1) When fixed costs are $50,000 and variable costs are 60% of the selling price, then

breakeven sales are ________.

A) $115,000

B) $125,000

C) $175,000

D) $275,000

2) A budget ________.

A) is the qualitative expression of a proposed plan of action by management

B) is an aid to coordinating what needs to be done to execute a plan

C) helps in identifying problems and uncertainties

D) promotes production automation

3) The ________ is primarily responsible for management accounting and financial

accounting.

A) COO (Chief Operating Officer)

B) CIO (Chief Information Officer)

C) treasurer

D) controller

4) Cysco Corp has a budget of $1,200,000 in 2015 for prevention costs. If it decides to

automate a portion of its prevention activities, it will save $100,000 in variable costs.

The new method will require $50,000 in training costs and $140,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 200,000 units.

Appraisal costs for the year are budgeted at $500,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $30 per failed unit of

finished goods. The internal failure rate is expected to be 5% of all completed items.

The proposed changes will cut the internal failure rate by one-half. Internal failure units

are destroyed. External failure costs average $50 per failed unit. The company’s average

external failures average 2.5% of units sold. The new proposal will reduce this rate to

1%. Assume all units produced are sold and there are no ending inventories.

Management has offered to allow the prevention changes if all changes take place as

anticipated and the amounts netted are less than the cost of the equipment. What is the

net impact of all the changes created by the preventive changes?

A) $185,200

B) $(230,000)

C) $(234,000)

D) $(250,000)

5) If the contribution margin ratio is 0.25, targeted operating income is $50,000, and

targeted sales volume in dollars is $250,000, then total fixed costs are ________.

A) $11,500

B) $15,000

C) $20,000

D) $12,500

6) ________ is an organization’s ability to offer products or services that are perceived

by its customers as being superior and unique relative to those of its competitors.

A) Strategy

B) Product differentiation

C) Cost leadership

D) The balanced scorecard

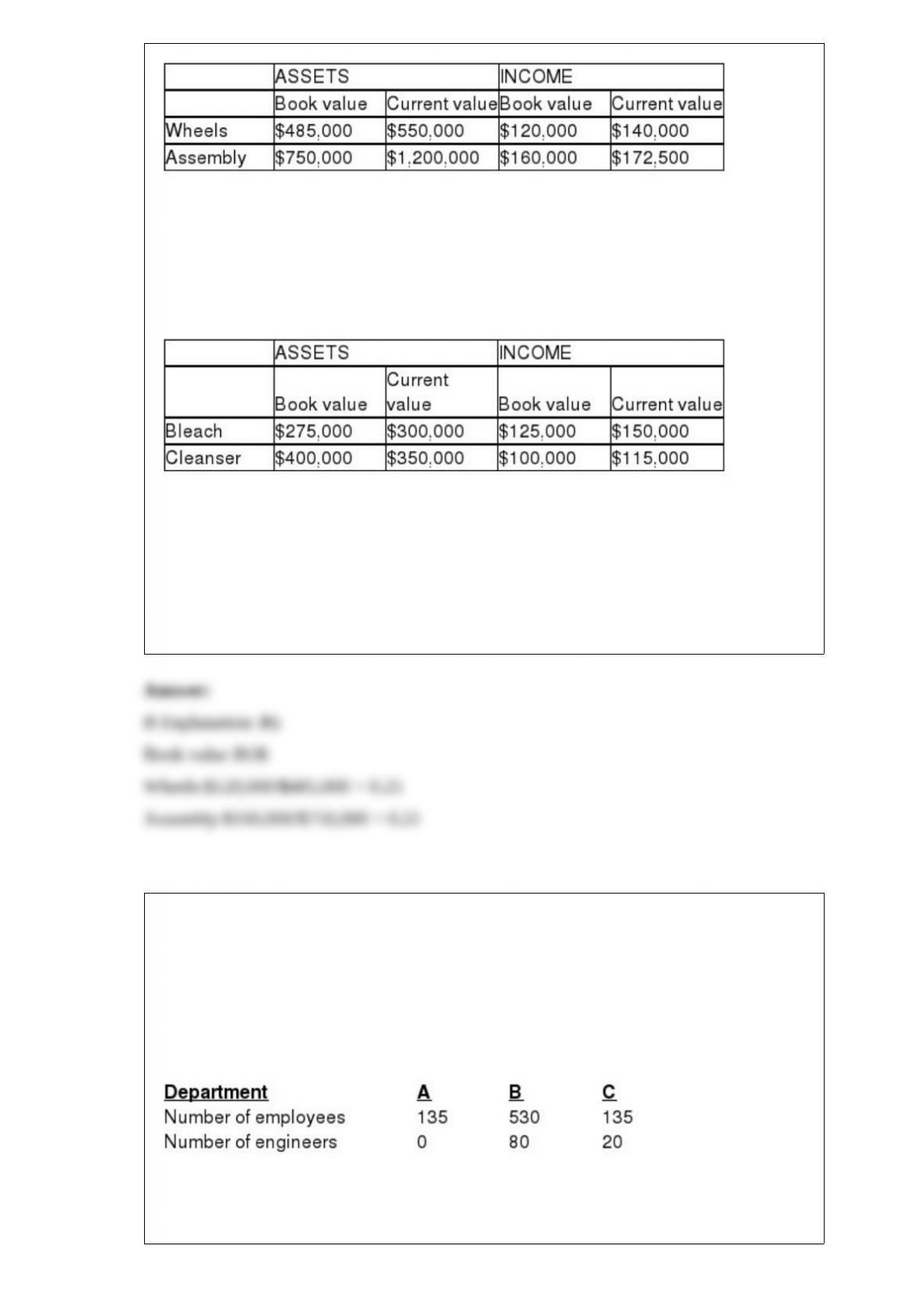

7) Carriage Incorporated manufactures horse carriages. The company has two divisions,

Wheels and Assembly. Because of different accounting methods and inflation rates, the

company is considering multiple evaluation measures. The following information is

provided for 2015:

The company is currently using a 12% required rate of return.

Home Decor Inc., manufactures home cleaning products. The company has two

divisions, Bleach and Cleanser. Because of different accounting methods and inflation

rates, the company is considering multiple evaluation measures. The following

information is provided for 2015:

The company is currently using a 15% required rate of return.

What are Wheels’s and Assembly’s return on investment based on book values,

respectively?

A) 0.21; 0.25

B) 0.25; 0.21

C) 0.14; 0.25

D) 0.25; 0.14

8) At the Verill Company, the cost of the library and information center has always been

charged to the various departments based upon number of employees. Recently,

opinions gathered from the department managers indicate that the number of engineers

within a department might be a better predictor of library and information center costs.

Total library and information center costs are $200,000.

What were total fixed costs for 2015?

A) $924,000

B) $576,000

C) $348,000

D) $224,000

9) Using the high-low method, the estimate of the fixed component of office expense

per month is closest to:

A) $9,606

B) $13,485

C) $13,181

D) $13,793

10) The method that allocates costs in each cost pool using the same rate per unit is

known as the ________.

A) incremental cost-allocation method

B) reciprocal cost-allocation method

C) single-rate cost allocation method

D) dual-rate cost-allocation method

11) For planning, control, and decision-making purposes:

A) fixed costs should be converted to a per unit basis.

B) discretionary fixed costs should be eliminated.

C) variable costs should be ignored.

D) mixed costs should be separated into their variable and fixed components.

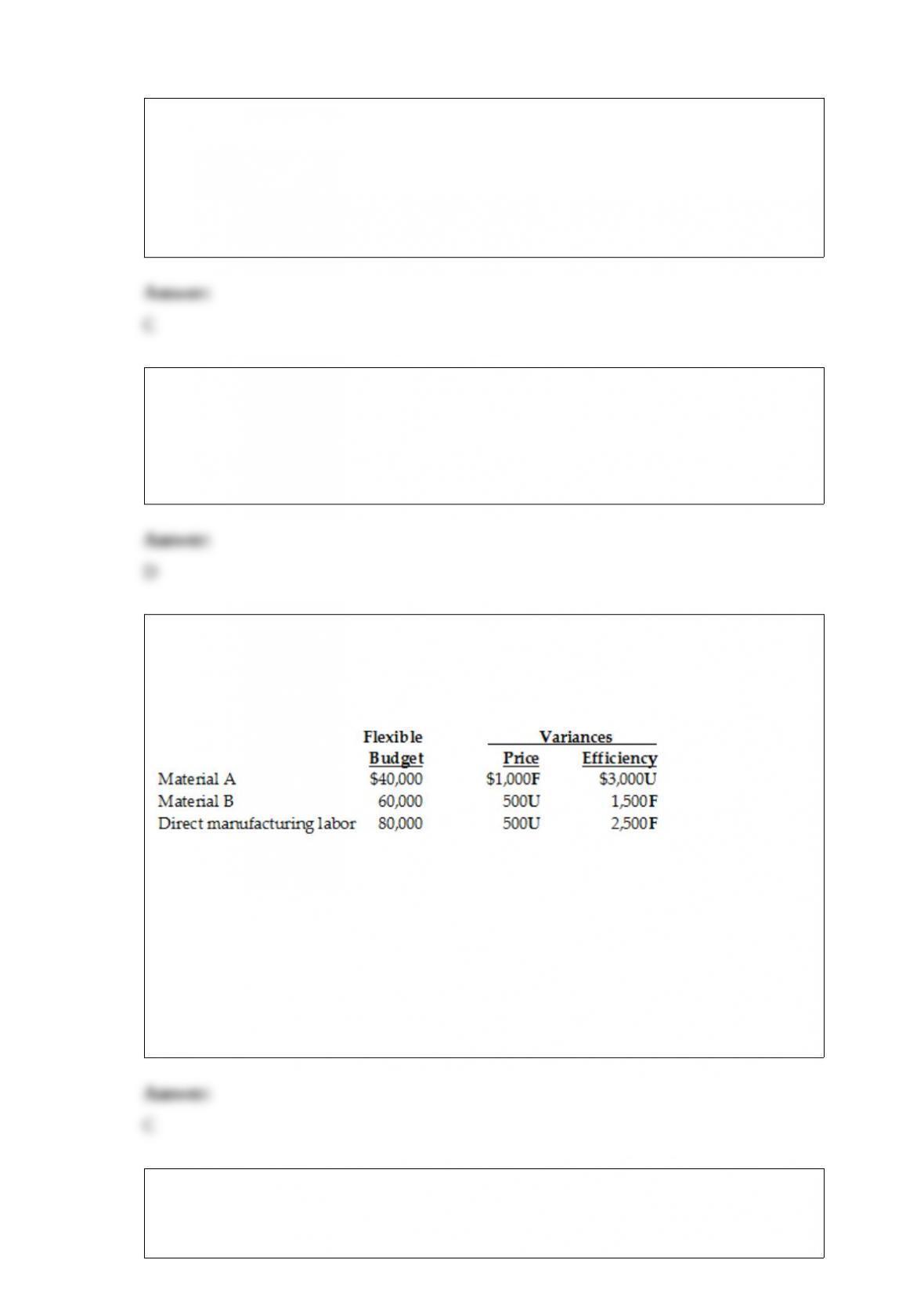

12) Berman’s Camera Shop has prepared the following flexible budget for September

and is in the process of interpreting the variances. F denotes a favorable variance and U

denotes an unfavorable variance.

The most likely explanation of the above direct manufacturing labor variances is that

________.

A) the average wage rate paid to employees was less than expected

B) employees did not work as efficiently as expected to accomplish the job

C) the company may have assigned more experienced employees this month than

originally planned

D) management may have a problem with budget slack and might be using lax

standards for both labor-wage rates and expected efficiency

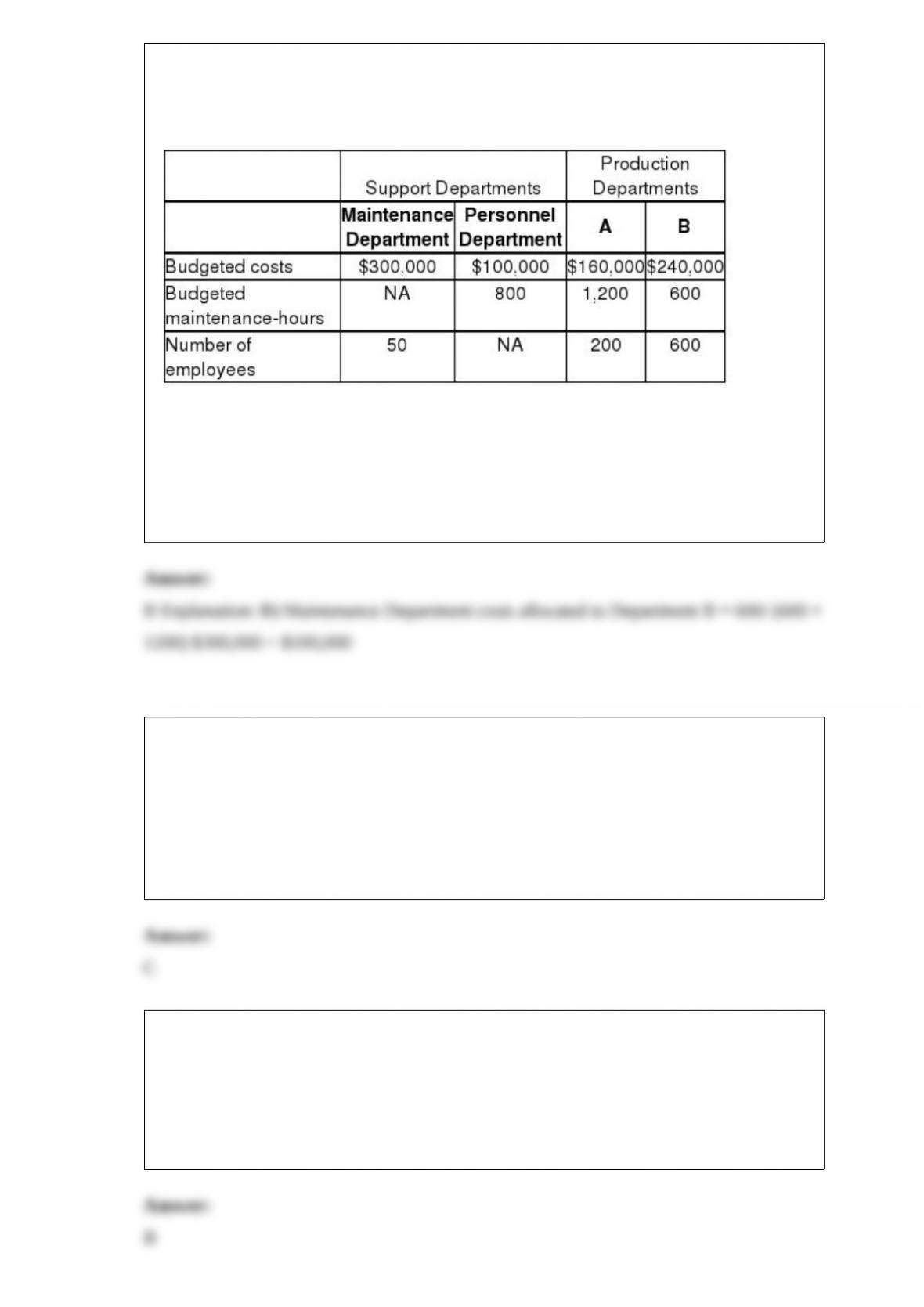

13) Hanung Corp has two service departments, Maintenance and Personnel.

Maintenance Department costs of $300,000 are allocated on the basis of budgeted

maintenance-hours. Personnel Department costs of $100,000 are allocated based on the

number of employees. The costs of operating departments A and B are $160,000 and

$240,000, respectively. Data on budgeted maintenance-hours and number of employees

are as follows:

Using the direct method, what amount of Maintenance Department costs will be

allocated to Department B?

A) $96,000

B) $100,000

C) $110,000

D) $122,000

14) Which of the following terms could be used to correctly describe the cost of the

soap used to wash the denim cloth?

Direct Cost Product Cost

A) Yes Yes

B) Yes No

C) No Yes

D) No No

15) One of the problems in using one set of accounting records for tax reporting and

another set of records for internal management reporting is that ________.

A) it is illegal as well as unethical to do so

B) the tax authorities may suspect manipulation of records

C) it is almost impossible to keep the records straight and hard to reconcile the books

D) the shareholders do not approve of such methods and the market prices will decline

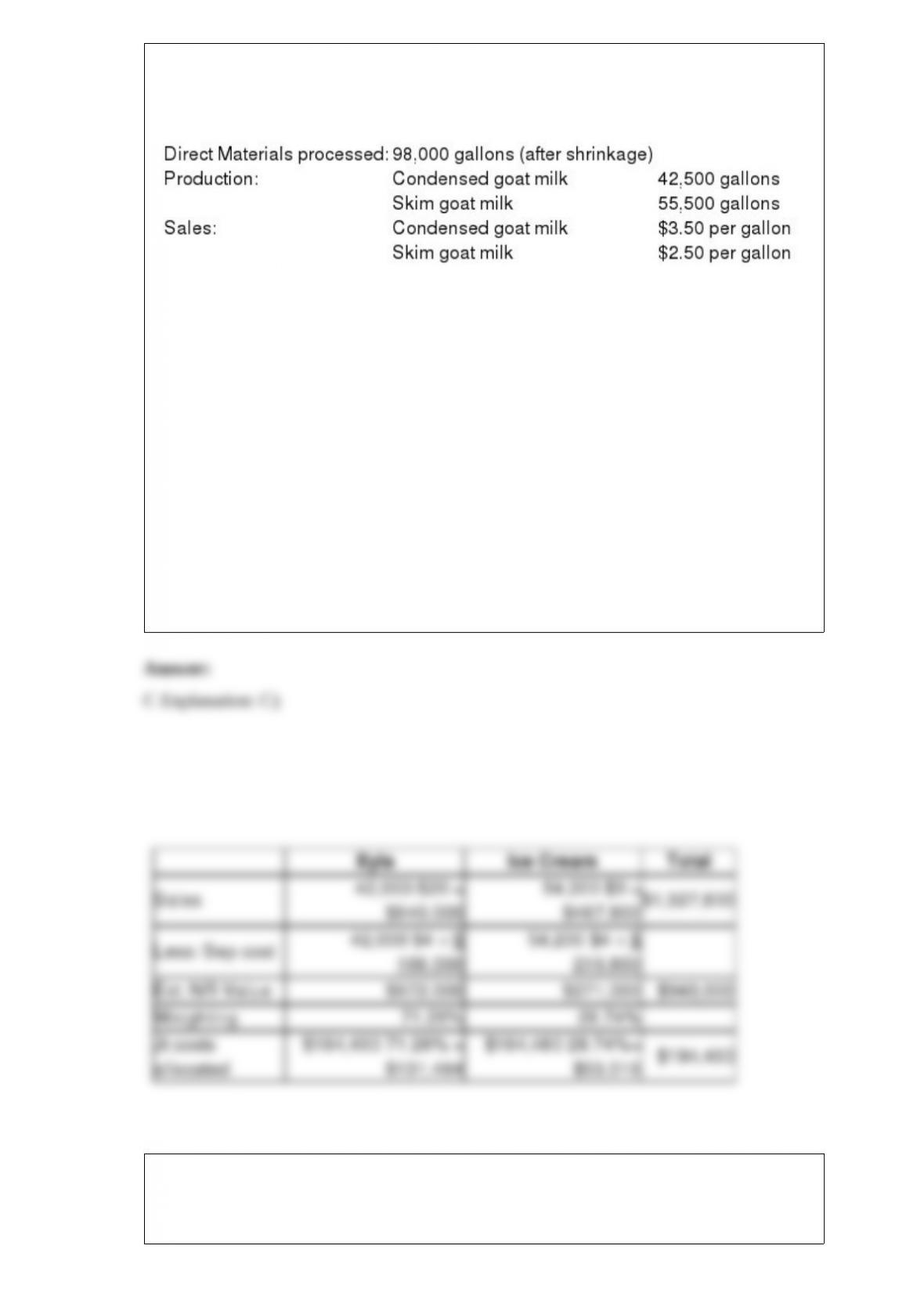

16) The Green Company processes unprocessed goat milk up to the splitoff point where

two products, condensed goat milk and skim goat milk result. The following

information was collected for the month of October:

The costs of purchasing the of unprocessed goat milk and processing it up to the splitoff

point to yield a total of 98,000 gallons of saleable product was $184,480. There were no

inventory balances of either product.

Condensed goat milk may be processed further to yield 42,000 gallons (the remainder is

shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $4

per usable gallon. Xyla can be sold for $20 per gallon.

Skim goat milk can be processed further to yield 54,200 gallons of skim goat ice cream,

for an additional processing cost per usable gallon of $4. The product can be sold for $9

per gallon.

There are no beginning and ending inventory balances.

What is the estimated net realizable value of Xyla at the splitoff point?

A) $271,000

B) $287,400

C) $672,000

D) $712,600

17) If separable costs of Butter Cream was 16,000 and constant gross margin was 25%,

what would have been the total allocated joint costs of production?

A) $37,675

B) $33,700

C) $30,238

D) $34,500

18) Unfavorable direct material price variances are ________.

A) always credits

B) always debits

C) credited to the Materials Control account

D) credited to the Accounts Payable Control account

19) Which of the following increases (are debited to) the Work-in-Process Control

account?

A) actual plant insurance costs

B) customer services costs

C) marketing expenses

D) direct manufacturing labor costs

20) The cost of goods sold for March was:

A) $146,000

B) $150,000

C) $142,000

D) $237,000