$2,250,000

Operating income

$1,440,000

$2,188,800

Total operating income

$3,628,800

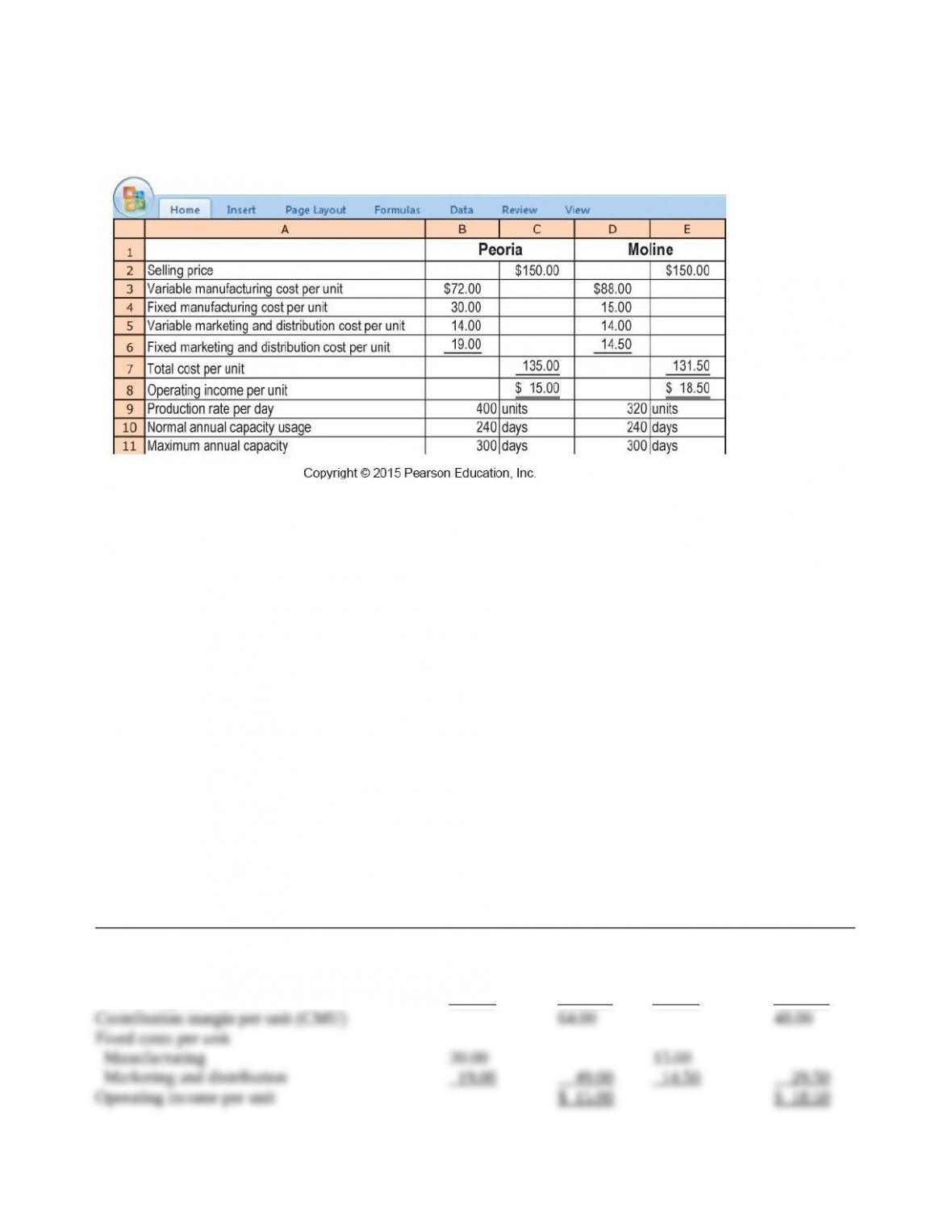

3. The optimal production plan is to produce 120,000 units at the Peoria plant and 72,000

units at the Moline plant. The full capacity of the Peoria plant, 120,000 units (400 units × 300

days), should be used because the contribution from these units is higher at all levels of production

than is the contribution from units produced at the Moline plant.

Contribution margin per plant:

Peoria, 96,000 × $64 $ 6,144,000

Peoria 24,000 × ($64 – $3) 1,464,000

Moline, 72,000 × $48 3,456,000

Total contribution margin 11,064,000

Deduct total fixed costs 6,969,600

Operating income $ 4,094,400

The contribution margin is higher when 120,000 units are produced at the Peoria plant and 72,000

units at the Moline plant. As a result, operating income will also be higher in this case because

total fixed costs for the division remain unchanged regardless of the quantity produced at each

plant.