1) Post-investment audits prevent managers from overstating the expected cash inflows

from projects and accepting projects they should reject.

2) Activity-based budgeting would permit the use of multiple drivers and multiple cost

pools in the budgeting process.

3) From an accounting standpoint, favorable cost variances are debit entries, while

unfavorable ones are credits.

4) When actual indirect costs exceed allocated indirect costs, indirect costs have been

underapplied.

5) Discounted cash flow methods focus on operating income.

6) In multiproduct situations when sales mix shifts toward the product with the highest

contribution margin, operating income will be higher.

7) One criticism of team-based compensation is that it diminishes the incentives of

individual employees, which can harm a firm’s overall performance.

8) When using variance analysis for performance evaluation, managers often focus on

effectiveness and efficiency as two of the common attributes used in comparing

expected results with actual results.

9) Dual pricing insulates managers from the realities of the marketplace because costs,

not market prices, affect the revenues of the supplying division.

10) If a cost pool is homogeneous, the cost allocations using that pool will be the same

as they would be if costs of each individual activity in that pool were allocated

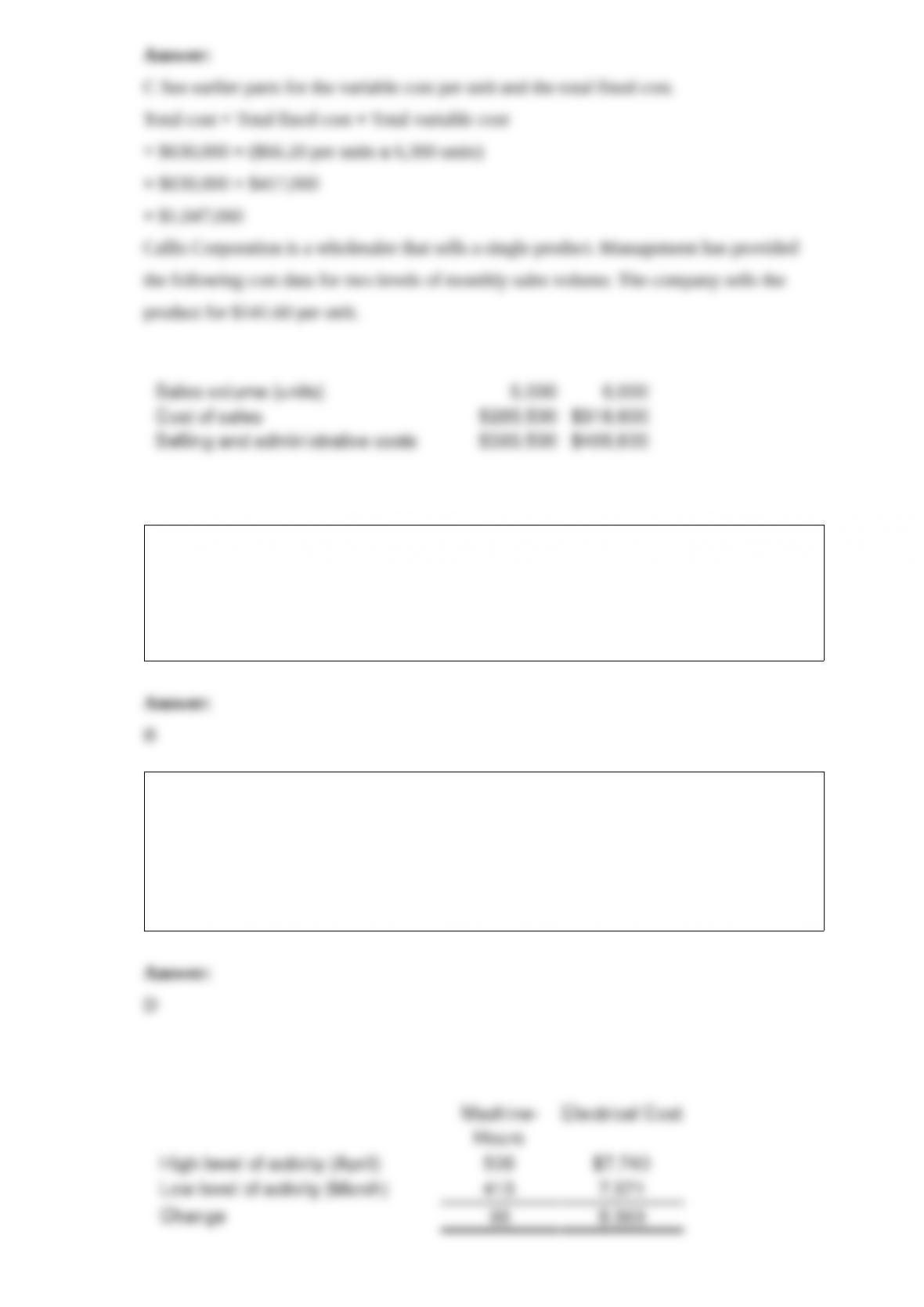

separately.

11) Prorated allocation of production-volume variance results in a higher operating

income for current year than if the entire favorable production-volume variance were

credited to Cost of Goods Sold.

12) Higher selling prices, rather than unique products or services, provide a competitive

advantage for the cost leader companies.

13) When using a control chart, the observations outside the upper and lower control

limits are ordinarily regarded as nonrandom and worth investigating.

14) Management accounting information and reports do not have to follow set

principles or rules such as GAAP.

15) Which of the following best describes a rolling budget?

A) It is a budget that outlines the amount required to roll over debt in a future period.

B) It is a budget that is always available for a specified future time period.

C) It is a budget that outlines budgeted expenses.

D) It is a budget that is submitted to a bank at the beginning of every month as per a

loan covenant.

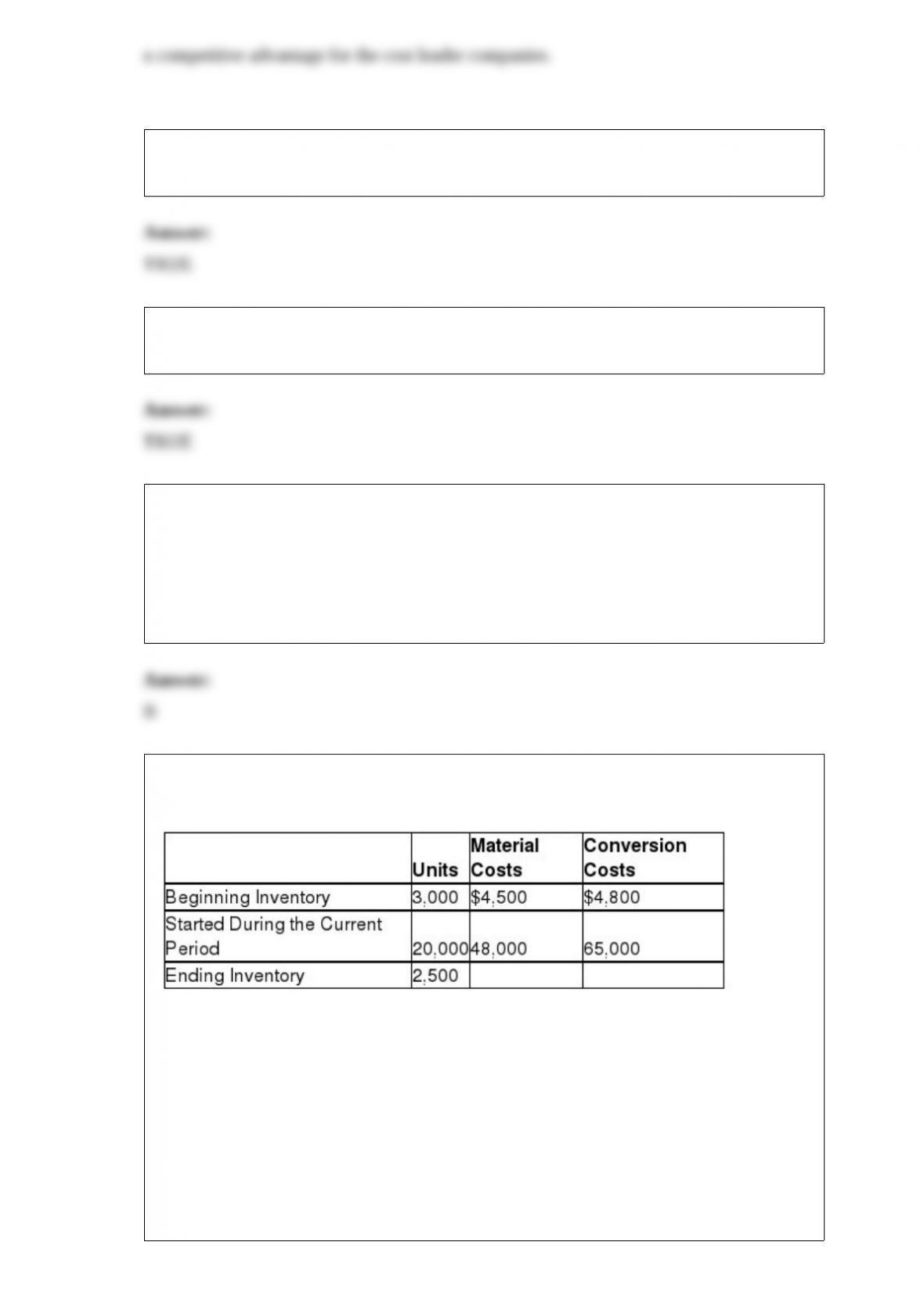

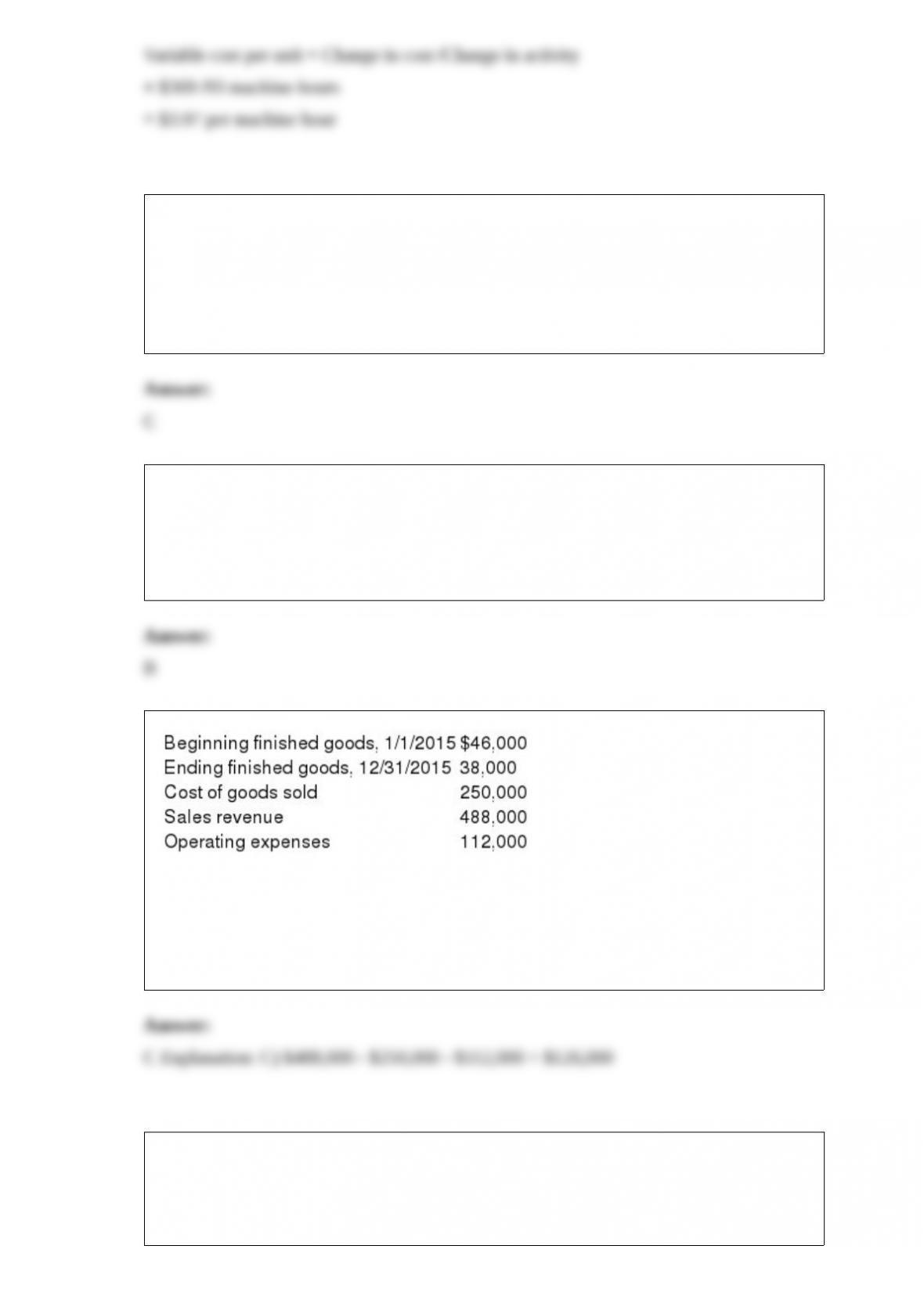

16) FIFO Aluminum processes a single type of aluminum. During the current period the

following information was given:

All materials are added at the beginning of the production process. The beginning

inventory was 30% complete as to conversion, while the ending inventory was 40%

completed for conversion purposes.

FIFO Aluminum uses the first-in, first-out system of process costing.

What were the costs assigned to the units transferred out this period (round equivalent

unit cost to the nearest penny)?

A) $113,160

B) $113,236

C) $113,980

D) $122,300

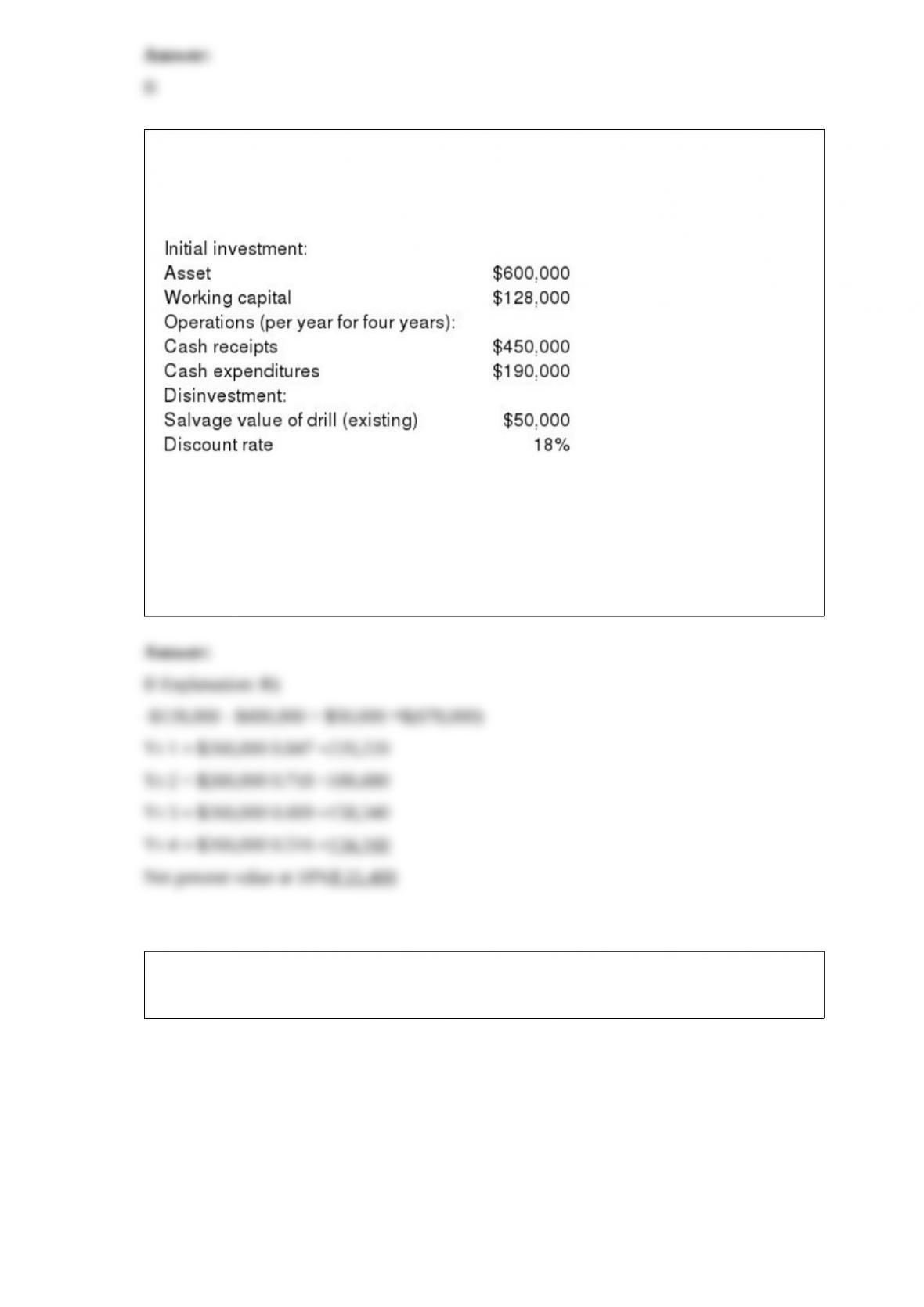

17) Forise Water Company drills small commercial water wells. The company is in the

process of analyzing the purchase of a new drill. Information on the proposal is

provided below.

What is the net present value of the investment? Assume there is no recovery of

working capital.

A) $(124,280)

B) $21,400

C) $82,724

D) $149,400

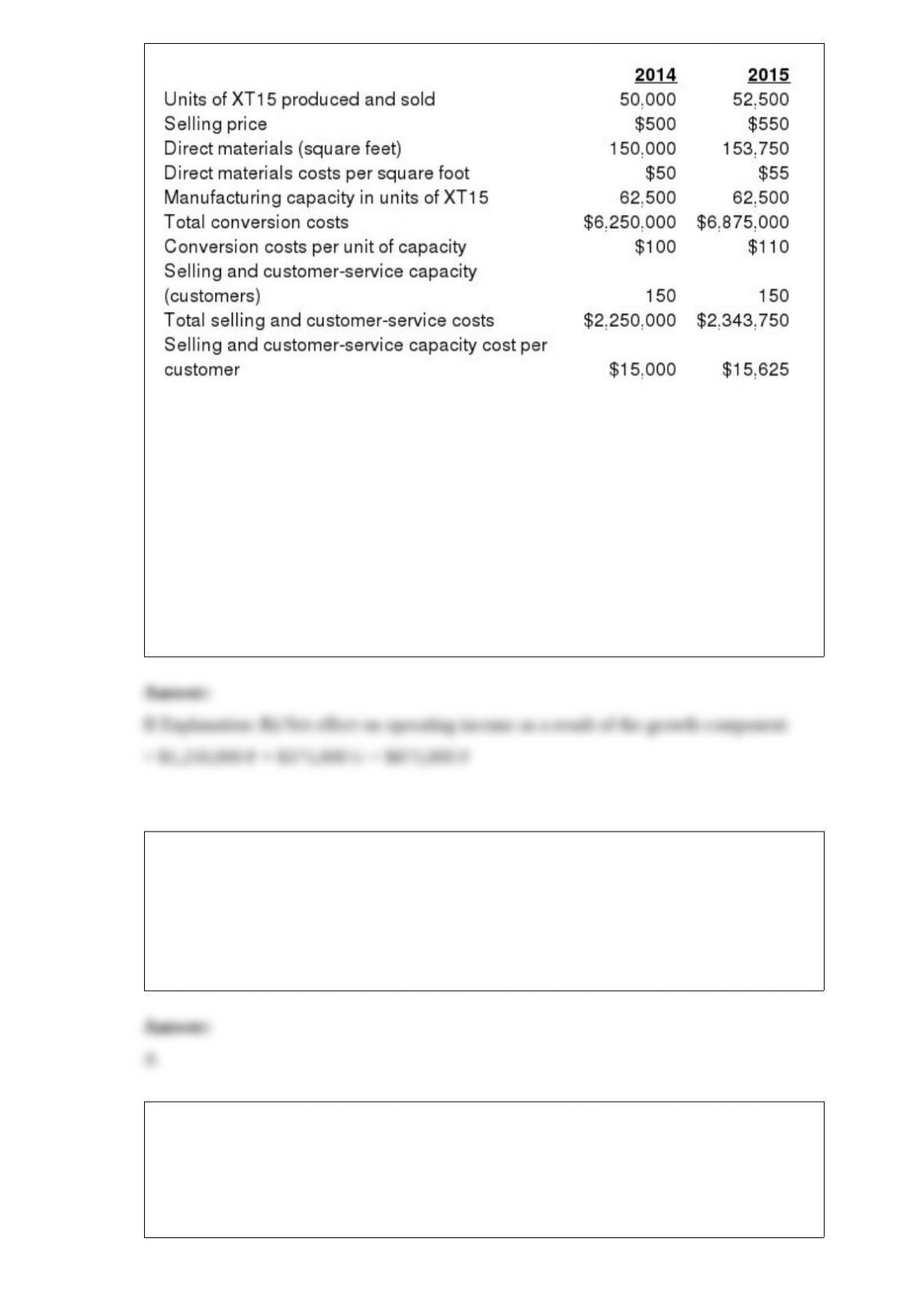

18) Following a strategy of product differentiation, Arseniq Company makes a high-end

Appliance, XT15. Arseniq presents the following data for the years 2014 and 2015:

Arseniq produces no defective units but it wants to reduce direct materials usage per

unit of XT15. Manufacturing conversion costs in each year depend on production

capacity defined in terms of XT15 units that can be produced. Selling and

customer-service costs depend on the number of customers that the customer and

service functions are designed to support. Arseniq had 140 customers in 2014 and 145

customers in 2015.

What is the net effect on operating income as a result of the growth component?

A) $1,118,750 F

B) $875,000 F

C) $875,000 U

D) $1,118,750 U

19) Variance analysis should be used ________.

A) to understand why variances arise and to improve future performance

B) as the sole source of information for performance evaluation

C) to punish employees that do not meet standards

D) to set the standards which are very easy to achieve to encourage employees to focus

on meeting standards

20) The best estimate of the total cost to manufacture 6,300 units is closest to:

A) $984,060

B) $1,031,310

C) $1,047,060

D) $1,078,560

21) The advantage of using practical capacity to allocate costs ________.

A) is that it allows a downward supply spiral to develop

B) is that it focuses management’s attention on managing unused capacity

C) is that budgets are much easier to develop

D) is that it results in departments bearing a lower percentage of fixed costs

22) Using the high-low method, the estimate of the variable component of electrical

cost per machine-hour is closest to:

A) $0.12

B) $20.38

C) $7.98

D) $3.97

23) Service companies, in particular, find great value from ABC because a vast majority

of their cost structure is composed of ________ costs.

A) prime

B) factory

C) indirect

D) committed

24) Customer revenues and ________ are the determinants of customer profitability.

A) customer profile

B) customer costs

C) customer location

D) customer industry

25) What is operating income for 2015?

A) $116,000

B) $137,000

C) $126,000

D) $144,000

26) Contract disputes regarding cost allocation can be reduced by defining ________.

A) the material items allowed for production

B) the terms used, such as what constitutes direct labor

C) permissible tax deductions

D) minimum profit level the company should earn

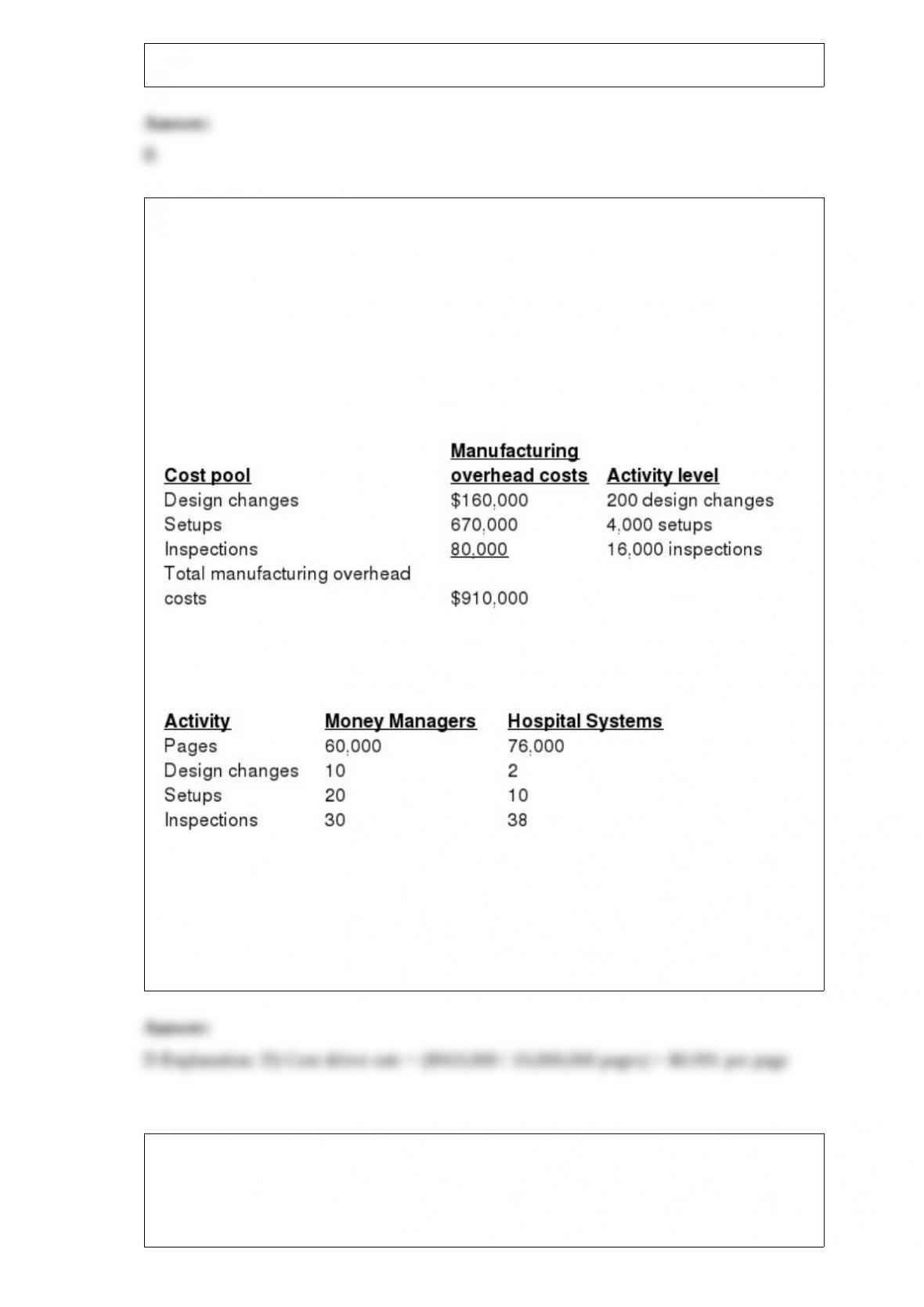

27) Xylon Corp. has contracts to complete weekly supplements required by forty-six

customers. For the year 2015, manufacturing overhead cost estimates total $840,000 for

an annual production capacity of 10 million pages.

For 2015, Xylon decided to evaluate the use of additional cost pools. After analyzing

manufacturing overhead costs, it was determined that number of design changes,

setups, and inspections are the primary manufacturing overhead cost drivers. The

following information was gathered during the analysis:

During 2015, two customers, Money Managers and Hospital Systems, are expected to

use the following printing services:

If manufacturing overhead costs are considered one large cost pool and are assigned

based on 10 million pages of production capacity, what is the cost driver rate?

A) $0.750 per page

B) $0.240 per page

C) $0.670 per page

D) $0.091 per page

28) The list of representative cost drivers in the right column below are randomized

with respect to the list of functions in the left column. That is, they do not match.

Function Representative Cost Driver

1. Purchasing A. Number of employees

2. Billing B. Number of shipments

3. Shipping C. Number of customers

4. Computer Support D. Number of invoices

5. Personnel E. Number of desktop computers

6. Customer Service F. Number of purchase orders

Required:

Match each business function with its representative cost driver.

29) In making the decision to buy the model 230 machine rather than the model 380

machine, the differential cost was:

A) $71,000

B) $59,000

C) $12,000

D) $39,000

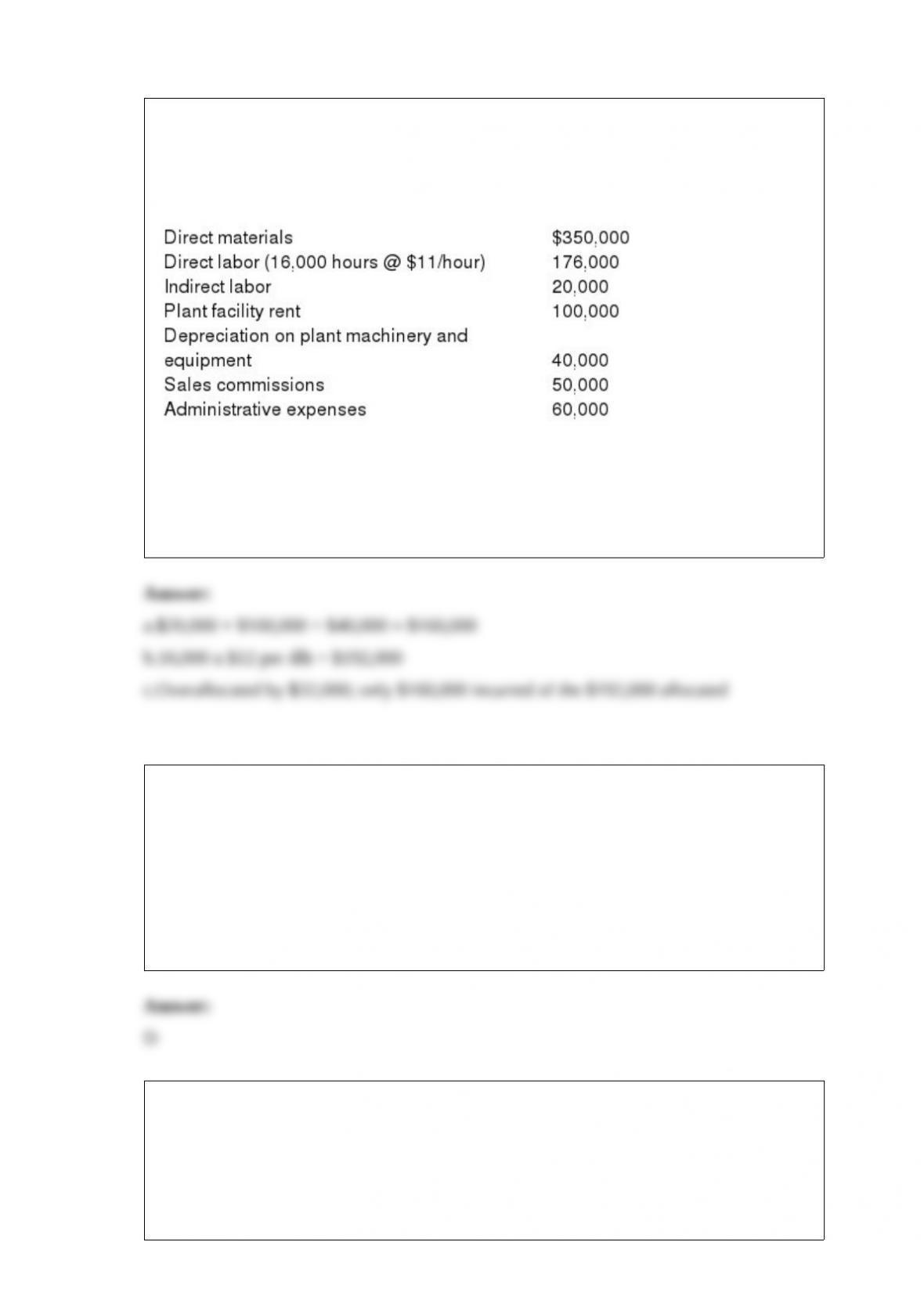

30) Plastic Products Company manufactures pipes and applies manufacturing costs to

production at a budgeted indirect-cost rate of $12 per direct labor-hour. The following

data are obtained from the accounting records for June 2014:

Required:

a.What actual amount of manufacturing overhead costs was incurred during June 2014?

b.What amount of manufacturing overhead was allocated to all jobs during June 2014?

c.For June 2014, was manufacturing overhead underallocated or overallocated?

Explain.

31) When using the high-low method, the numerator of the equation that determines the

slope is the ________.

A) difference between the positive and negative values of dependent and independent

variables

B) difference between the fixed cost and variable cost associated with the cost driver

C) difference between the high and low observations of the cost driver

D) difference between the costs associated with highest and lowest observations of the

cost driver

32) The sales-mix variance is calculated by ________.

A) deducting budgeted contribution margin based on actual units at budgeted mix from

budgeted contribution margin based on actual units sold at the actual mix

B) deducting budgeted contribution margin based on budgeted units at actual mix from

budgeted contribution margin based on actual units sold at the budgeted mix

C) deducting budgeted contribution margin based on actual units at actual mix from

budgeted contribution margin based on budgeted units sold at the budgeted mix

D) deducting budgeted contribution margin based on actual units at actual mix from

budgeted contribution margin based on actual units sold at the actual mix