14-1

N CHAPTER 14

COST ALLOCATION, CUSTOMER-PROFITABILITY

ANALYSIS, AND SALES-VARIANCE ANALYSIS

14-1 Disagree. Cost accounting data plays a key role in many management planning and control

decisions. The division president will be able to make better operating and strategy decisions by

being involved in key decisions about cost pools and cost allocation bases. Such an understanding,

for example, can help the division president evaluate the profitability of different customers.

14-2 Customer profitability analysis highlights for managers how individual customers

differentially contribute to total profitability. It helps managers to see whether customers who

contribute sizably to total profitability are receiving a comparable level of attention from the

organization.

14-3 Companies that separately record (a) the list price and (b) the discount have sufficient

information to subsequently examine the level of discounting by each individual customer and by

each individual salesperson.

14-4 No. A customer-profitability profile highlights differences in the current period’s

profitability across customers. Dropping customers should be the last resort. An unprofitable

customer in one period may be highly profitable in subsequent future periods. Moreover, costs

assigned to individual customers need not be purely variable with respect to short-run elimination

of sales to those customers. Thus, when customers are dropped, costs assigned to those customers

may not disappear in the short run.

14-5 Five categories in a customer cost hierarchy are identified in the chapter. The examples

given relate to the Provalue Division of Astel Computers used in the chapter:

• Customer output-unit-level costs—costs of activities to sell each unit (computer) to a

customer. An example is product-handling costs of each computer sold.

• Customer batch-level costs—costs of activities that are related to a group of units (computers)

sold to a customer. Examples are costs incurred to process orders or to make deliveries.

• Customer–sustaining costs—costs of activities to support individual customers, regardless of

the number of units or batches of product delivered to the customer. Examples are costs of

visits to customers or costs of displays at customer sites.

• Distribution-channel costs—costs of activities related to a particular distribution channel

rather than to each unit of product, each batch of product, or specific customers. An example

is the salary of the manager of Provalue Division’s wholesale distribution channel.

• Division-sustaining costs—costs of division activities that cannot be traced to individual

customers or distribution channels. An example is the salary of the Provalue Division

manager.

14-6 Charting cumulative profits by customer or product type generates a whale curve. This

provides information on the profitability of customers and clearly differentiates the most profitable

from the least profitable.

14-2

14-7 Disagree. In general, companies have three choices regarding the allocation of corporate

costs to divisions: allocate all corporate costs, allocate some corporate costs (those “controllable”

by the divisions), and allocate none of the corporate costs. Which one of these is appropriate

depends on several factors: the composition of corporate costs, the purpose of the costing exercise,

and the time horizon, to name a few. For example, one can easily justify allocating all corporate

costs when they are closely related to the running of the divisions and when the purpose of costing

is, say, pricing products or motivating managers to consume corporate resources judiciously.

14-8 Exhibit 14-8 lists four criteria used to guide cost allocation decisions:

1. Cause and effect.

2. Benefits received.

3. Fairness or equity.

4. Ability to bear.

The cause-and-effect criterion and the benefits-received criterion are the dominant criteria when

the purpose of the allocation is related to the economic decision purpose or the motivation purpose.

14-9 Disagree. If corporate costs allocated to a division can be reallocated to the indirect cost

pools of the division on the basis of a logical cause-and-effect relationship, then it is in fact

preferable to do so—this will result in fewer division-indirect-cost pools and a more cost-effective

cost allocation system. This reallocation of allocated corporate costs should only be done if the

allocation base used for each division indirect cost pool has the same cause–and-effect relationship

with every cost in that indirect cost pool, including the reallocated corporate cost.

14-10 Disagree. A company will frequently allocate costs that are fixed in the short run to

customers to determine long-run profitability of customers. In the long run, a company must ensure

that the revenues received from a customer exceed the total resources consumed to support the

customer, regardless of whether these costs are variable or fixed in the short run. For short-run

decisions, however, costs that are fixed in the short run may often be irrelevant.

14-11 When allocating costs to divisions, channels, and customers, companies must construct

cost pools that are, to the extent possible, homogeneous, so that all costs in the cost pool have the

same or a similar cause-and-effect or benefits-received relationship with the cost-allocation base.

If each cost category has a cause-and-effect or benefits-received relationship with a different cost-

allocation base, the company should maintain separate cost pools for each of these costs.

Determining homogeneous cost pools requires judgment and should be revisited on a regular basis.

14-12 Using the levels approach introduced in Chapter 7, the sales-volume variance is a Level 2

variance. By sequencing through Level 3 (sales-mix and sales-quantity variances) and then Level 4

(market-size and market-share variances), managers can gain insight into the causes of a specific

sales-volume variance caused by changes in the mix and quantity of the products sold as well as

changes in market size and market share.

14-13 The total sales-mix variance arises from differences in the budgeted contribution margin

of the actual and budgeted sales mix. The composite unit concept enables the effect of individual

product changes to be summarized in a single intuitive number by using weights based on the mix

of individual units in the actual and budgeted mix of products sold.

14-3

14-14 A favorable sales-quantity variance arises because the actual units of all products sold

exceed the budgeted units of all products sold.

14-15 The sales-quantity variance can be decomposed into (a) a market-size variance (which

arises when the actual total market size in units is different from the budgeted market size in units)

and (b) a market share variance (which arises when the actual market share of a company is

different from its budgeted market share). Both variances use the budgeted average contribution

margin per unit.

14-16 (15-20 min.) Cost allocation in hospitals, alternative allocation criteria.

Dave Meltzer vacationed at Lake Tahoe last winter. Unfortunately, he broke his ankle while skiing

and spent two days at the Sierra University Hospital. Meltzer’s insurance company received a

$4,800 bill for his two-day stay. One item that caught Meltzer’s attention was an $11.52 charge

for a roll of cotton. Meltzer is a salesman for Johnson & Johnson and knows that the cost to the

hospital of the roll of cotton is between $2.20 and $3.00. He asked for a breakdown of the $11.52

charge. The accounting office of the hospital sent him the following information:

Meltzer believes the overhead charge is outrageous. He comments, “There was nothing I could do

about it. When they come in and dab your stitches, it’s not as if you can say, ‘Keep your cotton

roll. I brought my own.’”

Required:

1. Compute the overhead rate Sierra University Hospital charged on the cotton roll.

2. What criteria might Sierra use to justify allocation of the overhead items b–i in the preceding

list? Examine each item separately and use the allocation criteria listed in Exhibit 14-8 (page

563) in your answer.

3. What should Meltzer do about the $11.52 charge for the cotton roll?

14-4

SOLUTION

1. Direct costs = $2.40

Indirect costs ($11.52 – $2.40) = $9.12

Overhead rate = $9.12

$2.40 = 380%

2. The answers here are less than clear-cut in some cases.

Overhead Cost Item

Allocation Criteria

Processing of paperwork for purchase

Supply-room management fee

Operating-room and patient-room handling costs

Administrative hospital costs

University teaching-related costs

Malpractice insurance costs

Cost of treating uninsured patients

Profit component

Cause and effect

Benefits received

Cause and effect

Benefits received

Ability to bear

Ability to bear or benefits received

Ability to bear

None. This is not a cost.

3. Assuming that Meltzer’s insurance company is responsible for paying the $4,800 bill,

Meltzer probably can only express outrage at the amount of the bill. The point of this question is

to note that even if Meltzer objects strongly to one or more overhead items, it is his insurance

company that likely has the greater incentive to challenge the bill. Individual patients have very

little power in the medical arena. In contrast, insurance companies have considerable power and

may decide that certain costs are not reimbursable—for example, the costs of treating uninsured

patients.

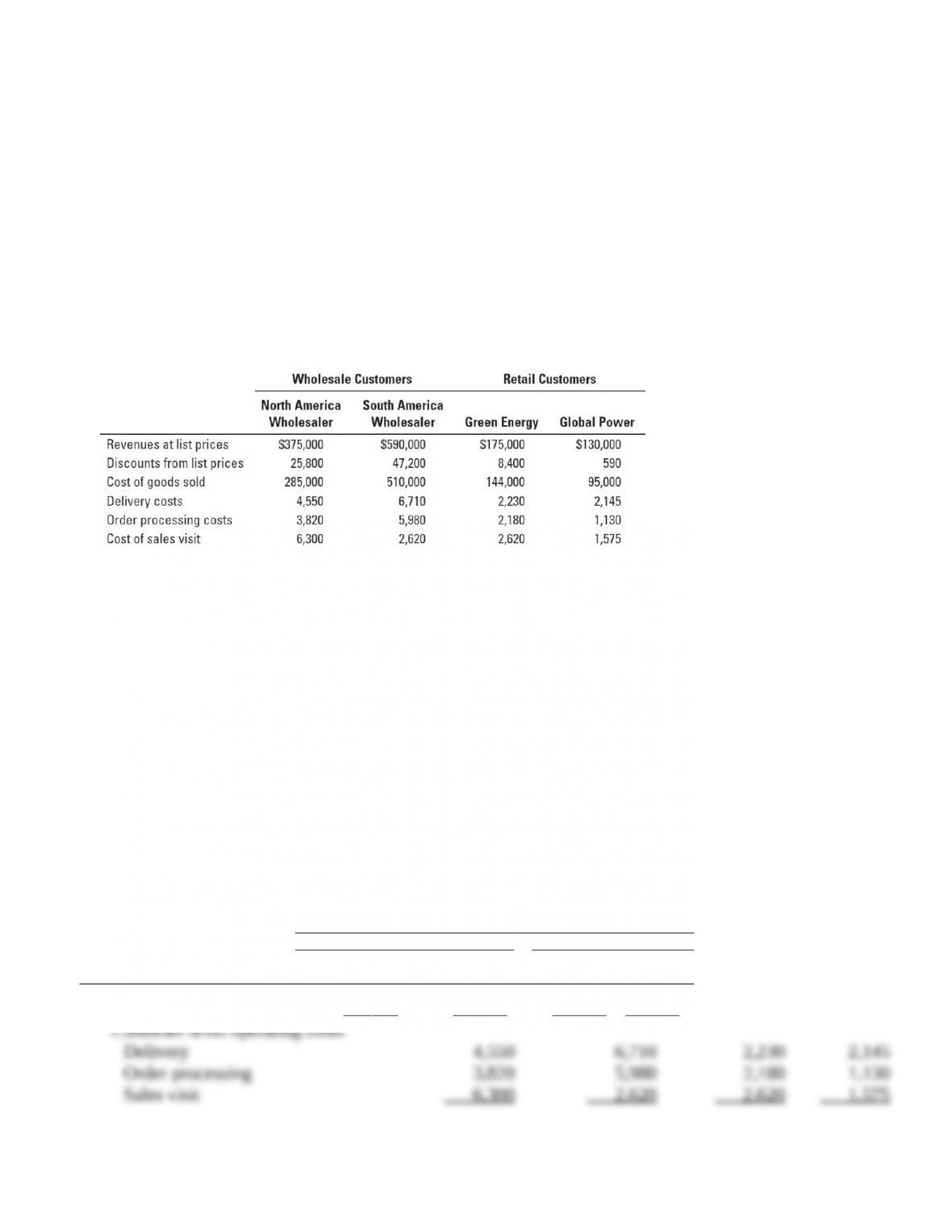

14-17 (30 min.) Customer profitability, customer-cost hierarchy.

Enviro-Tech has only two retail and two wholesale customers. Information relating to each

customer for 2013 follows (in thousands):

Enviro-Tech’s annual distribution-channel costs are $33 million for wholesale customers and $12

million for retail customers. The company’s annual corporate-sustaining costs, such as salary for

top management and general-administration costs, are $48 million. There is no cause-and-effect

or benefits-received relation- ship between any cost-allocation base and corporate-sustaining costs.

That is, Enviro-Tech could save corporate-sustaining costs only if the company completely shuts

down.

Required:

1. Calculate customer-level operating income using the format in Exhibit 14-3.

2. Prepare a customer-cost hierarchy report, using the format in Exhibit 14-6.

3. Enviro-Tech’s management decides to allocate all corporate-sustaining costs to distribution

channels: $38 million to the wholesale channel and $10 million to the retail channel. As a

result, distribution channel costs are now $71 million ($33 million + $38 million) for the

wholesale channel and $22 million ($12 million + $10 million) for the retail channel. Calculate

the distribution channel–level operating income. On the basis of these calculations, what

actions, if any, should Enviro–Tech’s managers take? Explain.

4. How might Enviro-Tech use the new cost information from its activity-based costing system

to better manage its business?

SOLUTION

1.

All amounts in thousands of U.S. dollars

Wholesale

Retail

North America

South America

Green

Global

Wholesaler

Wholesaler

Energy

Power

Revenues at list prices

$375,000

$590,000

$175,000

$130,000

Price discounts

25,800

47,200

8,400

590

Revenues (at actual prices)

349,200

542,800

166,600

129,410

Cost of goods sold

285,000

510,000

144,000

95,000

Gross margin

64,200

32,800

22,600

34,410

Customer-level operating costs

Delivery

4,550

6,710

2,230

2,145

Order processing

3,820

5,980

2,180

1,130

Sales visit

6,300

2,620

2,620

1,575

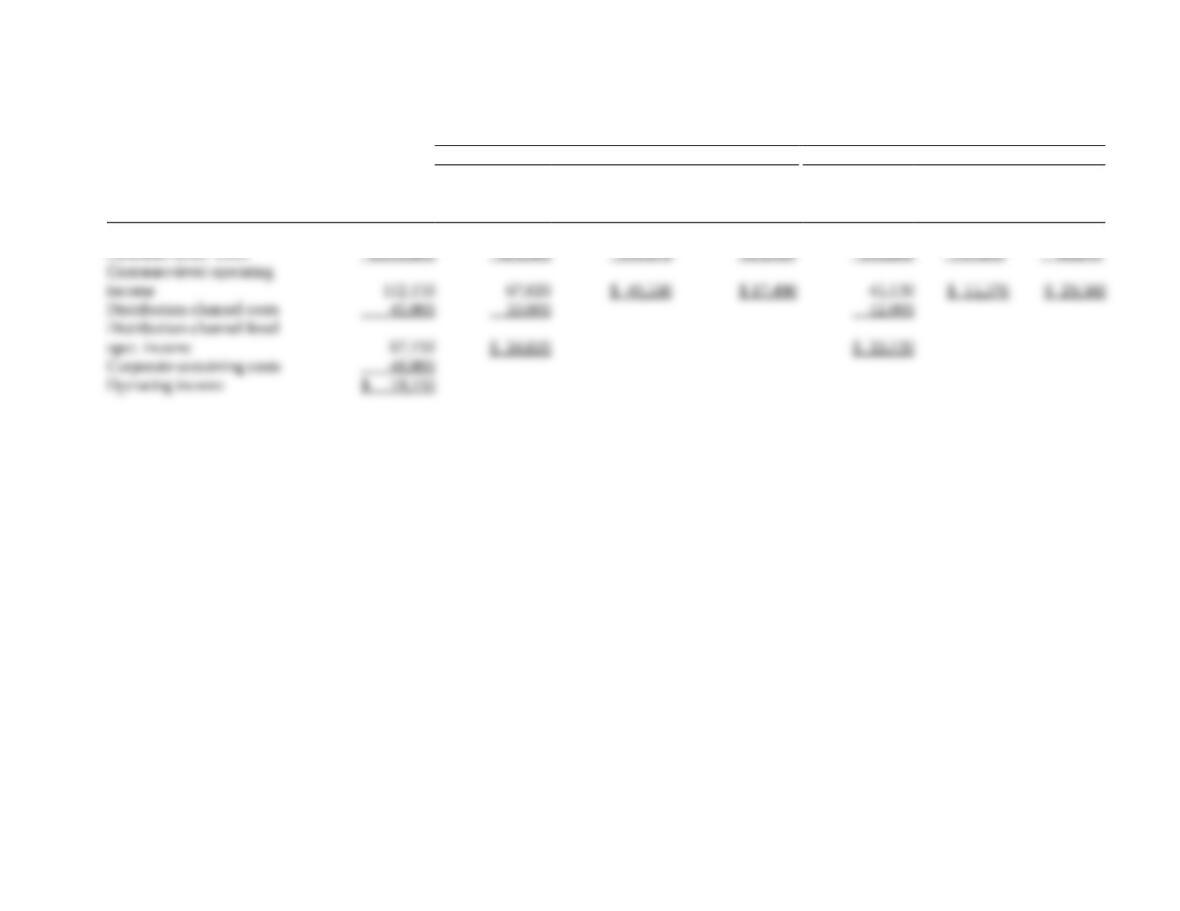

14-6

Total customer-level oper. costs

14,670

15,310

7,030

4,850

Customer-level operating. income

$ 49,530

$ 17,490

$ 15,570

$ 29,560

14-7

2. Customer Distribution Channels

(all amounts in $000s)

Wholesale Customers

Retail Customers

Total

Total

North America

South America

Total

Green

Global

(all customers)

Wholesale

Wholesaler

Wholesaler

Retail

Energy

Power

(1) = (2) + (5)

(2) = (3) + (4)

(3)

(4)

(5) = (6) + (7)

(6)

(7)

Revenues (at actual prices)

$1,188,010

$892,000

$349,200

$542,800

$296,010

$166,600

$129,410

Customer-level costs

1,050,860

824,980

299,670a

525,310a

243,880

151,030a

99,850a

Customer-level operating

income

112,150

67,020

$ 49,530

$ 17,490

45,130

$ 15,570

$ 29,560

Distribution-channel costs

45,000

33,000

12,000

Distribution-channel-level

oper. income

67,150

$ 34,020

$ 33,130

Corporate-sustaining costs

48,000

Operating income

$ 19,150

aCost of goods sold + Total customer-level operating costs from Requirement 1

14-8

3. If corporate costs are allocated to the channels, the retail channel will show an operating

profit of $23,130,000 ($33,130,000 – $10,000,000), and the wholesale channel will show

an operating loss of $3,980,000 ($34,020,000 – $38,000,000). The overall operating profit,

of course, is still $19,150,000, as in requirement 2. There is, however, no cause-and-effect

or benefits-received relationship between corporate costs and any allocation base, i.e., the

allocation of $38,000,000 to the wholesale channel and $10,000,000 to the retail channel

is arbitrary and not useful for decision making. Therefore, the management of Enviro-Tech

should not base any performance evaluations or investment/disinvestment decisions based

on these channel-level operating income numbers. They may want to take corporate costs

into account, however, when making long-run pricing decisions.

4. Enviro-Tech could use activity-based cost information to better manage its business by

evaluating the customer-level costs and determining which activities are providing a value

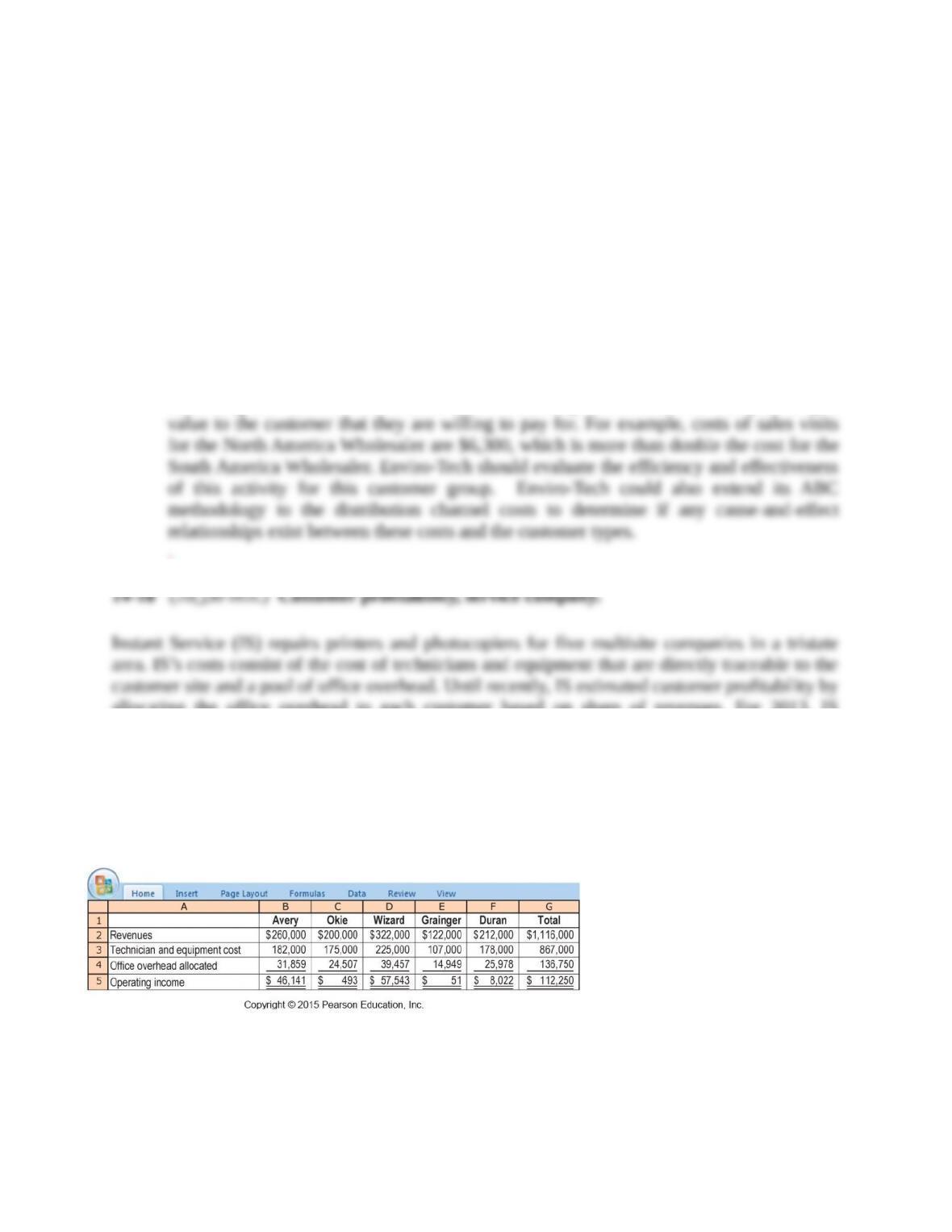

to the customer that they are willing to pay for. For example, costs of sales visits for the

North America Wholesaler are $6,300, which is more than double the cost for the South

America Wholesaler. Enviro-Tech should evaluate the efficiency and effectiveness of this

activity for this customer group. Enviro-Tech could also extend its ABC methodology to

the distribution channel costs to determine if any cause-and-effect relationships exist

between these costs and the customer types.

.

14-18 (20−30 min.) Customer profitability, service company.

Instant Service (IS) repairs printers and photocopiers for five multisite companies in a tristate area.

IS’s costs consist of the cost of technicians and equipment that are directly traceable to the

customer site and a pool of office overhead. Until recently, IS estimated customer profitability by

allocating the office overhead to each customer based on share of revenues. For 2013, IS reported

the following results:

Tina Sherman, IS’s new controller, notes that office overhead is more than 10% of total costs, so

she spends a couple of weeks analyzing the consumption of office overhead resources by

customers. She collects the following information:

14-9

Required:

1. Compute customer-level operating income using the new information that Sherman has

gathered.

2. Prepare exhibits for IS similar to Exhibits 14-4 and 14-5. Comment on the results.

3. What options should IS consider, with regard to individual customers, in light of the new data

and analysis of office overhead?

SOLUTION

1.

Avery

Okie

Wizard

Grainger

Duran

Revenues

$260,000

$200,000

$322,000

$122,000

$212,000

Technician and equipment cost

182,000

175,000

225,000

107,000

178,000

Gross margin

78,000

25,000

97,000

15,000

34,000

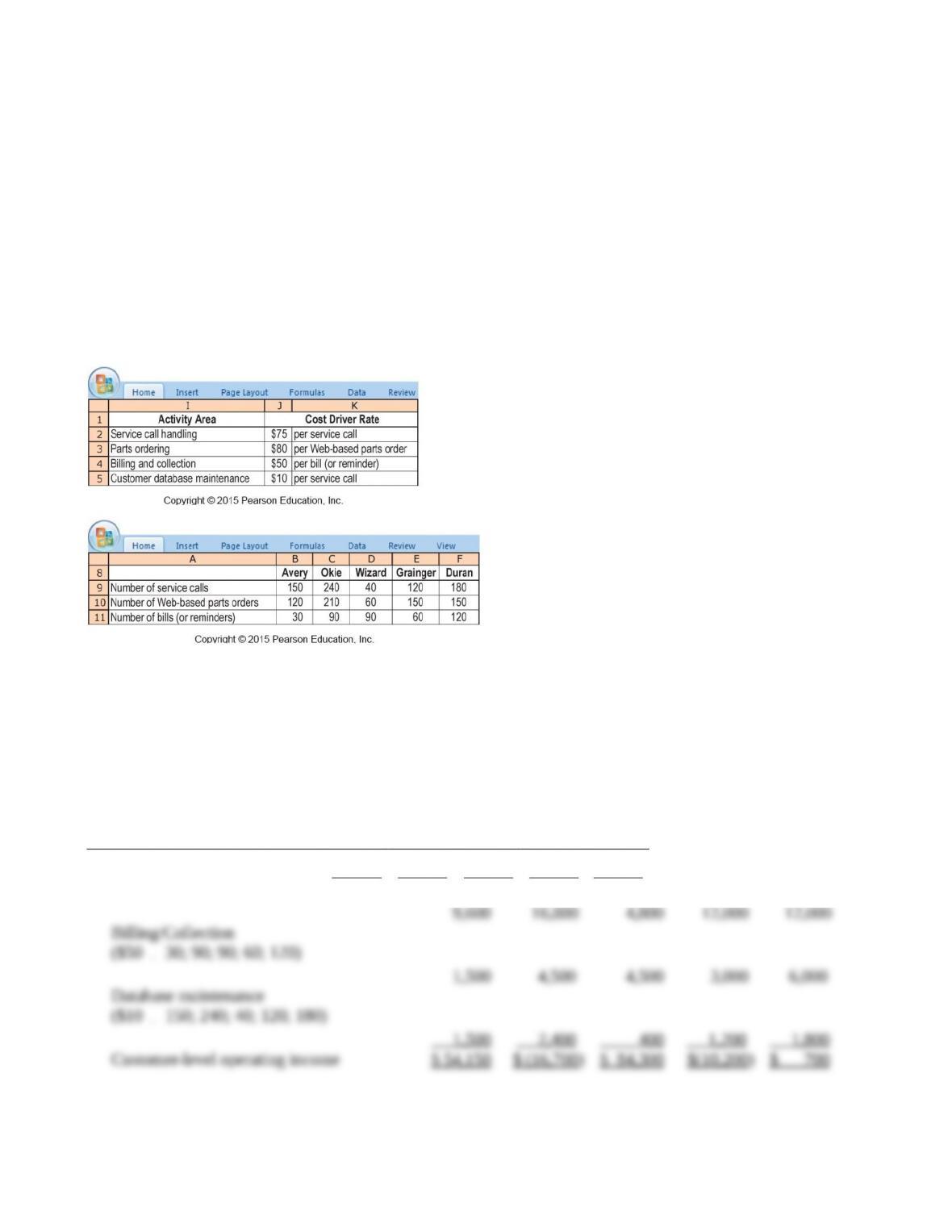

Service call handling

($75

150; 240; 40; 120; 180)

11,250

18,000

3,000

9,000

13,500

Web-based parts ordering

($80

120; 210; 60; 150; 150)

9,600

16,800

4,800

12,000

12,000

Billing/Collection

($50

30; 90; 90; 60; 120)

1,500

4,500

4,500

3,000

6,000

Database maintenance

($10

150; 240; 40; 120; 180)

1,500

2,400

400

1,200

1,800

Customer-level operating income

$ 54,150

$ (16,700)

$ 84,300

$(10,200)

$ 700

2. Customers Ranked on Customer-Level Operating Income

Cumulative

Customer-Level

Operating Income

Customer-Level

Customer-Level

Cumulative

as a % of Total

Operating

Customer

Operating Income

Customer-Level

Customer-Level

Customer

Income

Revenue

as a % of Revenue

Operating Income

Operating Income

Code

(1)

(2)

(3) = (1)

(2)

(4)

(5) = (4)

$112,250

Wizard

$ 84,300

$ 322,000

26.18%

$ 84,300

75%

Avery

54,150

260,000

20.83%

138,450

123%

Duran

700

212,000

0.33%

139,150

124%

Grainger

(10,200)

122,000

–8.36%

128,950

115%

Okie

(16,700)

200,000

–8.35%

112,250

100%

$112,250

$1,116,000

The table and graph above present the summary results.

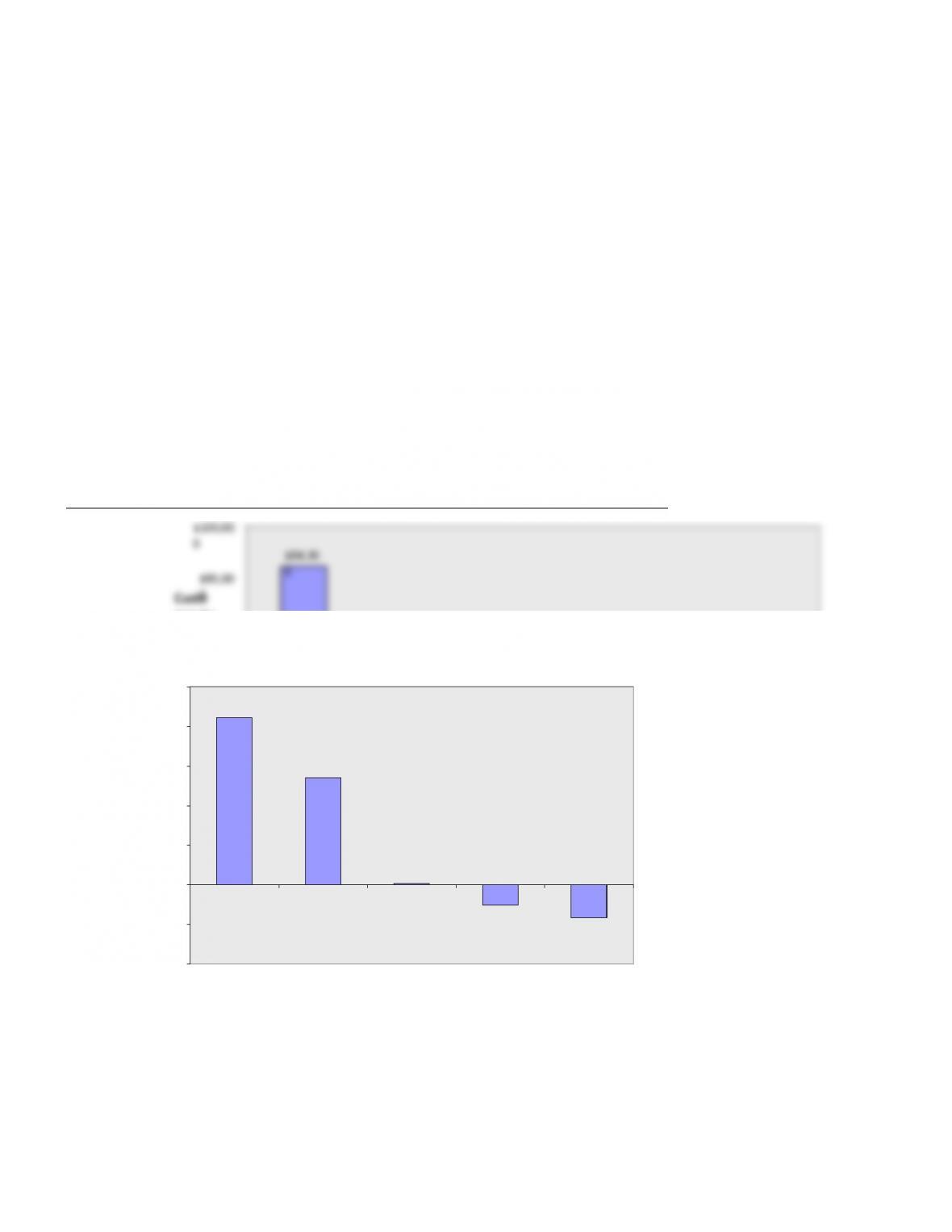

Customer-Level Operating Income

$84,300

$54,150

$700

$(10,200)

$(16,700)

-$40,000

-$20,000

$0

$20,000

$40,000

$60,000

$80,000

$100,000

Customers

Customer-Level Operating Income

Grainger

Avery

Okie

Duran

Wizard

14-11

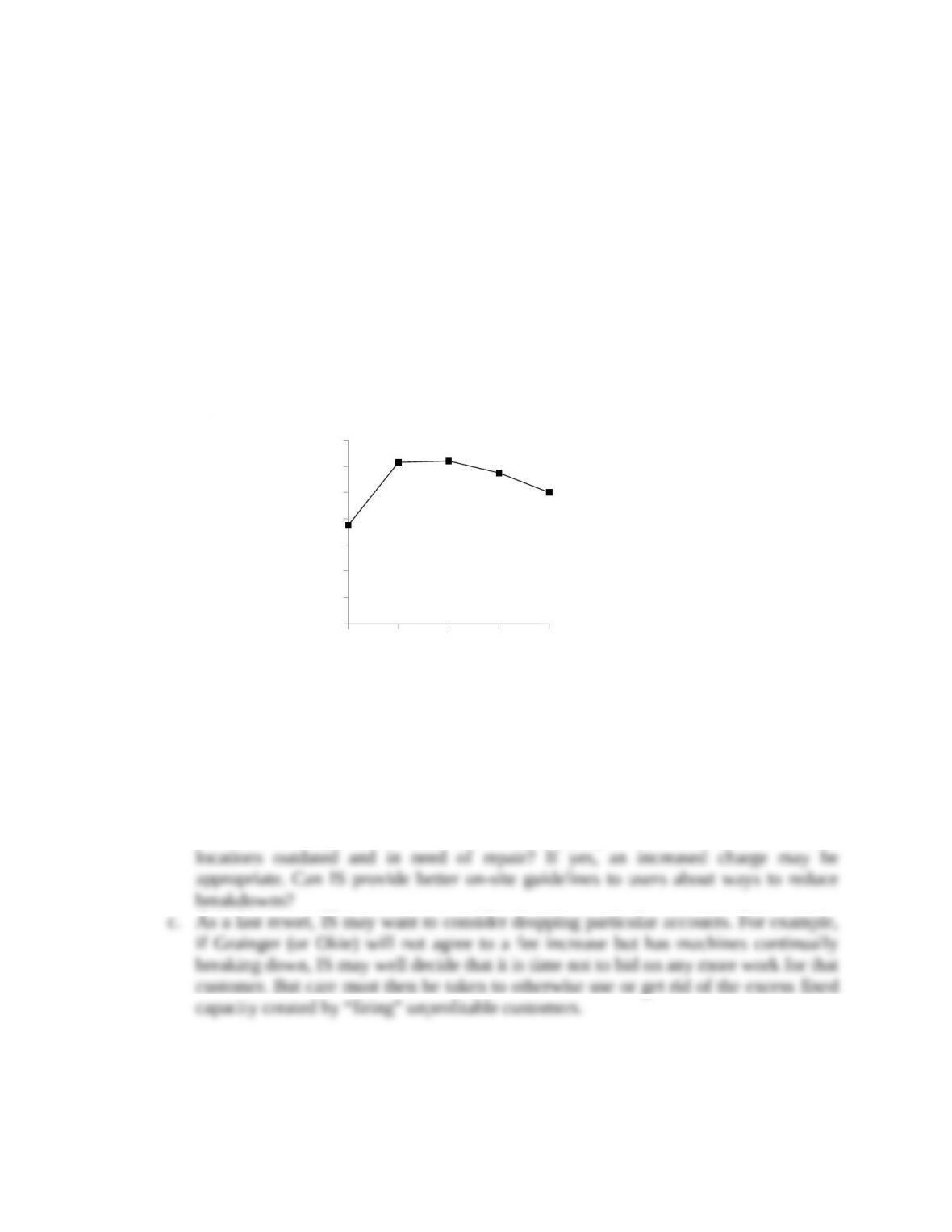

The following is the whale curve of cumulative profitability for Instant Service’s customers.

Wizard, the most profitable customer, provides 75% of total operating income. The three best

customers provide 124% of IS’s operating income, and the other two, by incurring losses for IS,

erode the extra 24% of operating income down to IS’s operating income.

3. The options that IS should consider include:

a. Increase the attention paid to Wizard and Avery. These are “key customers,” and every

effort has to be made to ensure they retain IS. IS may well want to suggest a minor

price reduction to signal how important it is in their view to provide a cost-effective

service to these customers.

b. Seek ways of reducing the costs or increasing the revenues of the problem accounts—

Okie and Grainger. For example, are the copying machines at those customer locations

outdated and in need of repair? If yes, an increased charge may be appropriate. Can IS

provide better on-site guidelines to users about ways to reduce breakdowns?

c. As a last resort, IS may want to consider dropping particular accounts. For example, if

Grainger (or Okie) will not agree to a fee increase but has machines continually

breaking down, IS may well decide that it is time not to bid on any more work for that

customer. But care must then be taken to otherwise use or get rid of the excess fixed

capacity created by “firing” unprofitable customers.

0%

20%

40%

60%

80%

100%

120%

140%

Wizard Avery Duran Grainger Okie

Cumulative Income as a

Percent of Total Income

Customers

Whale Curve of Cumulative Profitability for Instant

Service’s Customers