11-21 (10 min.) Inventory decision, opportunity costs.

Best Trim, a manufacturer of lawn mowers, predicts that it will purchase 204,000 spark plugs next

year. Best Trim estimates that 17,000 spark plugs will be required each month. A supplier quotes

a price of $9 per spark plug. The supplier also offers a special discount option: If all 204,000 spark

plugs are purchased at the start of the year, a discount of 2% off the $9 price will be given. Best

Trim can invest its cash at 10% per year. It costs Best Trim $260 to place each purchase order.

Required:

1. What is the opportunity cost of interest forgone from purchasing all 204,000 units at the start

of the year instead of in 12 monthly purchases of 17,000 units per order?

2. Would this opportunity cost be recorded in the accounting system? Why?

3. Should Best Trim purchase 204,000 units at the start of the year or 17,000 units each month?

Show your calculations.

4. What other factors should Best Trim consider when making its decision?

SOLUTION

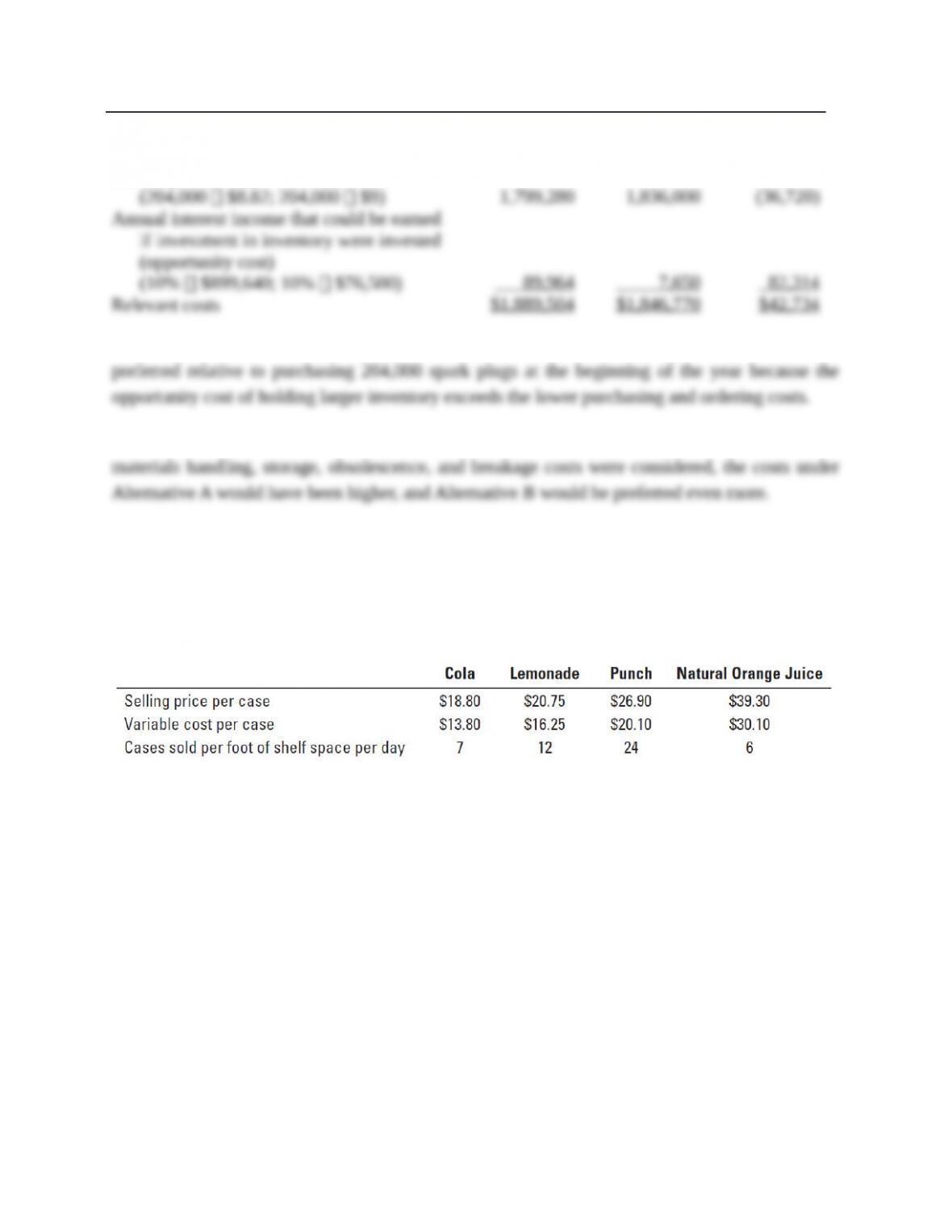

1. Unit cost, orders of 17,000 $9.00

Unit cost, order of 204,000 (0.98 $9.00) $8.82

Alternatives under consideration:

(a) Buy 204,000 units at start of year.

(b) Buy 17,000 units at start of each month.

Average investment in inventory:

(a) (204,000 $8.82) ÷ 2 $899,640

(b) (17,000 $9.00) ÷ 2 76,500

Difference in average investment $823,140

Opportunity cost of interest forgone from 204,000–unit purchase at start of year

= $823,140 0.10 = $82,314

2. No. The $82,314 is an opportunity cost rather than an incremental or outlay cost. No actual

transaction records the $82,314 as an entry in the accounting system.

3. The following table presents the two alternatives:

Alternative A:

Purchase

204,000

spark plugs at

beginning of

year

(1)

Alternative B:

Purchase

17,000

spark plugs

at beginning

of each month

(2)

Difference

(3) = (1) – (2)

Annual purchase-order costs

(1 $260; 12 $260)

Annual purchase (incremental) costs

(204,000 $8.82; 204,000 $9)

Annual interest income that could be earned

if investment in inventory were invested

(opportunity cost)

(10% $899,640; 10% $76,500)

Relevant costs

$ 260

1,799,280

89,964

$1,889,504

$ 3,120

1,836,000

7,650

$1,846,770

$ (2,860)

(36,720)

82,314

$42,734

Column (3) indicates that purchasing 17,000 spark plugs at the beginning of each month is

preferred relative to purchasing 204,000 spark plugs at the beginning of the year because the

opportunity cost of holding larger inventory exceeds the lower purchasing and ordering costs.

4. If other incremental benefits of holding lower inventory such as lower insurance, materials

handling, storage, obsolescence, and breakage costs were considered, the costs under Alternative

A would have been higher, and Alternative B would be preferred even more.

11-22 (20–25 min.) Relevant costs, contribution margin, product emphasis.

The Snack Shack is a take-out food store at a popular beach resort. Susan Sexton, owner of the

Snack Shack, is deciding how much refrigerator space to devote to four different drinks. Pertinent

data on these four drinks are as follows:

Sexton has a maximum front shelf space of 12 feet to devote to the four drinks. She wants a

minimum of 1 foot and a maximum of 6 feet of front shelf space for each drink.

Required:

1. Calculate the contribution margin per case of each type of drink.

2. A coworker of Sexton’s recommends that she maximize the shelf space devoted to those drinks

with the highest contribution margin per case. Do you agree with this recommendation?

Explain briefly.

3. What shelf-space allocation for the four drinks would you recommend for the Snack Shack?

Show your calculations.

SOLUTION

1.

Cola

Lemonade

Punch

Natural

Orange

Juice

11-3

Selling price $18.80 $20.75 $26.90 $39.30

Deduct variable cost per case 13.80 16.25 20.10 30.10

Contribution margin per case $ 5.00 $ 4.50 $ 6.80 $ 9.20

2. The argument fails to recognize that shelf space is the constraining factor. There are only

12 feet of front shelf space to be devoted to drinks. Sexton should aim to get the highest daily

contribution margin per foot of front shelf space:

Cola

Lemonade

Punch

Natural

Orange

Juice

Contribution margin per case $ 5.00 $ 4.50 $ 6.80 $ 9.20

Sales (number of cases) per foot

of shelf space per day 7 12 24 6

Daily contribution per foot

of front shelf space $35.00 $54.00 $163.20 $55.20

3. The allocation that maximizes the daily contribution from soft drink sales is:

Daily Contribution

Feet of

per Foot of

Total Contribution

Shelf Space

Front Shelf Space

Margin per Day

Punch

6

$163.20

$ 979.20

Natural Orange Juice

4

55.20

220.80

Lemonade

1

54.00

54.00

Cola

1

35.00

35.00

$1,289.00

The maximum of six feet of front shelf space will be devoted to Punch because it has the highest

contribution margin per unit of the constraining factor. Four feet of front shelf space will be

devoted to Natural Orange Juice, which has the second highest contribution margin per unit of the

constraining factor. No more shelf space can be devoted to Natural Orange Juice because each of

the remaining two products, Lemonade and Cola (that have the second lowest and lowest

contribution margins per unit of the constraining factor), must each be given at least one foot of

front shelf space.

11-23 (10 min.) Selection of most profitable product.

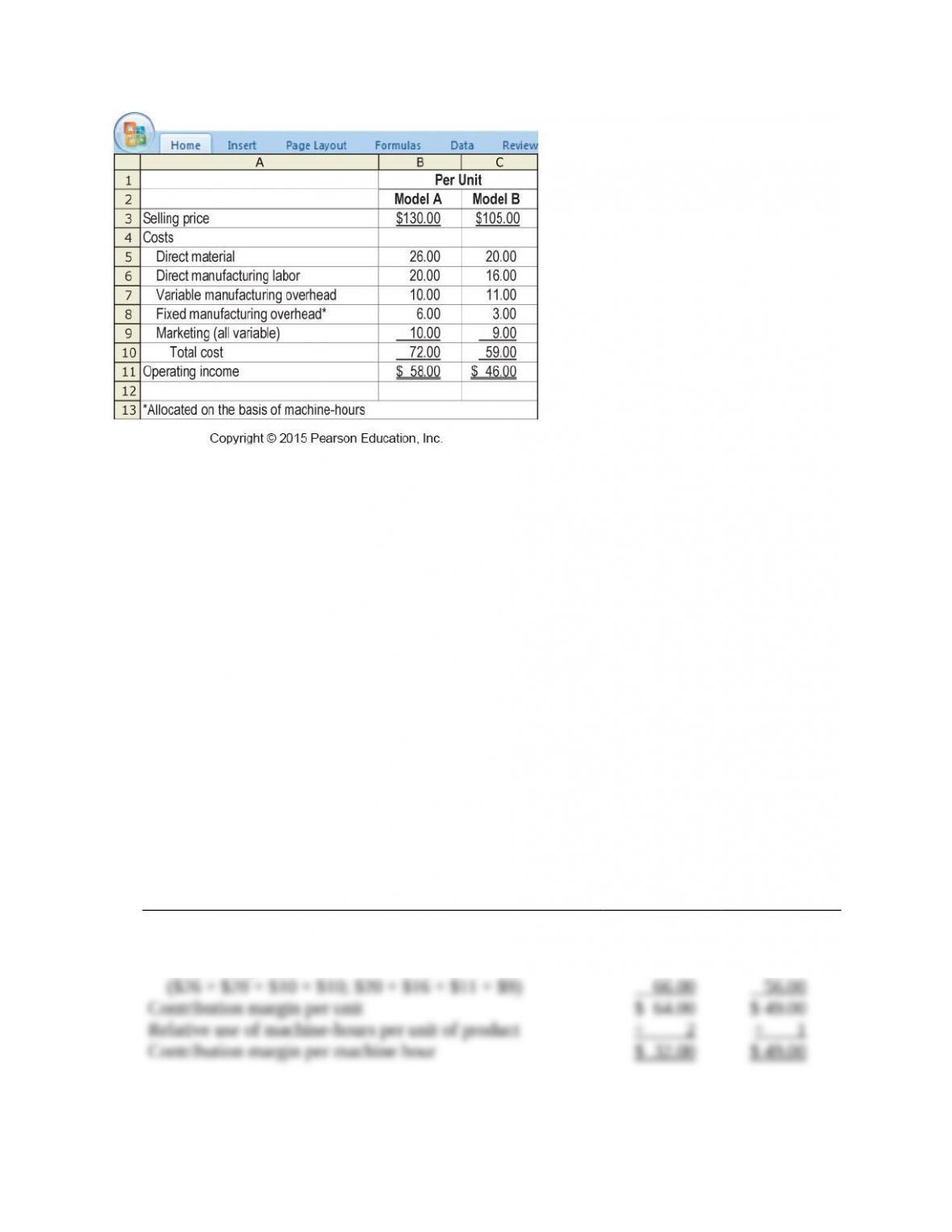

Fitness Gym, Inc., produces two basic types of weight-lifting equipment, Model 9 and Model 14.

Pertinent data are as follows:

11-4

The weight-lifting craze suggests that Fitness Gym can sell enough of either Model 9 or Model 14

to keep the plant operating at full capacity. Both products are processed through the same

production departments.

Required:

Which product should the company produce? Briefly explain your answer.

SOLUTION

Note: In some print versions of the text, the column headings appear as Model A and

Model B. The column headings in the problem should be Model 9 instead of Model A and

Model 14 instead of Model B.

Only Model 14 should be produced. The key to this problem is the relationship of manufacturing

overhead to each product. Note that it takes twice as long to produce Model 9; machine-hours for

Model 9 are twice that for Model 14. Management should choose the product mix that maximizes

operating income for a given production capacity (the scarce resource in this situation). In this

case, Model 14 will yield a $49 contribution to fixed costs per machine hour, and Model 9 will

yield $32:

Model 9

Model 14

Selling price

Variable cost per unit*

($26 + $20 + $10 + $10; $20 + $16 + $11 + $9)

Contribution margin per unit

Relative use of machine-hours per unit of product

Contribution margin per machine hour

$130.00

66.00

$ 64.00

÷ 2

$ 32.00

$105.00

56.00

$ 49.00

÷ 1

$ 49.00

11-5

*Variable cost per unit = Direct material cost per unit + Direct manufacturing labor cost per unit

+ Variable manufacturing cost per unit + Variable marketing cost per

unit.

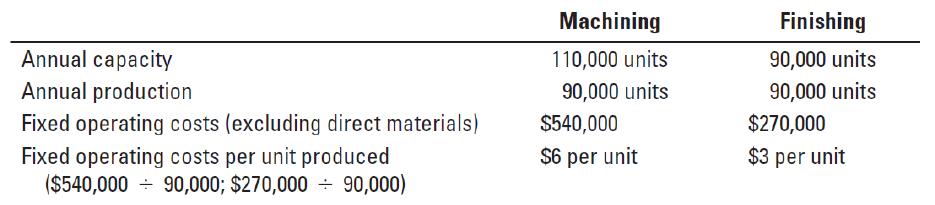

11-24 (25 min.) Theory of constraints, throughput contribution, relevant costs.

The Pierce Corporation manufactures filing cabinets in two operations: machining and finishing.

It provides the following information:

Each cabinet sells for $70 and has direct material costs of $30 incurred at the start of the machining

operation. Pierce has no other variable costs. Pierce can sell whatever output it produces. The

following requirements refer only to the preceding data. There is no connection between the

requirements.

Required:

1. Pierce is considering using some modern jigs and tools in the finishing operation that would

increase annual finishing output by 1,150 units. The annual cost of these jigs and tools is

$35,000. Should Pierce acquire these tools? Show your calculations.

2. The production manager of the Machining Department has submitted a proposal to do faster

setups that would increase the annual capacity of the Machining Department by 9,000 units

and would cost $4,000 per year. Should Pierce implement the change? Show your calculations.

3. An outside contractor offers to do the finishing operation for 9,500 units at $9 per unit, triple

the $3 per unit that it costs Pierce to do the finishing in-house. Should Pierce accept the

subcontractor’s offer? Show your calculations.

4. The Hammond Corporation offers to machine 5,000 units at $3 per unit, half the $6 per unit

that it costs Pierce to do the machining in–house. Should Pierce accept Hammond’s offer?

Show your calculations.

5. Pierce produces 1,700 defective units at the machining operation. What is the cost to Pierce of

the defective items produced? Explain your answer briefly.

6. Pierce produces 1,700 defective units at the finishing operation. What is the cost to Pierce of

the defective items produced? Explain your answer briefly.

SOLUTION

1. Finishing is a bottleneck operation. Therefore, producing 1,150 more units will generate

additional contribution (throughput) margin and operating income.

Increase in contribution (throughput) margin ($70 – $30) 1,150 $46,000

11-6

Incremental costs of the jigs and tools 35,000

Increase in operating income investing in jigs and tools $11,000

Pierce should invest in the modern jigs and tools because the benefit of higher contribution

(throughput) margin of $46,000 exceeds the cost of $35,000.

2. The Machining Department has excess capacity and is not a bottleneck operation.

Increasing its capacity further will not increase contribution (throughput) margin. There is,

therefore, no benefit from spending $4,000 to increase the Machining Department’s capacity by

9,000 units. Pierce should not implement the change to do setups faster.

3. Finishing is a bottleneck operation. Therefore, getting an outside contractor to produce

9,500 units will increase contribution (throughput) margin.

Increase in contribution (throughput) margin ($70 – $30) 9,500 $380,000

Incremental contracting costs $9 9,500 85,500

Increase in operating income by contracting 9,500 units of finishing $294,500

Pierce should contract with an outside contractor to do 9,500 units of finishing at $9 per unit

because the benefit of higher throughput margin of $380,000 exceeds the cost of $85,500. The fact

that the cost of $9 per unit is three times Pierce’s finishing cost of $3 per unit is irrelevant.

4. Operating costs in the Machining Department of $540,000, or $6 per unit, are fixed costs.

Pierce will not save any of these costs by subcontracting machining of 5,000 units to Hammond

Corporation. Total costs will be greater by $15,000 ($3 per unit 5,000 units) under the

subcontracting alternative. Machining more filing cabinets will not increase contribution

(throughput) margin, which is constrained by the finishing capacity. Pierce should not accept

Hammond’s offer. The fact that Hammond’s costs of machining per unit are half of what it costs

Pierce in-house is irrelevant.

5. The cost of 1,700 defective units in the Machining Operation is $30 per unit 1,700 units

= $51,000. Because the Machining Operation has a capacity of 110,000 units, it can still produce

and transfer 90,000 good units to the Finishing Operation. There is, therefore, no opportunity cost

of producing defective units in the Machining Operation.

6. The cost of 1,700 defective units in the Finishing Operation is:

Cost of direct materials used in the defective units $30 per unit 1,700 units $ 51,000

Opportunity cost, lost contribution (throughput) margin $40 per unit 1,700 units 68,000

Total cost of defective unit in the Finishing Operation $119,000

Alternatively, the cost of 1,700 defective units in the Finishing Operation equals the revenues lost

by selling 1,700 fewer units = $70 per unit 1,700 units = $119,000. The cost of the defective unit

at a bottleneck operation is much higher than at a non-bottleneck operation because of the

opportunity cost of lost contribution margin at the bottleneck operation.

11-25 (25−30 min.) Closing and opening stores.

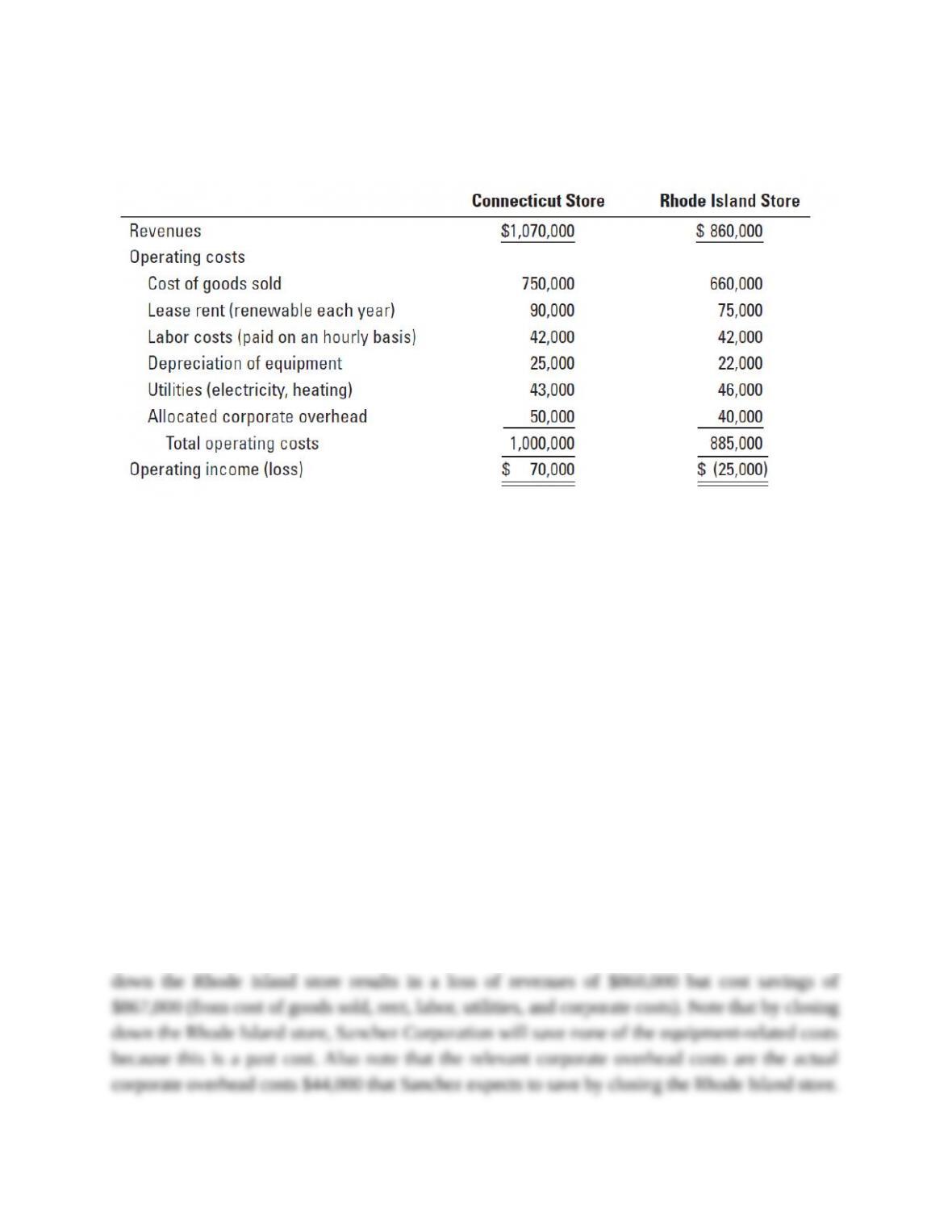

Sanchez Corporation runs two convenience stores, one in Connecticut and one in Rhode Island.

Operating income for each store in 2014 is as follows:

11-7

The equipment has a zero disposal value. In a senior management meeting, Maria Lopez, the

management accountant at Sanchez Corporation, makes the following comment, “Sanchez can

increase its profitability by closing down the Rhode Island store or by adding another store like

it.”

Required:

1. By closing down the Rhode Island store, Sanchez can reduce overall corporate overhead costs

by $44,000. Calculate Sanchez’s operating income if it closes the Rhode Island store. Is Maria

Lopez’s statement about the effect of closing the Rhode Island store correct? Explain.

2. Calculate Sanchez’s operating income if it keeps the Rhode Island store open and opens

another store with revenues and costs identical to the Rhode Island store (including a cost of

$22,000 to acquire equipment with a one-year useful life and zero disposal value). Opening

this store will increase corporate overhead costs by $4,000. Is Maria Lopez’s statement about

the effect of adding another store like the Rhode Island store correct? Explain.

SOLUTION

1. Solution Exhibit 11-25, Column 1, presents the relevant loss in revenues and the relevant

savings in costs from closing the Rhode Island store. Lopez is correct that Sanchez Corporation’s

operating income would increase by $7,000 if it closes down the Rhode Island store. Closing down

the Rhode Island store results in a loss of revenues of $860,000 but cost savings of $867,000 (from

cost of goods sold, rent, labor, utilities, and corporate costs). Note that by closing down the Rhode

Island store, Sanchez Corporation will save none of the equipment-related costs because this is a

past cost. Also note that the relevant corporate overhead costs are the actual corporate overhead

costs $44,000 that Sanchez expects to save by closing the Rhode Island store. The corporate

overhead of $40,000 allocated to the Rhode Island store is irrelevant to the analysis.

11-8

2. Solution Exhibit 11-25, Column 2, presents the relevant revenues and relevant costs of

opening another store like the Rhode Island store. Lopez is correct that opening such a store would

increase Sanchez Corporation’s operating income by $11,000. Incremental revenues of $860,000

exceed the incremental costs of $849,000 (from higher cost of goods sold, rent, labor, utilities, and

some additional corporate costs). Note that the cost of equipment written off as depreciation is

relevant because it is an expected future cost that Sanchez will incur only if it opens the new store.

Also note that the relevant corporate overhead costs are the $4,000 of actual corporate overhead

costs that Sanchez expects to incur as a result of opening the new store. Sanchez may, in fact,

allocate more than $4,000 of corporate overhead to the new store, but this allocation is irrelevant

to the analysis.

The key reason that Sanchez’s operating income increases either if it closes down the Rhode

Island store or if it opens another store like it is the behavior of corporate overhead costs. By

closing down the Rhode Island store, Sanchez can significantly reduce corporate overhead costs

presumably by reducing the corporate staff that oversees the Rhode Island operation. On the other

hand, adding another store like Rhode Island does not increase actual corporate costs by much,

presumably because the existing corporate staff will be able to oversee the new store as well.

SOLUTION EXHIBIT 11-25

Relevant-Revenue and Relevant-Cost Analysis of Closing Rhode Island Store and Opening

Another Store Like It.

Incremental

(Loss in Revenues) Revenues and

and Savings in (Incremental Costs)

Costs from Closing of Opening New Store

Rhode Island Store Like Rhode Island Store

(1) (2)

Revenues $(860,000) $ 860,000

Cost of goods sold 660,000 (660,000)

Lease rent 75,000 (75,000)

Labor costs 42,000 (42,000)

Depreciation of equipment 0 (22,000)

Utilities (electricity, heating) 46,000 (46,000)

Corporate overhead costs 44,000 (4,000)

Total costs 867,000 (849,000)

Effect on operating income (loss) $ 7,000 $ 11,000

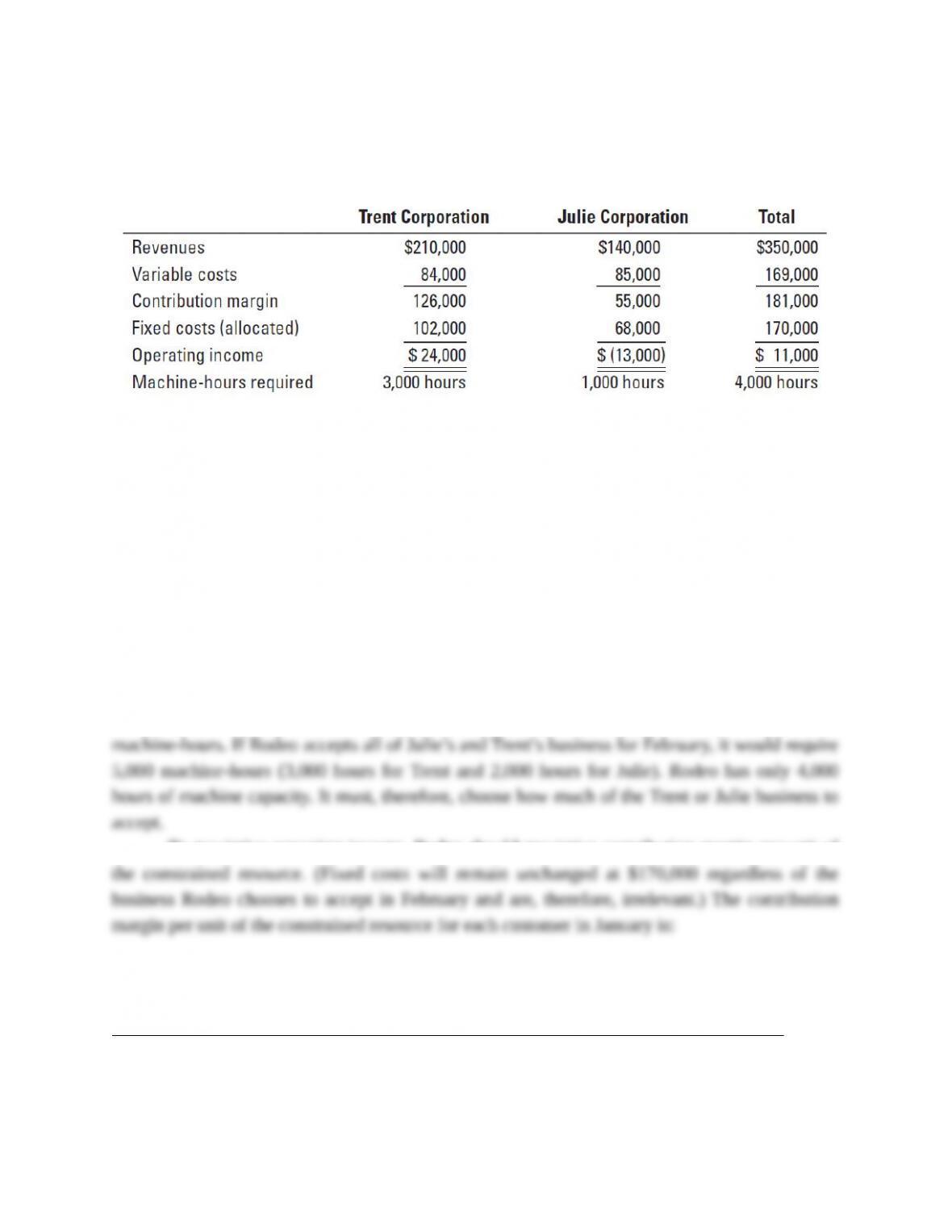

11-26 (20 min.) Choosing customers.

Rodeo Printers operates a printing press with a monthly capacity of 4,000 machine-hours. Rodeo

has two main customers: Trent Corporation and Julie Corporation. Data on each customer for

January are:

11-9

Julie Corporation indicates that it wants Rodeo to do an additional $140,000 worth of printing jobs

during February. These jobs are identical to the existing business Rodeo did for Julie in January in

terms of variable costs and machine-hours required. Rodeo anticipates that the business from Trent

Corporation in February will be the same as that in January. Rodeo can choose to accept as much

of the Trent and Julie business for February as its capacity allows. Assume that total machine–

hours and fixed costs for February will be the same as in January.

Required:

What action should Rodeo take to maximize its operating income? Show your calculations. What

other factors should Rodeo consider before making a decision?

SOLUTION

If Rodeo accepts the additional business from Julie, it would take an additional 500 machine-hours.

If Rodeo accepts all of Julie’s and Trent’s business for February, it would require 5,000 machine–

hours (3,000 hours for Trent and 2,000 hours for Julie). Rodeo has only 4,000 hours of machine

capacity. It must, therefore, choose how much of the Trent or Julie business to accept.

To maximize operating income, Rodeo should maximize contribution margin per unit of

the constrained resource. (Fixed costs will remain unchanged at $170,000 regardless of the

business Rodeo chooses to accept in February and are, therefore, irrelevant.) The contribution

margin per unit of the constrained resource for each customer in January is:

Trent Julie

Corporation Corporation

Contribution margin per machine-hour

$126,000

3,000

= $42

$55,000

1,000

= $55

Because the $140,000 of additional Julie business in February is identical to jobs done in

January, it will also have a contribution margin of $55 per machine-hour, which is greater than the

contribution margin of $42 per machine–hour from Trent. To maximize operating income, Rodeo

should first allocate all the capacity needed to take the Julie Corporation business (2,000 machine–

hours) and then allocate the remaining 2,000 (4,000 – 2,000) machine-hours to Trent.

Trent Julie

11-10

Corporation Corporation Total

Contribution margin per machine-hour $42 $55

Machine-hours to be worked 2,000 2,000

Contribution margin $84,000 $110,000 $194,000

Fixed costs 170,000

Operating income $ 24,000

An alternative approach is to use the opportunity cost approach. The opportunity cost of

giving up 1,000 machine-hours for the Trent Corporation jobs is the contribution margin forgone

of $42 per machine-hour 1,000 machine-hours equal to $42,000. The contribution margin

gained from using the 1,000 machine-hours for the Julie Corporation business is the contribution

margin per machine-hour of $55 1,000 machine-hours equal to $55,000.

The net benefit is:

Contribution margin from Julie Corporation business

$55,000

Less: Opportunity cost (of giving up Trent Corporation business)

(42,000)

Net benefit

$13,000

Although taking the Julie Corporation business over the Trent Corporation business will

maximize Rodeo’s profits in the short run, Rodeo’s managers must also consider the long-run

effects of this decision. Will Julie Corporation continue to demand the same level of business

going forward? Will turning down the Trent business affect customer satisfaction? If Rodeo

turns down the Trent business, will Trent continue to place orders with Rodeo or seek alternative

suppliers? Rodeo’s managers need to consider these long-run effects and then decide whether it

should accept Julie’s business at the cost of Trent’s. In other words, choosing customers is a

strategic decision. If it sees long–run benefit in working with Trent, Rodeo’s managers must also

look for ways to increase the profitability of the business it does with Trent by increasing prices

or reducing costs.