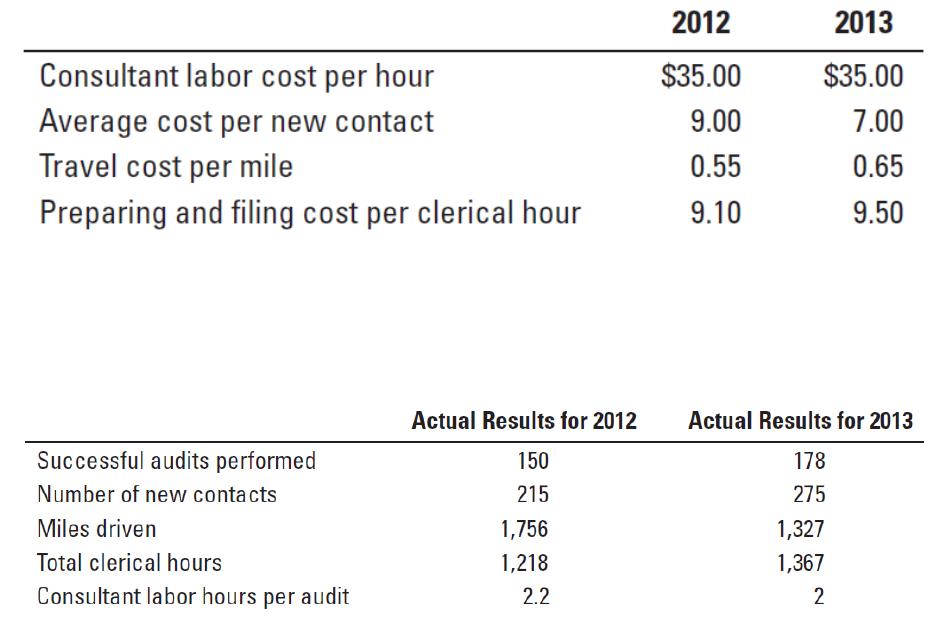

2012

2013

Total

Per unit

(2)=

(1) ÷ 150

Total

Per unit

(4)=

(3) ÷ 178

Consultation labor

$35 × 2.2 hrs. × 150; $35 × 2 hrs. × 178

$11,550.0

0

$ 77.00

$12,460.00

$ 70.00

Cost of new contacts, $9 × 215; $7 × 275

1,935.00

12.90

1,925.00

10.81

Travel costs, $0.55 × 1,756; $0.65 × 1,327

965.80

6.44

862.55

4.85

Preparing and filing costs

$9.10 × 1,218; $9.50 × 1,367

11,083.80

73.89

12,986.50

72.96

Total

$25,534.6

0

$170.23

$28,234.05

$158.62

3. Target cost per audit in 2013 = Cost per audit in 2012 × 95%

= $170.23 × 0.95 = $161.72

Actual cost per audit in 2013 was $158.62. Hence, Sun Systems did achieve its target cost per audit

of $161.72

In spite of rising transportation costs and clerical wages, the company was able to reduce the cost

per audit in 2013. This was possible by reducing the number of miles driven per appointment from

11.7 miles (1,756 ÷ 150) in 2012 to 7.5 miles (1,327 ÷ 178) in 2013. This could be due to a

implementing a better scheduling system to maximize the number of appointments in a given area.

Also, the number of clerical hours per audit decreased from 8.12 hours (1,218 ÷ 150) in 2012 to

7.68 hours (1,367 ÷ 178) in 2013. This could be due to process improvements in preparing the

required forms. There is also a reduction in consultant labor hours and consultation labor cost per

audit. Presumably, there is no reduction in customer satisfaction.

4. The challenges Sun Systems may face in achieving their target cost include employee resistance

to changes in processes, unexpected increases in the cost of supplies, fuel, etc, and new compliance

requirements imposed from the federal and/or state governments that increase clerical time on each

audit. To overcome these challenges, Sun Systems managers should encourage employee

participation and celebrate small improvements toward achieving the target cost and set cost-

cutting targets after taking into account the external environment such as cost of supplies and new

compliance requirements. Managers should create a culture where employees are encouraged to

continuously improve the energy audit process.

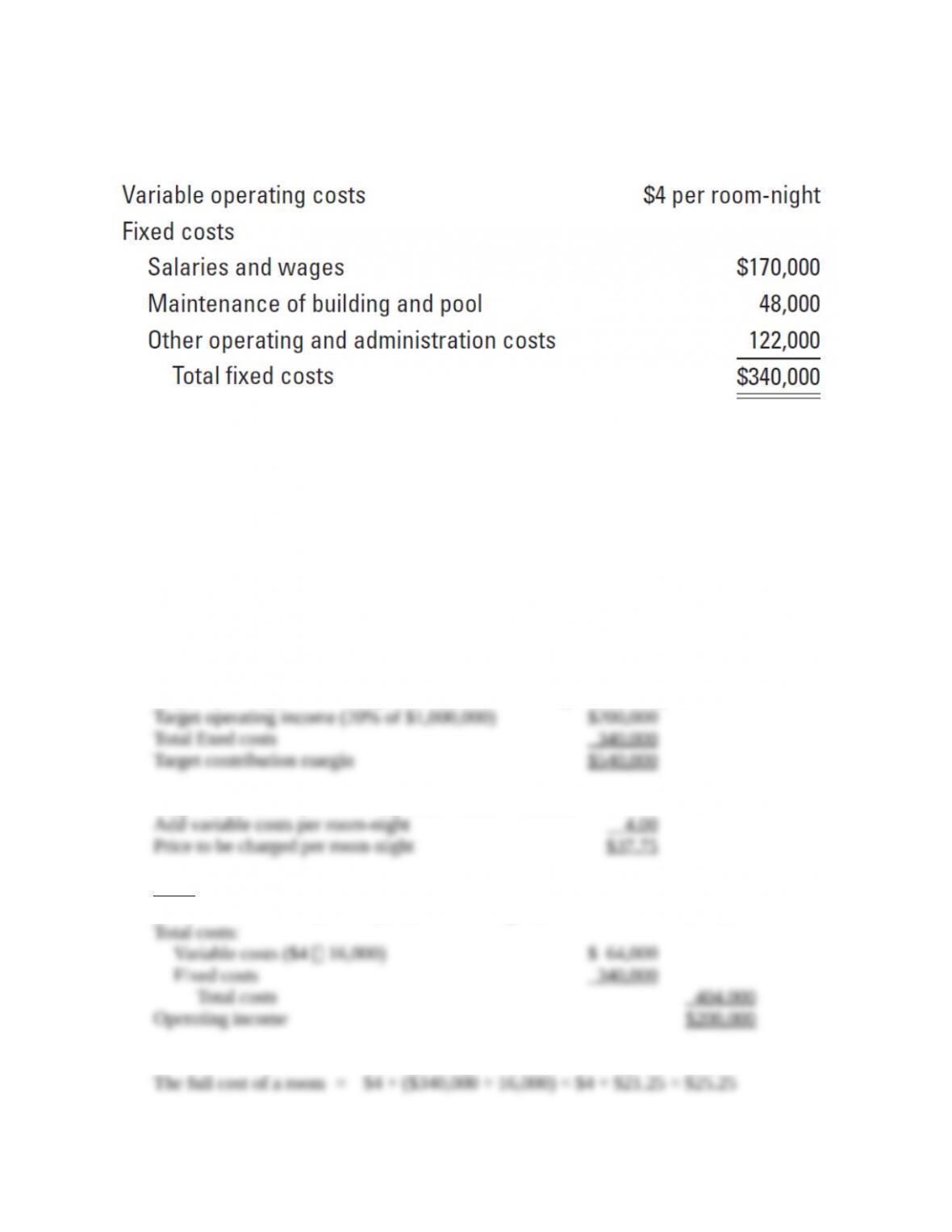

13-21 (20 min.) Cost-plus target return on investment pricing.

John Branch is the managing partner of a business that has just finished building a 60-room motel.

Branch anticipates that he will rent these rooms for 16,000 nights next year (or 16,000 room–

nights). All rooms are similar and will rent for the same price. Branch estimates the following

operating costs for next year:

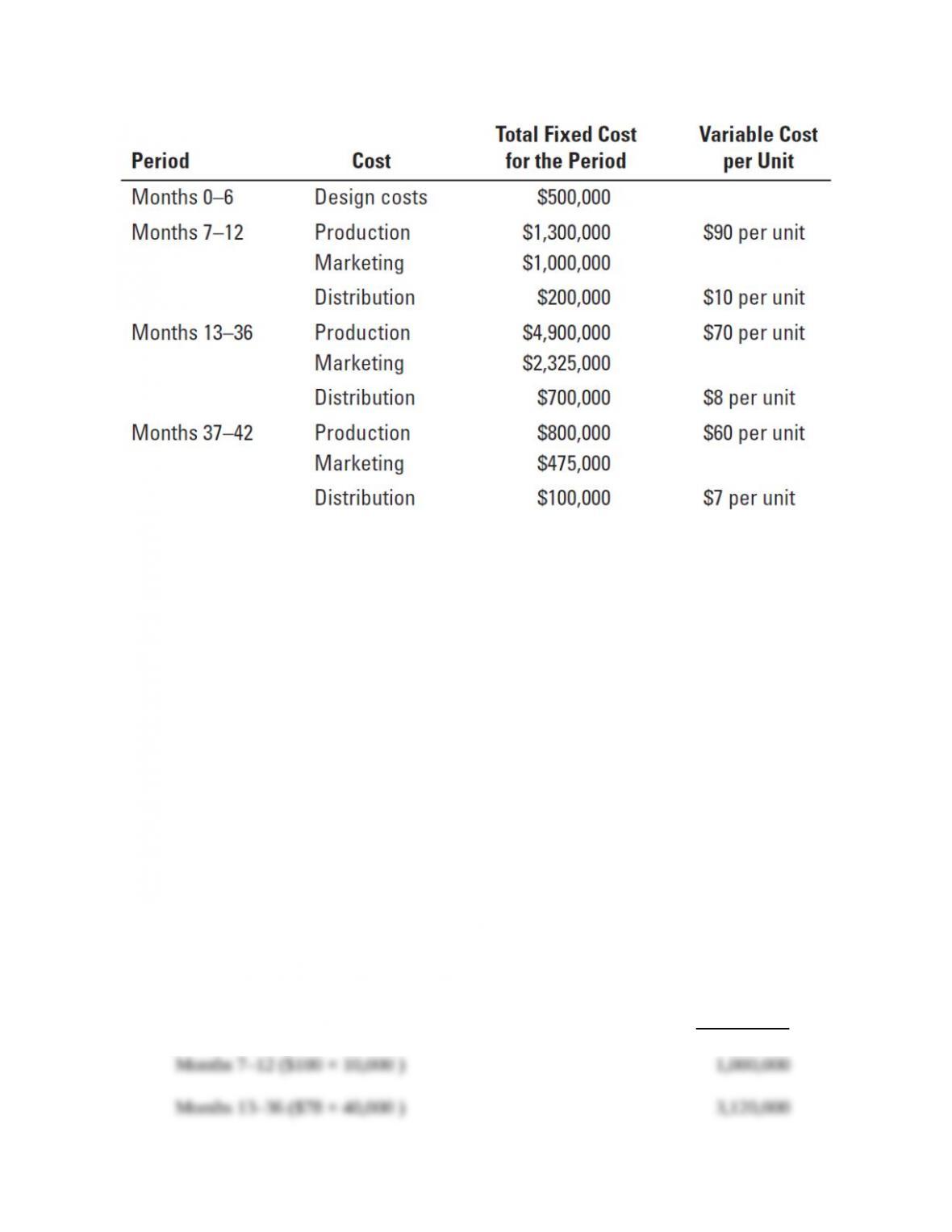

Months 37–42 ($67 × 5,000 )

335,000

Total variable costs

4,455,000

Fixed costs:

Design costs

500,000

Production ($1,300,000 + $4,900,000 + $800,000)

7,000,000

Marketing ($1,000,000 + $2,325,000 + $475,000)

3,800,000

Distribution ($200,000 + $700,000 + $100,000)

1,000,000

Total fixed costs

12,300,000

Life cycle operating income

$ 3,870,000

Average profit per sweeper = $3,870,000/(10,000 + 40,000 + 5,000) = $70.36

2.

Projected Life Cycle Income Statement (in 000s)

Months 7–12

Revenues ($375 × 10,000)

$3,750,000

Variable costs:

Months 7–12 ($100 × 10,000 )

1,000,000

Fixed costs:

Production

1,300,000

Marketing

1,000,000

Distribution

200,000

Total fixed costs

2,500,000

Operating income

$ 250,000

Average profit per sweeper = $250,000/10,000 = $25

Projected Life Cycle Income Statement (in 000s)

Months 13–36

Revenues ($375 × 40,000)

$15,000,000

Variable costs:

Months 13-36 ($78 × 40,000 )

3,120,000

Fixed costs:

Production

4,900,000

Marketing

2,325,000

Distribution

700,000

Total fixed costs

7,925,000

Operating income

$ 3,955.000

Average profit per sweeper = $3,955,000/40,000 = $98.88

Projected Life Cycle Income Statement

Revenues [$425 × 9,500 + $375 × (38,000 + 5,000)]

$20,162,500

Variable costs:

Months 7–12 ($100 × 9,500 )

950,000

Months 13–36 ($78 × 38,000 )

2,964,000

Months 37–42 ($67 × 5,000 )

335,000

Total variable costs

4,249,000

Fixed costs:

Design costs

500,000

Production ($1,300,000 + $4,900,000 + $800,000)

7,000,000

Marketing ($1,000,000 + $2,325,000 + $475,000)

3,800,000

Distribution ($200,000 + $700,000 + $100,000)

1,000,000

Total fixed costs

12,300,000

Life cycle operating income

$ 3,613,500

Average profit per sweeper = $3,613,500/(9,500 + 38,000 + 5,000) = $68.83

Jurgensen earns more profit under its original plan ($3,870,000) than it does if it increases the

price to $425 for the first six months ($3,613,500). The decline in sales as a result of increasing

the price reduces operating income. Therefore, Jurgensen should price the seepers at $375 for the

first six months rather than increase the price to $425.