Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

6-1

1. When the office manager receives calls from potential customers, she is instructed to handle

the contracts herself. Recently, however, the number of contracts written up by the office

manager has declined. At the same time, one of the sales representatives has experienced a

significant increase in contracts. The other two representatives believe that the office manager

has been colluding with the third representative to send him the prospective customers.

2. One of the motor coach drivers seems to be reaching his destinations more quickly than any of

the other drivers and is reporting longer idle time.

3. Fuel costs have increased significantly in recent months. Driving the motor coaches at 60 miles

per hour on the highway consumes significantly less fuel than driving them at 65 miles per

hour.

4. Regular preventive maintenance of the motor coaches has been proven to improve fuel

efficiency and reduce overall operating costs by averting costly repairs. During busy months,

however, it is difficult for the maintenance technician to complete all of the maintenance tasks

within his 40-hour workweek.

5. Jason Haslett has read about stretch targets, and he believes that a change in the compensation

structure of the sales representatives may improve sales. Rather than a straight commission of

10% of sales, he is considering a system where each representative is given a monthly goal of

50 contracts. If the goal is met, the representative is paid a 12% commission. If the goal is not

met, the commission falls to 8%. Currently, each sales representative averages 45 contracts per

month.

Required:

For situations 1–4, discuss which employee has responsibility for the related costs and the extent

to which costs are controllable and by whom. What are the risks or costs to the company? What

can be done to solve the problem or improve the situation? For situation 5, describe the potential

benefits and costs of establishing stretch targets.

SOLUTION

1. The office manager has the responsibility to follow company guidelines and write contracts

herself for customers who call her directly. Diverting potential customers to the sales

representative costs the company a sales commission that would not have otherwise been paid. If

satisfaction surveys are sent to customers asking about their first contact with the company, this

may be enough to prevent the office manager from breaking the rules.

2. Each driver is responsible for keeping an accurate accounting of his or her time. Because the

drivers are paid for mileage while driving and an hourly rate while in idle, there is an incentive to

report less travel time and more idle time. The cost could be controlled by using global positioning

systems (GPS) to track the movement and location of the motor coaches.

3. The drivers are responsible for driving the motor coaches at fuel-efficient speeds on the

highway. The maintenance technician is responsible for maintaining the vehicles to improve

efficiency. An increase in fuel consumption would be difficult to pin on either employee because

either could be responsible. Further, there is no incentive for the drivers to drive slower, as they

are paid by the mile. Again, global positioning systems (GPS) could be used to track the movement

6-2

of the vehicles. Some kind of bonus could be offered to the technician for improvements in fuel

efficiency.

4. The maintenance technician is clearly responsible for completing all of the preventative

maintenance. If he cannot complete the tasks during busy months, the company should consider

outsourcing some of the more routine maintenance jobs. Requiring the technician to work

significant overtime will likely decrease his efficiency. Ignoring routine maintenance will end up

costing the company more money in fuel and repair costs.

5. Haslett has designed the stretch target system correctly. Taking advantage of loss aversion,

Haslett has set a stretch target of 50 contracts rewarding the representative with a 12 percent

commission (assuming paying this amount of commission is profitable). If the target is not met,

the commission decreases to 8 percent. This will motivate the representatives to achieve 50

contracts.

In establishing “stretch targets,” Haslett should be sure that there are sufficient potential

contracts to allow all three sales representatives to achieve the higher target. Otherwise, the stretch

target may cause friction among the representatives. One or more of representatives may decide

that the 8 percent commission is not sufficient incentive to stay with the company, and may leave

to work for a competitor, resulting in overall reduced sales.

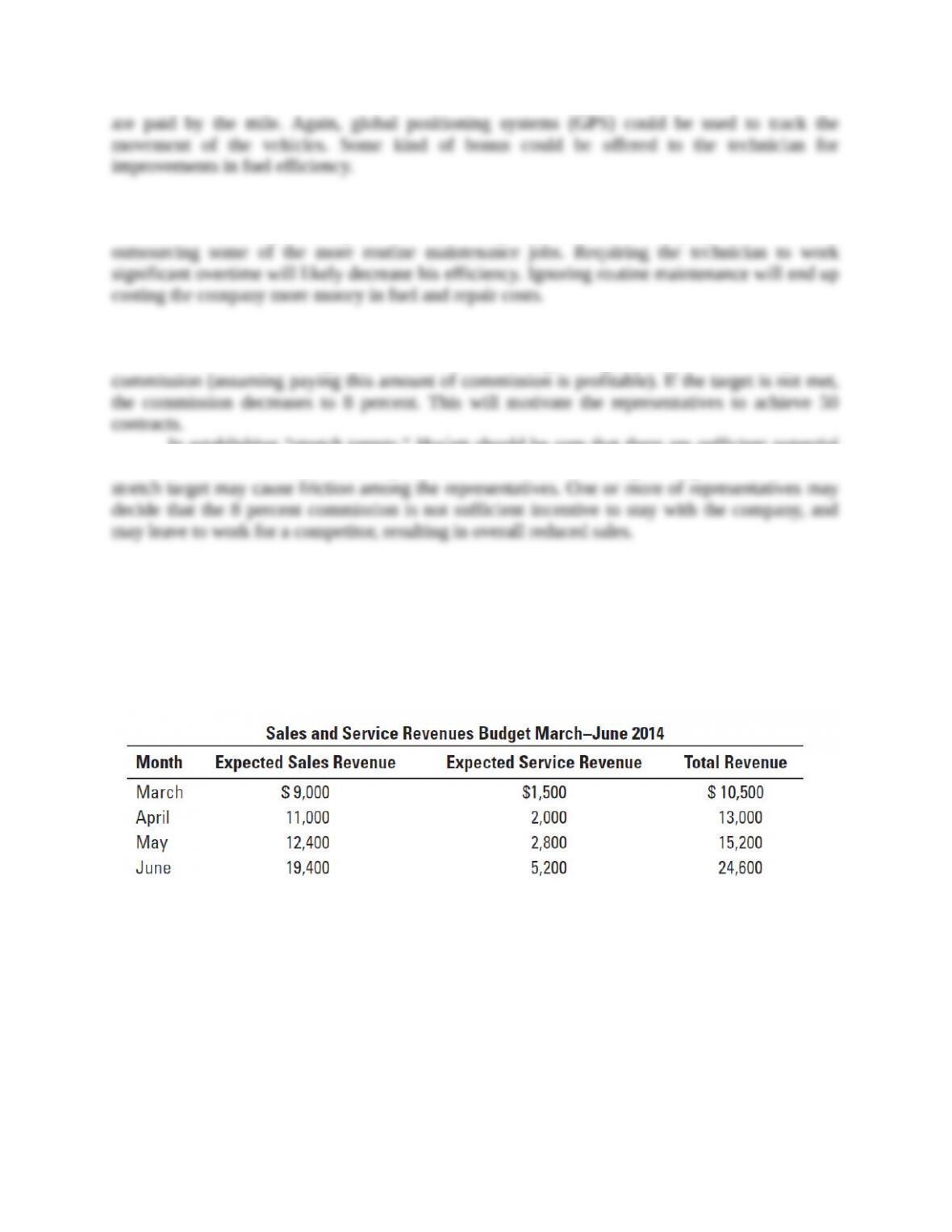

6-29 (30 min.) Cash flow analysis, sensitivity analysis.

Game Depot is a retail store selling video games. Sales are uniform for most of the year but pick

up in June and December both because new releases come out and because consumers purchase

games in anticipation of summer or winter holidays. Game Depot also sells and repairs game

systems. The forecast of sales and service revenue for the March–June 2014 is as follows:

Almost all the service revenue is paid for by bank credit card, so Game Depot budgets this as 100%

bank card revenue. The bank cards charge an average fee of 3% of the total. Half of the sales

revenue is also paid for by bank credit card, for which the fee is also 3% on average. About 10%

of the sales are paid in cash, and the rest (the remaining 40%) are carried on a store account.

Although the store tries to give store credit only to the best customers, it still averages about 2%

for uncollectible accounts; 90% of store accounts are paid in the month following the purchase,

and 8% are paid 2 months after purchase.

Required:

1. Calculate the cash that Game Depot expects to collect in May and in June 2014. Show

calculations for each month.

2. Game Depot has budgeted expenditures for May of $8,700 for the purchase of games and game

systems, $2,800 for rent and utilities and other costs, and $2,000 in wages for the two part-

time employees.

a. Given your answer to requirement 1, will Game Depot be able to cover its payments for

May?

b. The projections for May are a budget. Assume (independently for each situation) that May

revenues might also be 5% less and 10% less and that costs might be 8% higher. Under

each of those three scenarios, show the total net cash for May and the amount Game Depot

would have to borrow if cash receipts are less than cash payments. Assume the beginning

cash balance for May is $200.

3. Why do Game Depot’s managers prepare a cash budget in addition to the revenue, expenses,

and operating income budget? Has preparing the cash budget been helpful? Explain briefly.

4. Suppose the costs for May are as described in requirement 2, but the expected cash receipts for

May are $12,400 and beginning cash balance is $200. Game Depot has the opportunity to

purchase the games and game systems on account in May, but the supplier offers the company

credit terms of 2/10 net 30, which means if Game Depot pays within 10 days (in May) it will

get a 2% discount on the price of the merchandise. Game Depot can borrow money at a rate of

24%. Should Game Depot take the purchase discount?

SOLUTION

1. The cash that Game Depot can expect to collect during May and June is calculated below.

Cash collected in May June

From service revenue

May ($2,800 0.97) $ 2,716

June ($5,200 0.97) $ 5,044

From sales revenue

Cash sales

From credit card sales

May (0.5 $12,400 0.97) 6,014

June (0.5 $19,400 0.97) 9,409

From cash sales

May (0.1 $12,400) 1,240

June (0.1 $19,400) 1,940

Credit sale collections

From March (0.4 $9,000 0.08) 288

From April (0.4 $11,000 0.9) 3,960

(0.4 $11,000 0.08) 352

From May (0.4 $12,400 0.9) _______ 4,464

Total collections $14,218 $21,209

2. (a) Budgeted expenditures for May are as follows.

Costs

Inventory purchases

$ 8,700

Rent, utilities, etc.

2,800

6-4

Wages

2,000

Total

$13,500

Yes, Game Depot will be able to cover its May costs because receipts are $14,218 and

expenditures are only $13,500.

(b)

Original

numbers

May

Revenues

decrease

10%

May Revenues

decrease 5%

May Costs

increase 8%

Beginning cash

$ 200.00

$ 200.00

$ 200.00

$ 200.00

Collections

14,218.00

13,221.00a

13, 719.50b

14,218.00c

Cash Costs

13,500.00

13,500.00

13,500.00

14,580.00

Total

$ 918.00

$ (79.00)

$ 419.50

$ (162.00)

aFrom requirement 1, this is 0.90 × ($2,716 + $6,014 + $1,240) + $288 + $3,960 = $13,221

bFrom requirement 1, this is 0.95 × ($2,716 + $6,014 + $1,240) + $288 + $3,960 = $13,719.50

c$13,500 1.08 = $14,580.

3. Game Depot’s managers prepare a cash budget in addition to the operating income budget

to plan cash flows to ensure that the company has adequate cash to pay vendors, meet payroll, and

pay operating expenses as these payments come due. Game Depot could be very profitable on an

accrual accounting basis, but the pattern of cash receipts from revenues might be delayed and result

in insufficient cash being available to make scheduled payments for its expenses. Game Depot’s

managers may then need to initiate a plan to borrow money to finance any shortfall. Building a

profitable operating plan does not guarantee that adequate cash will be available, so Game Depot’s

managers need to prepare a cash budget in addition to an operating income budget.

4. The cost of inventory purchases without the discount is $8,700, which Game Depot would

not have to pay until June if it buys the inventory on account in May. However, if it takes the

discount and pays in May, the cost will be $8,700 (100% – 2%) = $8,526. This means it will

save $174.

This makes total expenditures for May

Costs

Inventory purchases

$ 8,526.00

Rent, utilities, etc.

2,800.00

Wages

2,000.00

Total

$13,326.00

Game Depot’s total cash available is $200 (cash balance) + $12,400 (cash receipts), so it will have

to borrow $726 ($13,326 – $12,600) at a rate of 24 percent (or 2 percent per month.) Based on the

information from #1, it will be able to pay this back in June (assuming cash expenditures do not

increase dramatically), so it will incur interest costs of $726 0.02 = $14.52. Because it will cost

6-5

them less than $15 to save $174, it makes sense to go ahead and take the short-term loan to pay

the account payable early.

Some students might interpret the question to mean that the cost of inventory purchases after taking

the 2percent discount in May is $8,700. Under this interpretation, the cost of the inventory is

$8,700 ÷ 0.98 = $8,878. If Game Depot takes the discount and pays in May, it will save $8,878 –

$8,700 = $178

Total expenditures in May:

Inventory purchases

$8,700

Rent, utilities, etc.

2,800

Wages

2,000

Total

$13,500

Total cash available is $200 + $12,400 = $12,600, so Game Depot will borrow $900 ($13,500 –

$12,600) at a rate of 24 percent (or 2 percent per month). The company can repay in June, so

interest cost = $900 0.02 = $18. It will cost $18 to save $178, so Game Depot should take the

short-term loan to pay the accounts payable early.

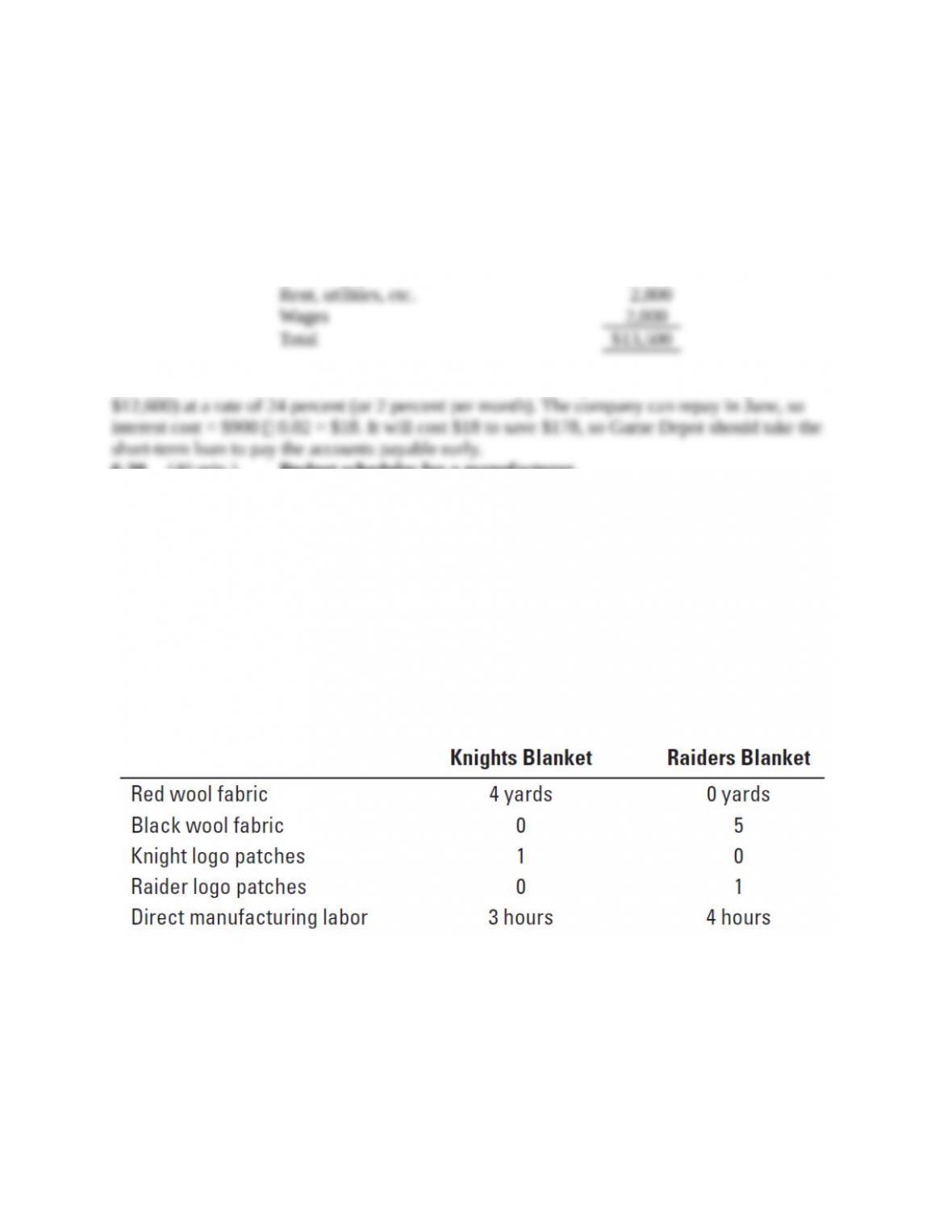

6-30 (40 min.) Budget schedules for a manufacturer.

Lame Specialties manufactures, among other things, woolen blankets for the athletic teams of the

two local high schools. The company sews the blankets from fabric and sews on a logo patch

purchased from the licensed logo store site. The teams are as follows:

▪ Knights, with red blankets and the Knights logo

▪ Raiders, with black blankets and the Raider logo

Also, the black blankets are slightly larger than the red blankets.

The budgeted direct-cost inputs for each product in 2014 are as follows:

Unit data pertaining to the direct materials for March 2014 are as follows:

6-6

Unit cost data for direct-cost inputs pertaining to February 2014 and March 2014 are as follows:

Manufacturing overhead (both variable and fixed) is allocated to each blanket on the basis of

budgeted direct manufacturing labor-hours per blanket. The budgeted variable manufacturing

overhead rate for March 2014 is $16 per direct manufacturing labor-hour. The budgeted fixed

manufacturing overhead for March 2014 is $14,640. Both variable and fixed manufacturing

overhead costs are allocated to each unit of finished goods.

Data relating to finished goods inventory for March 2014 are as follows:

Budgeted sales for March 2014 are 130 units of the Knights blankets and 190 units of the Raiders

blankets. The budgeted selling prices per unit in March 2014 are $229 for the Knights blankets

and $296 for the Raiders blankets. Assume the following in your answer:

▪ Work-in-process inventories are negligible and ignored.

▪ Direct materials inventory and finished goods inventory are costed using the FIFO method.

▪ Unit costs of direct materials purchased and finished goods are constant in March 2014.

Required:

1. Prepare the following budgets for March 2014:

a. Revenues budget

b. Production budget in units

c. Direct material usage budget and direct material purchases budget

d. Direct manufacturing labor budget

e. Manufacturing overhead budget

f. Ending inventories budget (direct materials and finished goods)

g. Cost of goods sold budget

2. Suppose Lame Specialties decides to incorporate continuous improvement into its budgeting

process. Describe two areas where it could incorporate continuous improvement into the

budget schedules in requirement 1.

SOLUTION

1a. Revenues Budget

Knights

Blankets

Raiders

Blankets

Total

Units sold

130

190

Selling price

$ 229

$ 296

Budgeted revenues

$29,770

$56,240

$86,010

b. Production Budget in Units

Knights

Blankets

Raiders

Blankets

Budgeted unit sales

130

190

Add budgeted ending fin. goods inventory

22

27

Total requirements

152

217

Deduct beginning fin. goods inventory

12

17

Budgeted production

140

200

c. Direct Materials Usage Budget (units)

Red

wool

Black

wool

Knights logo

patches

Raiders logo

patches

Total

Knights blankets:

1. Budgeted input per f.g. unit

4

–

1

–

2. Budgeted production

140

–

140

–

3. Budgeted usage (1 × 2)

560

–

140

–

Raiders blankets:

6-8

4. Budgeted input per f.g. unit

–

5

–

1

5. Budgeted production

–

200

–

200

6. Budgeted usage (4 × 5)

–

1,000

–

200

7. Total direct materials

usage (3 + 6)

560

1,000

140

200

Direct Materials Cost Budget

8. Beginning inventory

35

15

45

60

9. Unit price (FIFO)

$ 9

$ 12

$ 7

$ 6

10. Cost of DM used from

beginning inventory (8 × 9)

$ 315

$ 180

$315

$ 360

$ 1,170

11. Materials to be used from

purchases (7 – 8)

525

985

95

140

12. Cost of DM in March

$ 10

$ 11

$ 7

$ 8

13. Cost of DM purchased and

used in March (11 × 12)

$5,250

$10,835

$665

$1,120

$17,870

14. Direct materials to be used

(10 + 13)

$5,565

$11,015

$980

$1,480

$19,040

Direct Materials Purchases Budget

Red wool

Black

wool

Knights

logos

Raiders

logos

Total

Budgeted usage

(from line 7)

560

1,000

140

200

Add target ending inventory

25

25

25

25

Total requirements

585

1,025

165

225

Deduct beginning inventory

35

15

45

60

Total DM purchases

550

1,010

120

165

Purchase price (March)

$ 10

$ 11

$ 7

$ 8

Total purchases

$5,500

$11,110

$840

$1,320

$18,770

d. Direct Manufacturing Labor Budget

Budgeted

Direct

Manuf. Labor-

Units

Hours per

Total

Hourly

Produced

Output Unit

Hours

Rate

Total

Knights blankets

140

3

420

$27

$11,340

Raiders blankets

200

4

800

$27

21,600

1,220

$32,940

e. Manufacturing Overhead Budget

Variable manufacturing overhead costs (1,220 × $16) $19,520

Fixed manufacturing overhead costs 14,640

Total manufacturing overhead costs $34,160

6-9

Total manuf. overhead cost per hour = $34,160 ÷ 1,220 = $28 per direct manufacturing

labor-hour

Fixed manuf. overhead cost per hour = $ 14,640 ÷ 1,220 = $12 per direct manufacturing

labor-hour

f. Computation of unit costs of ending inventory of finished goods

Knights

Blankets

Raiders

Blankets

Direct materials

Red wool ($10 × 4, 0)

$ 40

$ 0

Black wool ($11 × 0, 5)

0

55

Knights logos ($7 × 1, 0)

7

0

Raiders logos ($8 × 0, 1)

0

8

Direct manufacturing labor ($27 × 3, 4)

81

108

Manufacturing overhead

Variable ($16 × 3, 4)

48

64

Fixed ($12 × 3, 4)

36

48

Total manufacturing cost

$212

$283

Ending Inventories Budget

Cost per Unit

Units

Total

Direct Materials

Red wool

$ 10

25

$ 250

Black wool

11

25

275

Knights logo patches

7

25

175

Raiders logo patches

8

25

200

900

Finished Goods

Knights blankets

212

22

4,664

Raiders blankets

283

27

7,641

12,305

Total

$13,205

g. Cost of goods sold budget

Beginning fin. goods inventory, March 1, 2014 ($1,440 + $2,550) $ 3,990

Direct materials used (from Dir. materials cost budget) $19,040

Direct manufacturing labor (Dir. manuf. labor budget) 32,940

Manufacturing overhead (Manuf. overhead budget) 34,160

Cost of goods manufactured 86,140

Cost of goods available for sale 90,130

Deduct ending fin. goods inventory, March 31, 2014 (Inventories budget) 12,305

Cost of goods sold $77,825

2. Areas where continuous improvement might be incorporated into the budgeting process:

(a) Direct materials. Either an improvement in usage or price could be budgeted. For

example, the budgeted usage amounts for the fabric could be related to the maximum

6-10

improvement (current usage – minimum possible usage) of yards of fabric for either

blanket. It may also be feasible to decrease the price paid, particularly with quantity

discounts on things like the logo patches.

(b) Direct manufacturing labor. The budgeted usage of 3 hours/4 hours could be

continuously revised on a monthly basis. Similarly, the manufacturing labor cost per

hour of $27 could be continuously revised down. The former appears more feasible

than the latter.

(c) Variable manufacturing overhead. By budgeting more efficient use of the allocation

base, a signal is given for continuous improvement. A second approach is to budget

continuous improvement in the budgeted variable overhead cost per unit of the

allocation base.

(d) Fixed manufacturing overhead. The approach here is to budget for reductions in the

year-to-year amounts of fixed overhead. If these costs are appropriately classified as

fixed, then they are more difficult to adjust down on a monthly basis.

6-31 (45 min.) Budgeted costs, Kaizen improvements.

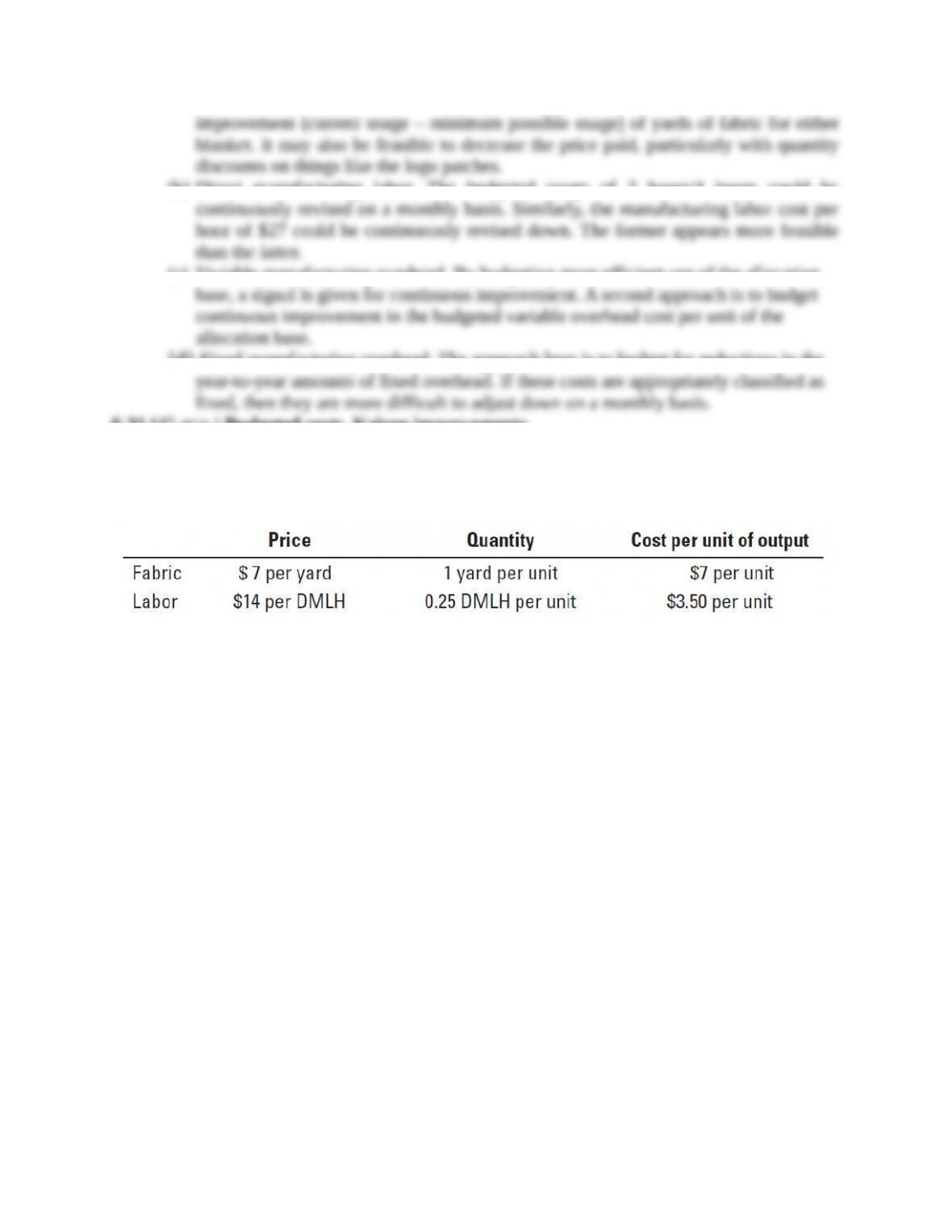

Trendy T-Shirt Factory manufactures plain white and solid- colored T-shirts. Inputs include the

following:

Additionally, the colored T-shirts require 3 ounces of dye per shirt at a cost of $0.40 per ounce.

The shirts sell for $14 each for white and $18 each for colors. The company expects to sell 12,000

white T-shirts and 60,000 colored T-shirts uniformly over the year.

Trendy has the opportunity to switch from using the dye it currently uses to using an

environmentally friendly dye that costs $1.25 per ounce. The company would still need 3 ounces

of dye per shirt. Trendy is reluctant to change because of the increase in costs (and decrease in

profit), but the Environmental Protection Agency has threatened to fine the company $120,000 if

it continues to use the harmful but less expensive dye.

Required:

1. Given the preceding information, would Trendy be better off financially by switching to the

environmentally friendly dye? (Assume all other costs would remain the same.)

2. Assume Trendy chooses to be environmentally responsible regardless of cost, and it switches

to the new dye. The production manager suggests trying Kaizen costing. If Trendy can reduce

fabric and labor costs each by 1% per month, how close will it be at the end of 12 months to

the profit it would have earned before switching to the more expensive dye? (Round to the

nearest dollar for calculating cost reductions.)

3. Refer to requirement 2. How could the reduction in material and labor costs be accomplished?

Are there any problems with this plan?