8-

1

CHAPTER 8

FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND

MANAGEMENT CONTROL

8-1 Effective planning of variable overhead costs involves:

1. Planning to undertake only those variable overhead activities that add value for

customers using the product or service, and

2. Planning to use the drivers of costs in those activities in the most efficient way.

8-2 At the start of an accounting period, a larger percentage of fixed overhead costs are locked–

in than is the case with variable overhead costs. When planning fixed overhead costs, a company

must choose the appropriate level of capacity or investment that will benefit the company over a

long time. This is a strategic decision.

8-3 The key differences are how direct costs are traced to a cost object and how indirect costs

are allocated to a cost object:

Actual Costing

Standard Costing

Direct costs

Actual prices

× Actual inputs used

Standard prices

× Standard inputs allowed for actual output

Indirect costs

Actual indirect rate

× Actual inputs used

Standard indirect cost-allocation rate

× Standard quantity of cost-allocation base

allowed for actual output

8-4 Steps in developing a budgeted variable-overhead cost rate are

1. Choose the period to be used for the budget.

2. Select the cost-allocation bases to use in allocating variable overhead costs to the

output produced.

3. Identify the variable overhead costs associated with each cost-allocation base.

4. Compute the rate per unit of each cost-allocation base used to allocate variable

overhead costs to output produced.

8-5 Two factors affect the spending variance for variable manufacturing overhead:

a. price changes of individual inputs (such as energy and indirect materials) included in

variable overhead relative to budgeted prices

b. percentage change in the actual quantity used of individual items included in variable

overhead cost pool, relative to the percentage change in the quantity of the cost driver

of the variable overhead cost pool

8-6 Possible reasons for a favorable variable-overhead efficiency variance include:

• Workers are more skillful in using machines than budgeted.

• Production scheduler was able to schedule jobs better than budgeted, resulting in

lower-than-budgeted machine-hours.

• Machines operated with fewer slowdowns than budgeted.

• Machine time standards were overly lenient.

8-7 A direct materials efficiency variance indicates whether more or less direct materials were

used than was budgeted for the actual output achieved. A variable manufacturing overhead

efficiency variance indicates whether more or less of the chosen allocation base was used than was

budgeted for the actual output achieved.

8-8 Steps in developing a budgeted fixed-overhead rate are

1. Choose the period to use for the budget.

2. Select the cost-allocation base to use in allocating fixed overhead costs to output

produced.

3. Identify the fixed-overhead costs associated with each cost-allocation base.

4. Compute the rate per unit of each cost-allocation base used to allocate fixed overhead

costs to output produced.

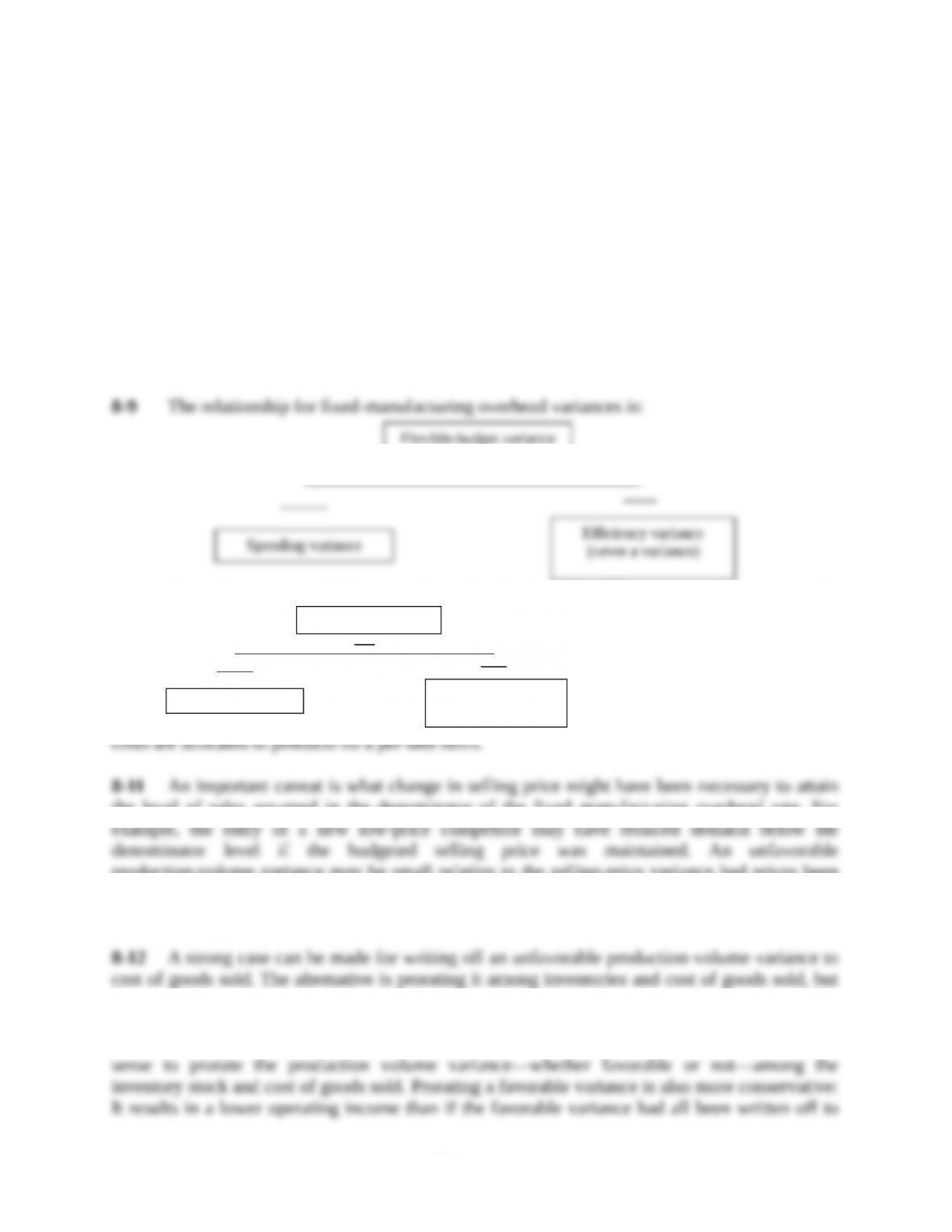

8-9 The relationship for fixed-manufacturing overhead variances is:

There is never an efficiency variance for fixed overhead because managers cannot be more

or less efficient in dealing with an amount that is fixed regardless of the output level. The result is

that the flexible-budget variance amount is the same as the spending variance for fixed–

manufacturing overhead.

8-10 For planning and control purposes, fixed overhead costs are a lump sum amount that is not

controlled on a per-unit basis. In contrast, for inventory costing purposes, fixed overhead costs are

allocated to products on a per-unit basis.

8-11 An important caveat is what change in selling price might have been necessary to attain

the level of sales assumed in the denominator of the fixed manufacturing overhead rate. For

example, the entry of a new low-price competitor may have reduced demand below the

denominator level if the budgeted selling price was maintained. An unfavorable production–

volume variance may be small relative to the selling-price variance had prices been dropped to

attain the denominator level of unit sales.

8-12 A strong case can be made for writing off an unfavorable production-volume variance to

cost of goods sold. The alternative is prorating it among inventories and cost of goods sold, but

this would “penalize” the units produced (and in inventory) for the cost of unused capacity, i.e.,

for the units not produced. But, if we take the view that the denominator level is a “soft” number—

i.e., it is only an estimate, and it is never expected to be reached exactly—then it makes more sense

to prorate the production volume variance—whether favorable or not—among the inventory stock

and cost of goods sold. Prorating a favorable variance is also more conservative: It results in a

Flexible-budget variance

Spending variance

Efficiency variance

(never a variance)

8-

3

lower operating income than if the favorable variance had all been written off to cost of goods

sold. Finally, prorating also dampens the efficacy of any steps taken by company management to

manage operating income through manipulation of the production volume variance. In sum, a

production-volume variance need not always be written off to cost of goods sold.

8-13 The four variances are

• Variable manufacturing overhead costs

− spending variance

− efficiency variance

• Fixed manufacturing overhead costs

− spending variance

− production-volume variance

8-14 Interdependencies among the variances could arise for the spending and efficiency

variances. For example, if the chosen allocation base for the variable overhead efficiency variance

is only one of several cost drivers, the variable overhead spending variance will include the effect

of the other cost drivers. As a second example, interdependencies can be induced when there are

misclassifications of costs as fixed when they are variable and vice versa.

8-15 Flexible-budget variance analysis can be used in the control of costs in an activity area by

isolating spending and efficiency variances at different levels in the cost hierarchy. For example,

an analysis of batch costs can show the price and efficiency variances from being able to use longer

production runs in each batch relative to the batch size assumed in the flexible budget.

8-16 (20 min.) Variable manufacturing overhead, variance analysis.

Esquire Clothing is a manufacturer of designer suits. The cost of each suit is the sum of three

variable costs (direct material costs, direct manufacturing labor costs, and manufacturing overhead

costs) and one fixed-cost category (manufacturing overhead costs). Variable manufacturing

overhead cost is allocated to each suit on the basis of budgeted direct manufacturing labor-hours

per suit. For June 2014, each suit is budgeted to take 4 labor-hours. Budgeted variable

manufacturing overhead cost per labor-hour is $12. The budgeted number of suits to be

manufactured in June 2014 is 1,040.

Actual variable manufacturing costs in June 2014 were $52,164 for 1,080 suits started and

completed. There were no beginning or ending inventories of suits. Actual direct manufacturing

labor-hours for June were 4,536.

Required:

1. Compute the flexible-budget variance, the spending variance, and the efficiency variance for

variable manufacturing overhead.

2. Comment on the results.

SOLUTION

1. Variable Manufacturing Overhead Variance Analysis for Esquire Clothing for June 2014

Actual Costs

Incurred

Actual Input Qty.

× Actual Rate

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(4,536 × $11.50)

$52,164

(4,536 × $12)

$54,432

(4 × 1,080 × $12)

$51,840

(4 × 1,080 × $12)

$51,840

2. Esquire had a favorable spending variance of $2,268 because the actual variable overhead

rate was $11.50 per direct manufacturing labor-hour versus $12 budgeted. It had an unfavorable

efficiency variance of $2,592 U because each suit averaged 4.2 labor-hours (4,536 hours ÷ 1,080

suits) versus 4.0 budgeted labor-hours.

8-17 (20 min.) Fixed-manufacturing overhead, variance analysis (continuation of 8-16).

Esquire Clothing allocates fixed manufacturing overhead to each suit using budgeted direct

manufacturing labor-hours per suit. Data pertaining to fixed manufacturing overhead costs for June

2014 are budgeted, $62,400, and actual, $63,916.

Required:

1. Compute the spending variance for fixed manufacturing overhead. Comment on the results.

2. Compute the production-volume variance for June 2014. What inferences can Esquire Clothing

draw from this variance?

SOLUTION

1 & 2.

Budgeted fixed overhead

rate per unit of

allocation base

=

4040,1

400,62$

=

160,4

400,62$

= $15 per hour

Fixed Manufacturing Overhead Variance Analysis for Esquire Clothing for June 2014

$2,268 F

Spending variance

$2,592 U

Efficiency variance

Never a variance

$324 U

Flexible-budget variance

Never a variance

8-

5

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for Actual

Output

× Budgeted Rate

(4)

$63,916

$62,400

$62,400

(4 × 1,080 × $15)

$64,800

$1,516 U $2,400 F

Spending variance Never a variance Production-volume variance

$1,516 U $2,400 F

Flexible-budget variance Production-volume variance

The fixed manufacturing overhead spending variance and the fixed manufacturing flexible

budget variance are the same––$1,516 U. Esquire spent $1,516 more than the $62,400 budgeted

amount for June 2014.

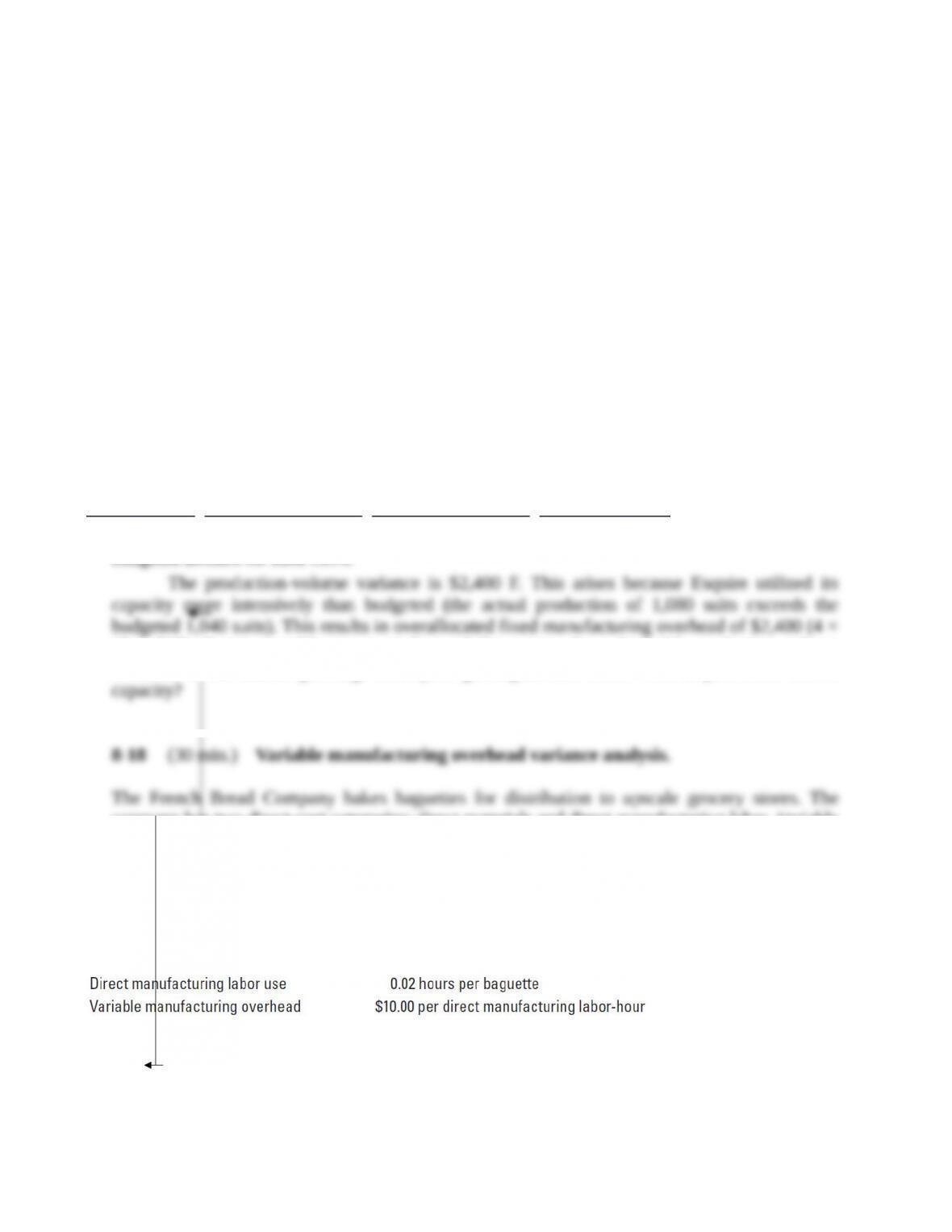

The production-volume variance is $2,400 F. This arises because Esquire utilized its

capacity more intensively than budgeted (the actual production of 1,080 suits exceeds the budgeted

1,040 suits). This results in overallocated fixed manufacturing overhead of $2,400 (4 × 40 × $15).

Esquire would want to understand the reasons for a favorable production-volume variance. Is the

market growing? Is Esquire gaining market share? Will Esquire need to add capacity?

8-18 (30 min.) Variable manufacturing overhead variance analysis.

The French Bread Company bakes baguettes for distribution to upscale grocery stores. The

company has two direct-cost categories: direct materials and direct manufacturing labor. Variable

manufacturing overhead is allocated to products on the basis of standard direct manufacturing

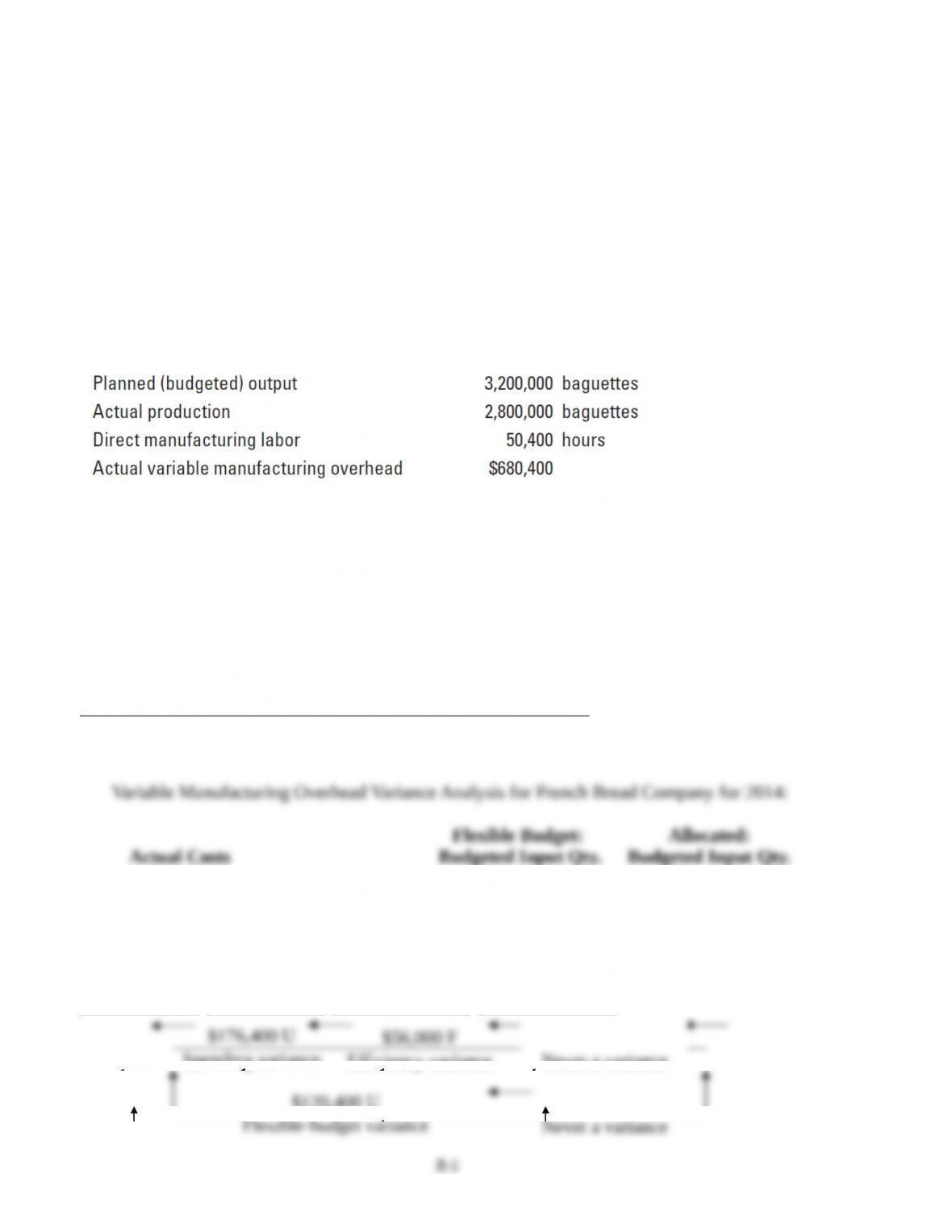

labor-hours. Following is some budget data for the French Bread Company:

The French Bread Company provides the following additional data for the year ended December

31, 2014:

Required:

1. What is the denominator level used for allocating variable manufacturing overhead? (That is,

for how many direct manufacturing labor-hours is French Bread budgeting?)

2. Prepare a variance analysis of variable manufacturing overhead. Use Exhibit 8-4 (page 304)

for reference.

3. Discuss the variances you have calculated and give possible explanations for them.

SOLUTION

1. Denominator level = (3,200,000 × 0.02 hours) = 64,000 hours

2.

Actual

Results

Flexible

Budget Amounts

1. Output units (baguettes)

2,800,000

2,800,000

2. Direct manufacturing labor-hours

50,400

56,000a

3. Labor-hours per output unit (2 1)

0.018

0.020

4. Variable manuf. overhead (MOH) costs

$680,400

$560,000

5. Variable MOH per labor-hour (4 2)

$13.50

$10

6. Variable MOH per output unit (4 1)

$0.243

$0.200

a2,800,000

0.020 = 56,000 hours

Variable Manufacturing Overhead Variance Analysis for French Bread Company for 2014:

Actual Costs

Incurred

Actual Input Qty.

× Actual Rate

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(50,400 × $13.50)

$680,400

(50,400 × $10)

$504,000

(56,000 × $10)

$560,000

(56,000 × $10)

$560,000

3. Spending variance of $176,400 U. It is unfavorable because variable manufacturing

overhead was 35 percent higher than planned. A possible explanation could be an increase in

energy rates relative to the rate per standard labor-hour assumed in the flexible budget.

Efficiency variance of $56,000 F. It is favorable because the actual number of direct

manufacturing labor-hours required was lower than the number of hours in the flexible budget.

$176,400 U

Spending variance

$56,000 F

Efficiency variance

Never a variance

$120,400 U

Flexible-budget variance

Never a variance

8-

7

Labor was more efficient in producing the baguettes than management had anticipated in the

budget. This could occur because of improved morale in the company, which could result from an

increase in wages or an improvement in the compensation scheme.

Flexible-budget variance of $120,400 U. It is unfavorable because the favorable efficiency

variance was not large enough to compensate for the large unfavorable spending variance.

8-19 (30 min.) Fixed manufacturing overhead variance analysis (continuation of 8-18).

The French Bread Company also allocates fixed manufacturing overhead to products on the basis

of standard direct manufacturing labor-hours. For 2014, fixed manufacturing overhead was

budgeted at $4.00 per direct manufacturing labor-hour. Actual fixed manufacturing overhead

incurred during the year was $272,000.

Required:

1. Prepare a variance analysis of fixed manufacturing overhead cost. Use Exhibit 8-4 (page 304)

as a guide.

2. Is fixed overhead underallocated or overallocated? By what amount?

3. Comment on your results. Discuss the variances and explain what may be driving them.

SOLUTION

1. Budgeted standard direct manufacturing labor used = 0.02 per baguette

Budgeted output = 3,200,000 baguettes

Budgeted standard direct manufacturing labor-hours

= 3,200,000 × 0.02

= 64,000 hours

Budgeted fixed manufacturing overhead costs

= 64,000 × $4.00 per hour

= $256,000

Actual output = 2,800,000 baguettes

Allocated fixed manufacturing overhead

= 2,800,000 × 0.02 × $4

= $224,000

Fixed Manufacturing Overhead Variance Analysis for French Bread Company for 2014

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

$272,000

$256,000

$256,000

(2,800,000 × 0.02 × $4)

$224,000

2. The fixed manufacturing overhead is underallocated by $48,000.

3. The production-volume variance of $32,000 U captures the difference between the budgeted

3,200,0000 baguettes and the lower actual 2,800,000 baguettes produced—the fixed cost

capacity not used. The spending variance of $16,000 U means that the actual aggregate of

fixed costs ($272,000) exceeds the budget amount ($256,000). For example, monthly leasing

rates for baguette-making machines may have increased above those in the budget for 2014.

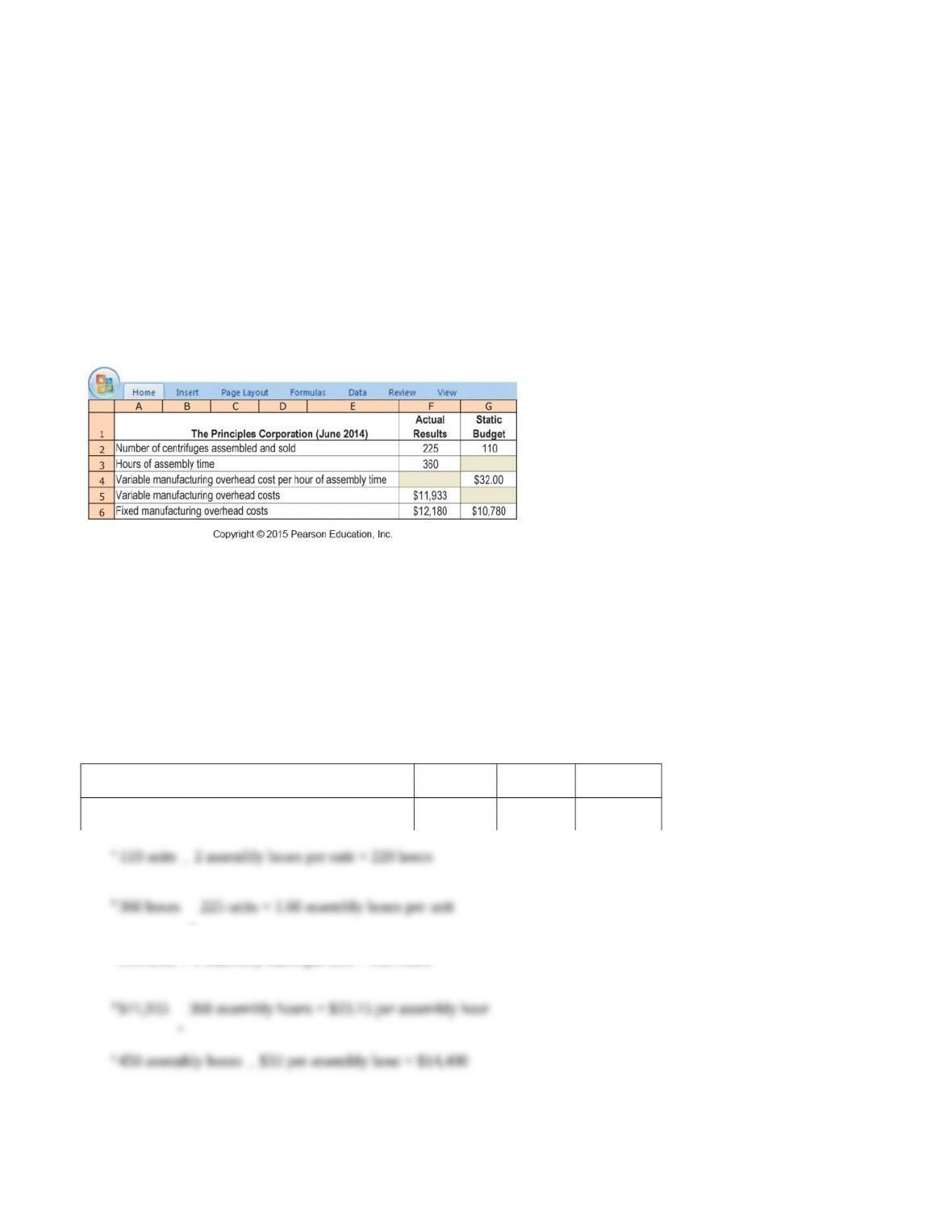

8-20 (30–40 min.) Manufacturing overhead, variance analysis.

The Principles Corporation is a manufacturer of centrifuges. Fixed and variable manufacturing

overheads are allocated to each centrifuge using budgeted assembly–hours. Budgeted assembly

time is 2 hours per unit. The following table shows the budgeted amounts and actual results related

to overhead for June 2014.

Required:

$16,000 U

Spending variance

Never a variance

$32,000 U

Production-volume

variance

$16,000 U

Flexible-budget variance

$32,000 U

Production-volume

variance

$48,000 U

Underallocated fixed overhead

(Total fixed overhead variance)

8-

9

1. Prepare an analysis of all variable manufacturing overhead and fixed manufacturing overhead

variances using the columnar approach in Exhibit 8-4 (page 304).

2. Prepare journal entries for Principles’ June 2014 variable and fixed manufacturing overhead

costs and variances; write off these variances to cost of goods sold for the quarter ending June

30, 2014.

3. How does the planning and control of variable manufacturing overhead costs differ from the

planning and control of fixed manufacturing overhead costs?

SOLUTION

1. The summary information is:

The Principles Corporation (June 2014)

Actual

Flexible

Budget

Static

Budget

Outputs units (number of assembled units)

225

225

110

Hours of assembly time

360

450

220a

Assembly hours per unit

1.60b

2.00

2.00

Variable mfg. overhead cost per hour of assembly time

$ 33.15d

$ 32.00

$ 32.00

Variable mfg. overhead costs

$11,933

$14,400e

$ 7,040f

Fixed mfg. overhead costs

$12,180

$10,780

$10,780

Fixed mfg. overhead costs per hour of assembly time

$ 33.83g

$ 49.00h

a 110 units

2 assembly hours per unit = 220 hours

b 360 hours

225 units = 1.60 assembly hours per unit

c 225 units

2 assembly hours per unit = 450 hours

d $11,933

360 assembly hours = $33.15 per assembly hour

e 450 assembly hours

$32 per assembly hour = $14,400

f 220 assembly hours

$32 per assembly hour = $7,040

g $12,180

360 assembly hours = $33.83 per assembly hour

h $10,780

220 assembly hours = $49 per assembly hour

8-

10

Flexible Budget:

Allocated:

Actual Costs

Actual Input Qty.

Budgeted Input

Qty. Allowed

Budgeted

Budgeted Input

Qty. Allowed

Budgeted

Incurred

Budgeted Rate

for Actual Output

Rate

for Actual Output

Rate

Variable

360

$32.00

450

$32.00

450

$32.00

Manufacturing

assy. hrs.

per assy. hr.

assy. hrs.

per assy. hr.

assy. hrs.

per assy. hr.

Overhead

$11,933

$11,520

$14,400

$14,400

$413 U $2,880 F

Spending variance Efficiency variance Never a variance

$2,467 F

Flexible-budget variance Never a variance

$2,467 F

Overallocated variable overhead

Flexible Budget:

Allocated:

Actual Costs

Static Budget Lump Sum

Static Budget Lump Sum

Budgeted Input

Allowed

Budgeted

Incurred

Regardless of Output Level

Regardless of Output Level

for Actual Output

Rate

Fixed

450

$49.00

Manufacturing

assy. hrs.

per assy. hr.

Overhead

$12,180

$10,780

$10,780

$22,050

$1,400 U $11,270 F

Spending Variance Never a Variance Production-volume variance

$1,400 U $11,270 F

Flexible-budget variance Production-volume variance

$9,870 F

Overallocated fixed overhead

8-

11

The summary analysis is:

Spending

Variance

Efficiency

Variance

Production-Volume

Variance

Variable

Manufacturing

Overhead

$413 U

$2,880 F

Never a variance

Fixed Manufacturing

Overhead

$1,400 U

Never a variance

$11,270 F

2. Variable Manufacturing Costs and Variances

a. Variable Manufacturing Overhead Control

11,933

Accounts Payable Control and various other accounts

11,933

To record actual variable manufacturing overhead costs

incurred.

b. Work–in–Process Control

14,400

Variable Manufacturing Overhead Allocated

14,400

To record variable manufacturing overhead allocated.

c. Variable Manufacturing Overhead Allocated

14,400

Variable Manufacturing Overhead Spending Variance

413

Variable Manufacturing Overhead Control

11,933

Variable Manufacturing Overhead Efficiency Variance

2,880

To isolate variances for the accounting period.

d. Variable Manufacturing Overhead Efficiency Variance

2,880

Variable Manufacturing Overhead Spending Variance

413

Cost of Goods Sold

2,467

To write off variable manufacturing overhead variances to cost of goods sold.