Absorption-costing

Variable costing

Fixed manufacturing

Fixed manufacturing

Variable manufacturing costs: $5.10 × 294,900

1,503,990

Cost of goods available for sale

1,937,490

Deduct ending inventory: $5.10 × 34,500

(175,950)

Variable cost of goods sold

1,761,540

Variable operating costs: $1.10 × 345,400

379,940

Adjustment for variances

0

Total variable costs

2,141,480

Contribution margin

5,457,320

Fixed costs

Fixed manufacturing overhead costs

1,440,000

Fixed operating costs

1,080,000

Total fixed costs

2,520,000

Operating income

$2,937,320

Absorption Costing Data

Fixed manufacturing overhead allocation rate =

Fixed manufacturing overhead/Denominator level machine-hours = $1,440,000

6,000

= $240 per machine-hour

Fixed manufacturing overhead allocation rate per unit =

Fixed manufacturing overhead allocation rate/standard production rate = $240

50

= $4.80 per unit

Income Statement for the Zwatch Company, Absorption Costing

for the Year Ended December 31, 2014

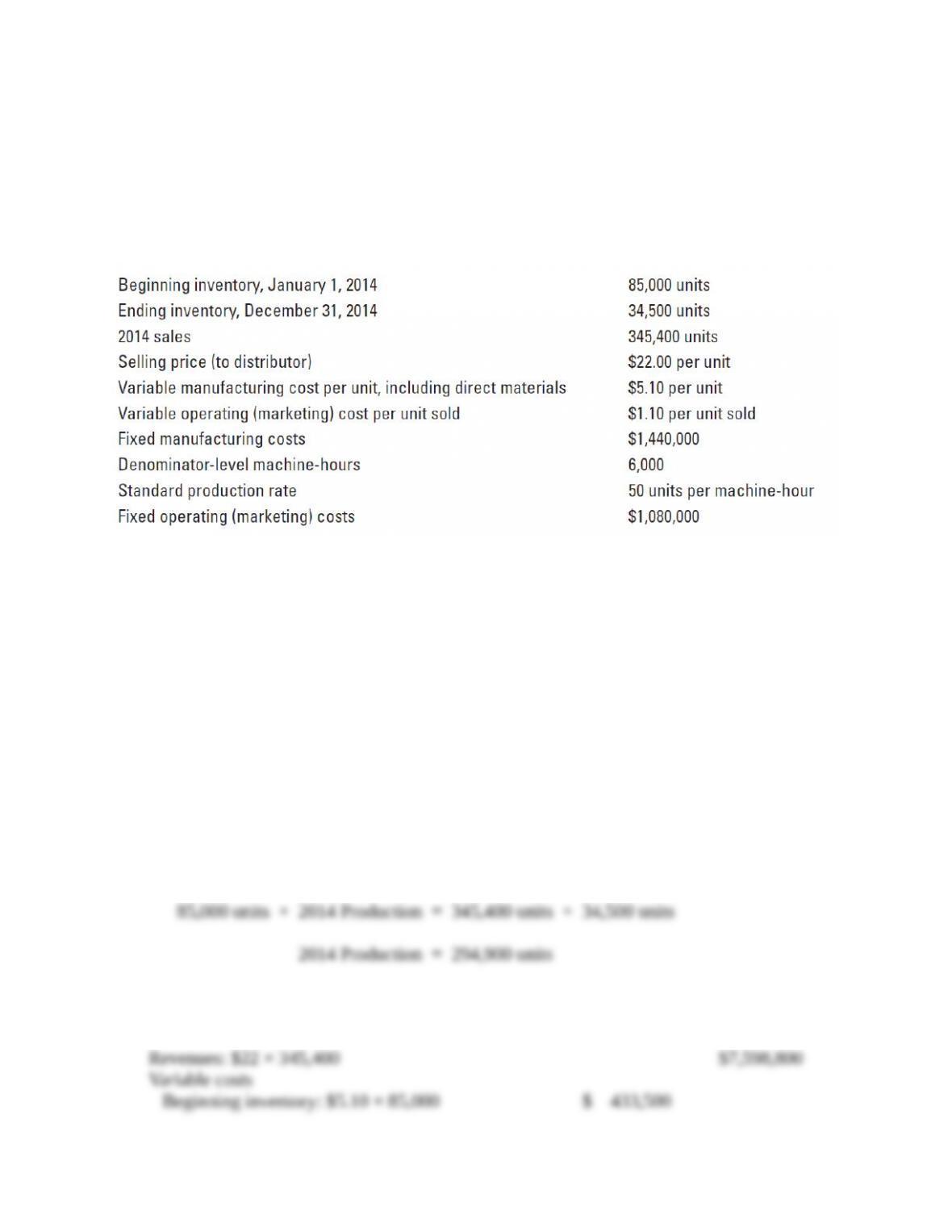

Revenues: $22 × 345,400

$7,598,800

Cost of goods sold

Beginning inventory ($5.10 + $4.80) × 85,000

$ 841,500

Variable manuf. costs: $5.10 × 294,900

1,503,990

Allocated fixed manuf. costs: $4.80 × 294,900

1,415,520

Cost of goods available for sale

$3,761,010

Deduct ending inventory: ($5.10 + $4.80) × 34,500

(341,550)

Adjust for manuf. variances ($4.80 × 5,100)a

24,480 U

Cost of goods sold

3,443,940

Gross margin

4,154,860

Operating costs

Variable operating costs: $1.10 × 345,400

$ 379,940

Fixed operating costs

1,080,000

Total operating costs

1,459,940

Operating income

$2,694,920

a Production volume variance = [(6,000 hours × 50) – 294,900] × $4.80

= (300,000 – 294,900) × $4.80

= $24,480

Total fixed costs

3,531,850

Operating income

$1,543,150

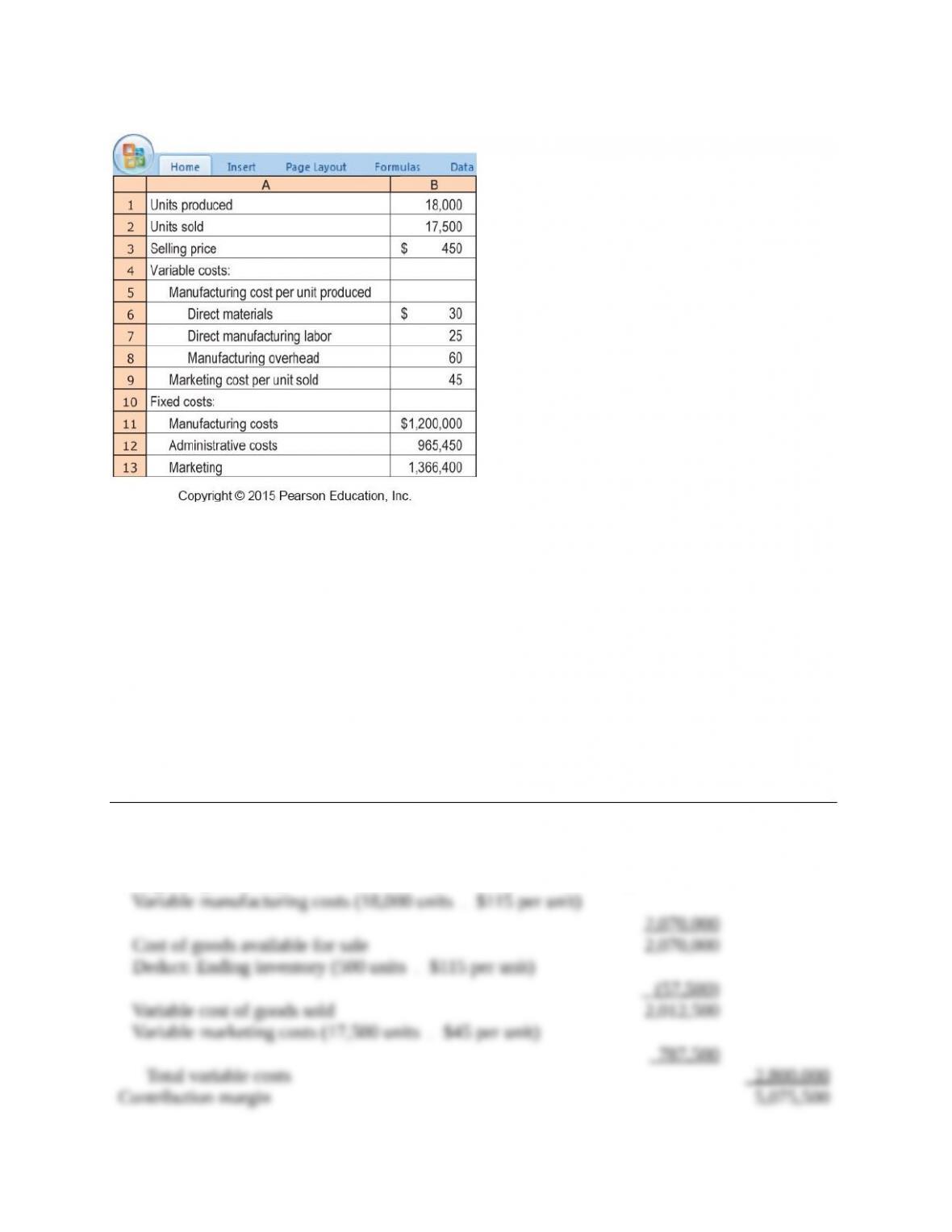

2. Fixed manufacturing overhead rate = $1,200,000 / 20,000 units = $60 per unit

2014 Absorption-Costing Based Income Statement

Revenues (17,500 units

$450 per unit)

$7,875,500

Cost of goods sold

Beginning inventory

$ 0

Variable manufacturing costs (18,000 units

$115 per unit)

2,070,000

Allocated fixed manufacturing costs (18,000 units

$60 per unit)

1,080,000

Cost of goods available for sale

3,150,000

Deduct ending inventory [500 units

($115 + $60) per unit]

(87,500)

Add unfavorable production volume variance

120,000a U

Cost of goods sold

3,182,500

Gross margin

4,692,500

Operating costs

Variable marketing costs (17,500 units

$45 per unit)

787,500

Fixed administrative costs

965,450

Fixed marketing

1,366,400

Total operating costs

3,119,350

Operating income

$1,573,150

a PVV = $1,200,000 budgeted fixed mfg. costs – $1,080,000 allocated fixed mfg. costs = $120,000 U

3. 2014 operating income under absorption costing is greater than the operating income under

variable costing because in 2014 inventory increased by 500 units. As a result, under absorption

costing, a portion of the fixed overhead remained in the ending inventory and led to a lower cost

of goods sold (relative to variable costing). As shown below, the difference in the two operating

incomes is exactly the same as the difference in the fixed manufacturing costs included in ending

versus beginning inventory (under absorption costing).

Operating income under absorption costing

$1,573,150

Operating income under variable costing

1,543,150

Difference in operating income under absorption versus variable

costing

$ 30,000

Under absorption costing:

Fixed mfg. costs in ending inventory (500 units

$60 per unit)

$ 30,000

Fixed mfg. costs in beginning inventory (0 units

$60 per unit)

0

Change in fixed mfg. costs between ending and beginning inventory

$ 30,000

4. Relative to the alternative of using contribution margin (from variable costing), the