20-1

SOLUTION EXHIBIT 20-21

Annual Relevant Costs of Current Production System and JIT Production System

for Colonial Hardware Company

Relevant Items

Relevant

Costs under

Current

Production

System

Relevant

Costs under

JIT

Production

System

Annual tooling costs

–

$200,000

Required return on investment:

15% per year $2,000,000 of average inventory per year

$ 300,000

15% per year $400,000a of average inventory per year

60,000

Insurance, space, materials handling, and setup costs

600,000

450,000b

Rework costs

400,000

280,000c

Incremental revenues from higher selling prices

(320,000)d

Total net incremental costs

$1,300,000

$670,000

Annual difference in favor of JIT production $630,000

a $2,000,000 (1 – 80%) = $400,000

b$600,000 (1 – 0.25) = $450,000

c$400,000 (1 – 0.30) = $280,000

d$8 × 40,000 units = $320,000

20-22 (30 min.) Backflush costing and JIT production.

Grand Devices Corporation assembles handheld computers that have scaled-down capabilities of

laptop computers. Each handheld computer takes 6 hours to assemble. Grand Devices uses a JIT

production system and a backflush costing system with three trigger points:

▪ Purchase of direct materials and incurring of conversion costs

▪ Completion of good finished units of product

▪ Sale of finished goods

There are no beginning inventories of materials or finished goods and no beginning or ending

work-in– process inventories. The following data are for August 2013:

Grand Devices records direct materials purchased and conversion costs incurred at actual costs. It

has no direct materials variances. When finished goods are sold, the backflush costing system

“pulls through” standard direct material cost ($102 per unit) and standard conversion cost ($28 per

20-2

unit). Grand Devices produced 28,800 finished units in August 2013 and sold 28,400 units. The

actual direct material cost per unit in August 2013 was $102, and the actual conversion cost per

unit was $27.

Required:

1. Prepare summary journal entries for August 2013 (without disposing of under– or overallocated

conversion costs).

2. Post the entries in requirement 1 to T-accounts for applicable Materials and In-Process

Inventory Control, Finished Goods Control, Conversion Costs Control, Conversion Costs

Allocated, and Cost of Goods Sold.

3. Under an ideal JIT production system, how would the amounts in your journal entries differ

from those in requirement 1?

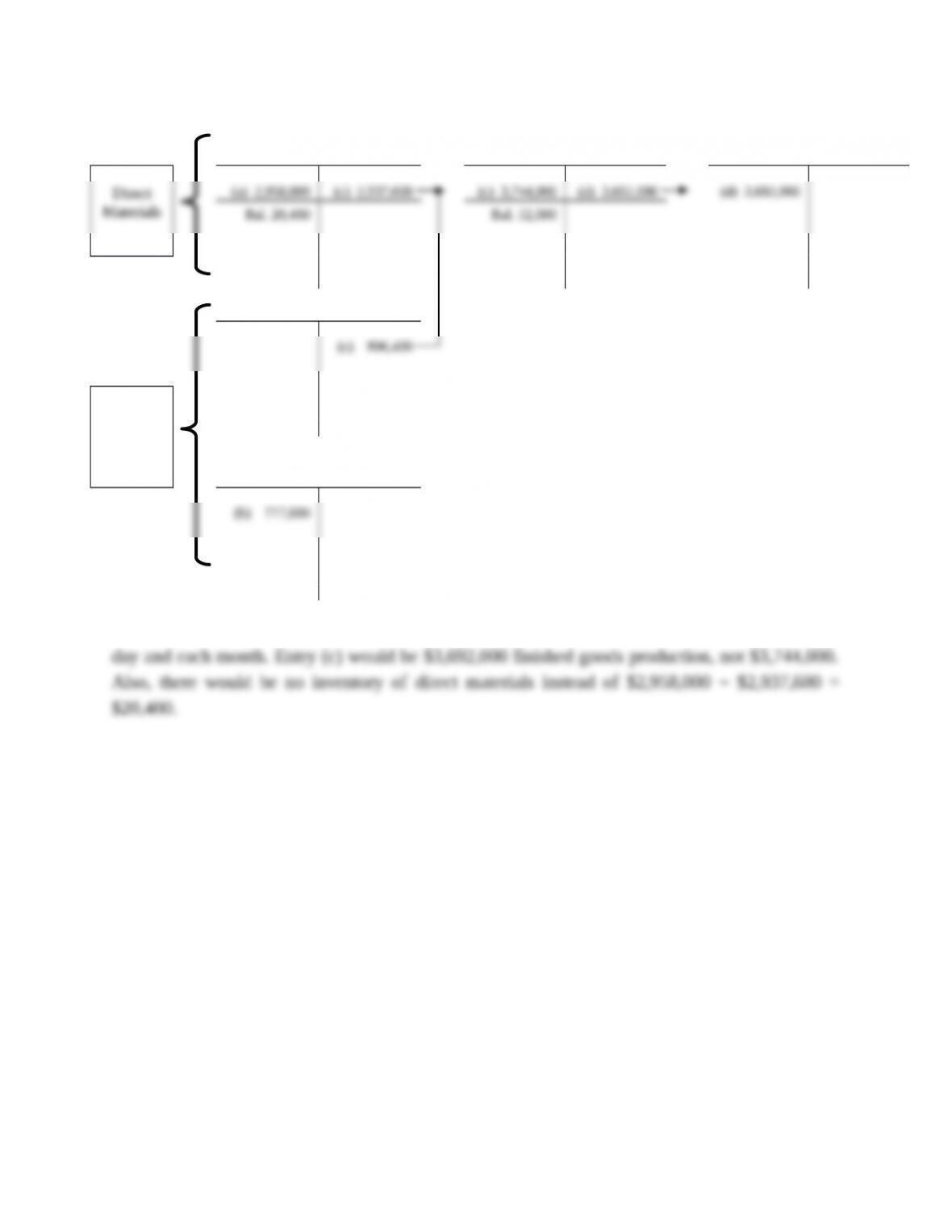

SOLUTION

1.

(a) Record purchases of

direct materials

Materials and In-Process Inventory Control

Accounts Payable Control

2,958,000

2,958,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

777,600

Wages Payable Control)

777,600

(c) Record cost of good

finished units completed

Finished Goods Controla

Materials and In-Process

3,744,000

Inventory Controla

2,937,600

Conversion Costs Allocateda

806,400

(d) Record cost of finished

goods sold

Cost of Goods Soldb

Finished Goods Control

3,692,000

3,692,000

a28,800 × ($102 + $28) = $3,744,000; 28,800 × $102 = $2,937,600; 28,800 × $28 = $806,400

b28,400 × ($102 + $28) = $3,692,000

20-3

2.

Materials and In-Process

Inventory Control

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(a) 2,958,000

(c) 2,937,600

(c) 3,744,000

(d) 3,692,000

(d) 3,692,000

Bal. 20,400

Bal. 52,000

Conversion Costs Allocated

(c) 806,400

Conversion

Costs

Conversion Costs Control

(b) 777,600

3. Under an ideal JIT production system, there would be zero inventories at the end of each

day and each month. Entry (c) would be $3,692,000 finished goods production, not $3,744,000.

Also, there would be no inventory of direct materials instead of $2,958,000 – $2,937,600 =

$20,400.

20-4

20-23 (20 min.) Backflush costing, two trigger points, materials purchase and sale

(continuation of 20-22).

Assume the same facts as in Exercise 20-22, except that Grand Devices now uses a backflush

costing system with the following two trigger points:

▪ Purchase of direct materials and incurring of conversion costs

▪ Sale of finished goods

The Inventory Control account will include direct materials purchased but not yet in production,

materials in work in process, and materials in finished goods but not sold. No conversion costs are

inventoried. Any under- or overallocated conversion costs are written off monthly to Cost of Goods

Sold.

Required:

1. Prepare summary journal entries for August, including the disposition of under– or

overallocated conversion costs.

2. Post the entries in requirement 1 to T-accounts for Inventory Control, Conversion Costs

Control, Conversion Costs Allocated, and Cost of Goods Sold.

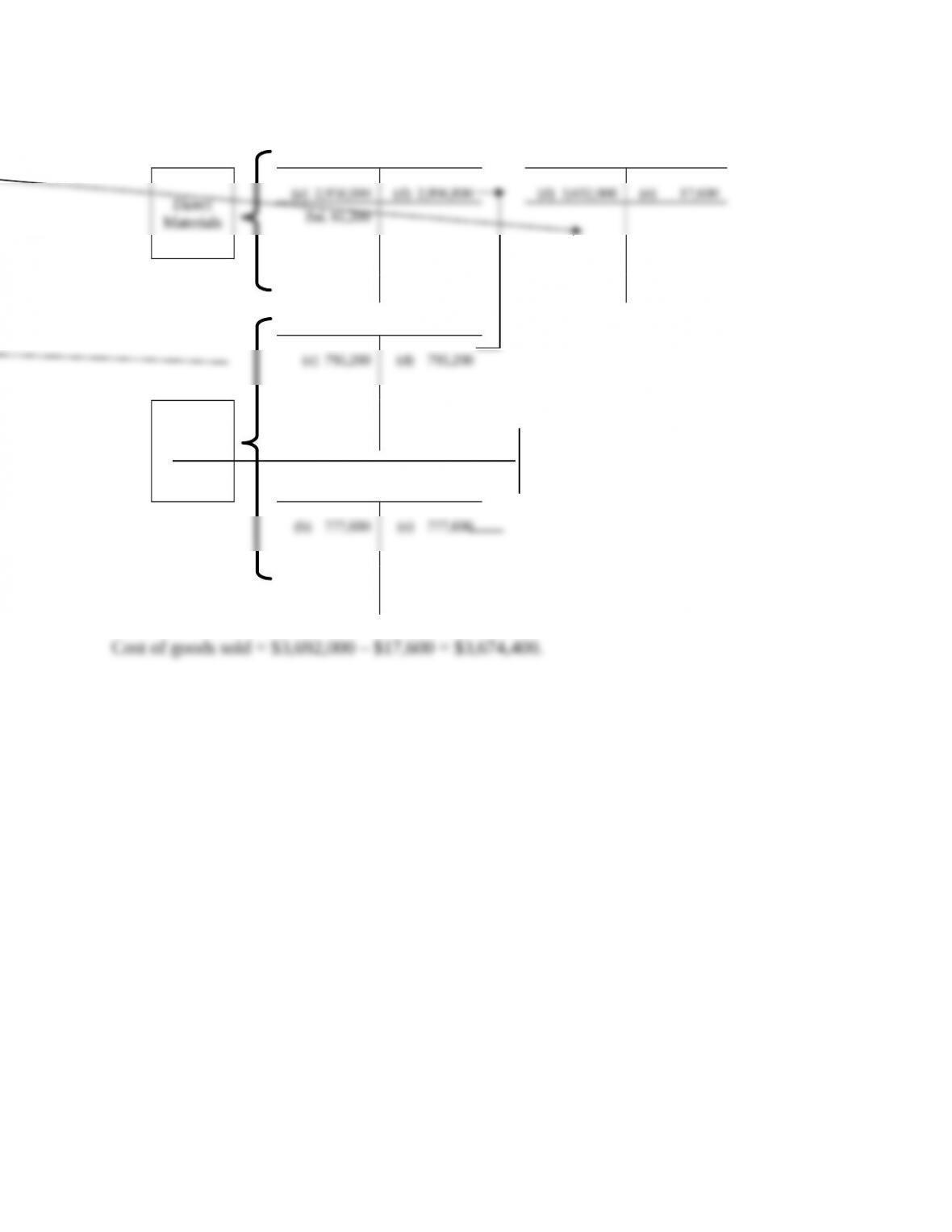

SOLUTION

1.

(a) Record purchases of direct

materials

Inventory Control

Accounts Payable Control

2,958,000

2,958,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

777,600

Wages Payable Control)

777,600

(c) Record cost of good

finished units completed

No entry

(d) Record cost of finished

goods sold

Cost of Goods Solda

Inventory Controla

3,692,000

2,896,800

Conversion Costs Allocateda

795,200

(e) Record underallocated or over-

allocated conversion costs

Conversion Costs Allocated

Costs of Goods Sold

795,200

17,600

Conversion Costs Control

777,600

a28,400 × ($102 + $28) = $3,692,000; 28,400 × $102 = $2,896,800; 28,400 × $28 = $795,200

20-5

2.

Inventory Control

Cost of Goods Sold

Direct

Materials

(a) 2,958,000

(d) 2,896,800

(d) 3,692,000

(e) 17,600

Bal. 61,200

Conversion Costs Allocated

(e) 795,200

(d) 795,200

Conversion

Costs

Conversion Costs Control

(b) 777,600

(e) 777,600

Cost of goods sold = $3,692,000 – $17,600 = $3,674,400.

20-6

20-24 (20 min.) Backflush costing, two trigger points, completion of production and

sale (continuation of 20-22).

Assume the same facts as in Exercise 20-22, except now Grand Devices uses only two trigger

points, Completion of good finished units of product and Sale of finished goods. Any under– or

overallocated conversion costs are written off monthly to Cost of Goods Sold.

Required:

1. Prepare summary journal entries for August, including the disposition of under– or

overallocated conversion costs.

2. Post the entries in requirement 1 to T-accounts for Finished Goods Control, Conversion Costs

Control, Conversion Costs Allocated, and Cost of Goods Sold.

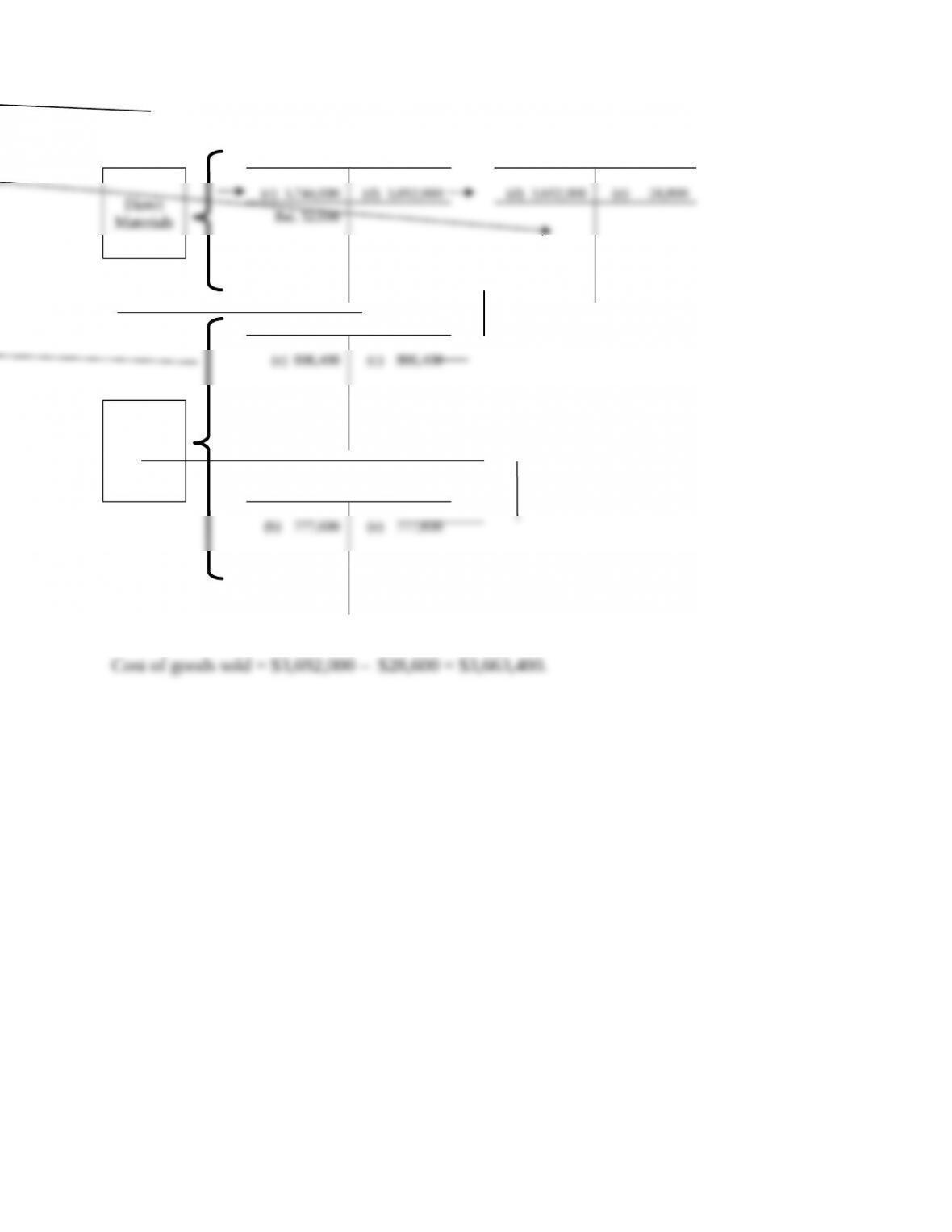

SOLUTION

1.

(a) Record purchases of direct

materials

No Entry

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

777,600

Wages Payable Control)

777,600

(c) Record cost of good finished

units completed

Finished Goods Controla

Accounts Payable Controla

3,744,000

2,937,600

Conversion Costs Allocateda

806,400

(d) Record cost of finished

goods sold

Cost of Goods Soldb

Finished Goods Control

3,692,000

3,692,000

(e) Record underallocated or over-

allocated conversion costs

Conversion Costs Allocated

Costs of Goods Sold

806,400

28,800

Conversion Costs Control

777,600

a28,800 × ($102 + $28) = $3,744,000; 28,800 × $102 = $2,937,600; 28,800 × $28 = $806,400

b28,400 × ($102 + $28) = $3,692,000

20-7

2.

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(c) 3,744,000

(d) 3,692,000

(d) 3,692,000

(e) 28,800

Bal. 52,000

Conversion Costs Allocated

(e) 806,400

(c) 806,400

Conversion

Costs

Conversion Costs Control

(b) 777,600

(e) 777,600

Cost of goods sold = $3,692,000 – $28,600 = $3,663,400.

20-8

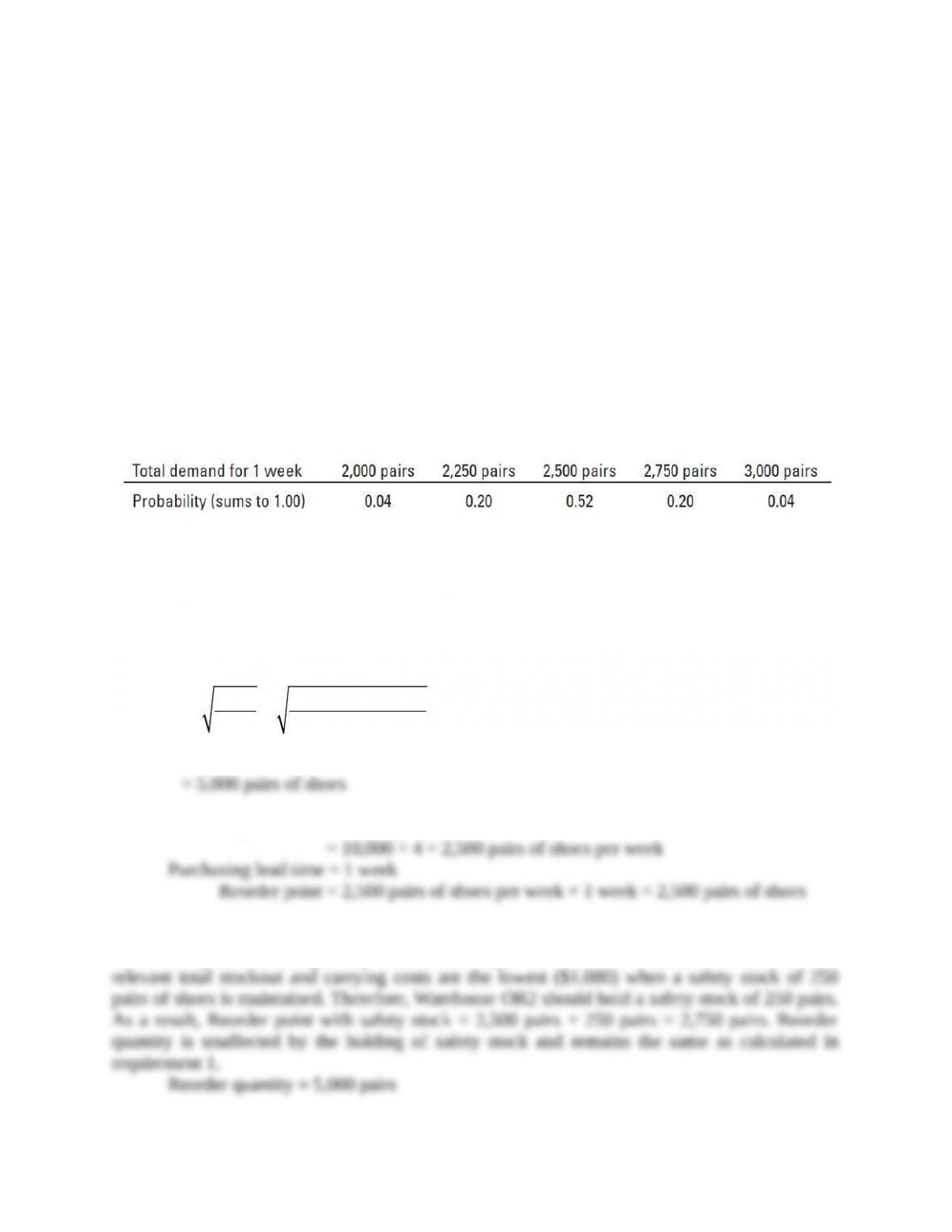

20-25 (30 min.) EOQ, uncertainty, safety stock, reorder point.

Chadwick Shoe Co. produces and sells an excellent-quality walking shoe. After production, the

shoes are distributed to 20 warehouses around the country. Each warehouse services approximately

100 stores in its region. Chadwick uses an EOQ model to determine the number of pairs of shoes

to order for each warehouse from the factory. Annual demand for Warehouse OR2 is

approximately 120,000 pairs of shoes. The ordering cost is $250 per order. The annual carrying

cost of a pair of shoes is $2.40 per pair.

Required:

1. Use the EOQ model to determine the optimal number of pairs of shoes per order.

2. Assume each month consists of approximately 4 weeks. If it takes 1 week to receive an order,

at what point should warehouse OR2 reorder shoes?

3. Although OR2’s average weekly demand is 2,500 pairs of shoes (120,000 ÷ 12 months ÷ 4

weeks), demand each week may vary with the following probability distribution:

If a store wants shoes and OR2 has none in stock, OR2 can “rush” them to the store at an additional

cost of $2 per pair. How much safety stock should Warehouse OR2 hold? How will this affect the

reorder point and reorder quantity?

SOLUTION

1.

2 DP 2 120,000 $250

EOQ C $2.40

==

= 5,000 pairs of shoes

2. Weekly demand = Monthly demand ÷ 4

= 10,000 ÷ 4 = 2,500 pairs of shoes per week

Purchasing lead time = 1 week

Reorder point = 2,500 pairs of shoes per week × 1 week = 2,500 pairs of shoes

3. Solution Exhibit 20-25 presents the safety stock computations for Warehouse OR2 when

the reorder point excluding safety stock is 2,500 pairs of shoes. The exhibit shows that annual

relevant total stockout and carrying costs are the lowest ($1,080) when a safety stock of 250 pairs

of shoes is maintained. Therefore, Warehouse OR2 should hold a safety stock of 250 pairs. As a

result, Reorder point with safety stock = 2,500 pairs + 250 pairs = 2,750 pairs. Reorder quantity is

unaffected by the holding of safety stock and remains the same as calculated in requirement 1.

Reorder quantity = 5,000 pairs

Warehouse OR2 should order 5,000 pairs of shoes each time its inventory of shoes falls to 2,750

pairs.

20-9

SOLUTION EXHIBIT 20-25

Computation of Safety Stock for Warehouse OR2 When Reorder Point is 2,500 Units

Safety

Stock

Level

in Units

(1)

Demand

Levels

Resulting

in

Stockouts

(2)

Stockout

in Unitsa

(3) =

(2) – 2,500 –

(1)

Probability

of

Stockouts

(4)

Relevant

Stockout

Costsb

(5) =

(3) × $2

Number

of

Orders

per Yearc

(6)

Expected

Stockout

Costsd

(7) =

(4) × (5) ×

(6)

Relevant

Carrying

Costse

(8) =

(1) × $2.40

Relevant

Total

Costs

(9) =

(7) + (8)

0

2,750

250

0.20

$ 500

24

$2,400

3,000

500

0.04

1,000

24

960

$3,360

$ 0

$3,360

250

3,000

250

0.04

500

24

$ 480

$ 600

$1,080

500

—

—

—

—

—

$ 0f

$1,200

$1,200

aDemand level resulting in stockouts – Inventory available during lead time (excluding safety stock), 2,500 units –

Safety stock.

bStockout in units × Relevant stockout costs of $2.00 per unit.

cAnnual demand, 120,000 ÷ 5,000 EOQ = 24 orders per year.

dProbability of stockout × Relevant stockout costs × Number of orders per year.

eSafety stock × Annual relevant carrying costs of $2.40 per unit (assumes that safety stock is on hand at all times and

that there is no overstocking caused by decreases in expected usage).

fAt a safety stock level of 500 units, no stockout will occur and, hence, expected stockout costs = $0.

20-10

20-26 (30 min.) EOQ, uncertainty, safety stock, reorder point.

Stewart Corporation is a major automobile manufacturer. It purchases steering wheels from Coase

Corporation. Annual demand is 10,400 steering wheels per year or 200 steering wheels per week.

The ordering cost is $100 per order. The annual carrying cost is $13 per steering wheel. It currently

takes 1.5 weeks to supply an order to the assembly plant.

Required:

1. What is the optimal number of steering wheels that Stewart’s managers should order according

to the EOQ model?

2. At what point should managers reorder the steering wheels, assuming that both demand and

purchase-order lead time are known with certainty?

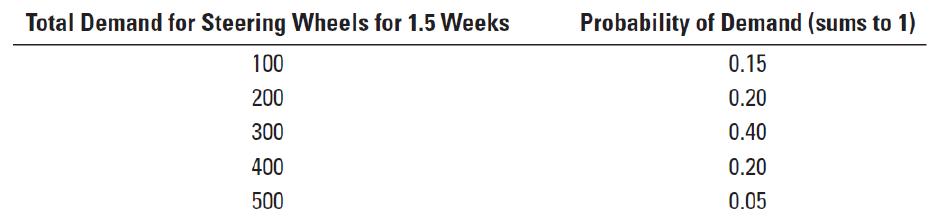

3. Now assume that demand can vary during the 1.5-week purchase-order lead time. The

following table shows the probability distribution of various demand levels:

If Stewart runs out of stock, it would have to rush order the steering wheels at an additional

cost of $9 per steering wheel. How much safety stock should the assembly plant hold? How

will this affect the reorder point and reorder quantity.