15-1

15-28 (20 min.) Revenue allocation

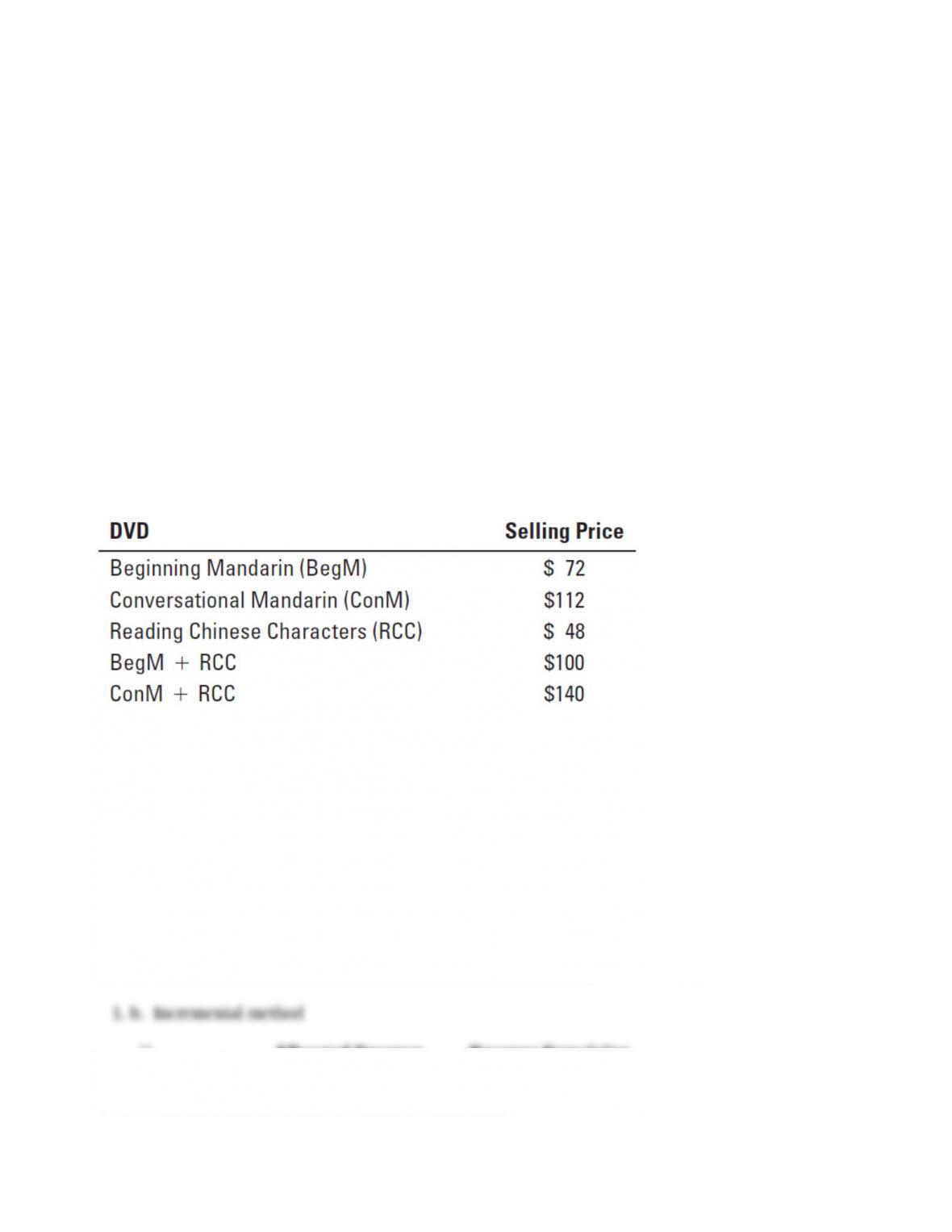

Yang Inc. produces and sells DVDs to business people and students who are planning extended

stays in China. It has been very successful with two DVDs: Beginning Mandarin and

Conversational Mandarin. It is introducing a third DVD, Reading Chinese Characters. It has

decided to market its new DVD in two different packages grouping the Reading Chinese

Characters DVD with each of the other two language DVDs. Information about the separate DVDs

and the packages follow.

Required:

1. Using the selling prices, allocate revenues from the BegM + RCC package to each DVD in

that package using (a) the stand-alone method; (b) the incremental method, in either order; and

(c) the Shapley value method.

2. Using the selling prices, allocate revenues from the ConM + RCC package to each DVD in

that package using (a) the stand-alone method; (b) the incremental method, in either order; and

(c) the Shapley value method.

3. Which method is most appropriate for allocating revenues among the DVDs? Why?

SOLUTION

1. a. Stand-alone method for the BegM + RCC package

DVD

(1)

Separate

Revenue

(2)

Percentage

(3) = (2) ÷ $120

Joint

Revenue

(4)

Allocation

(5) = (3) × (4)

BegM $ 72 $72 ÷ $120=0.60 $100 $ 60

RCC 48 $48 ÷ $120=0.40 100 40

$120 $100

1. b. Incremental method

i)

Allocated Revenue

Revenue Remaining

(BegM first)

To Allocate

BegM $72 $28 ($100 ─ $72)

15-2

RCC 28

ii)

Allocated Revenue

Revenue Remaining

(RCC first)

To Allocate

RCC $48 $52 ($100 ─ $48)

BegM 52

1. c. Shapley method (assuming each DVD is demanded in equal proportion)

i) BegM ($72 + $52) ÷ 2 = $62

ii) RCC ($48 + $28) ÷ 2 = $38

2. a. Stand-alone method for the ConM + RCC package

DVD

(1)

Separate

Revenue

(2)

Percentage

(3) = (2) ÷ $160

Joint

Revenue

(4)

Allocation

(5) = (3) × (4)

ConM $ 112 $112 ÷ $120 = 0.70 $140 $ 98

RCC 48 $ 48 ÷ $120 = 0.30 140 42

$160 $140

2. b. Incremental method

i)

Allocated

Revenue

(ConM first)

Revenue

Remaining

To Allocate

ConM $112 $28 ($140 – $112)

RCC 28

ii)

Allocated

Revenue

(RCC first)

Revenue

Remaining

To Allocate

RCC $ 48 $92 ($140 – $48)

ConM 92

2. c. Shapley method (assuming each DVD is demanded in equal proportion)

i) ConM ($112 + $92) ÷ 2 = $102

ii) RCC ($ 48 + $28) ÷ 2 = $ 38

2. For each DVD package, the stand-alone method and the Shapley method give approximately

the same allocation to each DVD. These methods are fair if the demand for the DVDs is

approximately equal. The stand-alone method might be slightly preferable here because it is

simpler and easier to explain.

15-3

The incremental method would be appropriate if one DVD has a higher level of demand than

the other DVD. In this situation, the dominant DVD would be sold anyway, so it should

receive its stand-alone revenue, and the other DVD should receive the remainder.

15-29 (20 min.) Fixed cost allocation.

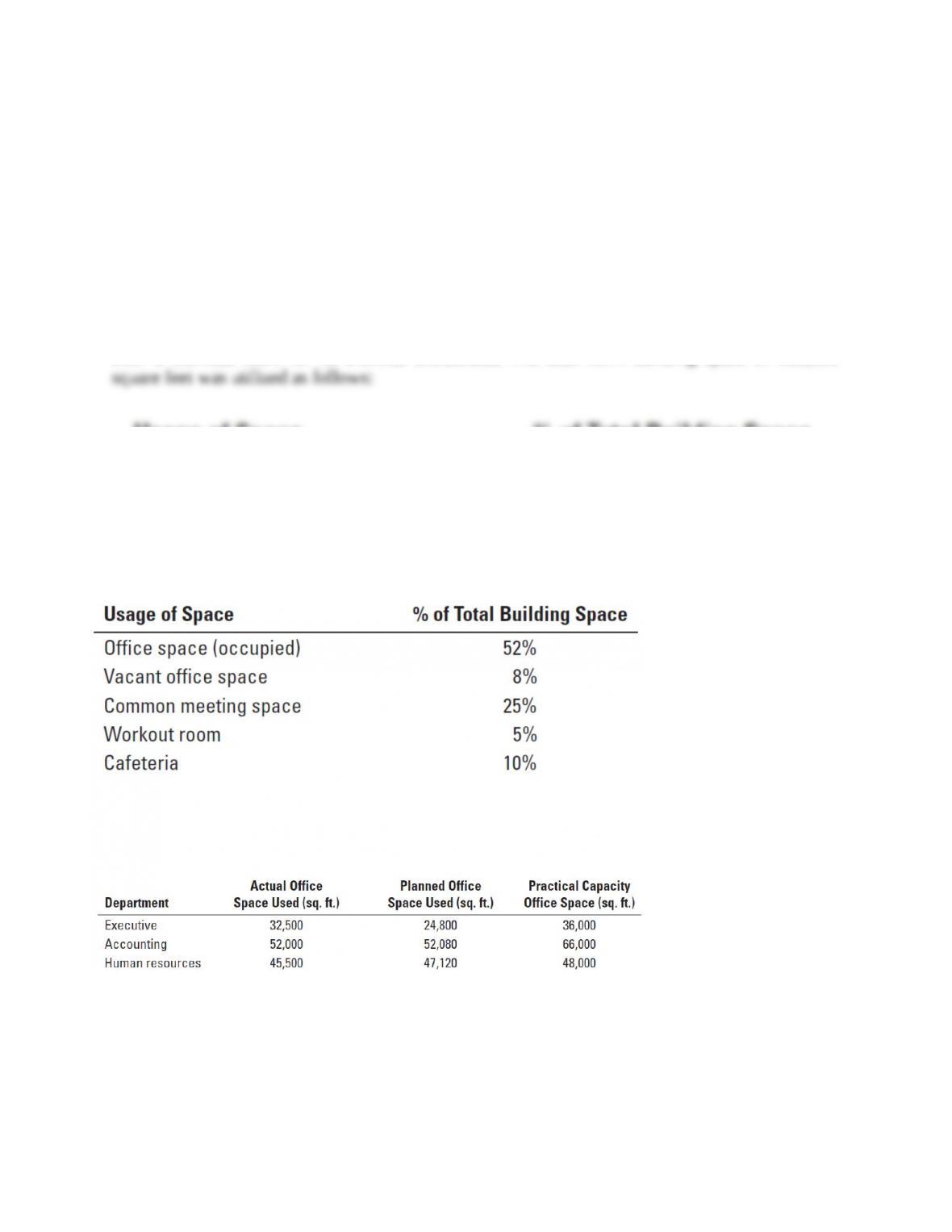

Baker University completed construction of its newest administrative building at the end of 2013.

The University’s first employees moved into the building on January 1, 2014. The building

consists of office space, common meeting rooms (including a conference center), a cafeteria, and

even a workout room for its exercise enthusiasts. The total 2014 building space of 250,000 square

feet was utilized as follows:

The new building cost the university $60 million and was depreciated using the straight-line

method over 20 years. At the end of 2014 three departments occupied the building: executive

offices of the president, accounting, and human resources. Each department’s usage of its assigned

space was as follows:

Required:

1. How much of the total building cost will be allocated in 2014 to each of the departments, if the

total cost is allocated to each department on the basis of the following?

a. Actual usage of the three departments

b. Planned usage of the three departments

c. Practical capacity of the three departments

2. Assume that Baker University allocates the total annual building cost in the following manner:

a. All vacant office space is absorbed by the university and is not allocated to the departments.

b. All occupied office space costs are allocated on the basis of actual square footage used.

c. All common area costs are allocated on the basis of a department’s practical capacity.

Calculate the cost allocated to each department in 2014 under this plan. Do you think the

allocation method used here is appropriate? Explain.

SOLUTION

1. i) Allocation using actual usage.

Department

(1)

Actual

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 130,000

Allocation

(4) = (3) × $3,000,000a

Executive

32,500

0.25

$ 750,000

Accounting

52,000

0.40

1,200,000

Human Resources

45,500

0.35

1,050,000

Total

130,000

$3,000,000

a$60,000,000 building cost/20 years straight-line depreciation = $3,000,000 annual depreciation

expense related to building.

ii) Allocation using planned usage.

Department

(1)

Planned

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 124,000

Allocation

(4) = (3) × $3,000,000

Executive

24,800

0.20

$ 600,000

Accounting

52,080

0.42

1,260,000

Human Resources

47,120

0.38

1,140,000

Total

124,000

$3,000,000

iii) Allocation using practical capacity.

Department

(1)

Practical

Capacity

(2)

Percentage of

Total Usage

(3) = (2) ÷ 150,000

Allocation

(4) = (3) × $3,000,000

Executive

36,000

0.24

$ 720,000

Accounting

66,000

0.44

1,320,000

Human Resources

48,000

0.32

960,000

Total

150,000

$3,000,000

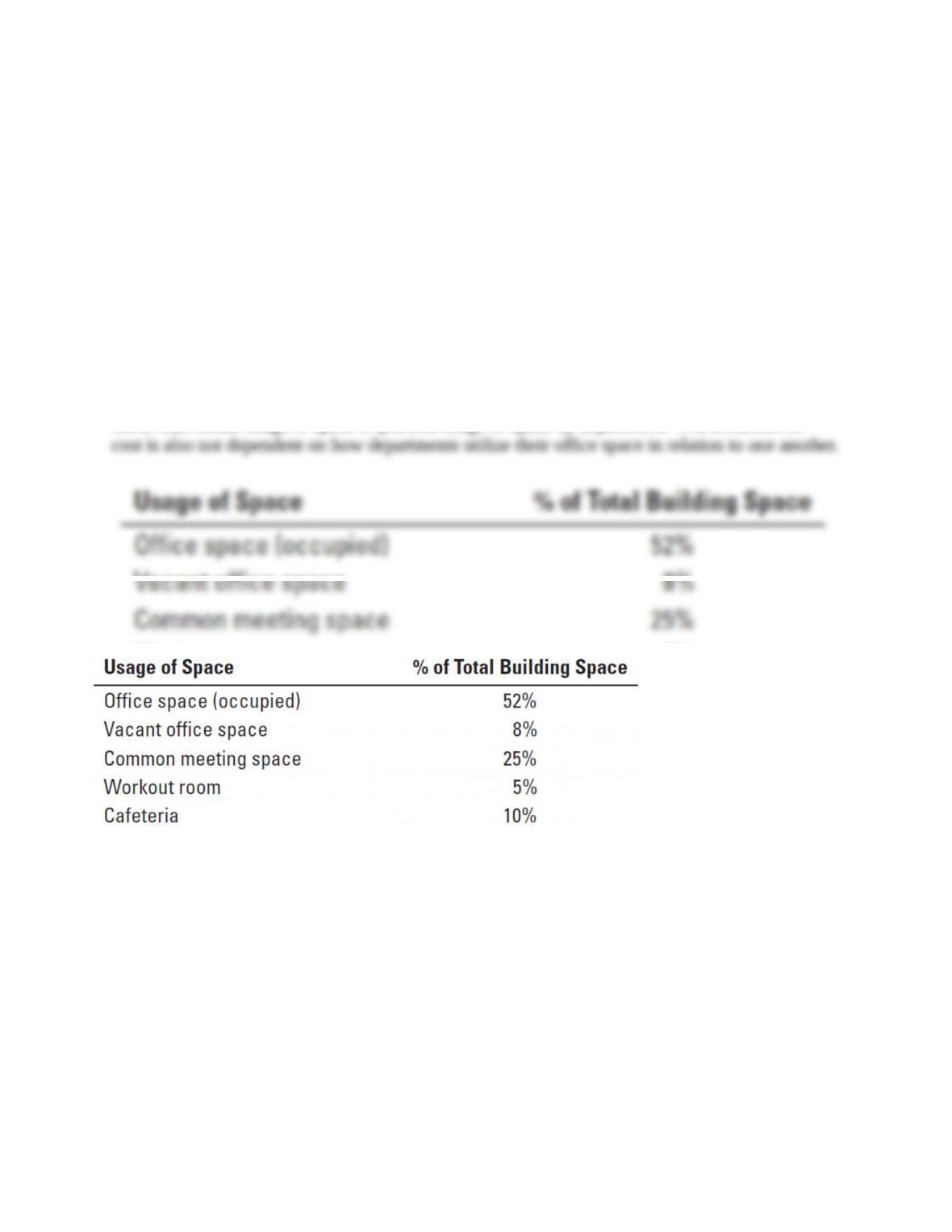

2.

Usage of Space

Percentage of

Total Building

Space

Total Annual

Building Cost

Office Space (occupied)

52%

$1,560,000

Vacant Office Space

8%

240,000

Common Meeting Space

25%

750,000

Workout Room

5%

150,000

15-5

Cafeteria

10%

300,000

Total 100% $3,000,000

a) $240,000 of Vacant Office Space cost will not be allocated to the departments but will be

absorbed by the university’s central administration.

b) Allocation of Office Space (occupied) costs ($1,560,000) using actual usage.

Department

(1)

Actual

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 130,000

Allocation

(4) = (3) × $1,560,000

Executive

32,500

0.25

$ 390,000

Accounting

52,000

0.40

624,000

Human Resources

45,500

0.35

546,000

Total

130,000

$1,560,000

c) Allocation of all common space cost ($750,000 + $150,000 + $300,000 = $1,200,000)

using practical capacity.

Department

(1)

Practical

Capacity

(2)

Percentage of

Total Usage

(3) = (2) ÷ 150,000

Allocation

(4) = (3) × $1,200,000

Executive

36,000

0.24

$ 288,000

Accounting

66,000

0.44

528,000

Human Resources

48,000

0.32

384,000

Total

150,000

$1,200,000

Department

(1)

Allocated Cost of

Occupied Office Space

(2)

Allocated Cost of

Common Space

(3)

Total Cost Allocated

to Department

(4) = (2) + (3)

Executive

$ 390,000

$ 288,000

$ 678,000

Accounting

624,000

528,000

1,152,000

Human Resources

546,000

384,000

930,000

Total

$1,560,000

$1,200,000

$2,760,000

The departments would likely consider portions of the allocation method used here “fair.”

In particular, the individual departments do not pay for unused office space that is intended for

use by other departments (perhaps even ones that are not yet in the building). The total costs

allocated to the departments is $2,760,000 ($3,000,000 – the cost of vacant space, $240,000).

This creates an incentive for central administration to fill the unoccupied space with departments,

so that the vacant office space cost of $240,000 can be allocated down.

As for the allocation of occupied office space costs, it may have been more appropriate to

allocate this based on relative practical capacity rather than actual usage by department. The

current system does not appropriately consider that the building was constructed based on the

15-6

practical capacity intended to be dedicated to each department. As a result, departments who are

taking up less space than originally assigned to them are not penalized for this. Moreover, the

assignment of the cost will change year to year under the present system, depending on that

period’s relative use of space by all departments, while a practical capacity-based system would

yield stable cost allocations. If, as a result of changed circumstances, a department will not be

utilizing the practical capacity initially assigned to it, Baker University’s president might choose

to house another department in the building. The university would then assign the cost of the

building based on the practical capacities assigned to all the departments in the building,

including the practical capacity assigned to the new department.

Finally, allocating the common space cost based on practical capacity is the most

equitable method because the allocation of cost is based on “assigned space” by department

rather than actual usage of space or planned usage of space by department. The allocation of

cost is also not dependent on how departments utilize their office space in relation to one

another.

15-7

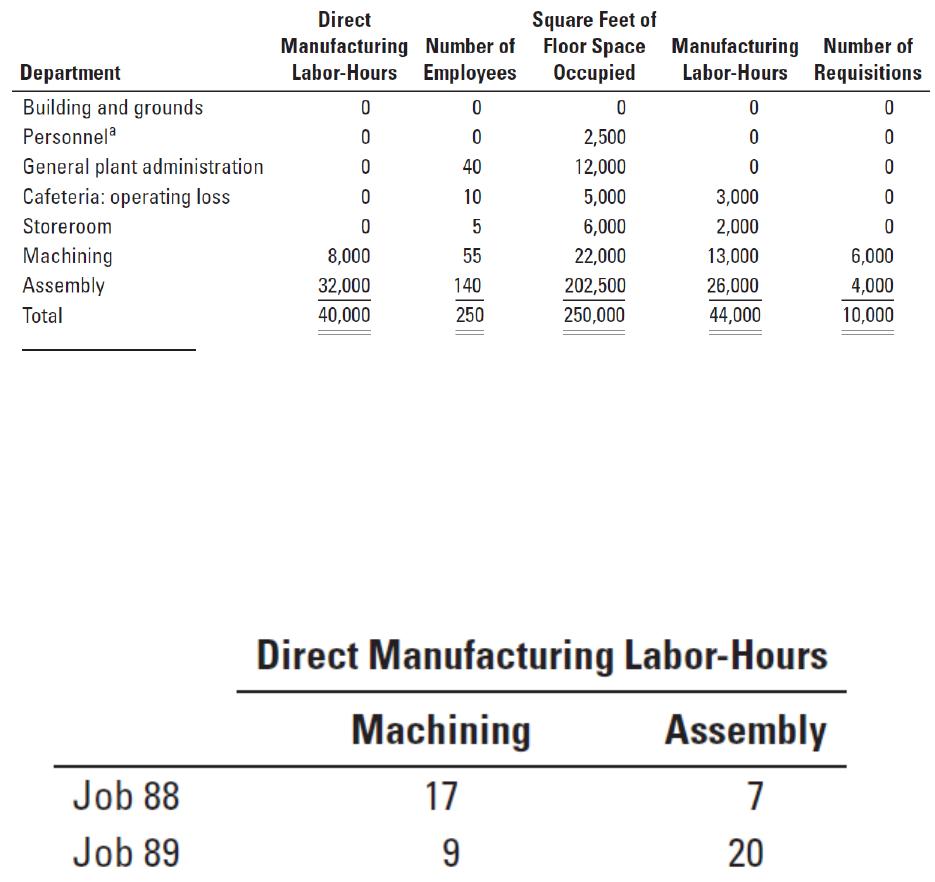

15-30 (45 min.) Allocating costs of support departments; step-down and direct methods.

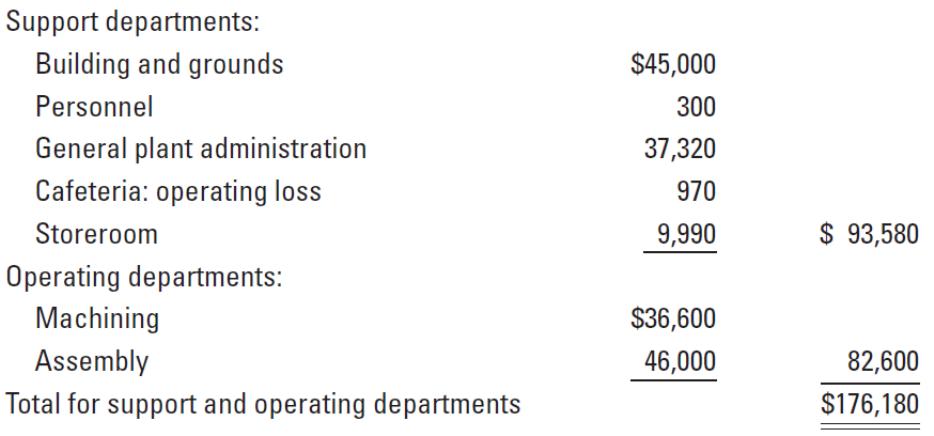

The Central Valley Company has prepared department overhead budgets for budgeted-volume levels before allocations as follows:

Management has decided that the most appropriate inventory costs are achieved by using individual-department overhead rates. These

rates are developed after support-department costs are allocated to operating departments.

Bases for allocation are to be selected from the following:

15-8

aBasis used is number of employees.

Required:

1. Using the step-down method, allocate support-department costs. Develop overhead rates per direct manufacturing labor-hour for

machining and assembly. Allocate the costs of the support departments in the order given in this problem. Use the allocation base

for each support department you think is most appropriate.

2. Using the direct method, rework requirement 1.

3. Based on the following information about two jobs, determine the total overhead costs for each job by using rates developed in (a)

requirement 1 and (b) requirement 2.

4. The company evaluates the performance of the operating department managers on the basis of how well they managed their total

costs, including allocated costs. As the manager of the Machining Department, which allocation method would you prefer from the

results obtained in requirements 1 and 2? Explain.

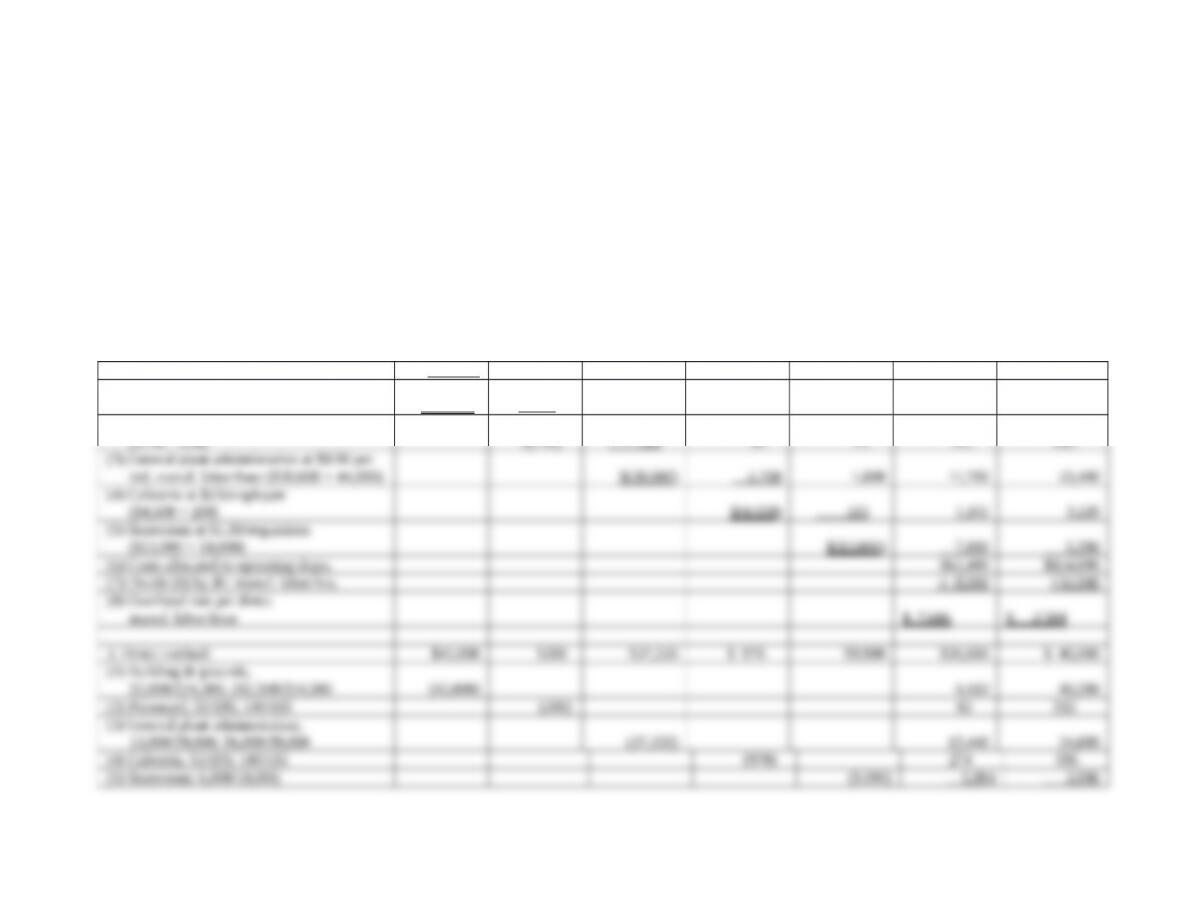

SOLUTION

In some print editions of the book, the column heading for the fifth column appears as “Manufacturing Labor–Hours.” The

column heading should be “Indirect Manufacturing Labor–Hours” instead of “Manufacturing Labor–Hours.” Indirect

Manufacturing Labor-Hours are used to allocate general plant administration costs to departments.

Building &

Grounds

Personnel

General

Plant Admin.

Cafeteria

Operating

Loss

Storeroom

Machining

Assembly

1. Step-down Method:

$ 45,000

$ 300

$ 37,320

$ 970

$ 9,990

$36,600

$ 46,000

(1) Building & grounds at $0.18/sq.ft.

($45,000 ÷ 250,000)

$(45,000)

450

2,160

900

1,080

3,960

36,450

(2) Personnel at $3/employee

($750 ÷ 250)

$(750)

120

30

15

165

420

(3) General plant administration at $0.90 per

ind. manuf. labor-hour ($39,600 ÷ 44,000)

$(39,600)

2,700

1,800

11,700

23,400

(4) Cafeteria at $23/employee

($4,600 ÷ 200)

$(4,600)

115

1,265

3,220

(5) Storeroom at $1.30/requisition

($13,000 ÷ 10,000)

$(13,000)

7,800

5,200

(6) Costs allocated to operating depts.

$61,490

$114,690

(7) Divide (6) by dir. manuf. labor-hrs.

÷ 8,000

÷32,000

(8) Overhead rate per direct

manuf. labor-hour

$ 7.686

$ 3.584

2. Direct method:

$45,000

$300

$37,320

$ 970

$9,990

$36,600

$ 46,000

(1) Building & grounds,

22,000/224,500; 202,500/224,500

(45,000)

4,410

40,590

(2) Personnel, 55/195; 140/195

(300)

85

215

(3) General plant administration,

13,000/39,000; 26,000/39,000

(37,320)

12,440

24,880

(4) Cafeteria, 55/195; 140/195

(970)

274

696

(5) Storeroom: 6,000/10,000;

4,000/10,000

(9,990)

5,994

3,996

(6) Costs allocated to operating depts.

$59,803

$116,377

(7) Divide (6) by direct manufacturing

labor-hours

÷ 8,000

÷32,000

(8) Overhead rate per direct

manufacturing labor-hour

$ 7.475

$ 3.637

15-11