20-1

CHAPTER 20

INVENTORY MANAGEMENT, JUST-IN-TIME,

AND SIMPLIFIED COSTING METHODS

20-1 Cost of goods sold (in retail organizations) or direct materials costs (in organizations with

a manufacturing function) as a percentage of sales frequently exceeds net income as a percentage

of sales by many orders of magnitude. In the Kroger grocery store example cited in the text, cost

of goods sold to sales is 79.4%, and net income to sales is 1.5%. Thus, a 10% reduction in the ratio

of cost of goods sold to sales (79.4 to 71.5% equal to 7.9%) without any other changes can result

in a 527% increase in net income to sales (1.5% plus 7.9% equal to 9.4%).

20-2 Six cost categories important in managing goods for sale in a retail organization are the

following:

1. Purchasing costs

2. Ordering costs

3. Carrying costs

4. Stockout costs

5. Costs of quality

6. Shrinkage costs

20-3 Five assumptions made when using the simplest version of the EOQ model are the

following:

1. The same quantity is ordered at each reorder point.

2. Demand, ordering costs, carrying costs, and the purchase-order lead time are certain.

3. Purchasing cost per unit is unaffected by the quantity ordered.

4. No stockouts occur.

5. Costs of quality and shrinkage costs are considered only to the extent that these costs affect

ordering costs or carrying costs.

20-4 Costs included in the carrying costs of inventory are incremental costs for such items as

insurance, rent, and obsolescence plus the opportunity cost of capital (or required return on

investment).

20-5 Examples of opportunity costs relevant to the EOQ decision model but typically not

recorded in accounting systems are the following:

1. The return forgone by investing capital in inventory

2. Lost contribution margin on existing sales when a stockout occurs;

3. Lost contribution margin on potential future sales that will not be made to disgruntled

customers

20-6 The steps in computing the costs of a prediction error when using the EOQ decision model

are: Step 1: Compute the monetary outcome from the best action that could be taken, given

the actual amount of the cost input.

Step 2: Compute the monetary outcome from the best action based on the incorrect

amount of the predicted cost input.

Step 3: Compute the difference between the monetary outcomes from Steps 1 and 2.

20-2

20-7 Goal congruence issues arise when there is an inconsistency between the EOQ decision

model and the model used for evaluating the performance of the person implementing the model.

For example, if opportunity costs are ignored in performance evaluation, the manager may be

induced to purchase in a quantity larger than the EOQ model indicates is optimal.

20-8 Just-in-time (JIT) purchasing is the purchase of materials (or goods) so that they are

delivered just as needed for production (or sales). Benefits include lower inventory holdings

(reduced warehouse space required and less money tied up in inventory) and less inventory

obsolescence and spoilage. The risk in JIT purchasing is the risk of stockouts—delays in supply

of materials (or goods) may result in materials (goods) not being available when needed for

production (or sales).

20-9 Factors causing reductions in the cost to place purchase orders of materials are the

following:

• Companies are establishing long-run purchasing agreements that define price and

quality terms over an extended period.

• Companies are using electronic links, such as the Internet, to place purchase orders.

• Companies are increasing the use of purchase-order cards.

20-10 Disagree. Choosing the supplier who offers the lowest price will not necessarily result in

the lowest total purchase cost to the buyer. This is because the price or purchase cost of the goods

is only one—and perhaps, most obvious—element of cost associated with purchasing and

managing inventories. Other relevant cost items are ordering costs, carrying costs, stockout costs,

quality costs, and shrinkage costs. A low-cost supplier may well impose conditions on the buyer—

such as poor quality or frequent stockouts or excessively high inventories—that result in high total

costs of purchase. Buyers must examine all the elements of costs relevant to inventory

management, not just the purchase price.

20-11 Supply-chain analysis describes the flow of goods, services, and information from the

initial sources of materials and services to the delivery of products to consumers, regardless of

Sharing of information across companies benefits manufacturers and retailers because it enables a

reduction in inventory levels at all stages of the supply chain, fewer stockouts at the retail level,

reduced manufacture of product not subsequently demanded by retailers, and a reduction in

expedited manufacturing orders.

20-12 Just-in–time (JIT) production is a “demand–pull” manufacturing system that manufactures

each component in a production line as soon as, and only when, needed by the next step in the

production line. It has the following features:

• Organize production in manufacturing cells.

• Hire and retain workers who are multi-skilled.

• Aggressively pursue total quality management (TQM) to eliminate defects.

• Place emphasis on reducing both setup time and manufacturing cycle time.

• Carefully select suppliers who are capable of delivering quality materials in a timely

manner.

The benefits of JIT production include lower costs and higher margins from better flow of

information, higher quality, and faster delivery, as well as simpler accounting systems. The cost

20-3

of JIT production is the risk of stockouts—a production problem in any step of the manufacturing

process will result in materials (goods) not being produced in time.

20-12 Traditional normal and standard costing systems use sequential tracking, in which journal

entries are recorded in the same order as actual purchases and progress in production,

typically at four different trigger points in the process.

Backflush costing omits recording some of the journal entries relating to the cycle from

purchase of direct materials to sale of finished goods, i.e., it has fewer trigger points at which

journal entries are made. When journal entries for one or more stages in the cycle are omitted, the

journal entries for a subsequent stage use normal or standard costs to work backward to “flush out”

the costs in the cycle for which journal entries were not made.

20-14 Versions of backflush costing differ in the number and placement of trigger points at which

journal entries are made in the accounting system:

Number of

Journal Entry

Trigger Points

Location in Cycle Where

Journal Entries Made

Version 1

3

Stage A. Purchase of direct materials and incurring of

conversion costs

Stage C. Completion of good finished units of product

Stage D. Sale of finished goods

Version 2

2

Stage A. Purchase of direct materials and incurring of

conversion costs

Stage D. Sale of finished goods

Version 3

2

Stage C. Completion of good finished units of product

Stage D. Sale of finished goods

20-15 Traditional accounting systems cost individual products and separate product costs from

selling, general, and administrative costs. Lean accounting costs the entire value stream instead

of individual products. Rework costs, unused capacity costs, and common costs that cannot be

reasonably assigned to value streams are excluded from value stream costs. In addition, many

lean accounting systems expense material costs in the period they are purchased, rather than

storing them on the balance sheet until the products using the material are sold.

20-16 (20 min.) Economic order quantity for retailer.

Fan Base (FB) operates a megastore featuring sports merchandise. It uses an EOQ decision model

to make inventory decisions. It is now considering inventory decisions for its Los Angeles Galaxy

soccer jerseys product line. This is a highly popular item. Data for 2013 are as follows:

20-4

Each jersey costs FB $40 and sells for $80. The $7 carrying cost per jersey per year consists of the

required return on investment of $4.80 (12% × $40 purchase price) plus $2.20 in relevant

insurance, handling, and storage costs. The purchasing lead time is 7 days. FB is open 365 days a

year.

Required:

1. Calculate the EOQ.

2. Calculate the number of orders that will be placed each year.

3. Calculate the reorder point.

SOLUTION

1. D = 10,000 jerseys per year, P = $200, C = $7 per jersey per year

7

200$000,102

C

DP 2

EOQ

==

= 755.93 756 jerseys

2. Number of orders per year =

EOQ

D

=

756

000,10

= 13.22 14 orders

3.

day working each Demand

=

days workingofNumber

D

=

365

000,10

= 27.40 jerseys per day

Purchase lead time = 7 days

Reorder point = 27.40 7

= 191.80 192 jerseys

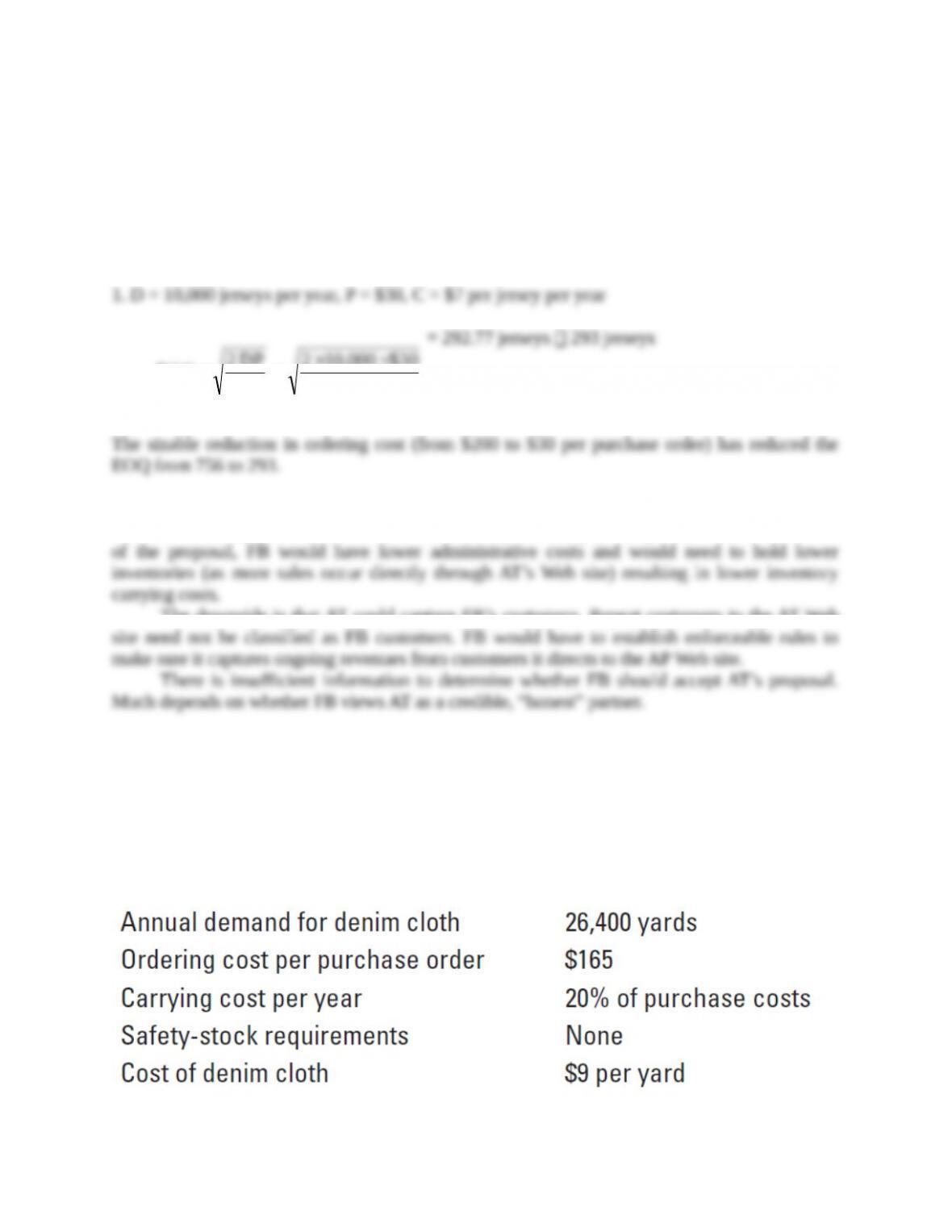

20-17 (20 min.) Economic order quantity, effect of parameter changes (continuation of 20-16).

Athletic Textiles (AT) manufactures the Galaxy jerseys that Fan Base (FB) sells to its customers.

AT has recently installed computer software that enables its customers to conduct “one–stop”

purchasing using state-of-the-art Web site technology. FB’s ordering cost per purchase order will

be $30 using this new technology.

Required:

1. Calculate the EOQ for the Galaxy jerseys using the revised ordering cost of $30 per purchase

order. Assume all other data from Exercise 20-16 are the same. Comment on the result.

2. Suppose AT proposes to “assist” FB. AT will allow FB customers to order directly from the

AT Web site. AT would ship directly to these customers. AT would pay $10 to FB for every

Galaxy jersey purchased by one of FB’s customers. Comment qualitatively on how this offer

would affect inventory management at FB. What factors should FB consider in deciding

whether to accept AT’s proposal?

20-5

SOLUTION

1. D = 10,000 jerseys per year, P = $30, C = $7 per jersey per year

7

30$000,102

C

DP 2

EOQ

==

= 292.77 jerseys 293 jerseys

The sizable reduction in ordering cost (from $200 to $30 per purchase order) has reduced the EOQ

from 756 to 293.

2. The AT proposal has both upsides and downsides. The upside is potentially higher sales.

FB customers may purchase more online than if they have to physically visit a store. As a result

of the proposal, FB would have lower administrative costs and would need to hold lower

inventories (as more sales occur directly through AT’s Web site) resulting in lower inventory

carrying costs.

The downside is that AT could capture FB’s customers. Repeat customers to the AT Web

site need not be classified as FB customers. FB would have to establish enforceable rules to make

sure it captures ongoing revenues from customers it directs to the AP Web site.

There is insufficient information to determine whether FB should accept AT’s proposal.

Much depends on whether FB views AT as a credible, “honest” partner.

20-18 (15 min.) EOQ for a retailer.

The Denim World sells fabrics to a wide range of industrial and consumer users. One of the

products it carries is denim cloth, used in the manufacture of jeans and carrying bags. The supplier

for the denim cloth pays all incoming freight. No incoming inspection of the denim is necessary

because the supplier has a track record of delivering high-quality merchandise. The purchasing

officer of the Denim World has collected the following information:

The purchasing lead time is 2 weeks. The Denim World is open 250 days a year (50 weeks for 5

days a week).

Required:

1. Calculate the EOQ for denim cloth.

2. Calculate the number of orders that will be placed each year.

20-6

3. Calculate the reorder point for denim cloth.

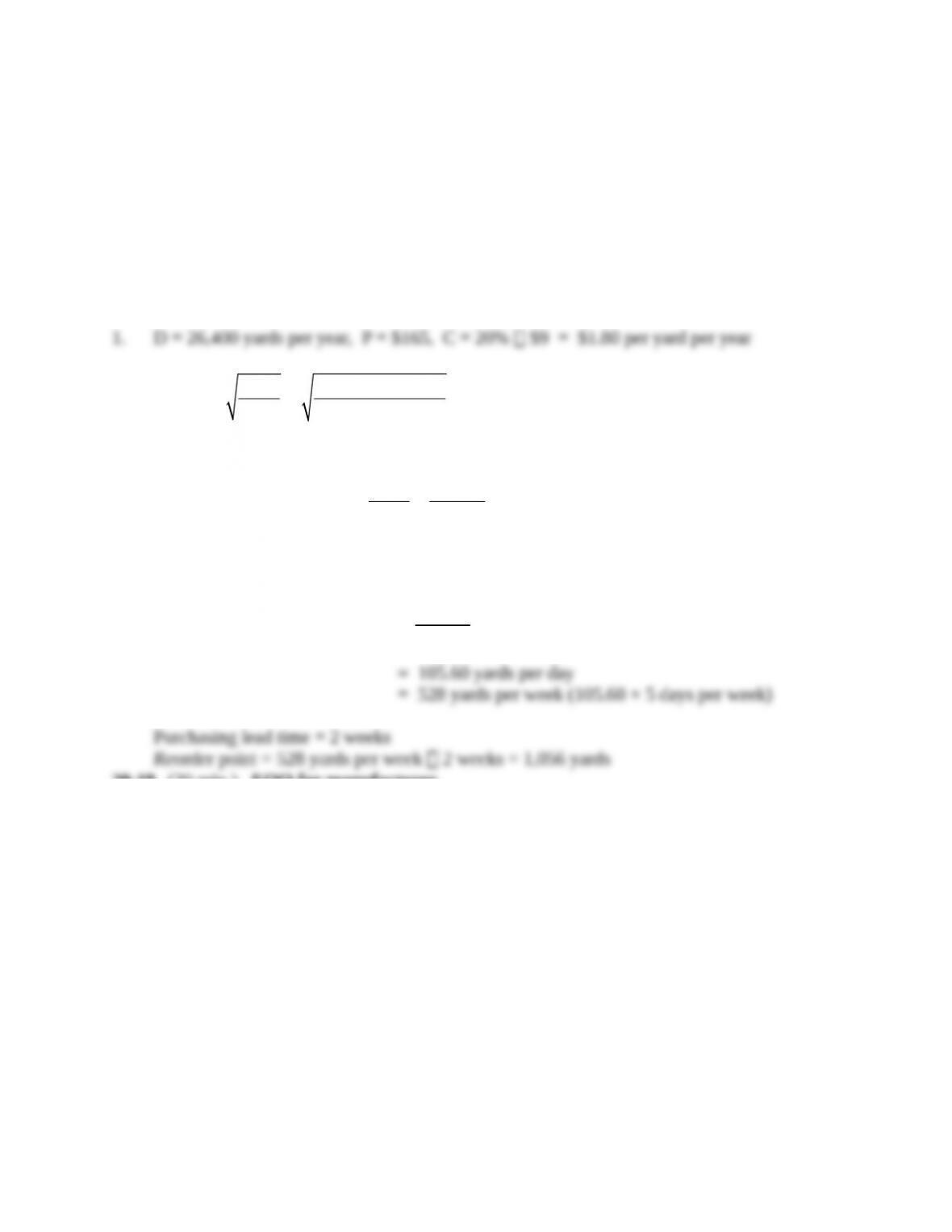

SOLUTION

1. D = 26,400 yards per year, P = $165, C = 20% $9 = $1.80 per yard per year

2 26,400 $165

2 DP

EOQ 2,200 yards

C $1.80

= = =

2. Number of orders per year:

D 26,400 12 orders per year

EOQ 2,200

==

3. Demand each working day = D

Number of working days

=

26,400

250

= 105.60 yards per day

= 528 yards per week (105.60 × 5 days per week)

Purchasing lead time = 2 weeks

Reorder point = 528 yards per week 2 weeks = 1,056 yards

20-19 (20 min.) EOQ for manufacturer.

Turfpro Company produces lawn mowers and purchases 4,500 units of a rotor blade part each year

at a cost of $30 per unit. Turfpro requires a 15% annual rate of return on investment. In addition,

the relevant carrying cost (for insurance, materials handling, breakage, etc.) is $3 per unit per year.

The relevant ordering cost per purchase order is $75.

Required:

1. Calculate Turfpro’s EOQ for the rotor blade part.

2. Calculate Turfpro’s annual relevant ordering costs for the EOQ calculated in requirement 1.

3. Calculate Turfpro’s annual relevant carrying costs for the EOQ calculated in requirement 1.

4. Assume that demand is uniform throughout the year and known with certainty so there is no

need for safety stocks. The purchase-order lead time is half a month. Calculate Turfpro’s

reorder point for the rotor blade part.

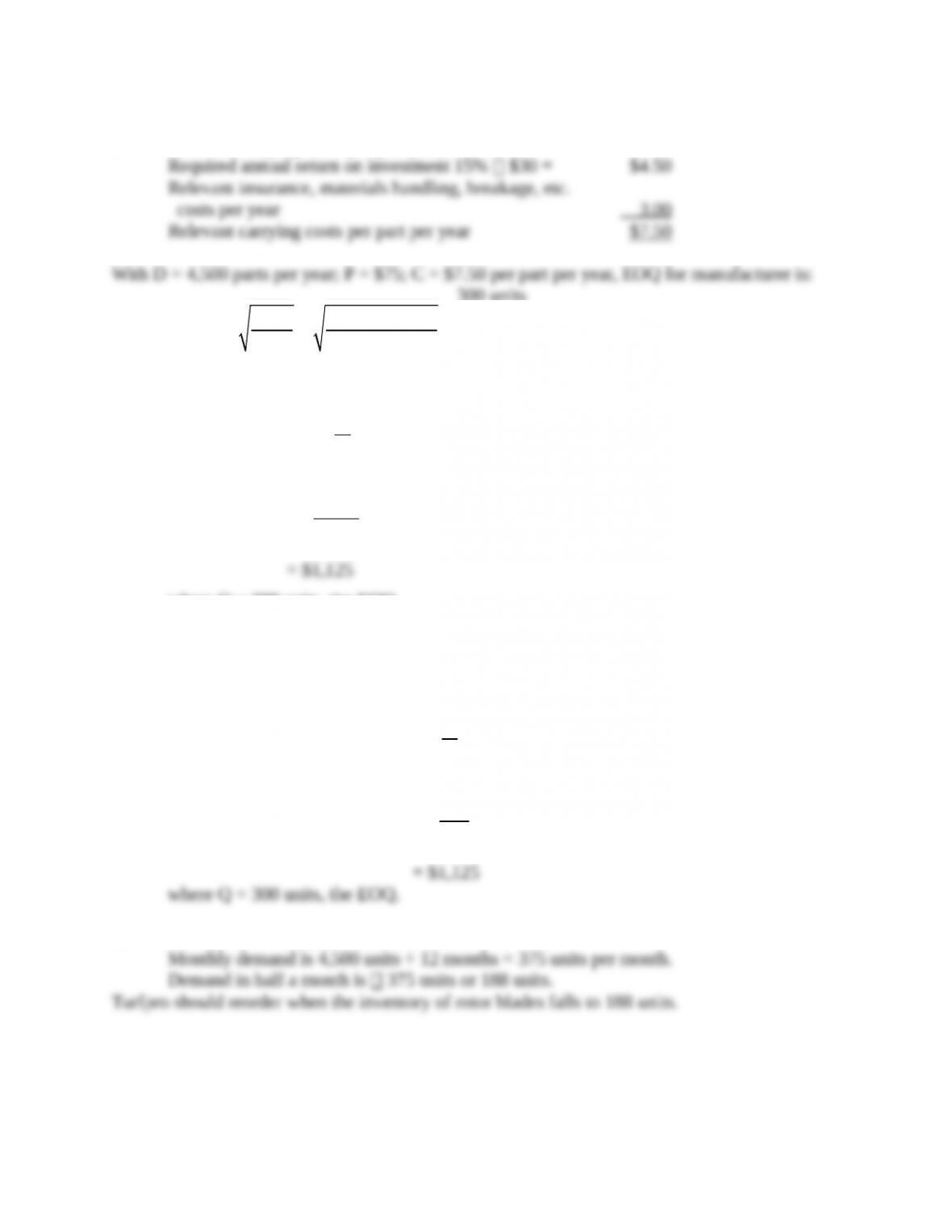

SOLUTION

1. Relevant carrying costs per part per year:

Required annual return on investment 15% $30 = $4.50

Relevant insurance, materials handling, breakage, etc.

costs per year 3.00

Relevant carrying costs per part per year $7.50

With D = 4,500 parts per year; P = $75; C = $7.50 per part per year, EOQ for manufacturer is:

20-7

2 DP 2 4,500 $75

EOQ C 7.50

= = =

300 units

2.

Relevant annual

ordering costs

=

D P

Q

=

4,500 $75

300

= $1,125

where Q = 300 units, the EOQ.

3. At the EOQ, total relevant ordering costs and total relevant carrying costs will be exactly

equal. Therefore, total relevant carrying costs at the EOQ = $1,125 (from requirement 2). We can

also confirm this with a direct calculation:

Relevant annual carrying costs

=

Q C

2

=

300 $7.50

2

= $1,125

where Q = 300 units, the EOQ.

4. Purchase order lead time is half a month.

Monthly demand is 4,500 units ÷ 12 months = 375 units per month.

Demand in half a month is 1

2 375 units or 188 units.

Turfpro should reorder when the inventory of rotor blades falls to 188 units.

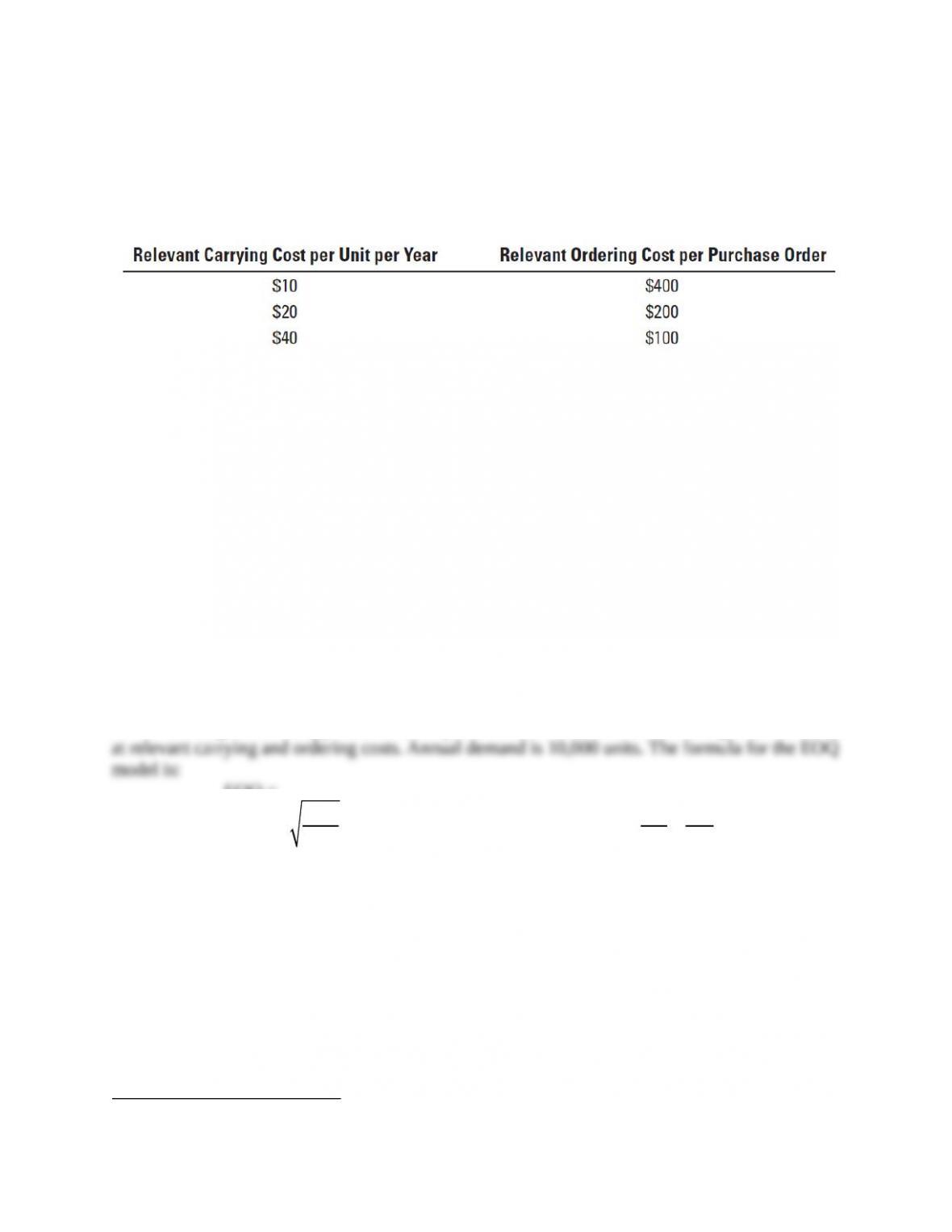

20-20 (20 min.) Sensitivity of EOQ to changes in relevant ordering and carrying costs.

Alpha Company’s annual demand for its only product, XT-590, is 10,000 units. Alpha is currently

analyzing possible combinations of relevant carrying cost per unit per year and relevant ordering

cost per purchase order, depending on the company’s choice of supplier and average levels of

inventory. This table presents three possible combinations of carrying and ordering costs.

Required:

1. For each of the relevant ordering and carrying-cost alternatives, determine (a) EOQ and (b)

annual relevant total costs.

20-8

2. How does your answer to requirement 1 give insight into the impact of changes in relevant

ordering and carrying costs on EOQ and annual relevant total costs? Explain briefly.

3. Suppose the relevant carrying cost per unit per year was $20 and the relevant ordering cost per

purchase order was $200. Suppose further that Alpha calculates EOQ after incorrectly

estimating relevant carrying cost per unit per year to be $10 and relevant ordering cost per

purchase order to be $400. Calculate the actual annual relevant total costs of Alpha’s EOQ

decision. Compare this cost to the annual relevant total costs that Alpha would have incurred

if it had correctly estimated the relevant carrying cost per unit per year of $20 and the relevant

ordering cost per purchase order of $200 that you have already calculated in requirement 1.

Calculate and comment on the cost of the prediction error.

SOLUTION

1. A straightforward approach to the requirement is to construct the following table for EOQ

at relevant carrying and ordering costs. Annual demand is 10,000 units. The formula for the EOQ

model is:

EOQ =

2DP DP QC

and for Relevant Total Costs (RTC) =

C Q 2

+

where D = demand in units per year

P = relevant ordering costs per purchase order

C = relevant carrying costs of one unit in stock for the time period used for D (one year in

this problem.

Relevant

Carrying

Costs per Unit

per Year

(C)

Relevant

Ordering

Costs per

Purchase

Order

(P)

$10 $400

2 10,000 $400 10,000 $400 895 $10

EOQ = 895, RTC= $8,944

$10 895 2

= + =

$20 $200

2 10,000 $200 10,000 $200 447 $20

EOQ = 447, RTC= $8,944

$20 447 2

= + =

$40 $100

2 10,000 $100 10,000 $100 224 $40

EOQ = 224, RTC= $8,944

$40 224 2

= + =

2. For a given demand level, as relevant carrying costs increase and relevant ordering costs

decrease, EOQ becomes smaller. That is EOQ decreases to compensate for increases in carrying

costs and to take advantage of decreases in ordering costs. That is, the EOQ offsets the effect on

total costs of the increase in carrying costs and the decrease in ordering costs.

In this example, the change in EOQ results in relevant total costs (RTC) being the same

across all three cases. The fact that the total costs are the same is a function of the specific

numbers chosen in this example. For example, in the last combination, if relevant carrying costs

20-9

per unit per year were $35 instead of $40 and relevant ordering costs per purchase order

remained at $100, the relevant total costs would equal $8,367.

2 10,000 $100 10,000 $100 239 $35

EOQ = 239, RTC= $8,367

$35 239 2

= + =

3. If Alpha estimates C = $10 per unit per year and P = $400 per order, then from

requirement 1,

EOQ = 224 units and Relevant Total Cost (RTC) = $8,944

For EOQ = 224 units, C = $20 per unit per year and P = $200 per order,

Relevant total costs (RTC) =

DP QC

Q2

+

10,000 $200 224 $20

224 2

=+

= $8,929 + $2,240 = $11,169

The prediction error equals $11,169 – $8,944 = $2,225, which is 25% ($2,225 ÷ $8,944) of the

relevant total cost had there been no prediction error. The error in prediction results in a

significantly higher cost but is still limited, given that the estimate of the carrying cost was half

the actual amount and the estimate of the ordering cost was twice the actual amount. The square

root function dampens the effect of the errors.

20-21 (20 min.) JIT production, relevant benefits, relevant costs.

The Colonial Hardware Company manufactures specialty brass door handles at its Lynchburg

plant. Colonial is considering implementing a JIT production system. The following are the

estimated costs and benefits of JIT production:

a. Annual additional tooling costs would be $200,000.

b. Average inventory would decline by 80% from the current level of $2,000,000.

c. Insurance, space, materials-handling, and setup costs, which currently total $600,000 annually,

would de- cline by 25%.

d. The emphasis on quality inherent in JIT production would reduce rework costs by 30%.

Colonial currently incurs $400,000 in annual rework costs.

e. Improved product quality under JIT production would enable Colonial to raise the price of its

product by $8 per unit. Colonial sells 40,000 units each year.

Colonial’s required rate of return on inventory investment is 15% per year.

Required:

1. Calculate the net benefit or cost to Colonial if it adopts JIT production at the Lynchburg plant.

2. What nonfinancial and qualitative factors should Colonial consider when making the decision

to adopt JIT production?

3. Suppose Colonial implements JIT production at its Lynchburg plant. Give examples of

performance measures Colonial could use to evaluate and control JIT production. What would

be the benefit of Colonial implementing an enterprise resource planning (ERP) system?

20-10

SOLUTION

1. Solution Exhibit 20-21 presents the annual net benefit of $630,000 to Colonial Hardware

Company of implementing a JIT production system.

2. Other nonfinancial and qualitative factors that Colonial should consider in deciding

whether it should implement a JIT system include:

a. The possibility of developing and implementing a detailed system for integrating the

sequential operations of the manufacturing process. Direct materials must arrive when

needed for each subassembly so that the production process functions smoothly.

b. The ability to design products that use standardized parts and reduce manufacturing

time.

c. The ease of obtaining reliable vendors who can deliver quality direct materials on time

with minimum lead time.

d. Willingness of suppliers to deliver smaller and more frequent orders.

e. The confidence of being able to deliver quality products on time. Failure to do so would

result in customer dissatisfaction.

f. The skill levels of workers to perform multiple tasks such as minor repairs,

maintenance, quality testing and inspection.

3. Personal observation by production line workers and managers is more effective in JIT

plants than in traditional plants. A JIT plant’s production process layout is streamlined. Operations

are not obscured by piles of inventory or rework. As a result, such plants are easier to evaluate by

personal observation than are cluttered plants where the flow of production is not logically laid

out.

Besides personal observation, nonfinancial performance measures are the dominant

methods of control. Nonfinancial performance measures provide most timely and easy to

understand measures of plant performance. Examples of nonfinancial performance measures of

time, inventory, and quality include the following:

• Manufacturing lead time

• Units produced per hour

• Machine setup time ÷ manufacturing time

• Number of defective units ÷ number of units completed

In addition to personal observation and nonfinancial performance measures, financial performance

measures are also used. Examples of financial performance measures include the following:

• Cost of rework

• Ordering costs

• Stockout costs

• Inventory turnover (cost of goods sold

average inventory)

The success of a JIT system depends on the speed of information flows from customers

to manufacturers to suppliers. The Enterprise Resource Planning (ERP) system has a single

database and gives lower-level managers, workers, customers, and suppliers access to operating

information. This benefit, accompanied by tight coordination across business functions, enables

20-11

the ERP system to rapidly transmit information in response to changes in supply and demand so

that manufacturing and distribution plans may be revised accordingly.