15-1

CHAPTER 15

ALLOCATION OF SUPPORT-DEPARTMENT COSTS,

COMMON COSTS, AND REVENUES

15-1 The single-rate (cost-allocation) method makes no distinction between fixed costs and

variable costs in the cost pool. It allocates costs in each cost pool to cost objects using the same

rate per unit of the single allocation base. The dual-rate (cost-allocation) method classifies costs in

each cost pool into two pools—a variable-cost pool and a fixed-cost pool—with each pool using a

different cost-allocation base.

15-2 The dual-rate method provides information to division managers about cost behavior.

Knowing how fixed costs and variable costs behave differently is useful in decision making.

15-3 Budgeted cost rates motivate the manager of the support department to improve efficiency

because the support department bears the risk of any unfavorable cost variances.

15-4 Examples of bases used to allocate support department cost pools to operating departments

include the number of employees, square feet of space, number of direct labor hours, and machine-

hours.

15-5 The use of budgeted indirect cost allocation rates rather than actual indirect rates has

several attractive features to the manager of a user department:

a. The user knows the costs in advance and can factor them into ongoing operating

choices.

b. The cost allocated to a particular user department does not depend on the amount of

resources used by other user departments.

c. Inefficiencies at the department providing the service do not affect the costs allocated

to the user department.

15-6 Disagree. Allocating costs on “the basis of estimated long-run use by user department

managers” means department managers can lower their cost allocations by deliberately

underestimating their long-run use (assuming all other managers do not similarly underestimate

their usage).

15-7 The three methods differ in how they recognize reciprocal services among support

departments:

a. The direct (allocation) method ignores any services rendered by one support

department to another; it allocates each support department’s costs directly to the

operating departments.

b. The step-down (allocation) method allocates support-department costs to other support

departments and to operating departments in a sequential manner that partially

recognizes the mutual services provided among all support departments.

c. The reciprocal (allocation) method allocates support-department costs to operating

departments by fully recognizing the mutual services provided among all support

departments.

15-2

15-8 The reciprocal method is theoretically the most defensible method because it fully

recognizes the mutual services provided among all departments, irrespective of whether those

departments are operating or support departments.

15-9 The stand-alone cost-allocation method uses information pertaining to each user of a cost

object as a separate entity to determine the cost-allocation weights.

The incremental cost-allocation method ranks the individual users of a cost object in the

order of users most responsible for the common costs and then uses this ranking to allocate costs

among those users. The first-ranked user of the cost object is the primary user and is allocated

costs up to the costs of the primary user as a stand-alone user. The second-ranked user is the first

incremental user and is allocated the additional cost that arises from two users instead of only the

primary user. The third-ranked user is the second incremental user and is allocated the additional

cost that arises from three users instead of two users, and so on.

The Shapley Value method calculates an average cost based on the costs allocated to each

user as first the primary user, the second-ranked user, the third-ranked user, and so on.

15-10 All contracts with U.S. government agencies must comply with cost accounting standards

issued by the Cost Accounting Standards Board (CASB).

15-11 Areas of dispute between contracting parties can be reduced by making the “rules of the

game” explicit and in writing at the time the contract is signed.

15-12 Companies increasingly are selling packages of products or services for a single price.

Revenue allocation is required when managers in charge of developing or marketing individual

products in a bundle are evaluated using product-specific revenues.

15-13 The stand-alone revenue-allocation method uses product-specific information on the

products in the bundle as weights for allocating the bundled revenues to the individual products.

The incremental revenue allocation method ranks individual products in a bundle according

to criteria determined by management—such as the product in the bundle with the most sales—

and then uses this ranking to allocate bundled revenues to the individual products. The first-ranked

product is the primary product in the bundle and is allocated revenue up to the revenue of the

primary product as a stand-alone product. The second-ranked product is the first incremental

product and is allocated the additional revenue that arises from two products instead of only the

primary product. The third-ranked product is the second incremental product and is allocated the

additional revenue that arises from three products instead of two products, and so on.

15-14 Managers typically will argue that their individual product is the prime reason why

consumers buy a bundle of products. Evidence on this argument could come from the sales of the

products when sold as individual products. Other pieces of evidence include surveys of users of

each product and surveys of people who purchase the bundle of products.

15-3

15-15 A dispute over allocation of revenues of a bundled product could be resolved by

(a) having an agreement that outlines the preferred method in the case of a dispute, or (b) having

a third party (such as the company president or an independent arbitrator) make a decision.

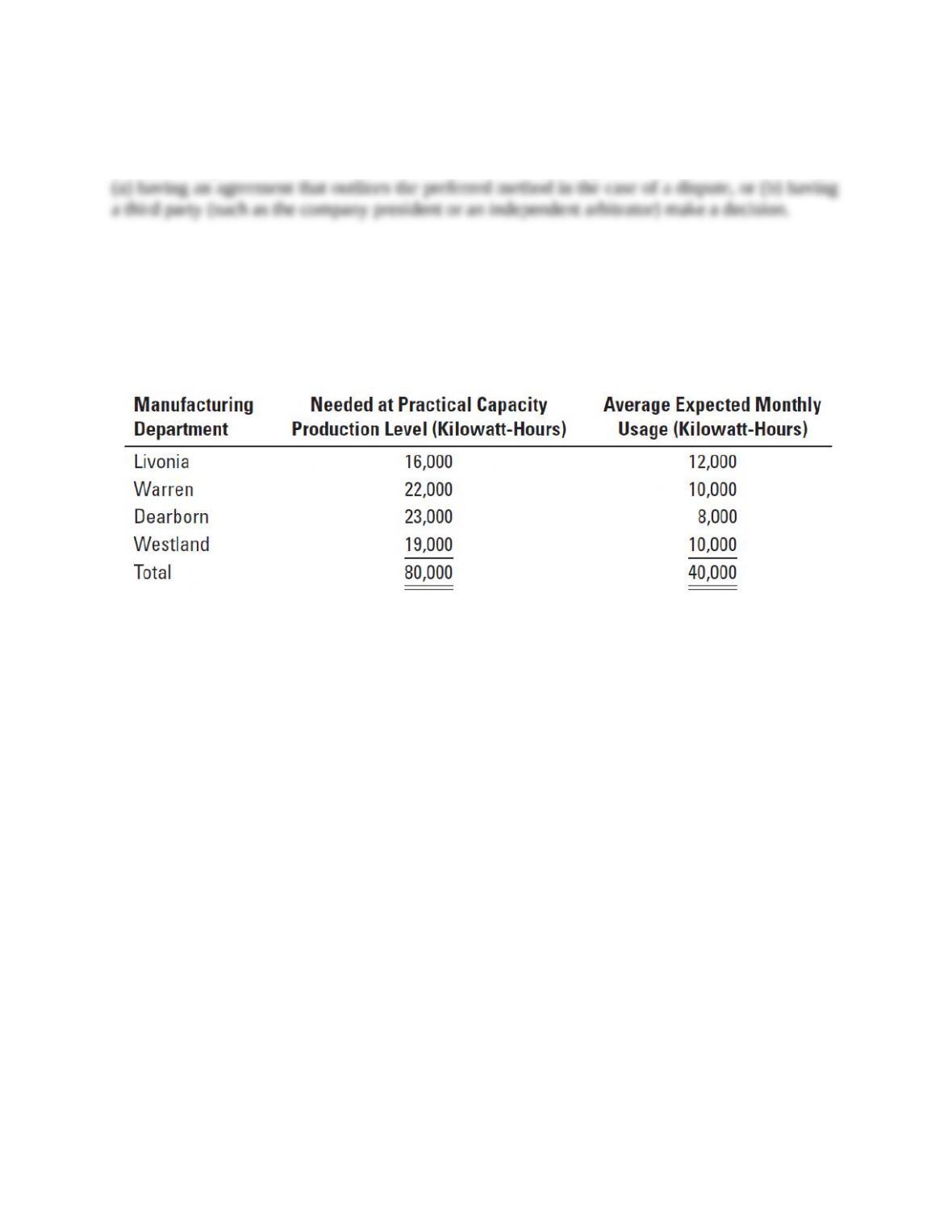

15-16 (20 min.) Single-rate versus dual-rate methods, support department.

The Detroit power plant that services all manufacturing departments of MidWest Engineering has

a budget for the coming year. This budget has been expressed in the following monthly terms:

The expected monthly costs for operating the power plant during the budget year are $21,600:

$4,000 variable and $17,600 fixed.

Required:

1. Assume that a single cost pool is used for the power plant costs. What budgeted amounts will

be allocated to each manufacturing department if (a) the rate is calculated based on practical

capacity and costs are allocated based on practical capacity and (b) the rate is calculated based

on expected monthly usage and costs are allocated based on expected monthly usage?

2. Assume the dual-rate method is used with separate cost pools for the variable and fixed costs.

Variable costs are allocated on the basis of expected monthly usage. Fixed costs are allocated

on the basis of practical capacity. What budgeted amounts will be allocated to each

manufacturing department? Why might you prefer the dual-rate method?

15-4

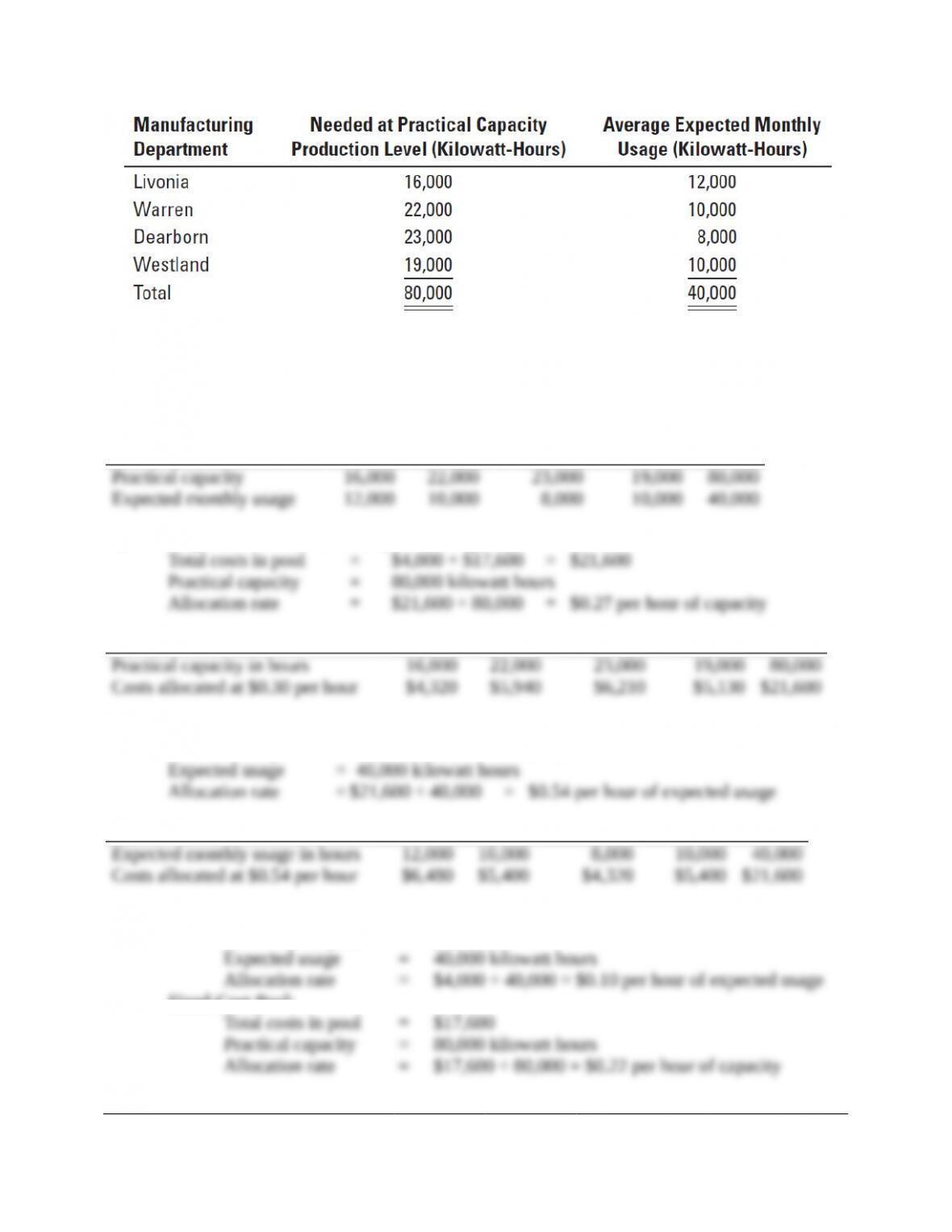

SOLUTION

Bases available (kilowatt hours):

Livonia

Warren

Dearborn

Westland

Total

Practical capacity

Expected monthly usage

16,000

12,000

22,000

10,000

23,000

8,000

19,000

10,000

80,000

40,000

1a. Single-rate method based on practical capacity:

Total costs in pool = $4,000 + $17,600 = $21,600

Practical capacity = 80,000 kilowatt hours

Allocation rate = $21,600 ÷ 80,000 = $0.27 per hour of capacity

Livonia

Warren

Dearborn

Westland

Total

Practical capacity in hours

Costs allocated at $0.30 per hour

16,000

$4,320

22,000

$5,940

23,000

$6,210

19,000

$5,130

80,000

$21,600

8

1b. Single-rate method based on expected monthly usage:

Total costs in pool = $4,000 + $17,600 = $21,600

Expected usage = 40,000 kilowatt hours

Allocation rate = $21,600 ÷ 40,000 = $0.54 per hour of expected usage

Livonia

Warren

Dearborn

Westland

Total

Expected monthly usage in hours

Costs allocated at $0.54 per hour

12,000

$6,480

10,000

$5,400

8,000

$4,320

10,000

$5,400

40,000

$21,600

2. Variable-Cost Pool:

Total costs in pool = $4,000

Expected usage = 40,000 kilowatt hours

Allocation rate = $4,000 ÷ 40,000 = $0.10 per hour of expected usage

Fixed-Cost Pool:

Total costs in pool = $17,600

Practical capacity = 80,000 kilowatt hours

Allocation rate = $17,600 ÷ 80,000 = $0.22 per hour of capacity

Livonia

Warren

Dearborn

Westland

Total

Variable-cost pool

$0.10 × 12,000; 10,000; 8,000, 10,000

Fixed-cost pool

$0.22 × 16,000; 22,000; 23,000, 19,000

Total

$1,200

3,520

$4,720

$1,000

4,840

$5,840

$ 800

5,060

$5,860

$1,000

4,180

$5,180

$ 4,000

17,600

$21,600

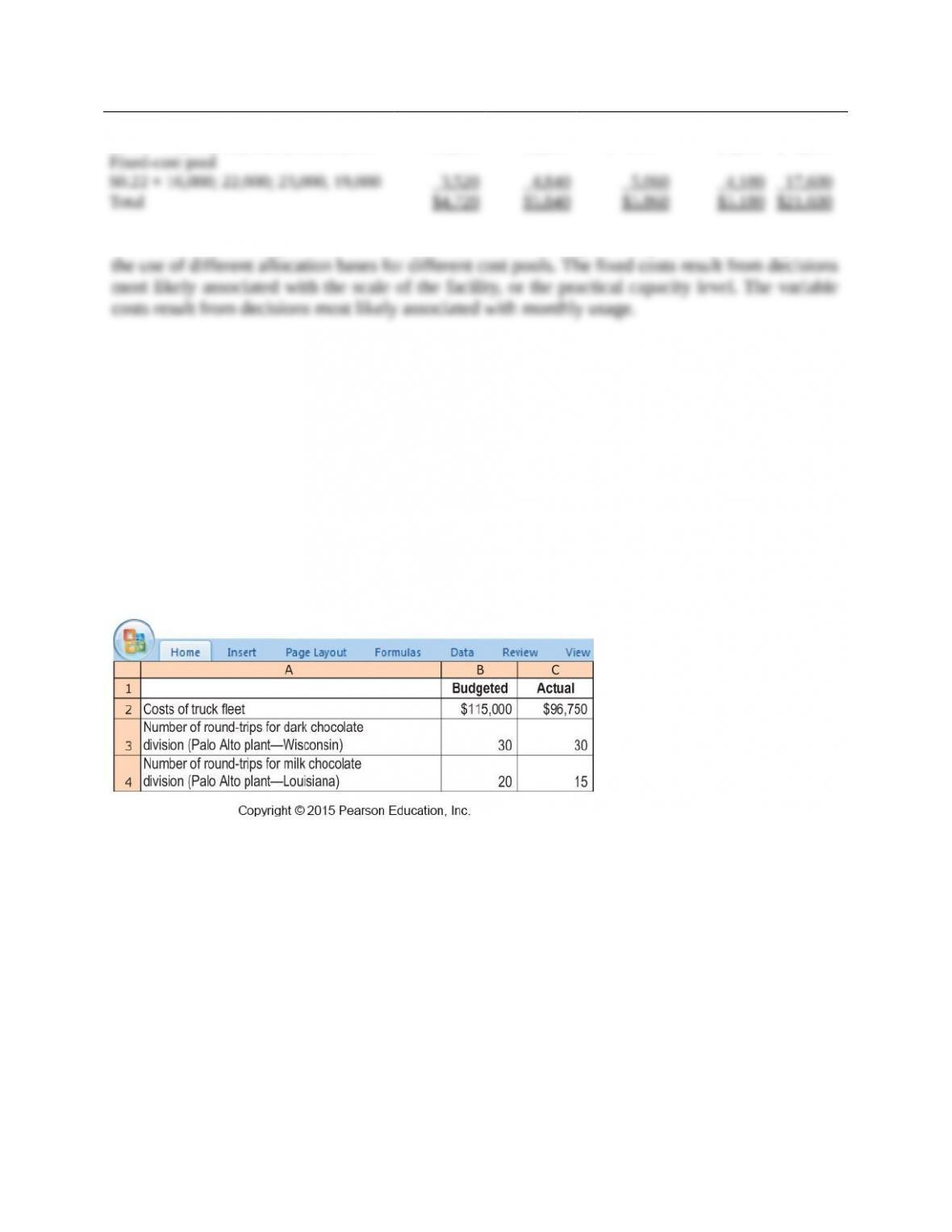

The dual-rate method permits a more refined allocation of the power department costs; it permits

the use of different allocation bases for different cost pools. The fixed costs result from decisions

most likely associated with the scale of the facility, or the practical capacity level. The variable

costs result from decisions most likely associated with monthly usage.

15-5

15-17 (20–25 min.) Single-rate method, budgeted versus actual costs and quantities.

Chocolat Inc. is a producer of premium chocolate based in Palo Alto. The company has a separate

division for each of its two products: dark chocolate and milk chocolate. Chocolat purchases

ingredients from Wisconsin for its dark chocolate division and from Louisiana for its milk

chocolate division. Both locations are the same distance from Chocolat’s Palo Alto plant.

Chocolat Inc. operates a fleet of trucks as a cost center that charges the divisions for variable

costs (drivers and fuel) and fixed costs (vehicle depreciation, insurance, and registration fees) of

operating the fleet. Each division is evaluated on the basis of its operating income. For 2013, the

trucking fleet had a practical capacity of 50 round-trips between the Palo Alto plant and the two

suppliers. It recorded the following information:

Required:

1. Using the single-rate method, allocate costs to the dark chocolate division and the milk

chocolate division in these three ways.

a. Calculate the budgeted rate per round-trip and allocate costs based on round-trips budgeted

for each division.

b. Calculate the budgeted rate per round-trip and allocate costs based on actual round-trips

used by each division.

c. Calculate the actual rate per round-trip and allocate costs based on actual round-trips used

by each division.

2. Describe the advantages and disadvantages of using each of the three methods in requirement

1. Would you encourage Chocolat Inc. to use one of these methods? Explain and indicate any

assumptions you made.

SOLUTION

1. a. Budgeted rate =

Budgeted indirect costs

Budgeted trips

= $115,000/50 trips = $2,300 per round-trip

Indirect costs allocated to Dark C. Division = $2,300 per round-trip

30 budgeted round trips

= $69,000

15-6

Indirect costs allocated to Milk C. Division = $2,300 per round-trip

20 budgeted round trips

= $46,000

b. Budgeted rate = $2,300 per round-trip

Indirect costs allocated to Dark C. Division = $2,300 per round-trip

30 actual round trips

= $69,000

Indirect costs allocated to Milk C. Division = $2,300 per round-trip

15 actual round trips

= $34,500

c. Actual rate =

Actual indirect costs

Actual trips

= $96,750/ 45 trips = $2,150 per round-trip

Indirect costs allocated to Dark C. Division = $2,150 per round-trip

30 actual round trips

= $64,500

Indirect costs allocated to Milk C. Division = $2,150 per round-trip

15 actual round trips

= $32,250

2. When budgeted rates/budgeted quantities are used, the Dark Chocolate and Milk Chocolate

Divisions know at the start of 2013 that they will be charged a total of $69,000 and $46,000,

respectively, for transportation. In effect, the fleet resource becomes a fixed cost for each division.

Then, each may be motivated to over-use the trucking fleet, knowing that their 2013 transportation

costs will not change.

When budgeted rates/actual quantities are used, the Dark Chocolate and Milk Chocolate

Divisions know at the start of 2013 that they will be charged a rate of $2,300 per round trip, i.e.,

they know the price per unit of this resource. This enables them to make operating decisions

knowing the rate they will have to pay for transportation. Each can still control its total

transportation costs by minimizing the number of round trips it uses. Assuming that the budgeted

rate was based on honest estimates of their annual usage, this method will also provide an estimate

of the excess trucking capacity (the portion of fleet costs not charged to either division). In contrast,

when actual costs/actual quantities are used, the two divisions must wait until year-end to know

their transportation charges.

The use of actual costs/actual quantities makes the costs allocated to one division a function

of the actual demand of other users. In 2013, the actual usage was 45 trips, which is 5 trips below

the 50 trips budgeted. The Dark Chocolate Division used all the 30 trips it had budgeted. The Milk

Chocolate Division used only 15 of the 20 trips budgeted. When costs are allocated based on actual

costs and actual quantities, the same fixed costs are spread over fewer trips resulting in a higher

rate than if the Milk Chocolate Division had used its budgeted 20 trips. As a result, the Dark

Chocolate Division bears a proportionately higher share of the fixed costs.

Using actual costs/actual rates also means that any efficiencies or inefficiencies of the

trucking fleet get passed along to the user divisions. In general, this will have the effect of making

the truck fleet less careful about its costs although, in 2013, it appears to have managed its costs

well, leading to a lower actual cost per roundtrip relative to the budgeted cost per round trip.

15-7

For the reasons stated previously, of the three single-rate methods suggested in this

problem, the budgeted rate and actual quantity may be the best one to use. (The management of

Chocolate would have to ensure that the managers of the Dark Chocolate and Milk Chocolate

divisions do not systematically overestimate their budgeted use of the fleet division in an effort to

drive down the budgeted rate).

15-18 (20 min.) Dual-rate method, budgeted versus actual costs, and practical capacity

versus actual quantities (continuation of 15-17).

Chocolat Inc. decides to examine the effect of using the dual-rate method for allocating truck costs

to each round- trip. At the start of 2013, the budgeted costs were as follows:

The actual results for the 45 round-trips made in 2013 were as follows:

Assume all other information to be the same as in Exercise 15-17.

Required:

1. Using the dual-rate method, what are the costs allocated to the dark chocolate division and the

milk chocolate division when (a) variable costs are allocated using the budgeted rate per round–

trip and actual round-trips used by each division and when (b) fixed costs are allocated based

on the budgeted rate per round-trip and round-trips budgeted for each division?

2. From the viewpoint of the dark chocolate division, what are the effects of using the dual-rate

method rather than the single-rate method?

SOLUTION

1. Charges with dual rate method.

Variable indirect cost rate = $1,350 per trip

Fixed indirect cost rate = $47,500 budgeted costs/ 50 round trips budgeted

= $950 per trip

15-8

Dark Chocolate Division

Variable indirect costs, $1,350 × 30 $40,500

Fixed indirect costs, $950 × 30 28,500

$69,000

Milk Chocolate Division

Variable indirect costs, $1,350 × 15 $20,250

Fixed indirect costs, $950 × 20 19,000

$39,250

2. The dual rate changes how the fixed indirect cost component is treated. By using budgeted

trips made, the Dark Chocolate Division is unaffected by changes from its own budgeted usage or

that of other divisions. When budgeted rates and actual trips are used for allocation (see

requirement 1.b. of problem 15-17), the Dark Chocolate Division is assigned the same $28,500 for

fixed costs as under the dual-rate method because it made the same number of trips as budgeted.

However, note that the Milk Chocolate Division is allocated $19,000 in fixed trucking costs under

the dual-rate system, compared to $950 15 actual trips = $14,250 when actual trips are used for

allocation. As such, the Dark Chocolate Division is not made to appear disproportionately more

expensive than the Milk Chocolate Division simply because the latter did not make the number of

trips it budgeted at the start of the year.

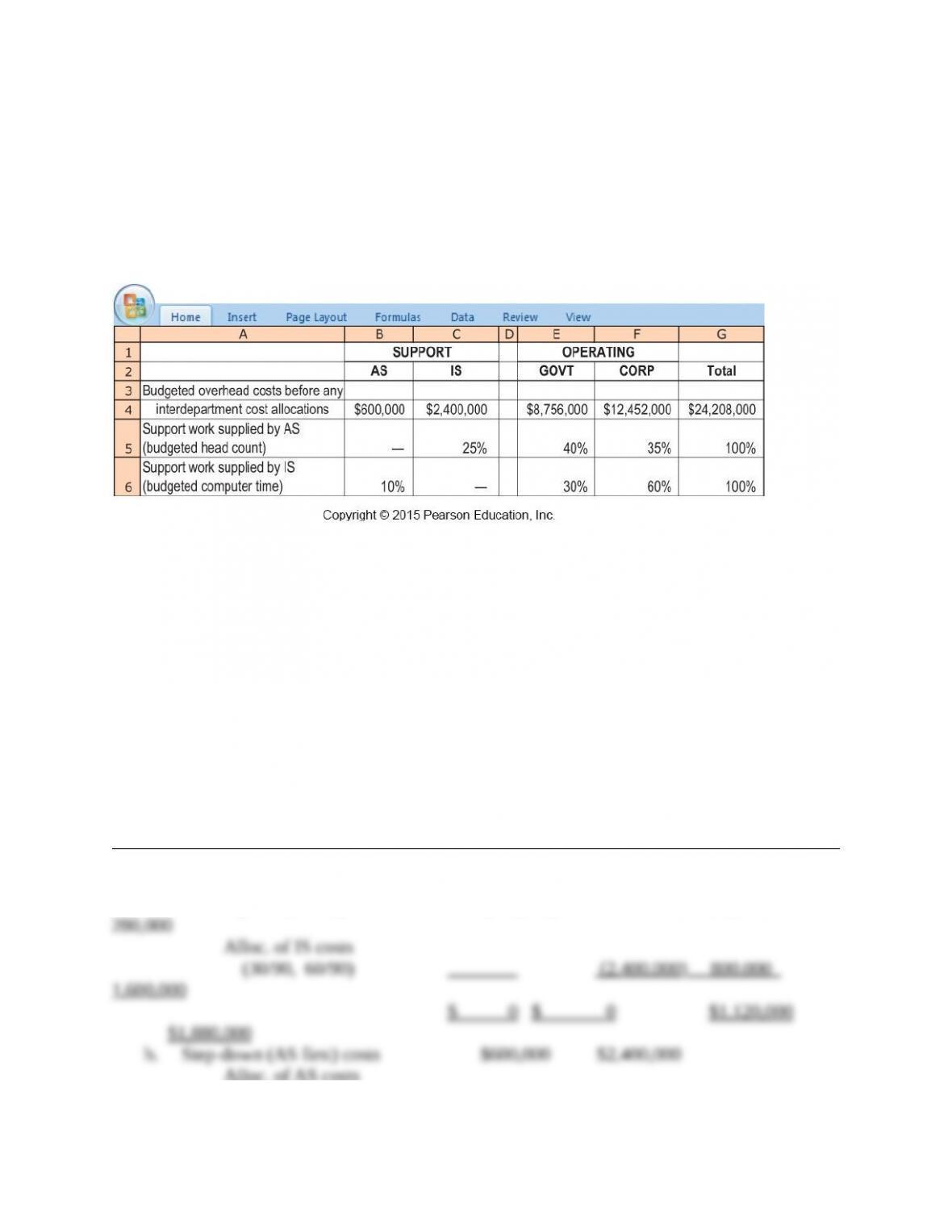

15-19 (30 min.) Support department cost allocation; direct and step-down methods.

Phoenix Partners provides management consulting services to government and corporate clients.

Phoenix has two support departments—administrative services (AS) and information systems

(IS)—and two operating departments—government consulting (GOVT) and corporate consulting

(CORP). For the first quarter of 2013, Phoenix’s cost records indicate the following:

A

Required:

1. Allocate the two support departments’ costs to the two operating departments using the

following methods:

a. Direct method

b. Step-down method (allocate AS first)

c. Step-down method (allocate IS first)

15-9

2. Compare and explain differences in the support-department costs allocated to each operating

department.

3. What approaches might be used to decide the sequence in which to allocate support

departments when using the step-down method?

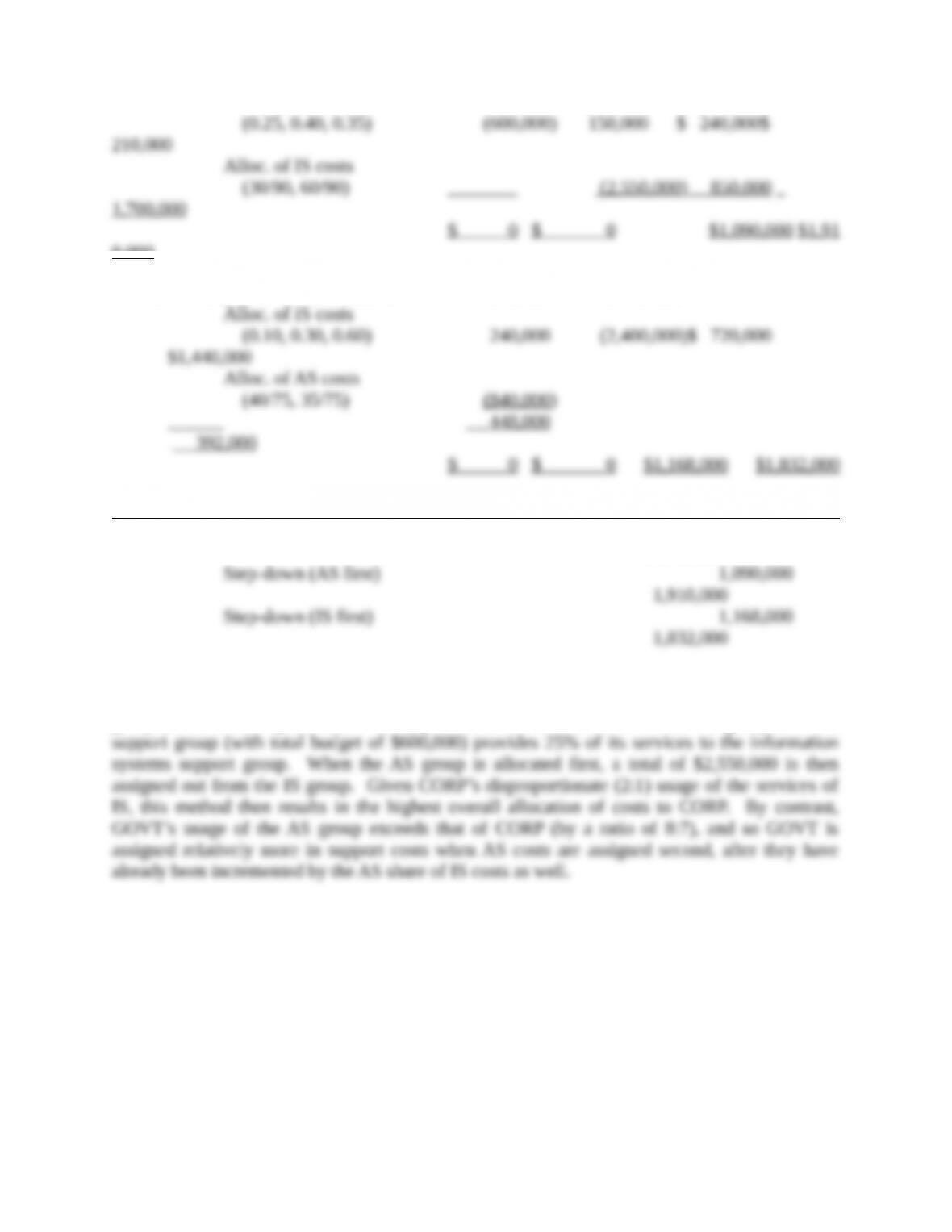

SOLUTION

1. AS IS GOVT CORP

a. Direct method costs $600,000 $2,400,000

Alloc. of AS costs

(40/75, 35/75) (600,000) $ 320,000 $ 280,000

Alloc. of IS costs

(30/90, 60/90) (2,400,000) 800,000 1,600,000

$ 0 $ 0 $1,120,000 $1,880,000

b. Step-down (AS first) costs $600,000 $2,400,000

Alloc. of AS costs

(0.25, 0.40, 0.35) (600,000) 150,000 $ 240,000 $ 210,000

Alloc. of IS costs

(30/90, 60/90) (2,550,000) 850,000 1,700,000

$ 0 $ 0 $1,090,000 $1,910,000

c. Step-down (IS first) costs $600,000 $2,400,000

Alloc. of IS costs

(0.10, 0.30, 0.60) 240,000 (2,400,000) $ 720,000 $1,440,000

Alloc. of AS costs

(40/75, 35/75) (840,000) 448,000 392,000

$ 0 $ 0 $1,168,000 $1,832,000

2. GOVT CORP

Direct method $1,120,000 $1,880,000

Step-down (AS first) 1,090,000 1,910,000

Step-down (IS first) 1,168,000 1,832,000

The direct method ignores any services to other support departments. The step-down method

partially recognizes services to other support departments. The information systems support group

(with total budget of $2,400,000) provides 10% of its services to the AS group. The AS support

group (with total budget of $600,000) provides 25% of its services to the information systems

support group. When the AS group is allocated first, a total of $2,550,000 is then assigned out

from the IS group. Given CORP’s disproportionate (2:1) usage of the services of IS, this method

then results in the highest overall allocation of costs to CORP. By contrast, GOVT’s usage of the

AS group exceeds that of CORP (by a ratio of 8:7), and so GOVT is assigned relatively more in

support costs when AS costs are assigned second, after they have already been incremented by the

AS share of IS costs as well.

15-10

3. Three criteria that could determine the sequence in the step-down method are as follows:

a. Allocate support departments on a ranking of the percentage of their total services

provided to other support departments.

1. Administrative Services 25%

2. Information Systems 10%

b. Allocate support departments on a ranking of the total dollar amount in the support

departments.

1. Information Systems $2,400,000

2. Administrative Services $ 600,000

c. Allocate support departments on a ranking of the dollar amounts of service provided to

other support departments

1. Information Systems

(0.10 $2,400,000) = $240,000

2. Administrative Services

(0.25 $600,000) = $150,000

The approach in (a) above typically better approximates the theoretically preferred reciprocal

method. It results in a higher percentage of support-department costs provided to other support

departments being incorporated into the step-down process than does (b) or (c), above.

15-20 (50 min.) Support-department cost allocation, reciprocal method (continuation of 15-19).

Refer to the data given in Exercise 15-19.

Required:

1. Allocate the two support departments’ costs to the two operating departments using the

reciprocal method. Use (a) linear equations and (b) repeated iterations.

2. Compare and explain differences in requirement 1 with those in requirement 1 of Exercise 15-

19. Which method do you prefer? Why?