Units

in sales

Breakeven

overhead

manuf. Fixed

operating

Target

fixed Total

−

+

+

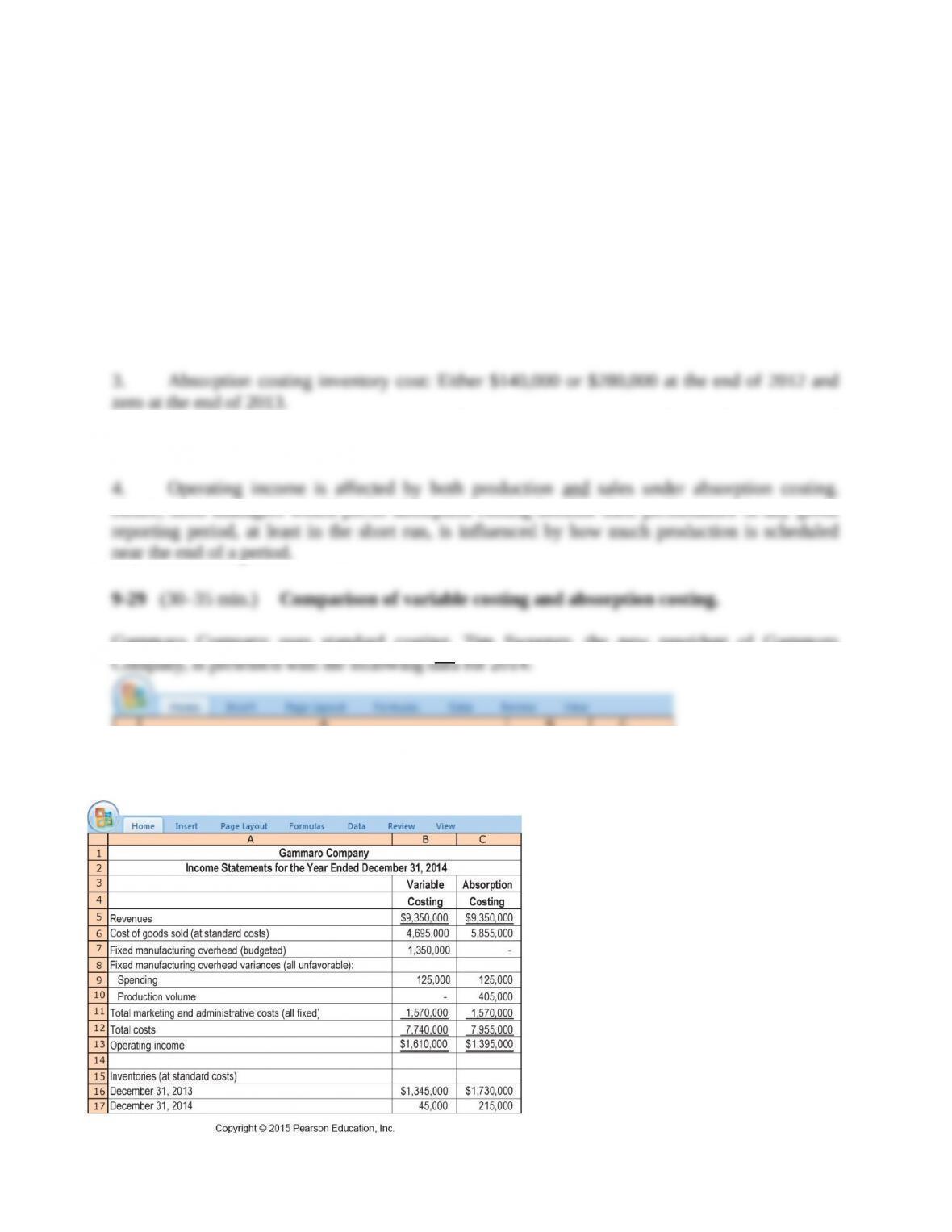

Absorpting

costing

operating

–

Variable

costing

operating

=

Fixed

manuf. costs in

ending

–

Fixed

manuf. costs in

beginning

26,000

Books

32,500

Books

33,800

Books

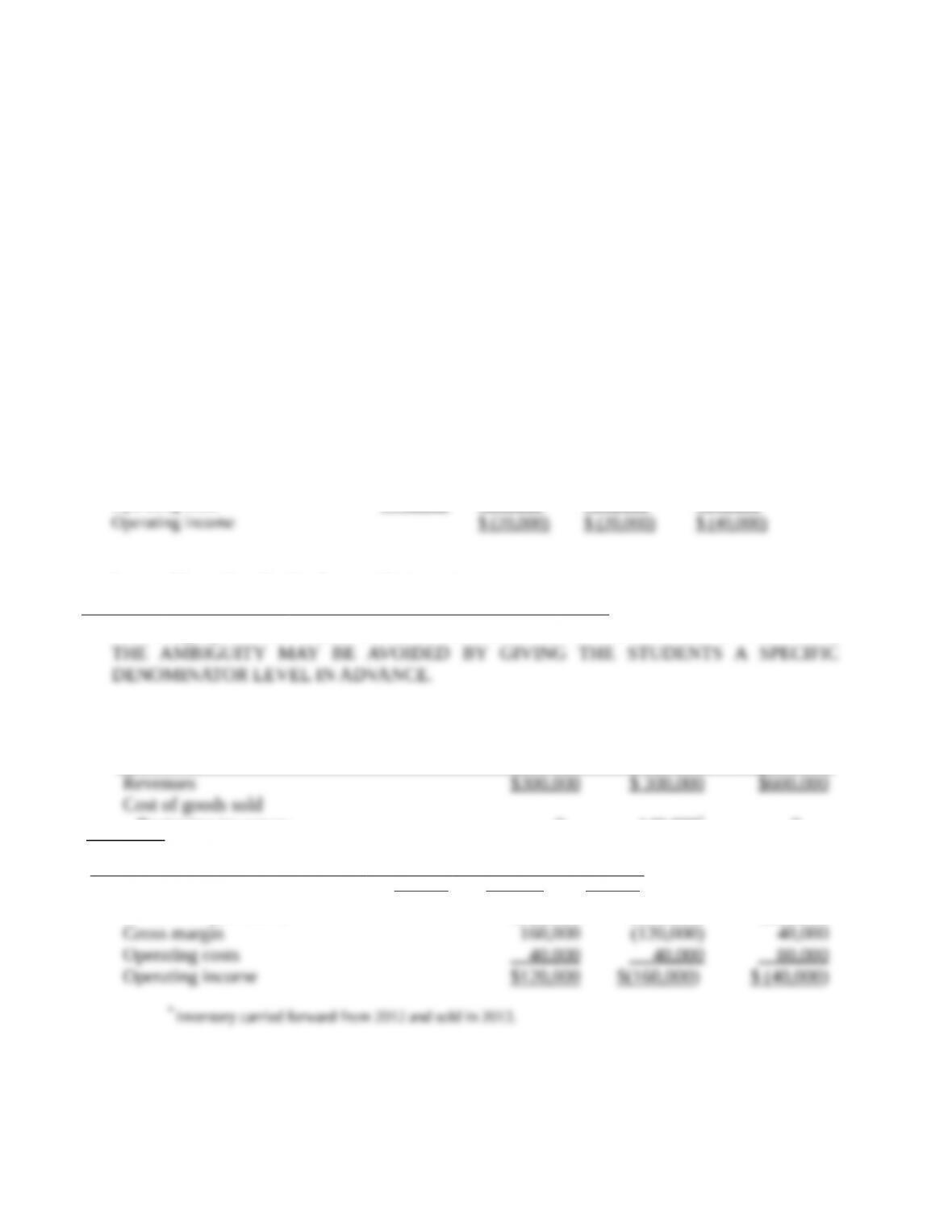

Gross margin $520,000 $624,000 $644,800

Less 10% Ending inventory 0 (19,825) (23,790)

Adjusted gross margin $520,000 $604,175 $621,010

While adjusting for ending inventory does to some degree mitigate the increase in inventory

associated with excess production, it may be difficult to mechanically compensate for all of the

increased income. In addition, it does nothing to hold the manager responsible for the poor

decisions from the organization’s standpoint.

3b.

26,000

Books

32,500

Books

33,800

Books

1) Inventory change:

End inventory ─ begin inventory 0 6,500 books 7,800 books

2) Excess production (%)

Production ÷ sales 26,000 ÷ 26,000 32,500 ÷ 26,000 33,800 ÷26,000

1.0 1.25 1.3

• A ratio of ending inventory to beginning inventory, as suggested in the book, is not

possible because beginning inventory was zero, so we substituted change in inventory

level.

For these nonfinancial measures to be useful they must be incorporated into the reward function

of the manager.

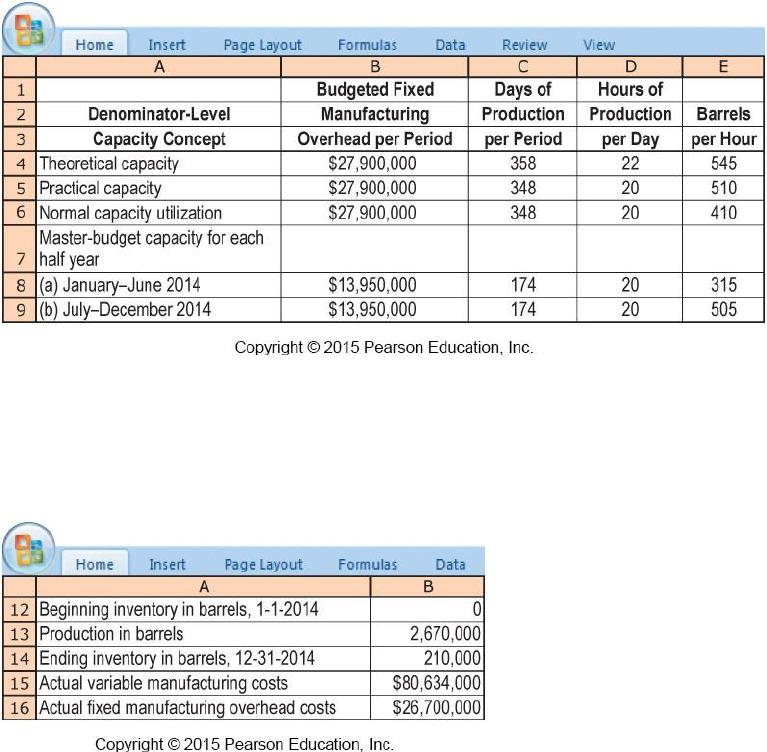

Theoretical capacity

$6.50

$30.20a

$36.70

$17,355,000

$9,345,000

U

Practical capacity

7.86

30.20

38.06

20,986,200

5,713,800

U

Normal capacity utilization

9.78

30.20

39.98

26,112,600

587,400

U

a $80,634,000

2,670,000 barre