4-1

SOLUTION

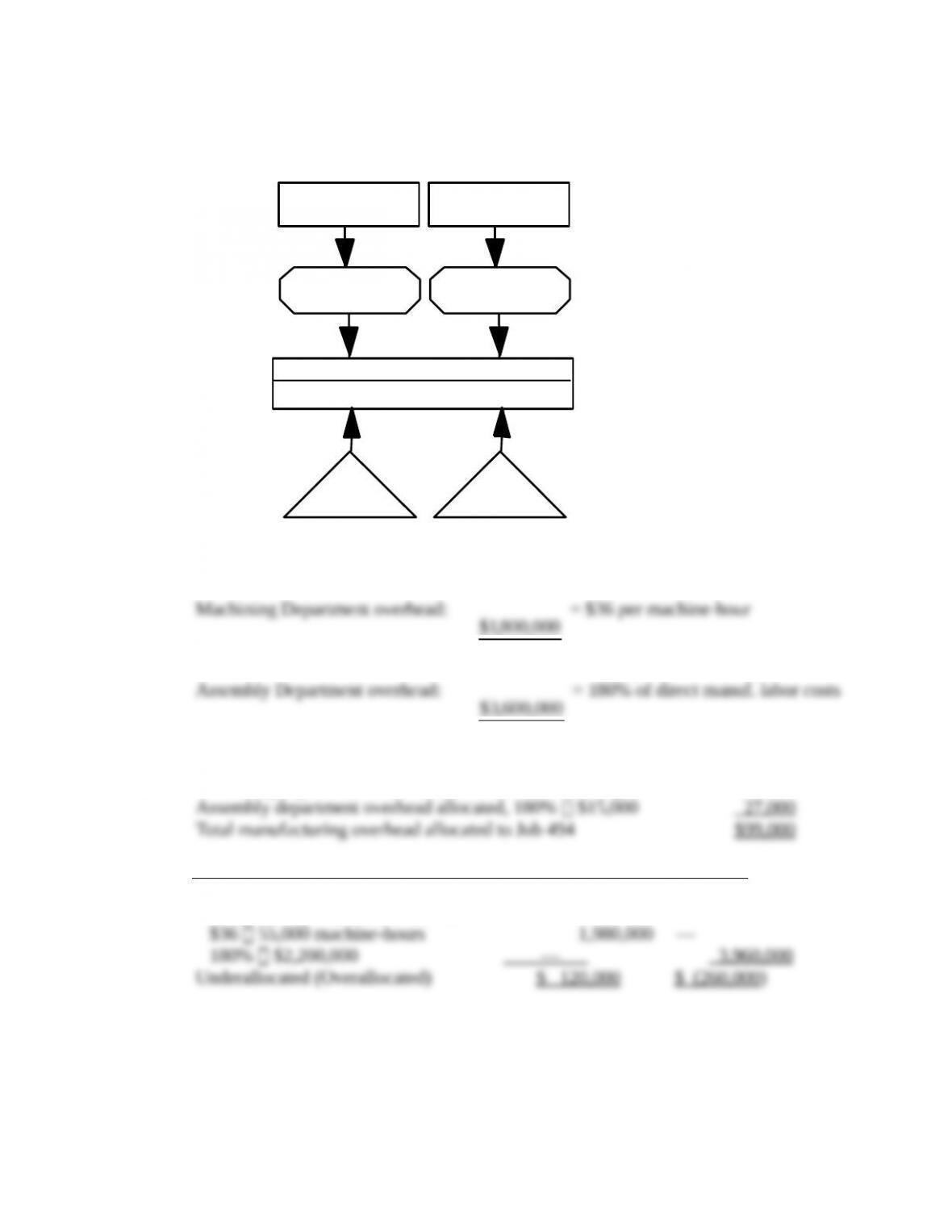

1. An overview of the product costing system is

COST OBJECT:

PRODUCT

COST

ALLOCATION

BASE

DIRECT

COST

Machining Department

Manufacturing Overhead

Machine-Hours

Direct

Materials

INDIRECT

COST

POOL

Direct

Manufacturing

Labor

Indirect Costs

Direct Costs

Assembly Department

Manufacturing Overhead

Direct Manuf.

Labor Cost

Budgeted manufacturing overhead divided by allocation base:

Machining Department overhead:

000,50

000,800,1$

= $36 per machine-hour

Assembly Department overhead:

000,000,2$

000,600,3$

= 180% of direct manuf. labor costs

2. Machining department overhead allocated, 2,000 hours $36 $72,000

Assembly department overhead allocated, 180% $15,000 27,000

Total manufacturing overhead allocated to Job 494 $99,000

3. Machining Dept. Assembly Dept.

Actual manufacturing overhead $2,100,000 $ 3,700,000

Manufacturing overhead allocated,

$36 55,000 machine-hours 1,980,000 —

180% $2,200,000 — 3,960,000

Underallocated (Overallocated) $ 120,000 $ (260,000)

4-2

COST OBJECT:

PRODUCT

COST

ALLOCATION

BASE

DIRECT

COST

Machining Department

Manufacturing Overhead

Machine-Hours

Direct

Materials

INDIRECT

COST

POOL

Direct

Manufacturing

Labor

Indirect Costs

Direct Costs

Assembly Department

Manufacturing Overhead

Direct Manuf.

Labor Cost

4-21 (20−25 min.) Job costing, consulting firm.

Taylor & Associates, a consulting firm, has the following condensed budget for 2014:

Revenues $20,000,000

Total costs:

Direct costs

Professional Labor $ 5,000,000

Indirect costs

Client support 13,000,000 18,000,000

Operating income $2,000,000

Taylor has a single direct-cost category (professional labor) and a single indirect-cost pool (client

support). Indirect costs are allocated to jobs on the basis of professional labor costs.

Required:

1. Prepare an overview diagram of the job-costing system. Calculate the 2014 budgeted indirect-

cost rate for Taylor & Associates.

2. The markup rate for pricing jobs is intended to produce operating income equal to 10% of

revenues. Calculate the markup rate as a percentage of professional labor costs.

3. Taylor is bidding on a consulting job for Tasty Chicken, a fast food chain specializing in

poultry meats. The budgeted breakdown of professional labor on the job is as follows:

Professional Labor Category

Budgeted Rate per Hour

Budgeted Hours

Director

$200

3

Partner

100

16

Associate

50

40

Assistant

30

160

Calculate the budgeted cost of the Tasty Chicken job. How much will Taylor bid for the job if it

is to earn its target operating income of 10% of revenues?

SOLUTION

1. Budgeted indirect-cost rate for client support can be calculated as follows:

Budgeted indirect-cost rate = $13,000,000 ÷ $5,000,000 = 260% of professional labor costs

2. At the budgeted revenues of $20,000,000 Taylor’s operating income of $2,000,000 equals

10% of revenues.

COST

ALLOCATION

BASE

Consulting

Support

Consulting

Support

COST OBJECT:

JOB FOR

CONSULTING

CLIENT

DIRECT

COSTS

Indirect Costs

Direct Costs

INDIRECT

COST

POOL

Professional

Labor Costs

Professional

Labor Costs

Professional

Labor

Client

Support

4-4

Markup rate = $20,000,000 ÷ $5,000,000 = 400% of direct professional labor costs

3. Budgeted costs

Direct costs:

Director, $200 3 $ 600

Partner, $100 16 1,600

Associate, $50 40 2,000

Assistant, $30 160 4,800 $ 9,000

Indirect costs:

Consulting support, 260% $9,000 23,400

Total costs $32,400

As calculated in requirement 2, the bid price to earn a 10% income–to–revenue margin is 400% of

direct professional costs. Therefore, Taylor should bid 4 $9,000 = $36,000 for the Tasty Chicken

job.

Bid price to earn target operating income-to–revenue margin of 10% can also be calculated

as follows:

Let R = revenue to earn target income

R – 0.10R = $32,400

0.90R = $32,400

R = $32,400 ÷ 0.90 = $36,000

Or

Direct costs $ 9,000

Indirect costs 23,400

Operating income (0.10 $36,000) 3,600

Bid price $36,000

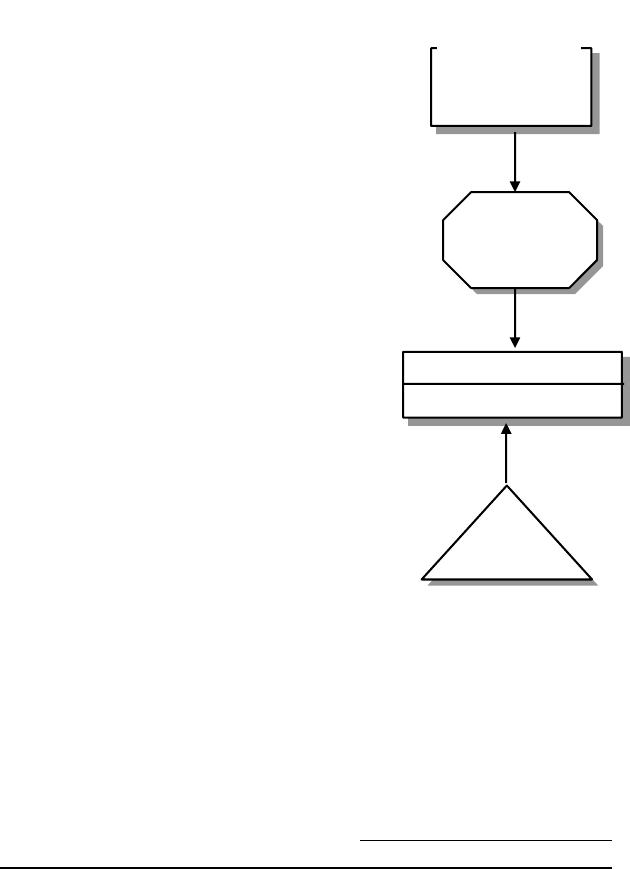

4-22 (15–20 min.) Time period used to compute indirect cost rates.

Plunge Manufacturing produces outdoor wading and slide pools. The company uses a normal–

costing system and allocates manufacturing overhead on the basis of direct manufacturing labor–

hours. Most of the company’s production and sales occur in the first and second quarters of the

year. The company is in danger of losing one of its larger customers, Socha Wholesale, due to

large fluctuations in price. The owner of Plunge has requested an analysis of the manufacturing

cost per unit in the second and third quarters. You have been provided the following budgeted

information for the coming year:

Quarter________

1 2 3 4_

Pools manufactured and sold 565 490 245 100

It takes 1 direct manufacturing labor-hour to make each pool. The actual direct material cost is

$14.00 per pool. The actual direct manufacturing labor rate is $20 per hour. The budgeted variable

manufacturing overhead rate is $15 per direct manufacturing labor-hour. Budgeted fixed

manufacturing overhead costs are $12,250 each quarter.

Required:

1. Calculate the total manufacturing cost per unit for the second and third quarter assuming the

company allocates manufacturing overhead costs based on the budgeted manufacturing

overhead rate determined for each quarter.

2. Calculate the total manufacturing cost per unit for the second and third quarter assuming the

company allocates manufacturing overhead costs based on an annual budgeted manufacturing

COST

ALLOCATION

BASE

Consulting

Support

Consulting

Support

COST OBJECT:

JOB FOR

CONSULTING

CLIENT

DIRECT

COSTS

Indirect Costs

Direct Costs

INDIRECT

COST

POOL

Professional

Labor Costs

Professional

Labor Costs

Professional

Labor

Client

Support

overhead rate.

3. Plunge Manufacturing prices its pools at manufacturing cost plus 30%. Why might Socha

Wholesale be seeing large fluctuations in the prices of pools? Which of the methods described

in requirements 1 and 2 would you recommend Plunge use? Explain.

SOLUTION

1.

Quarter

1

2

3

4

Annual

(1) Pools sold

565

490

245

100

1,400

(2) Direct manufacturing labor

hours (1 Row 1)

565

490

245

100

1,400

(3) Fixed manufacturing

overhead costs

$12,250

$12,250

$12,250

$12,250

$49,000

(4) Budgeted fixed

manufacturing overhead

rate per direct

manufacturing labor hour

($12,250 Row 2)

$21.68

$25

$50

$122.50

$35

Budgeted Costs Based on

Quarterly Manufacturing

Overhead Rate

2nd Quarter

3rd Quarter

Direct material costs ($14 490 pools; 245 pools)

$ 6,860

$ 3,430

Direct manufacturing labor costs

($20 490 hours; 245 hours)

9,800

4,900

Variable manufacturing overhead costs

($15 490 hours; 245 hours)

7,350

3,675

Fixed manufacturing overhead costs

($25 490 hours; $50 × 245 hours)

12,250

12,250

Total manufacturing costs

$36,260

$24,255

Divided by pools manufactured each quarter

÷ 490

÷ 245

Manufacturing cost per pool

$ 74.00

$ 99.00

2.

Budgeted Costs Based on

Annual Manufacturing

Overhead Rate

2nd Quarter

3rd Quarter

Direct material costs ($14 490 pools; 245 pools)

$ 6,860

$ 3,430

Direct manufacturing labor costs

($20 490 hours; 245 hours)

9,800

4,900

Variable manufacturing overhead costs

($15 490 hours; 245 hours)

7,350

3,675

Fixed manufacturing overhead costs

($35 490 hours; 75 hours)

17,150

8,575

Total manufacturing costs

$41,160

$20,580

4-7

Divided by pools manufactured each quarter

490

245

Manufacturing cost per pool

$ 84.00

$84.00

3.

2nd Quarter

3rd Quarter

Prices based on quarterly budgeted manufacturing

overhead rates calculated in requirement 1

($74.00 130%; $99.00 130%)

$96.20

$128.70

Price based on annual budgeted manufacturing overhead

rates calculated in requirement 2

($84.00 130%; $84.00 130%)

$109.20

$109.20

Socha might be seeing large fluctuations in the prices of its pools because Plunge is determining

budgeted manufacturing overhead rates on a quarterly rather than an annual basis. Plunge should

use the budgeted annual manufacturing overhead rate because capacity decisions are based on

longer annual periods rather than quarterly periods. Prices should not vary based on quarterly

fluctuations in production. Plunge could vary prices based on market conditions and demand for

its pools. In this case, Plunge would charge higher prices in quarter 2 when demand for its pools

is high. Pricing based on quarterly budgets would cause Plunge to do the opposite—to decrease

rather than increase prices!

4-23 (10–15 min.) Accounting for manufacturing overzhead.

Jamison Woodworking uses normal costing and allocates manufacturing overhead to jobs based

on a budgeted labor-hour rate and actual direct labor-hours. Under- or overallocated overhead, if

immaterial, is written off to Cost of Goods Sold. During 2014, Jamison recorded the following:

Budgeted manufacturing overhead costs

$4,400,000

Budgeted direct labor-hours

200,000

Actual manufacturing overhead costs

$4,650,000

Actual direct labor-hours

212,000

Required:

1. Compute the budgeted manufacturing overhead rate.

2. Prepare the summary journal entry to record the allocation of manufacturing overhead.

3. Compute the amount of under- or overallocated manufacturing overhead. Is the amount

significant enough to warrant proration of overhead costs, or would it be permissible to write

it off to cost of goods sold? Prepare the journal entry to dispose of the under– or overallocated

overhead.

SOLUTION

1. Budgeted manufacturing overhead rate =

$4,400,000

200,000 labor-hours

= $22 per direct labor-hour

2. Work-in–Process Control 4,664,000

Manufacturing Overhead Allocated 4,664,000

(212,000 direct labor-hours $22 per direct labor-hour = $4,664,000)

3. $4,650,000– $4,664,000 = $74,000 overallocated, an insignificant amount of difference

compared to manufacturing overhead costs allocated $14,000 ÷ $4,664,000 = 0.3%. If the

quantities of work-in-process and finished goods inventories are small, the difference between

proration and write off to Cost of Goods Sold account would be very small compared to net

income.

Manufacturing Overhead Allocated 4,664,000

Manufacturing Department Overhead Control 4.650,000

Cost of Goods Sold 14,000

4-24 (35−45 min.) Job costing, journal entries.

The University of Chicago Press is wholly owned by the university. It performs the bulk of its

work for other university departments, which pay as though the press were an outside business

enterprise. The press also publishes and maintains a stock of books for general sale. The press uses

normal costing to cost each job. Its job-costing system has two direct-cost categories (direct

materials and direct manufacturing labor) and one indirect-cost pool (manufacturing overhead,

allocated on the basis of direct manufacturing labor costs).

The following data (in thousands) pertain to 2014:

Direct materials and supplies purchased on credit

$ 800

Direct materials used

710

Indirect materials issued to various production departments

100

Direct manufacturing labor

1,300

Indirect manufacturing labor incurred by various production departments

900

Depreciation on building and manufacturing equipment

400

Miscellaneous manufacturing overhead* incurred by various production departments

(ordinarily would be detailed as repairs, photocopying, utilities, etc.)

550

Manufacturing overhead allocated at 160% of direct manufacturing labor costs

?

Cost of goods manufactured

4,120

Revenues

8,000

Cost of goods sold (before adjustment for under- or overallocated manufacturing overhead)

4,020

Required:

1. Prepare an overview diagram of the job-costing system at the University of Chicago Press.

2. Prepare journal entries to summarize the 2014 transactions. As your final entry, dispose of the

year- end under- or overallocated manufacturing overhead as a writeoff to Cost of Goods Sold.

Number your entries. Explanations for each entry may be omitted.

3. Show posted T-accounts for all inventories, Cost of Goods Sold, Manufacturing Overhead

Control, and Manufacturing Overhead Allocated.

4. How did the University of Chicago Press perform in 2014?

*The term manufacturing overhead is not used uniformly. Other terms that are often encountered

in printing companies include job overhead and shop overhead.

Inventories, December 31, 2013 (not 2014):

Materials Control

100

Work-in–Process Control

60

Finished Goods Control

500