21-1

CHAPTER 21

CAPITAL BUDGETING AND COST ANALYSIS

21-1 No. Capital budgeting focuses on an individual investment project throughout its life, recognizing the time value of money. The

life of a project is often longer than a year. Accrual accounting focuses on a particular accounting period, often a year, with an emphasis

on income determination.

21-2 The five stages in capital budgeting are the following:

1. An identification stage to determine which types of capital investments are available to accomplish organization objectives and

strategies.

2. An information-acquisition stage to gather data from all parts of the value chain in order to evaluate alternative capital investments.

3. A forecasting stage to project the future cash flows attributable to the various capital projects.

4. An evaluation stage where capital budgeting methods are used to choose the best alternative for the firm.

5. A financing, implementation, and control stage to fund projects, get them under way, and monitor their performance.

21-3 In essence, the discounted cash-flow method calculates the expected cash inflows and outflows of a project as if they occurred

at a single point in time so that they can be aggregated (added, subtracted, etc.) in an appropriate way. This enables comparison with

cash flows from other projects that might occur over different time periods.

21-4 No. Only quantitative outcomes are formally analyzed in capital budgeting decisions. Many effects of capital budgeting

decisions, however, are difficult to quantify in financial terms. These nonfinancial or qualitative factors (for example, the number of

accidents in a manufacturing plant or employee morale) are important to consider in making capital budgeting decisions.

21-5 Sensitivity analysis can be incorporated into DCF analysis by examining how the DCF of each project changes with changes in

the inputs used. These could include changes in revenue assumptions, cost assumptions, tax rate assumptions, and discount rates.

21-6 The payback method measures the time it will take to recoup, in the form of expected future net cash inflows, the net initial

investment in a project. The payback method is simple and easy to understand. It is a handy method when screening many proposals

and particularly when predicted cash flows in later years are highly uncertain. The main weaknesses of the payback method are its

neglect of the time value of money and of the cash flows after the payback period. The first drawback, but not the second, can be

addressed by using the discounted payback method.

21-7 The accrual accounting rate-of-return (AARR) method divides an accrual accounting measure of average annual income of a

project by an accrual accounting measure of investment. The strengths of the accrual accounting rate of return method are that it is

21-2

simple, easy to understand, and considers profitability. Its weaknesses are that it ignores the time value of money and does not consider

the cash flows for a project.

21-8 No. The discounted cash-flow techniques implicitly consider depreciation in rate of return computations; the compound interest

tables automatically allow for recovery of investment. The net initial investment of an asset is usually regarded as a lump–sum outflow

at time zero. Where taxes are included in the DCF analysis, depreciation costs are included in the computation of the taxable income

number that is used to compute the tax payment cash flow.

No. The discounted cash-flow techniques implicitly consider depreciation in rate of return computations; the compound interest

tables automatically allow for recovery of investment. the net initial investment of an asset is observed as a lump-sum outflow at time

zero. The DCF analysis comprises taxes and the computation of the taxable income number comprises depreciation costs that is used to

calculate the tax payment cash flow.

21-9 A point of agreement is that an exclusive attachment to the mechanisms of any single method examining only quantitative data

is likely to result in overlooking important aspects of a decision.

Two points of disagreement are (1) DCF can incorporate those strategic considerations that can be expressed in financial terms,

and (2) “practical considerations of strategy” not expressed in financial terms can be incorporated into decisions after DCF analysis.

21-10 All overhead costs are not relevant in NPV analysis. Overhead costs are relevant only if the capital investment results in a change

in total overhead cash flows. Overhead costs are not relevant if total overhead cash flows remain the same but the overhead allocated to

the particular capital investment changes.

21-11 The Division Y manager should consider why the Division X project was accepted and the Division Y project rejected by the

president. Possible explanations are

a. The president considers qualitative factors not incorporated into the IRR computation and this leads to the acceptance of the

X project and rejection of the Y project.

b. The president believes that Division Y has a history of overstating cash inflows and understating cash outflows.

c. The president has a preference for the manager of Division X over the manager of Division Y—this is a corporate politics

issue.

Factor a. means qualitative factors should be emphasized more in proposals. Factor b. means Division Y needs to document whether

its past projections have been relatively accurate. Factor c. means the manager of Division Y has to play the corporate politics game

better.

21-12 The categories of cash flow that should be considered in an equipment-replacement decision are:

1. a. Initial machine investment,

b. Initial working–capital investment,

21-3

c. After-tax cash flow from current disposal of old machine,

2. a. Annual after-tax cash flow from operations (excluding the depreciation effect),

b. Income tax cash savings from annual depreciation deductions,

3. a. After-tax cash flow from terminal disposal of machines, and

b. After-tax cash flow from terminal recovery of working–capital investment.

21-13 Income taxes can affect the cash inflows or outflows in a motor vehicle replacement decision as follows:

a. Tax is payable on gain or loss on disposal of the existing motor vehicle.

b. Tax is payable on any change in the operating costs of the new vehicle vis-à-vis the existing vehicle.

c. Tax is payable on gain or loss on the sale of the new vehicle at the project termination date.

d. Additional depreciation deductions for the new vehicle result in tax cash savings.

21-14 A cellular telephone company manager responsible for retaining customers needs to consider the expected future revenues and

the expected future costs of “different investments” to retain customers. One such investment could be a special price discount. An

alternative investment is offering loyalty club benefits to long-time customers.

These two rates of return differ in their elements:

Real-rate of return

Nominal rate of return

1. Risk-free element

1. Risk-free element

2. Business-risk element

2. Business-risk element

3. Inflation element

The inflation element is the premium above the real rate of return that is demanded for the anticipated decline in the general purchasing

power of the monetary unit.

21-16 Exercises in compound interest, no income taxes.

To be sure that you understand how to use the tables in Appendix A at the end of this book, solve the following exercises. Ignore income

tax considerations. The correct answers, rounded to the nearest dollar, appear on pages 838–839.

Required:

21-4

1. You have just won $10,000. How much money will you accumulate at the end of 10 years if you invest it at 8% compounded

annually? At 10%?

2. Ten years from now, the unpaid principal of the mortgage on your house will be $154,900. How much do you need to invest today

at 4% interest compounded annually to accumulate the $154,900 in 10 years?

3. If the unpaid mortgage on your house in 10 years will be $154,900, how much money do you need to invest at the end of each year

at 10% to accumulate exactly this amount at the end of the 10th year?

4. You plan to save $7,500 of your earnings at the end of each year for the next 10 years. How much money will you accumulate at the

end of the 10th year if you invest your savings compounded at 8% per year?

5. You have just turned 65 and an endowment insurance policy has paid you a lump sum of $250,000. If you invest the sum at 8%,

how much money can you withdraw from your account in equal amounts at the end of each year so that at the end of 10 years (age

75) there will be nothing left?

6. You have estimated that for the first 10 years after you retire you will need a cash inflow of $65,000 at the end of each year. How

much money do you need to invest at 8% at your retirement age to obtain this annual cash inflow? At 12%?

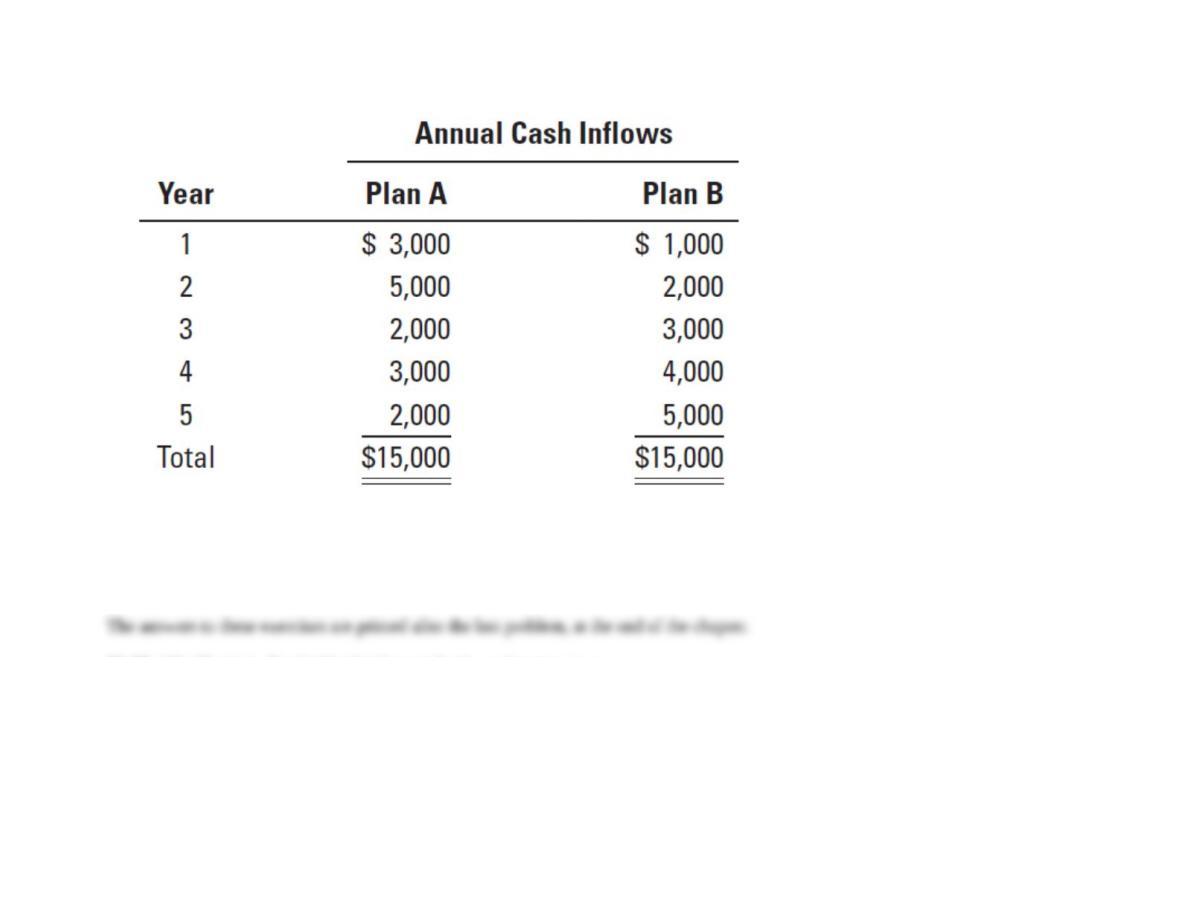

7. The following table shows two schedules of prospective operating cash inflows, each of which requires the same net initial

investment of $10,000 now:

21-5

The required rate of return is 8% compounded annually. All cash inflows occur at the end of each year. In terms of net present value,

which plan is more desirable? Show your computations.

SOLUTION

The answers to these exercises are printed after the last problem, at the end of the chapter.

21-17 (20–25 min.) Capital budgeting methods, no income taxes.

Riverbend Company runs hardware stores in a tristate area. Riverbend’s management estimates that if it invests $250,000 in a new

computer system, it can save $65,000 in annual cash operating costs. The system has an expected useful life of 8 years and no terminal

disposal value. The required rate of return is 8%. Ignore income tax issues in your answers. Assume all cash flows occur at year-end

except for initial investment amounts.

21-6

Required:

1. Calculate the following for the new computer system:

a. Net present value

b. Payback period

c. Discounted payback period

d. Internal rate of return (using the interpolation method)

e. Accrual accounting rate of return based on the net initial investment (assume straight–line depreciation)

2. What other factors should Riverbend consider in deciding whether to purchase the new computer system?

SOLUTION

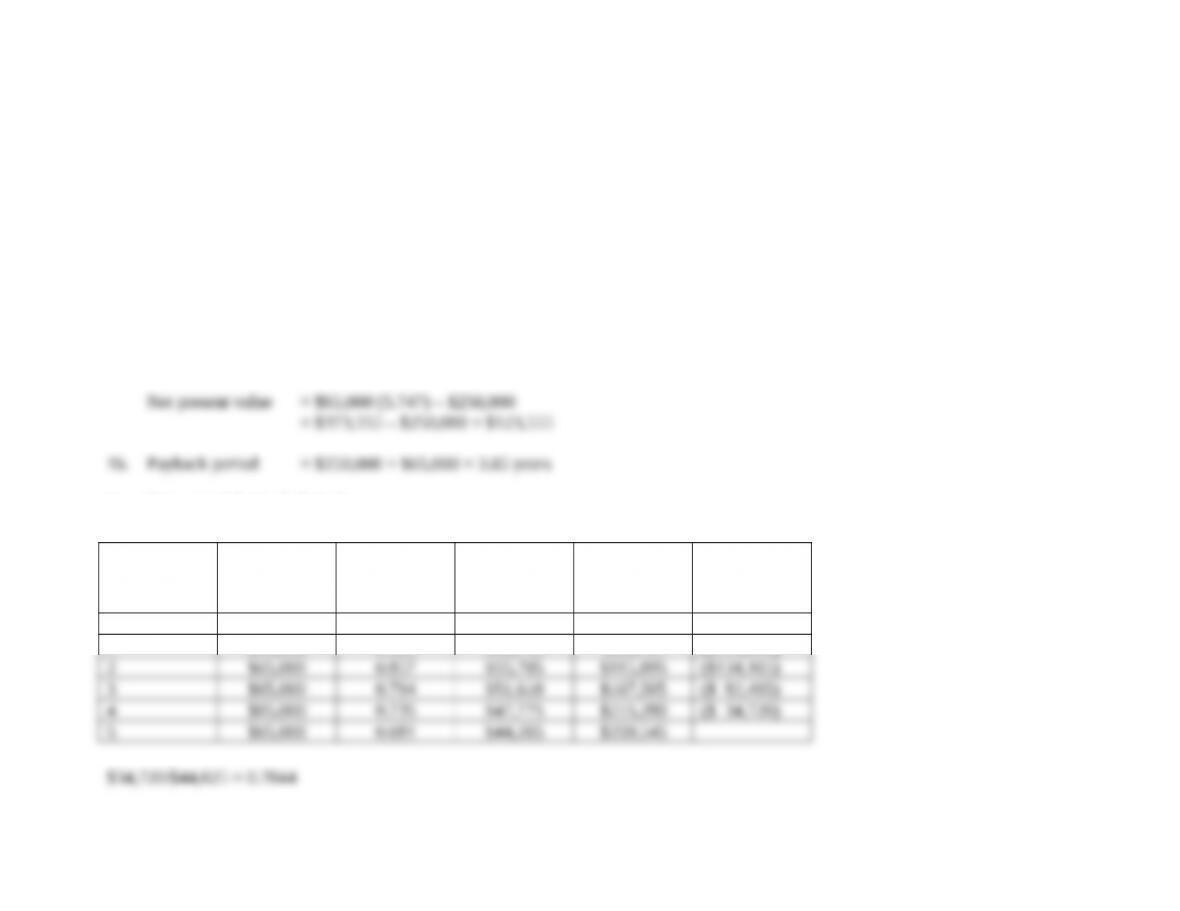

1a. The table for the present value of annuities (Appendix A, Table 4) shows:

8 periods at 8% = 5.747

Net present value = $65,000 (5.747) – $250,000

= $373,555 – $250,000 = $123,555

1b. Payback period = $250,000 ÷ $65,000 = 3.85 years

1c. Discounted Payback Period

Period

Cash Savings

Discount

Factor (8%)

Discounted

Cash Savings

Cumulative

Discounted

Cash Savings

Unrecovered

Investment

0

-$250,000

1

$65,000

0.926

$60,190

$60,190

($189,810)

2

$65,000

0.857

$55,705

$115,895

($134,105)

3

$65,000

0.794

$51,610

$167,505

($ 82,495)

4

$65,000

0.735

$47,775

$215,280

($ 34,720)

5

$65,000

0.681

$44,265

$259,545

$34,720/$44,625 = 0.7844

Discounted Payback period = 4.78 years

21-7

1d. Internal rate of return:

$250,000 = Present value of annuity of $65,000 at R% for 8 years, or what factor (F) in the table of present

values of an annuity (Appendix A, Table 4) will satisfy the following equation.

$250,000 = $65,000F

F = 250000/65000= 3.85

On the eight-year line in the table for the present value of annuities (Appendix A, Table 4), find the column closest to 3.85; it is between

a rate of return of 18% and 20%.

Interpolation is necessary:

Present Value Factors

18% 4.078 4.078

IRR rate – 3.850

20% 3.837 ––

Difference 0.241 0.228

Internal rate of return = 18% + (0.228/0.241) × (2%)

= 18% + 0.946 (2%) = 19.89%

1d. Accrual accounting rate of return based on net initial investment:

Net initial investment = $250,000

Estimated useful life = 8 years

Annual straight-line depreciation = $250,000 ÷ 8 = $31,250

return of rate accounting Accrual

=

investment initialNet

income operating annual average expectedin Increase

= ($65,000 – $31,250) / $250,000 = $33,750 / $250,000 = 13.5%

Note how the accrual accounting rate of return can produce results that differ markedly from the internal rate of return.

2. Other than the NPV, rate of return and the payback period on the new computer system, factors that Riverbend should consider

are the following:

21-8

• Issues related to the financing the project, and the availability of capital to pay for the system.

• The effect of the system on employee morale, particularly those displaced by the system. Salesperson expertise and real-time

help from experienced employees is key to the success of a hardware store.

• The benefits of the new system for customers (faster checkout, fewer errors).

• The upheaval of installing a new computer system. Its useful life is estimated to be eight years. This means that Riverbend

could face this upheaval again in eight years. Also, ensure that the costs of training and other “hidden” start-up costs are

included in the estimated $250,000 cost of the new computer system.

21-18 (25 min.) Capital budgeting methods, no income taxes.

City Hospital, a nonprofit organization, estimates that it can save $28,000 a year in cash operating costs for the next 10 years if it buys

a special-purpose eye-testing machine at a cost of $110,000. No terminal disposal value is expected. City Hospital’s required rate of

return is 14%. Assume all cash flows occur at year–end except for initial investment amounts. City Hospital uses straight–line

depreciation.

Required:

1. Calculate the following for the special-purpose eye-testing machine:

a. Net present value

b. Payback period

c. Internal rate of return

d. Accrual accounting rate of return based on net initial investment

e. Accrual accounting rate of return based on average investment

2. What other factors should City Hospital consider in deciding whether to purchase the special-purpose eye-testing machine?

21-9

SOLUTION

The table for the present value of annuities (Appendix A, Table 4) shows:

10 periods at 14% = 5.216

1a. Net present value = $28,000 (5.216) – $110,000

= $146,048 – $110,000 = $36,048

b. Payback period =

000,28$

000,110$

= 3.93 years

c. For a $110,000 initial outflow, the project generates $28,000 in cash flows at the end of each of years one through ten.

Using either a calculator or Excel, the internal rate of return for this stream of cash flows is found to be 21.96%.

d. Accrual accounting rate of return based on net initial investment:

Net initial investment = $110,000

Estimated useful life = 10 years

Annual straight-line depreciation = $110,000 ÷ 10 = $11,000

Accrual accounting rate of return =

000,110$

000,11$000,28$−

=

000,110$

000,17$

= 15.45%

e. Accrual accounting rate of return based on average investment:

Average investment = ($110,000 + $0) / 2

= $55,000

Accrual accounting rate of return =

$28,000 $11,000

$55,000

−

= 30.91%.

2. Factors City Hospital should consider include the following:

21-10

a. Quantitative financial aspects

b. Qualitative factors, such as the benefits to its customers of a better eye-testing machine and the employee–morale advantages

of having up-to–date equipment

c. Financing factors, such as the availability of cash to purchase the new equipment

21-19 (35 min.) Capital budgeting, income taxes.

Assume the same facts as in Exercise 21-18 except that City Hospital is a taxpaying entity. The income tax rate is 30% for all transactions

that affect income taxes.

Required:

1. Do requirement 1 of Exercise 21-18.

2. How would your computations in requirement 1 be affected if the special-purpose machine had a $10,000 terminal disposal value at

the end of 10 years? Assume depreciation deductions are based on the $110,000 purchase cost and zero terminal disposal value using

the straight-line method. Answer briefly in words without further calculations.

SOLUTION

1a. Net after-tax initial investment = $110,000

Annual after-tax cash flow from operations (excluding the depreciation effect):

Annual cash flow from operation with new machine

$28,000

Deduct income tax payments (30% of $28,000)

8,400

Annual after-tax cash flow from operations

$19,600

Income tax cash savings from annual depreciation deductions

30% $11,000

$3,300

These three amounts can be combined to determine the NPV:

Net initial investment;

$110,000 1.00

$(110,000)

10-year annuity of annual after-tax cash flows from operations;

$19,600 5.216

102,234

10-year annuity of income tax cash savings from annual depreciation deductions;

$3,300 5.216

17,213

Net present value

$ 9,447

21-12

b. Payback period

=

)300,3$600,19($

000,110$

+

=

900,22$

000,110$

= 4.80 years

c. For a $110,000 initial outflow, the project now generates $22,900 in after–tax cash flows at the end of each of years one through

ten.

Using either a calculator or Excel, the internal rate of return for this stream of cash flows is found to be 16.17%.

d. Accrual accounting rate of return based on net initial investment:

AARR =

000,110$

000,11$900,22$−

=

000,110$

900,11$

= 10.82%

e. Accrual accounting rate of return based on average investment:

AARR =

$22,900 $11,000

$55,000

−

=

$11,900

$55,000

= 21.64%

2a. Increase in NPV.

To get a sense for the magnitude, note that from Table 2, the present value factor for 10 periods at 14% is 0.270. Therefore, the

$10,000 terminal disposal price at the end of 10 years would have an after-tax NPV of:

21-13

$10,000 (1 − 0.30) 0.270 = $1,890

b. No change in the payback period of 4.80 years. The cash inflow occurs at the end of year 10.

c. Increase in internal rate of return. The $10,000 terminal disposal price would raise the IRR because of the additional inflow.

(The new IRR is 16.54%.)

d. The AARR on net initial investment would increase because accrual accounting income in year 10 would increase by the $7,000

($10,000 gain from disposal, less 30% $10,000) after-tax gain on disposal of equipment. This increase in year 10 income would result

in higher average annual accounting income in the numerator of the AARR formula.

e. The AARR on average investment would also increase for the same reasons given in the previous answer. Note that the

denominator is unaffected because the investment is still depreciated down to zero terminal disposal value, and so the average investment

remains $55,000.

21-20 (25 min.) Capital budgeting with uneven cash flows, no income taxes.

America Cola is considering the purchase of a special-purpose bottling machine for $65,000. It is expected to have a useful life of 4

years with no terminal disposal value. The plant manager estimates the following savings in cash operating costs:

21-14

Southern Cola uses a required rate of return of 18% in its capital budgeting decisions. Ignore income taxes in your analysis. Assume all

cash flows occur at year-end except for initial investment amounts.

Calculate the following for the special-purpose bottling machine:

Required:

1. Net present value

2. Payback period

3. Discounted payback period

4. Internal rate of return (using the interpolation method)

5. Accrual accounting rate of return based on net initial investment (Assume straight-line depreciation. Use the average annual savings

in cash operating costs when computing the numerator of the accrual accounting rate of return.)

21-15