1) Which of the following is true of flexible budget?

A) It calculates total variable cost by multiplying actual units by budgeted variable cost

per unit.

B) It calculates total fixed cost by multiplying actual units by budgeted fixed cost per

unit.

C) It calculates revenues by multiplying budgeted units by actual selling price per unit.

D) It calculates contribution margin by multiplying budgeted units by actual

contribution margin per unit.

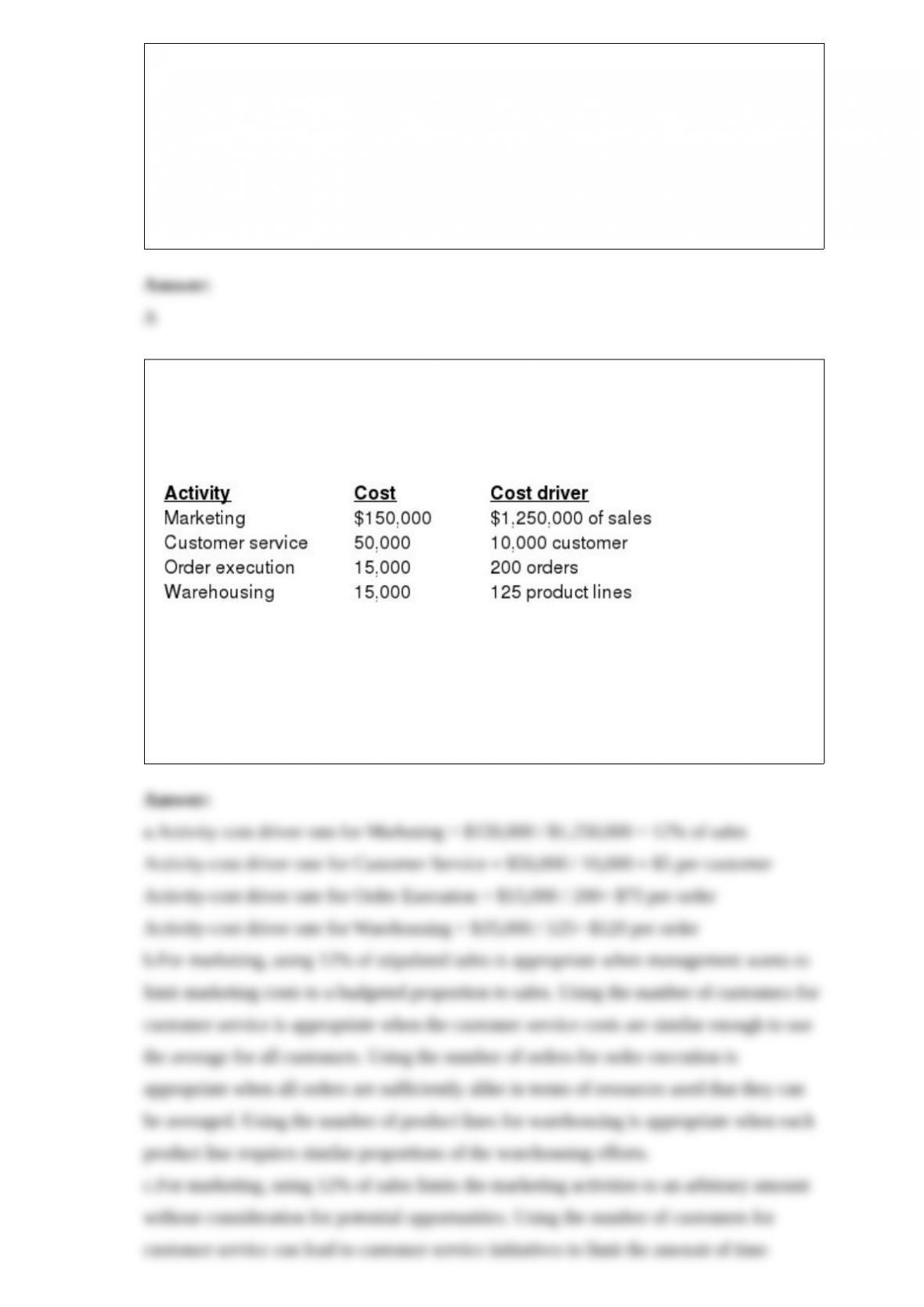

2) The Skynet Company is noted for an exceptionally impressive line of Mardi Gras

masks. Skynet has established the following selling and distribution support

activity-cost pools and their corresponding activity drivers for the year 2015:

Required:

a.Determine the activity-cost-driver rate for each of the four selling and distribution

activities.

b.Under what circumstances is it appropriate to use each of the activity-cost drivers?

c.Describe at least one possible negative behavioral consequence for each of the four

activity-cost drivers.

3) The following information is for Alex Corp:

What is the breakeven point assuming the sales mix consists of two units of Product X

and one unit of Product Y?

A) 1,000 units of Y and 2,000 units of X

B) 1,113 units of Y and 2,025 units of X

C) 2,313 units of Y and 4,025 units of X

D) 1,250 units of Y and 2,500 units of X

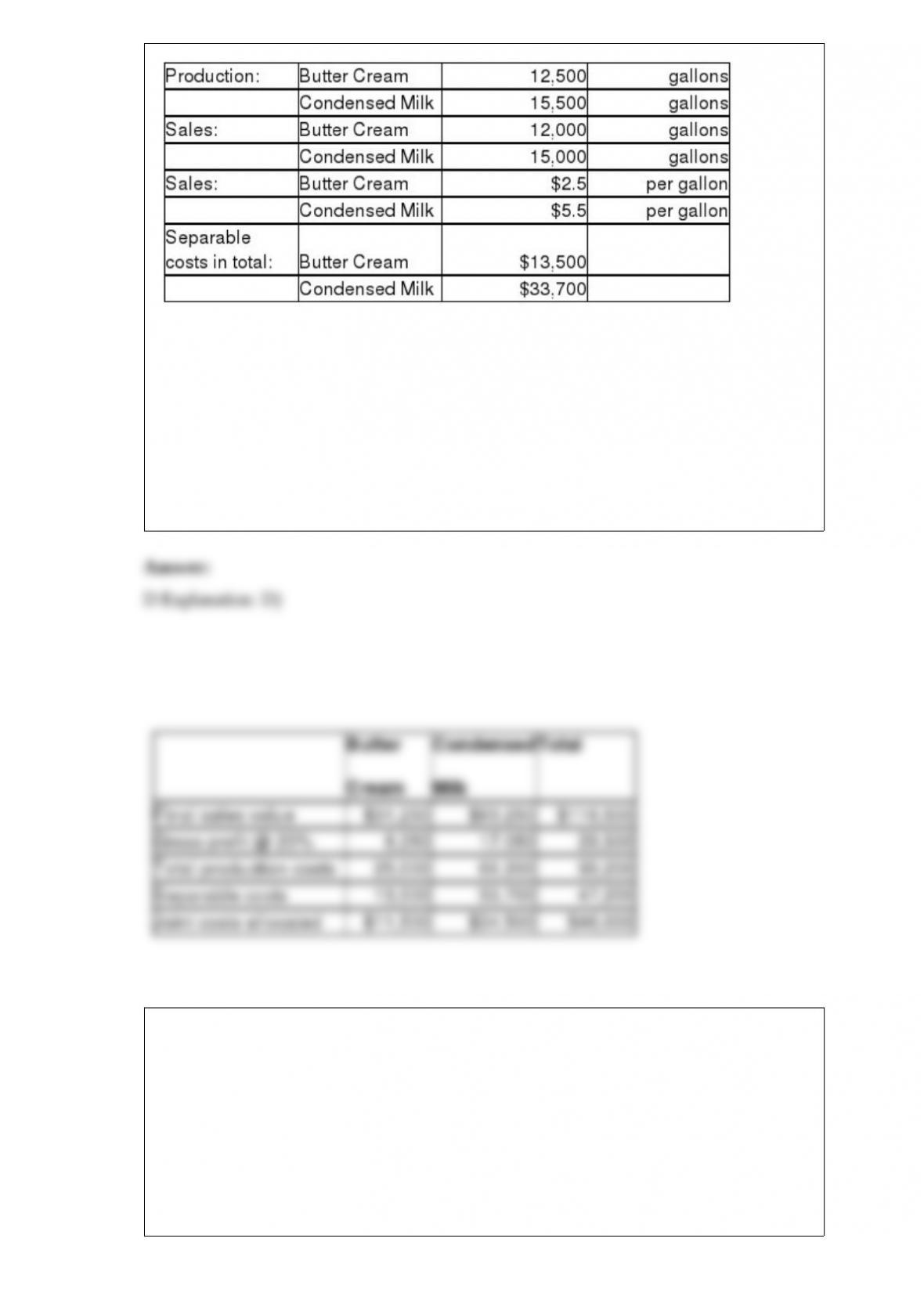

4) The Brital Company processes unprocessed milk to produce two products, Butter

Cream and Condensed Milk. The following information was collected for the month of

June:

Direct Materials processed:28,000 gallons

The costs of purchasing the of unprocessed milk and processing it up to the splitoff

point to yield a total of 28,000 gallons of saleable product was $46,000.

The company uses constant gross-margin percentage NRV method to allocate the joint

costs of production.

What is the allocated joint costs of Butter Cream?

A) $33,700

B) $13,500

C) $34,500

D) $11,500

5) Which of the following statements is true of variable overhead costs?

A) All the decisions determining the level of variable overhead costs are made at the

start of a budget period.

B) Planning of variable overhead costs includes choosing the appropriate level of

capacity.

C) Activities which add value are of least relevance while planning variable overhead

costs.

D) The level of variable overhead costs incurred in a period is mainly determined by

day-to-day operating decisions.

6) The Octova Corporation manufactures two types of vacuum cleaners: the ZENITH

for commercial building use and the House-Helper for residences. Budgeted and actual

operating data for the year 20X5 are as follows:

Static Budget ZENITHHouse-HelperTotal

Number sold20,00080,000100,000

Contribution margin$4,600,000$15,200,000$19,800,000

Actual Results ZENITHHouse-HelperTotal

Number sold21,50060,00081,500

Contribution margin$6,665,000$13,200,000$19,865,000

Required:

a.Calculate the contribution margin for the flexible budget.

b.Determine the total static-budget variance, the total flexible-budget variance, and the

total sales-volume variance in terms of the contribution margin.

7) When a greater proportion of costs are fixed costs, then ________.

A) a small increase in sales results in a small decrease in operating income

B) when demand is low the risk of loss is high

C) a decrease in sales reduces the total fixed cost per unit

D) a decrease in sales reduces the cost per unit

8) Activity-based budgeting ________.

A) uses one cost driver such as direct labor-hours

B) uses only output-based cost drivers such as units sold

C) focuses on activities necessary to produce and sell products and services

D) classifies costs by functional area within the value chain

9) As per control charts, nonrandom variations occurs when ________.

A) there is a sudden increase in production

B) chance fluctuations in the speed of equipment cause defective products to be

produced

C) defective products are produced as a result of a systematic problem

D) there is a sudden increase in sales

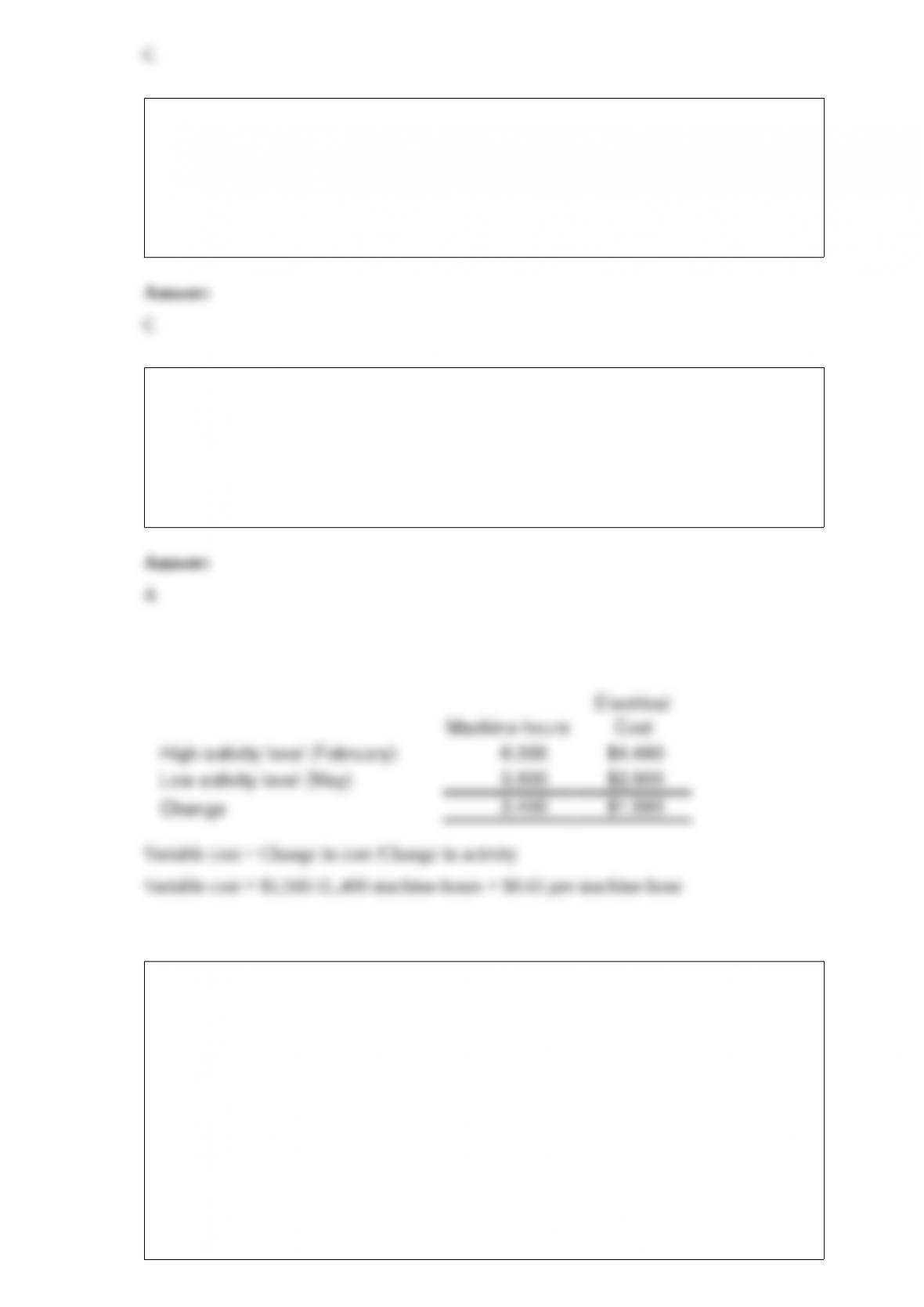

10) Using the high-low method of analysis, the estimated variable electrical cost per

machine hour is:

A) $0.65

B) $0.40

C) $0.70

D) $0.67

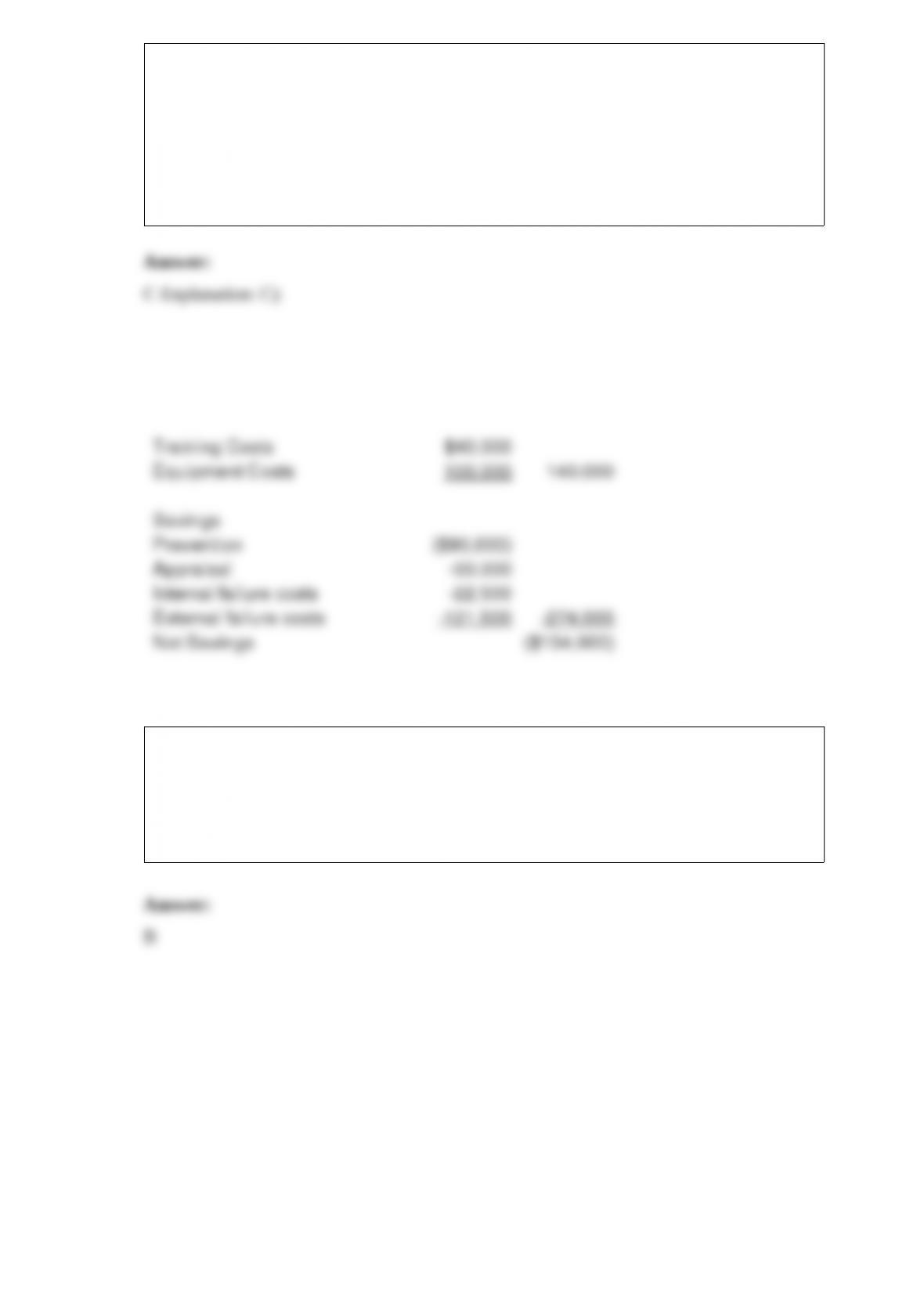

11) LaCrosse Products has a budget of $900,000 in 2015 for prevention costs. If it

decides to automate a portion of its prevention activities, it will save $80,000 in

variable costs. The new method will require $40,000 in training costs and $100,000 in

annual equipment costs. Management is willing to adjust the budget for an amount up

to the cost of the new equipment. The budgeted production level is 150,000 units.

Appraisal costs for the year are budgeted at $600,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $15 per failed unit of

finished goods. The internal failure rate is expected to be 3% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $54 per failed unit. The company’s

average external failures average 3% of units sold. The new proposal will reduce this

rate by 50%. Assume all units produced are sold and there are no ending inventories.

Management has offered to allow the prevention changes if all changes take place as

anticipated and the amounts netted are less than the cost of the equipment. What is the

net impact of all the changes created by the preventive changes?

A) $140,000

B) $(22,500)

C) $(134,000)

D) $(121,500)

12) For fixed manufacturing overhead, there is no ________.

A) spending variance

B) efficiency variance

C) flexible-budget variance

D) production-volume variance