Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

SOLUTION

Some instructors may also want to assign Exercise 4-25. It demonstrates the relationships of the

general ledger to the underlying subsidiary ledgers and source documents.

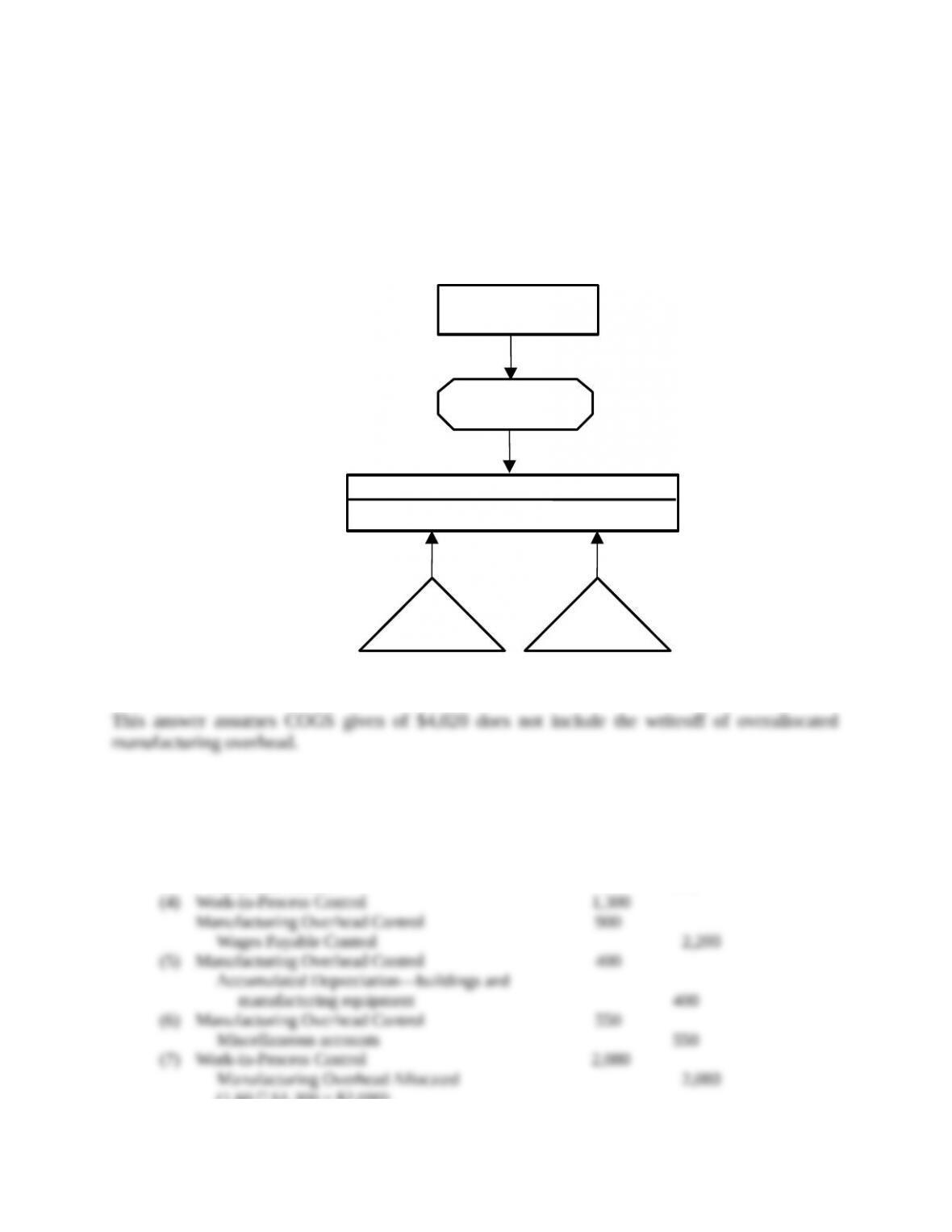

1. An overview of the product costing system is:

2. & 3.

This answer assumes COGS given of $4,020 does not include the writeoff of overallocated

manufacturing overhead.

2.

(1) Materials Control

Accounts Payable Control

800

800

(2) Work-in-Process Control

Materials Control

710

710

(3) Manufacturing Overhead Control

Materials Control

100

100

(4) Work-in-Process Control

Manufacturing Overhead Control

Wages Payable Control

1,300

900

2,200

(5) Manufacturing Overhead Control

Accumulated Depreciation––buildings and

manufacturing equipment

400

400

(6) Manufacturing Overhead Control

Miscellaneous accounts

550

550

(7) Work-in-Process Control

Manufacturing Overhead Allocated

(1.60 $1,300 = $2,080)

2,080

2,080

COST OBJECT:

PRINT JOB

COST

ALLOCATION

BASE

DIRECT

COST

Manufacturing Overhead

Direct Manufacturing

Labor Costs

Direct

Materials

INDIRECT

COST

POOL

Direct

Manuf

.

Labor

Indirect Costs

Direct Costs

4-2

(8) Finished Goods Control

Work-in-Process Control

4,120

4,120

(9) Accounts Receivable Control (or Cash)

Revenues

8,000

8,000

(10) Cost of Goods Sold

Finished Goods Control

4,020

4,020

(11) Manufacturing Overhead Allocated

Manufacturing Overhead Control

Cost of Goods Sold

2,080

1,950

130

4-3

3.

Materials Control

Bal. 1/1/2011

(1) Accounts Payable

Control (Purchases)

100

800

(2) Work-in-Process Control

(Materials used)

(3) Manufacturing Overhead

Control (Materials used)

710

100

Bal. 12/31/2011

90

Work-in-Process Control

Bal. 1/1/2011

(2) Materials Control

(Direct materials)

(4) Wages Payable

Control (Direct

manuf. labor)

(7) Manuf. Overhead

Allocated

60

710

1,300

2,080

(8) Finished Goods Control

(Goods completed)

4,120

Bal. 12/31/2011

30

Finished Goods Control

Bal. 1/1/2011

(8) WIP Control

(Goods completed)

500

4,120

(10) Cost of Goods Sold

4,020

Bal. 12/31/2011

600

Cost of Goods Sold

(10) Finished Goods

Control (Goods sold)

4,020

(11) Manufacturing Overhead

Allocated (Adjust for

overallocation)

130

Bal. 12/31/2011

3,890

Manufacturing Overhead Control

(3) Materials Control

(Indirect materials)

(4) Wages Payable Control

(Indirect manuf. labor)

(5) Accum. Deprn. Control

(Depreciation)

(6) Accounts Payable Control

(Miscellaneous)

100

900

400

550

(11) To close

1,950

Bal.

0

Manufacturing Overhead Allocated

(11) To close

2,080

(7) Work-in-Process Control

(Manuf. overhead allocated)

2,080

Bal.

0

4-4

4. Gross margin = Revenues Cost of goods sold = $8,000 $3,890 = $4,110. This is a very good

profit margin of 51% ($4,110 ÷ $8,000) indicating that University of Chicago Press

performed very well in 2014. (Gross margins above 30% are generally considered very

good.) It also accurately budgeted for manufacturing overhead costs resulting in a very small

overallocation.

4-5

3

4-25 (35 minutes) Journal entries, T-accounts, and source documents.

Creation Company produces gadgets for the coveted small appliance market. The following data

reflect activity for the year 2014:

Costs incurred:

Purchases of direct materials (net) on credit

$122,000

Direct manufacturing labor cost

83,000

Indirect labor

54,000

Depreciation, factory equipment

32,000

Depreciation, office equipment

7,900

Maintenance, factory equipment

29,000

Miscellaneous factory overhead

9,900

Rent, factory building

78,000

Advertising expense

94,000

Sales commissions

33,000

Inventories:

January 1, 2014

December 31, 2014

Direct materials

$ 9,800

$13,000

Work in process

6,300

23,000

Finished goods

68,000

27,000

Creation Co. uses a normal-costing system and allocates overhead to work in process at a rate of

$2.60 per direct manufacturing labor dollar. Indirect materials are insignificant so there is no

inventory account for indirect materials.

Required:

1. Prepare journal entries to record the transactions for 2014 including an entry to close out over-

or underallocated overhead to cost of goods sold. For each journal entry indicate the source

document that would be used to authorize each entry. Also note which subsidiary ledger, if

any, should be referenced as backup for the entry.

2. Post the journal entries to T-accounts for all of the inventories, Cost of Goods Sold, the

Manufacturing Overhead Control Account, and the Manufacturing Overhead Allocated

Account.

4-6

SOLUTION

1. i. Direct Materials Control 122,000

Accounts Payable Control 122,000

Source Document: Purchase Invoice, Receiving Report

Subsidiary Ledger: Direct Materials Record, Accounts Payable

ii. Work in Process Controla 118,800

Direct Materials Control 118,800

Source Document: Material Requisition Records, Job Cost Record

Subsidiary Ledger: Direct Materials Record, Work-in-Process Inventory Records by Jobs

iii. Work in Process Control 83,000

Manufacturing Overhead Control 54,000

Wages Payable Control 137,000

Source Document: Labor Time Sheets, Job Cost Records

Subsidiary Ledger: Manufacturing Overhead Records, Employee Labor Records, Work-in-

Process Inventory Records by Jobs

iv. Manufacturing Overhead Control 148,900

Salaries Payable Control 29,000

Accounts Payable Control 9,900

Accumulated Depreciation Control 32,000

Rent Payable Control 78,000

Source Document: Depreciation Schedule, Rent Schedule, Maintenance wages due, Invoices

for miscellaneous factory overhead items

Subsidiary Ledger: Manufacturing Overhead Records

v. Work in Process Control 215,800

Manufacturing Overhead Allocated 215,800

($83,000

$2.60)

Source Document: Labor Time Sheets, Job Cost Record

Subsidiary Ledger: Work-in-Process Inventory Records by Jobs

vi. Finished Goods Controlb 400,900

Work in Process Control 400,900

Source Document: Job Cost Record, Completed Job Cost Record

Subsidiary Ledger: Work-in-Process Inventory Records by Jobs, Finished Goods Inventory

Records by Jobs

vii. Cost of Goods Soldc 441,900

Finished Goods Control 441,900

Source Document: Sales Invoice, Completed Job Cost Record

Subsidiary Ledger: Finished Goods Inventory Records by Jobs

4-7

viii. Manufacturing Overhead Allocated 215,800

Manufacturing Overhead Control

($54,000 + $148,900) 202,900

Cost of Goods Sold 12,900

Source Document: Prior Journal Entries

ix. Administrative Expenses 7,900

Marketing Expenses 127,000

Salaries Payable Control 33,000

Accounts Payable Control 94,000

Accumulated Depreciation, Office Equipment 7,900

Source Document: Depreciation Schedule, Marketing Payroll Request, Invoice for

Advertising, Sales Commission Schedule.

Subsidiary Ledger: Employee Salary Records, Administration Cost Records, Marketing Cost

Records.

aMaterials used =

Beginning direct

materials inventory

+ Purchases –

Ending direct

materials inventory

= $9,800 + $122,000 $13,000 = $118,800−

b

Cost of

goods manufactured

=

Beginning WIP

inventory

+

Manufacturing

cost

–

Ending WIP

inventory

= $6,300 + ($118,800 + $83,000 + $215,800) $23,000 = $400,900−

cCost of goods sold =

Beginning finished

goods inventory

+

Cost of goods

manufactured

–

Ending finished

goods inventory

= $68,000 + $400,900 $27,000 = $441,900−

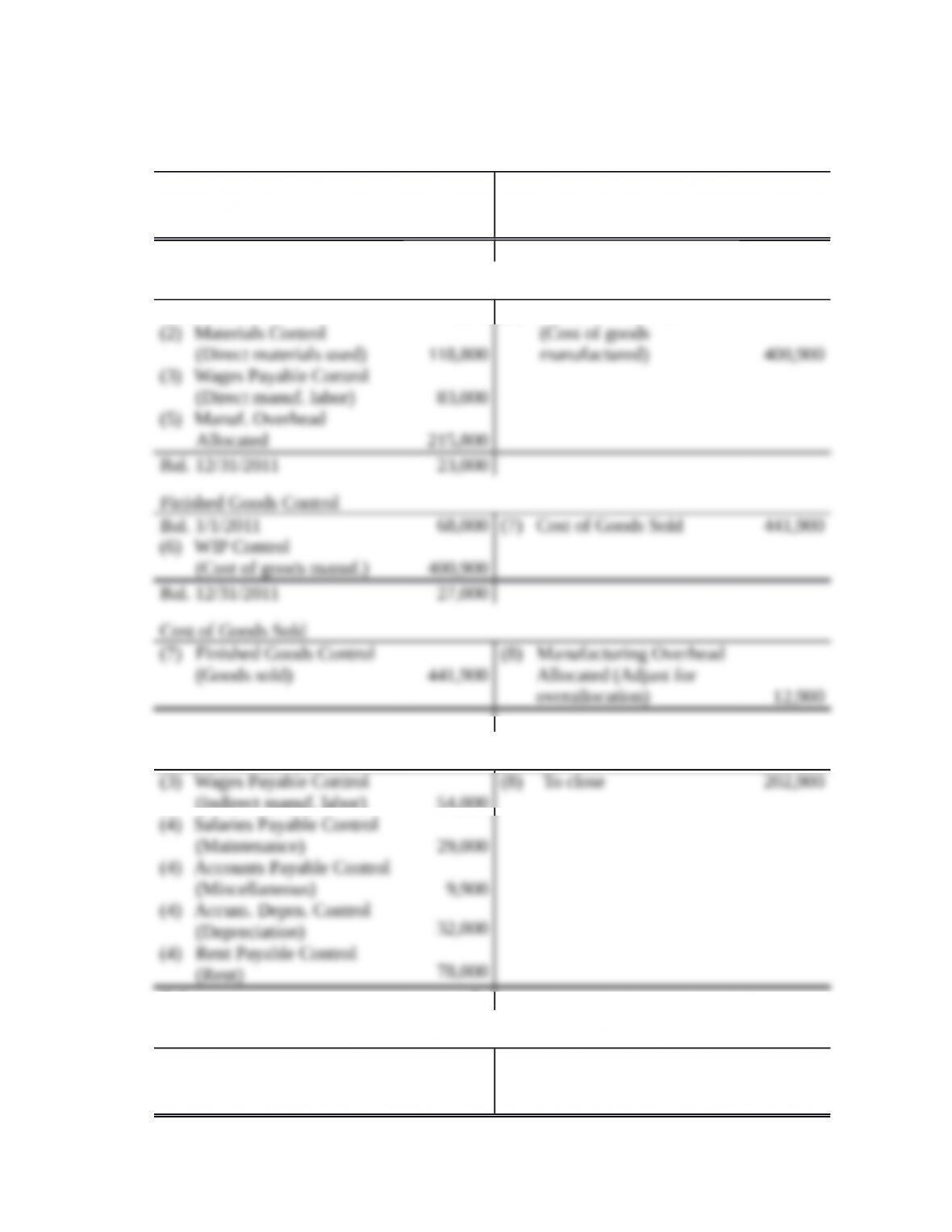

2. T-accounts

Direct Materials Control

Bal. 1/1/2011

(1) Accounts Payable Control

(Purchases)

9,800

122,000

(2) Work-in-Process Control

(Materials used)

118,800

Bal. 12/31/2011

13,000

Work-in-Process Control

Bal. 1/1/2011

(2) Materials Control

(Direct materials used)

(3) Wages Payable Control

(Direct manuf. labor)

(5) Manuf. Overhead

Allocated

6,300

118,800

83,000

215,800

(6) Finished Goods Control

(Cost of goods

manufactured)

400,900

Bal. 12/31/2011

23,000

Finished Goods Control

Bal. 1/1/2011

(6) WIP Control

(Cost of goods manuf.)

68,000

400,900

(7) Cost of Goods Sold

441,900

Bal. 12/31/2011

27,000

Cost of Goods Sold

(7) Finished Goods Control

(Goods sold)

441,900

(8) Manufacturing Overhead

Allocated (Adjust for

overallocation)

12,900

Manufacturing Overhead Control

(3) Wages Payable Control

(Indirect manuf. labor)

(4) Salaries Payable Control

(Maintenance)

(4) Accounts Payable Control

(Miscellaneous)

(4) Accum. Deprn. Control

(Depreciation)

(4) Rent Payable Control

(Rent)

54,000

29,000

9,900

32,000

78,000

(8) To close

202,900

Bal.

0

Manufacturing Overhead Allocated

(8) To close

215,800

(5) Work-in-Process Control

(Manuf. overhead

allocated)

215,800

4-9

Bal.

0

aMaterials used =

Beginning direct

materials inventory

+ Purchases –

Ending direct

materials inventory

= $9,800 + $122,000 $13,000 = $118,800−

b

Cost of

goods manufactured

=

Beginning WIP

inventory

+

Manufacturing

cost

–

Ending WIP

inventory

= $6,300 + ($118,800 + $83,000 + $215,800) $23,000 = $400,900−

cCost of goods sold =

Beginning finished

goods inventory

+

Cost of goods

manufactured

–

Ending finished

goods inventory

= $68,000 + $400,900 $27,000 = $441,900−

4-10

4-26 (45 min.) Job costing, journal entries.

Donald Transport assembles prestige manufactured homes. Its job- costing system has two direct-

cost categories (direct materials and direct manufacturing labor) and one indirect-cost pool

(manufacturing overhead allocated at a budgeted $31 per machine-hour in 2014). The following

data (in millions) show operation costs for 2014:

Materials Control, beginning balance, January 1, 2014 $ 18

Work-in-Process Control, beginning balance, January 1, 2014 9

Finished Goods Control, beginning balance, January 1, 2014 10

Materials and supplies purchased on credit 154

Direct materials used 152

Indirect materials (supplies) issued to various production departments 19

Direct manufacturing labor 96

Indirect manufacturing labor incurred by various production departments 34

Depreciation on plant and manufacturing equipment 28

Miscellaneous manufacturing overhead incurred (ordinarily would be detailed as 13

repairs, utilities, etc., with a corresponding credit to various liability accounts)

Manufacturing overhead allocated, 3,000,000 actual machine-hours ?

Cost of goods manufactured 298

Revenues 410

Cost of goods sold 294

Required:

1. Prepare an overview diagram of Donald Transport’s job-costing system.

2. Prepare journal entries. Number your entries. Explanations for each entry may be omitted. Post

to T-accounts. What is the ending balance of Work-in-Process Control?

3. Show the journal entry for disposing of under- or overallocated manufacturing overhead

directly as a year-end writeoff to Cost of Goods Sold. Post the entry to T-accounts.

4. How did Donald Transport perform in 2014?