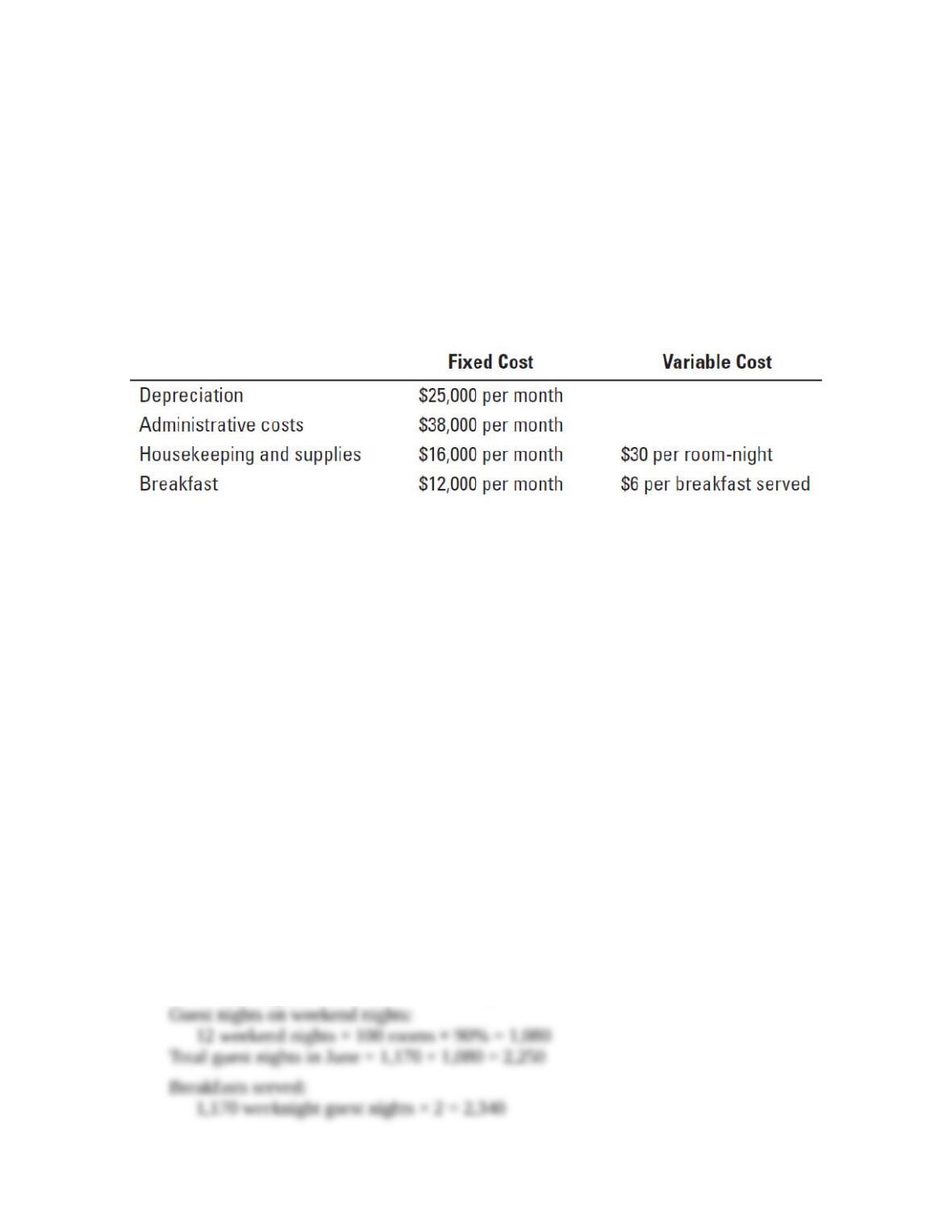

Total breakfasts served in June = 2,340 + 4,320 = 6,660

Total costs for June:

Depreciation

$ 25,000

Administrative costs

38,000

Fixed housekeeping and supplies

16,000

Variable housekeeping and supplies (2,250 × $30)

67,500

Fixed breakfast costs

12,000

Variable breakfast costs (6,660 × $6)

39,960

Total costs for June

$198,460

Cost per guest night ($198,460 ÷ 2,250)

$88.20

Revenue for June ($85 × 2,250)

$191,250

Total costs for June

198,460

Operating income/(loss)

$ (7,210)

2.

New weeknight guest nights

18 weeknights × 100 rooms × 75% = 1,350

New weekend guest nights

12 weeknights × 100 rooms × 90% = 1,080

Total guest nights in June l = 1,350 + 1,080 = 2,430

Breakfasts served:

1,350 weeknight guest nights × 2 = 2,700

1,080 weekend guest nights × 4 = 4,320

Total breakfasts served in June = 2,700 + 4,320 = 7,020

Total costs for June:

Depreciation

$ 25,000

Administrative costs

38,000

Fixed housekeeping and supplies

16,000

Variable housekeeping and supplies (2,430 × $30)

72,900

Fixed breakfast costs

12,000

Variable breakfast costs (7,020 × $6)

42,120

Total costs

$206,020

Revenue [(1,350 × $75) + (1,080 × $105)]

$214,650

Total costs for June

206,020

Operating income

$ 8,630

Yes, this pricing arrangement would increase operating income by $15,840 from an

operating loss of $7,210 to an operating income of $8,630 ($8,630 + $7,210 = $15,840).

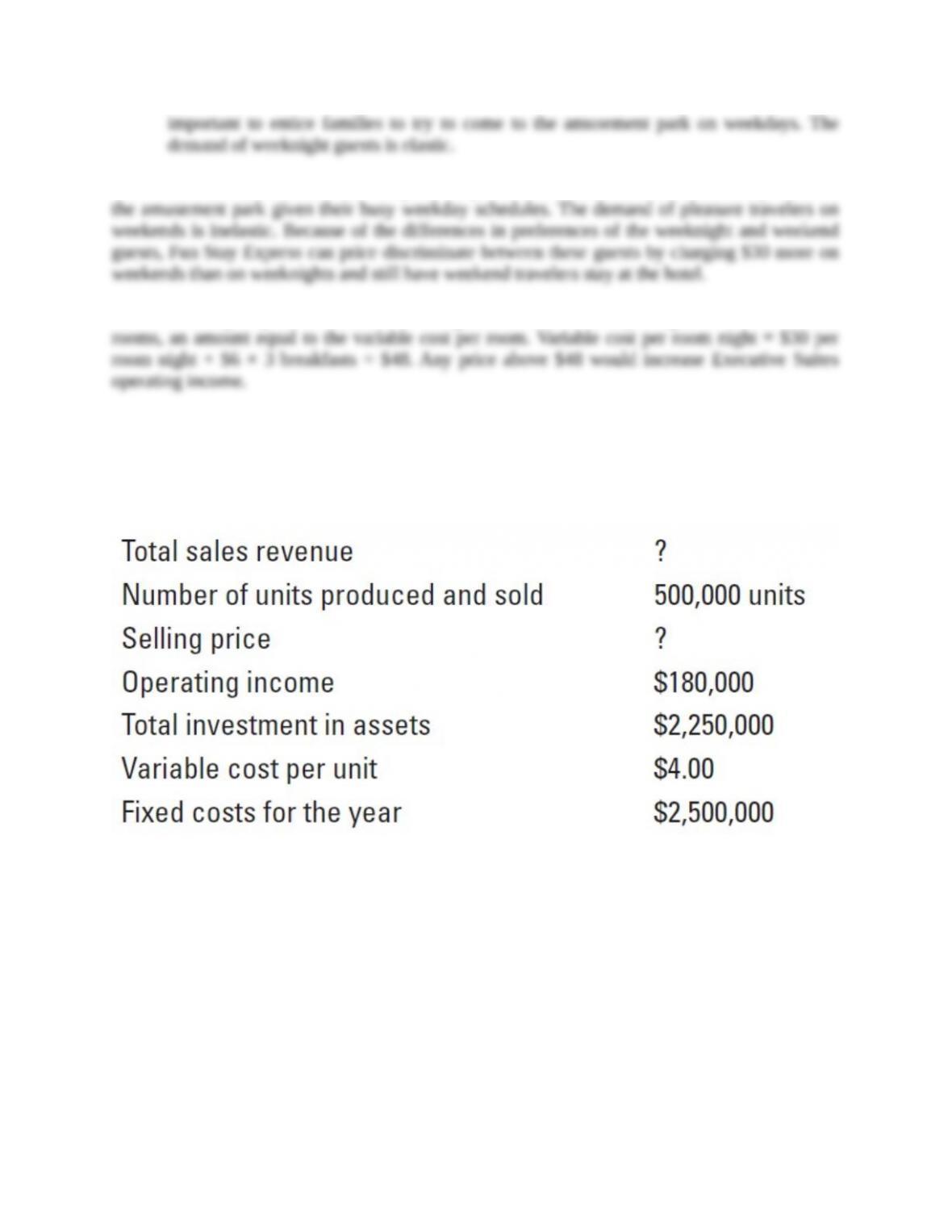

1. Guests typically do not come to the amusement park on weekdays because adults are busy

at work and children have to attend school. The weeknight guests are families who stay at

the hotel for convenience. They are willing to consider other hotel options or even not

travel at all if the price is high and unaffordable. Reducing the weeknight price is important

to entice families to try to come to the amusement park on weekdays. The demand of

weeknight guests is elastic.

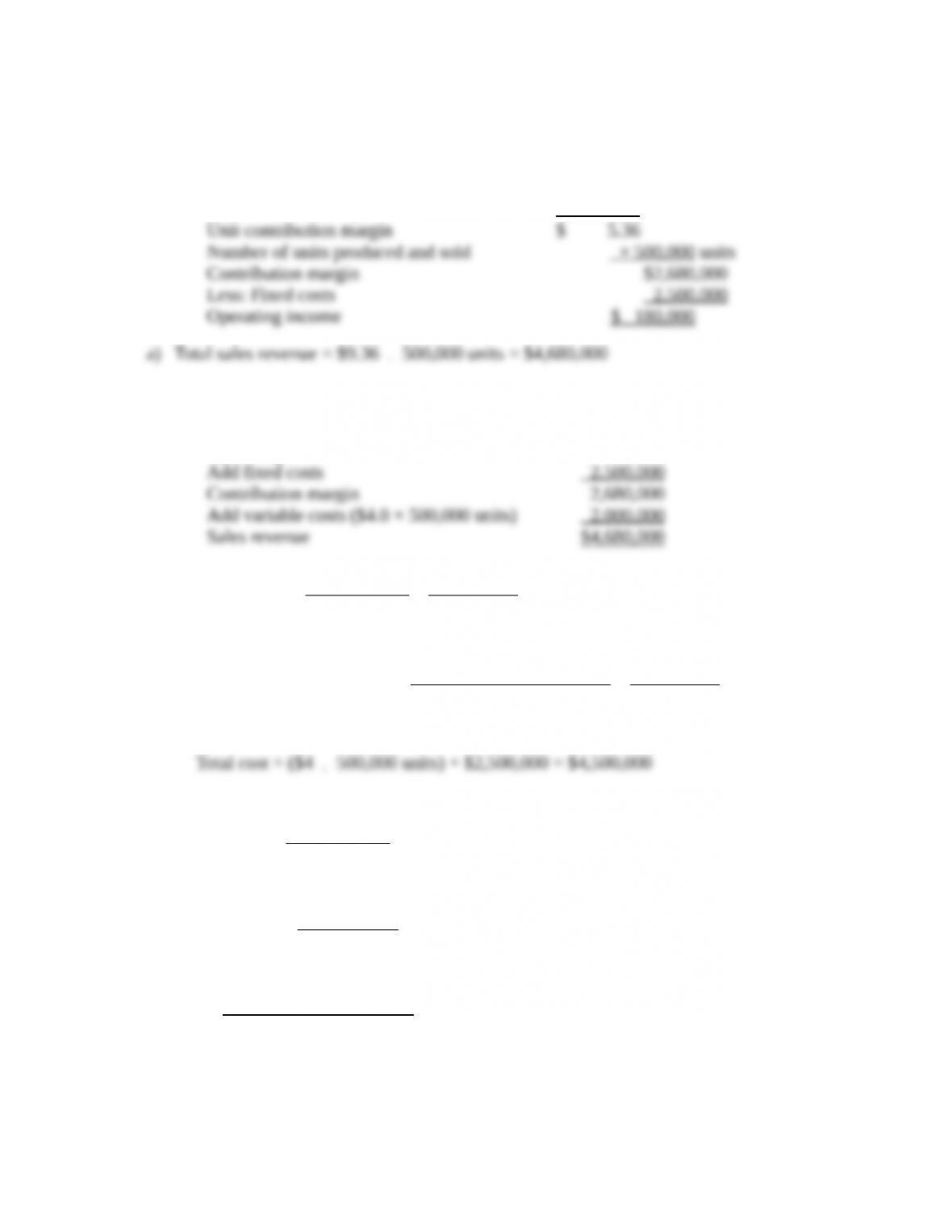

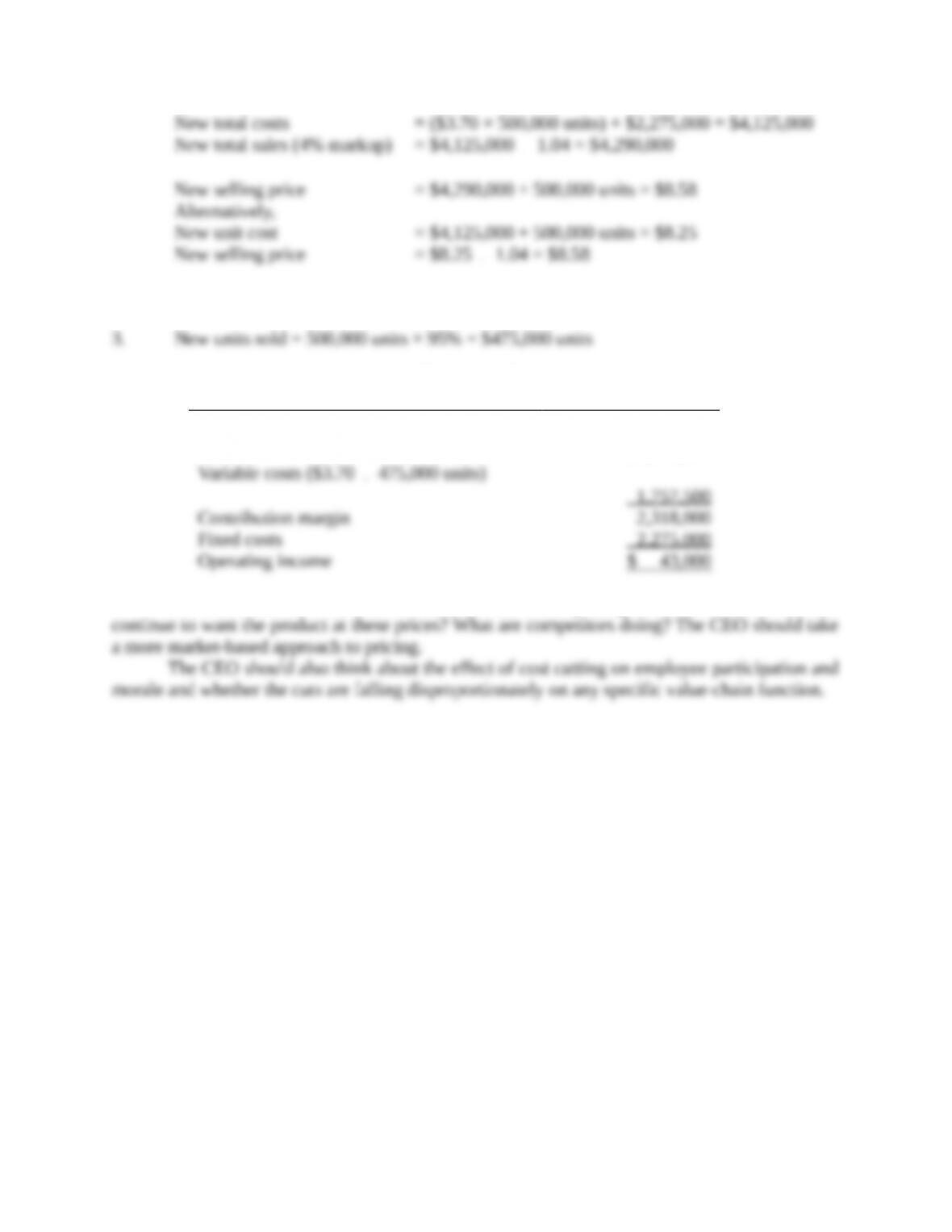

3.

New units sold = 500,000 units × 95% = $475,000 units

Budgeted Operating Income

for the Year Ending December 31, 20xx

Revenues ($8.58

475,000 units)

$4,075,500

Variable costs ($3.70

475,000 units)

1,757,500

Contribution margin

2,318,000

Fixed costs

2,275,000

Operating income

$ 43,000

4. The CEO has not considered customers in these pricing decisions. Will customers continue

to want the product at these prices? What are competitors doing? The CEO should take a more

market-based approach to pricing.

The CEO should also think about the effect of cost cutting on employee participation and

morale and whether the cuts are falling disproportionately on any specific value-chain function.

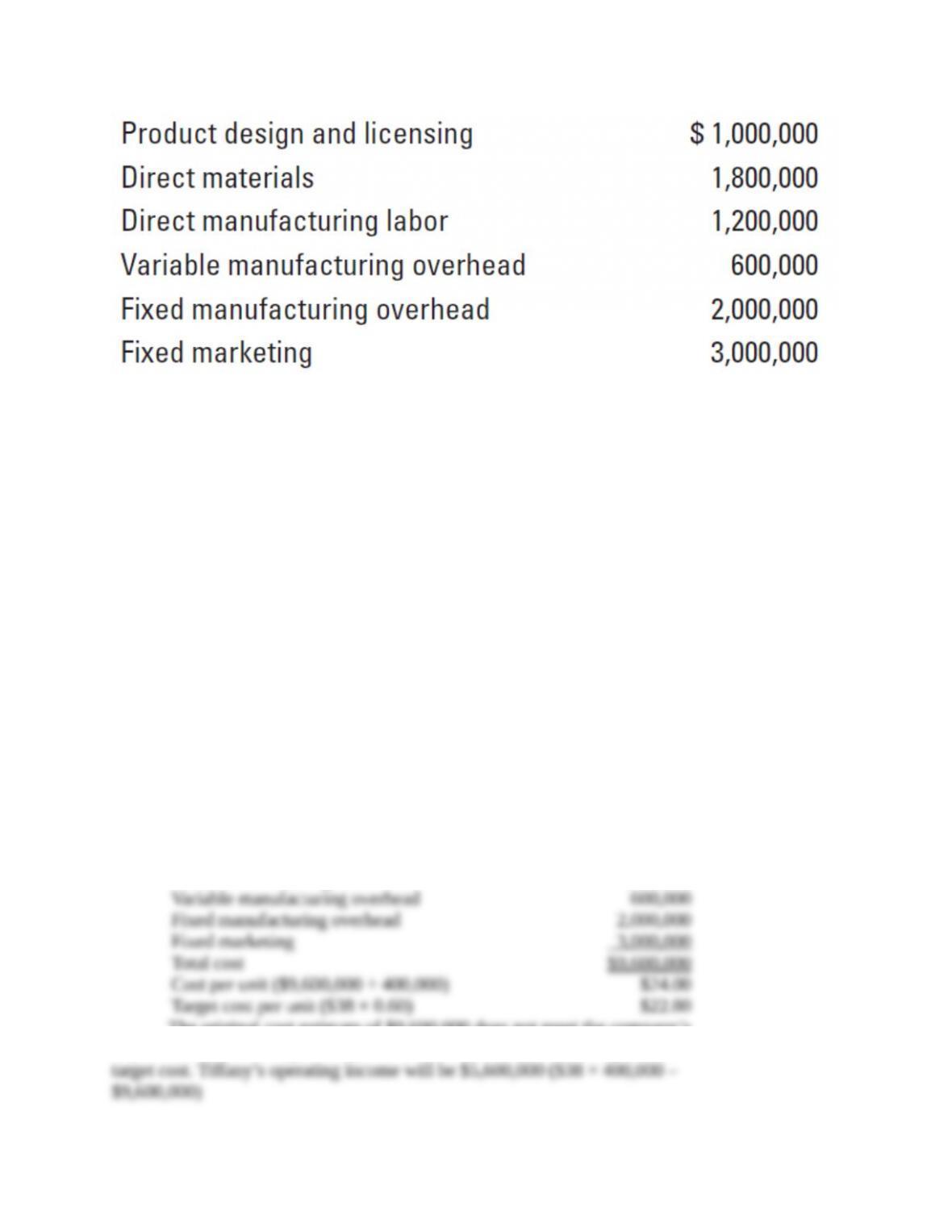

13-26 (30 min.) Value engineering, target pricing, and target costs.

Tiffany Cosmetics manufactures, and sells a variety of makeup and beauty products. The company

has come up with its own patented formula for a new anti-aging cream The company president

wants to make sure the product is priced competitively because its purchase will also likely

increase sales of other products. The company anticipates that it will sell 400,000 units of the

product in the first year with the following estimated costs:

Required:

1. The company believes that it can successfully sell the product for $38 a bottle. The company’s

target operating income is 40% of revenue. Calculate the target full cost of producing the

400,000 units. Does the cost estimate meet the company’s requirements? Is value engineering

needed?

2. A component of the direct materials cost requires the nectar of a specific plant in South

America. If the company could eliminate this special ingredient, the materials cost would drop

Weekly costs:

Ticket sales

Online ticket sales: 55,000 15% $1

$ 8,250

On-site sales: 55,000 85% $2

93,500

Ticket verification: 55,000 $1.50

82,500

Operating attractions: 11,340a runs $90.00

1,020,600

Litter patrol: 1,750b 20

35,000

Total weekly costs

$1,239,850

Cost per patron: $1,239,850 ÷ 55,000

$22.54

Operating profit: ($1,925,000 – $1,239,850)

$ 685,150

a6 runs per hour 10 hours per day 7 days per week 27 attractions = 11,340 runs per week

b(25 acres ÷ 1 acre per hour) 10 hours per day 7 days per week = 1,750 litter patrol hours

Lagoon does achieve its target profit of 35% of revenues.

2.

Weekly Revenue:

55,000 patrons $33

$1,815,000

Weekly costs

Ticket sales:

Online ticket sales: 55,000 40% $0.75 + $1,000

17,500

On-site sales: 55,000 60% $2

66,000

Ticket verification: 55,000 1.50

82,500

Operating attractions: 10,332a runs $90

929,880

Litter patrol: 1,400b $20 + $250

28,250

Total weekly costs

1,124,130

Operating profit

$ 690,870

a6 runs per hour 10 hours per day 7 days per week 19 attractions +

6 runs per hour 7 hours per day 7 days per week 8 attractions = 10,332 runs per week

b(25 acres ÷ 1.25 acres per hour) 10 hours per day 7 days per week = 1,400 litter patrol hours

This profit is slightly greater than Lagoon’s current profitability.

Yes, the changes and improvements will allow Lagoon to maintain its desired profit margin of

35% ($690,870 ÷ $1,815,000 = 38%).

3. The challenges that Lagoon might encounter in achieving the target cost are mostly

employee related. If the employees resist the changes, or struggle with the implementation of the

improvements, the target cost will be in danger of not being met. Lagoon might counter these

struggles by training employees to implement these changes successfully and by adapting its

incentive program to reward the desired improvements.