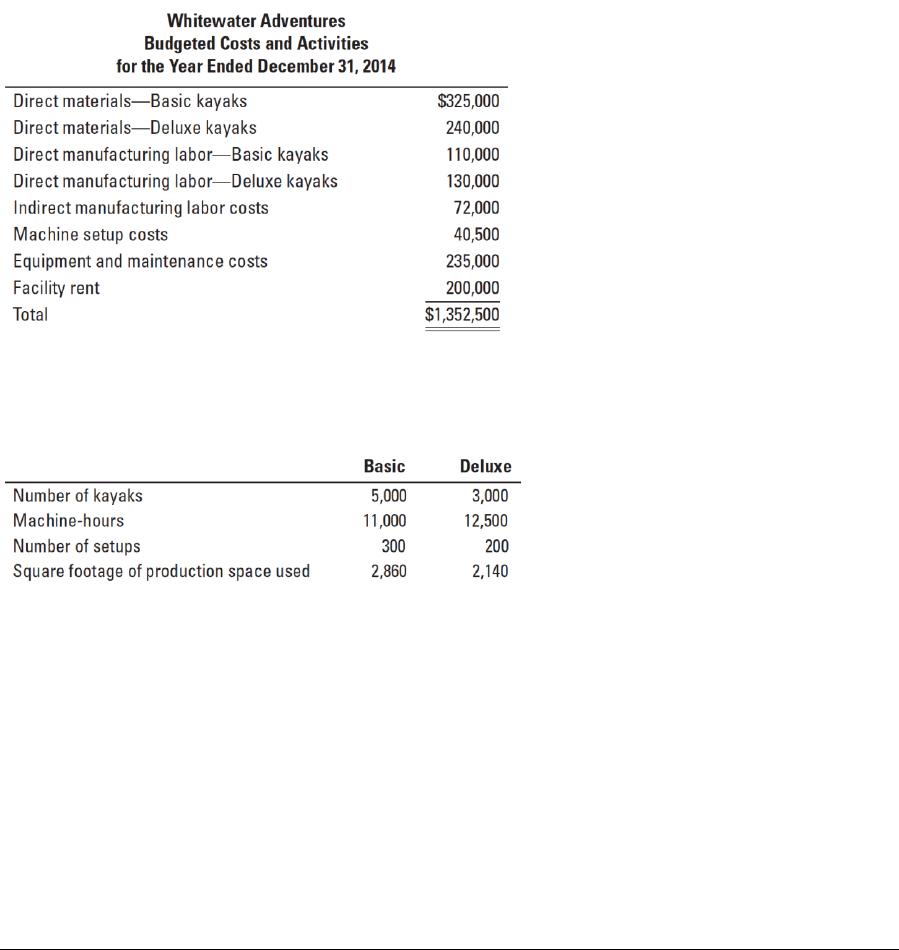

Machine setup costs

$ 40,500

500 batches

$81/batch

Equipment and

maintenance costs

$235,000

23,500 MH

$10/MH

Facility rent costs

$200,000

6,250 sq. ft.

$32/sq. ft.

1. Budgeted cost of unused capacity = $32 per sq. ft. (6,250 – 2,860 −2,140) sq. ft.

= $32 1,250 sq. ft. = $40,000

3.

Basic

Deluxe

Direct materials

$325,000

$240,000

Direct manufacturing labor

110,000

130,000

Indirect manuf. labor ($110,000 and $130,000 30%)

33,000

39,000

Machine setup (300 and 200 batches $81/batch)

24,300

16,200

Equipment and maintenance costs (11,000 and

12,500 MH $10/MH)

110,000

125,000

Facility rent (2,860 and 2,140 sq. ft. $32/sq. ft.)

91,520

68,480

Total cost

$693,820

$618,680

Divided by number of units

5,000

3,000

Cost per unit

$ 138.76

$ 206.23

4. Although the excess capacity is currently costing Whitewater $40,000 annually, having excess

capacity allows for the company to accept special orders if they are received, expand production

of either of the existing models, or add a new product line in the future. Whitewater should

consider if there is available labor and machine hours before increasing production to use the space,

as well as demand for the product. Whitewater may also consider renting out the available space

to a compatible outside user, with the option to take the space back if needed.

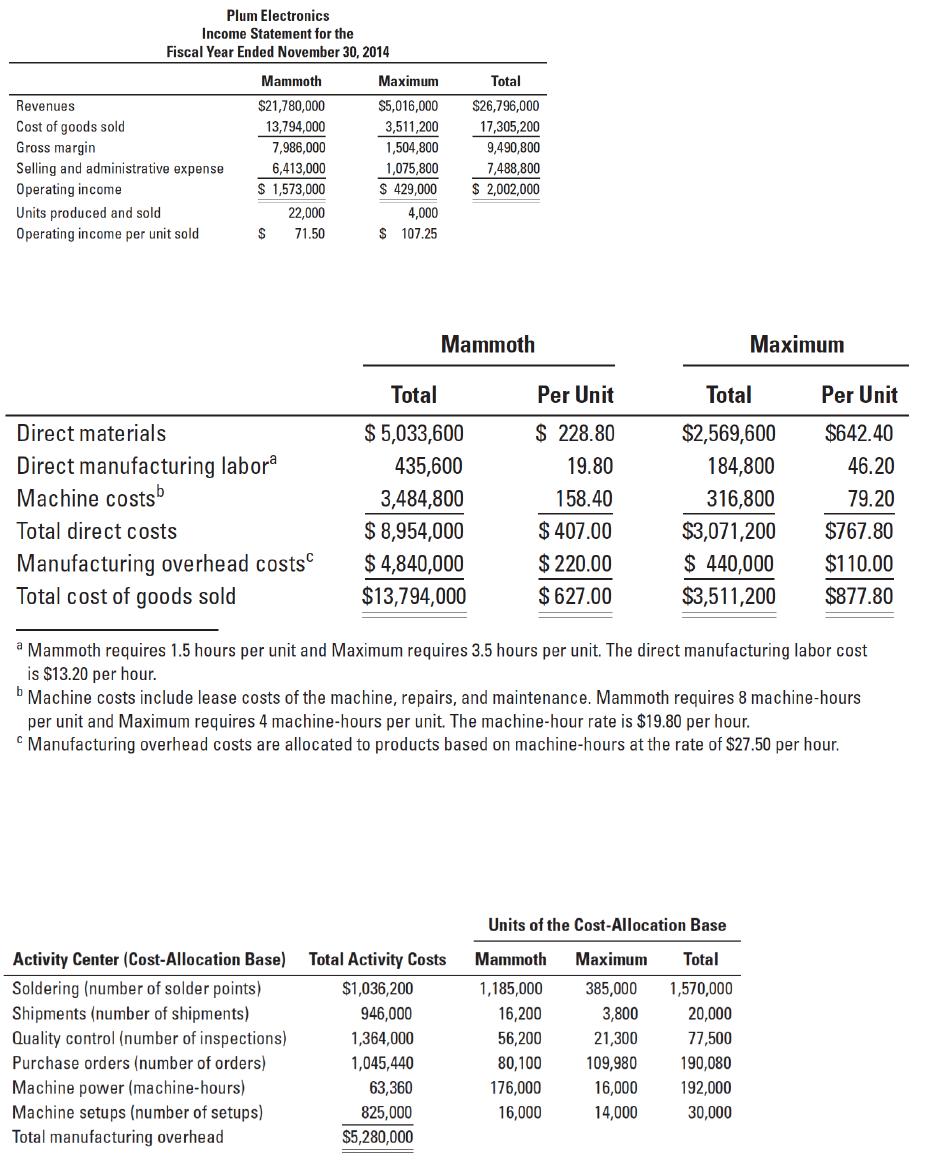

5-41 (50 min.) ABC, implementation, ethics.

(CMA, adapted) Plum Electronics, a division of Berry Corporation, manufactures two large-screen

television models: the Mammoth, which has been produced since 2010 and sells for $990, and the

Maximum, a newer model introduced in early 2012 that sells for $1,254. Based on the following

income statement for the year ended November 30, 2014, senior management at Berry have

decided to concentrate Plum’s marketing resources on the Maximum model and to begin to phase

out the Mammoth model because Maximum generates a much bigger operating income per unit.

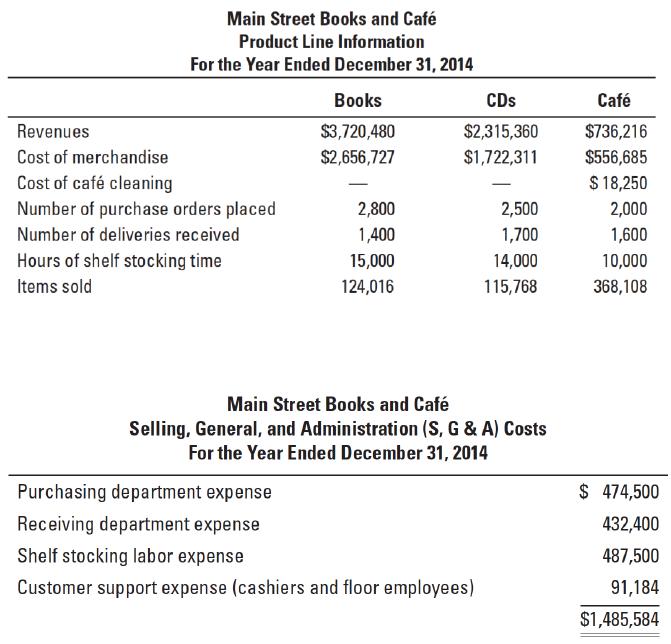

Total S, G, & A costs

516,903

511,265

475,666

1,503,834

Operating income

$ 546,850

$ 81,784

$(296,135)

$ 332,499

Comparing product line income statements in requirements 1 and 2, it appears that books are much

more profitable and café loses a lot more money under the ABC system compared to the simple

system. The reason is that books use far fewer S,G, & A resources relative to its merchandise

costs, and café uses far greater S, G, & A resources relative to its merchandise costs.

3.

To: Main Street Books and Café Management Team

From: Cost Analyst

Re: Costing System

The current accounting system allocates indirect costs (S,G, & A) to product lines based on the

Cost of Merchandise sold. Using this method, the S, G, & A costs are assigned 54%, 35%, 11%,

to the Books, CDs, and Café product lines, respectively.

I recommend that the organization switch to an activity-based costing (ABC) method. With ABC,

the product lines are assigned indirect costs based on their consumption of the activities that give

rise to the costs. An ABC analysis reveals that the Café consumes considerably more than 11% of

indirect costs. Instead, the café generally requires 25–35% of the purchasing, receiving, and

stocking activity and 60% of the customer support.

The current accounting technique masks the losses being produced by the café because it assumes

all indirect costs are driven by the dollar amount of merchandise sold. By adopting ABC,

management can evaluate the costs of operating the three product lines and make more informed

pricing and product mix decisions. For example, management may want to consider increasing

prices of the food and drinks served in the café. Before deciding whether to increase prices or to

close the café, management must consider the beneficial effect that having a cafe has on the other

product lines.

An ABC analysis can also help Main Street Books and Café manage its costs by reducing the

number of activities that each product line demands and by reducing the cost of each activity.

These actions will improve the profitability of each product line. ABC analysis can also be used

to plan and manage the various activities.