Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

SOLUTION

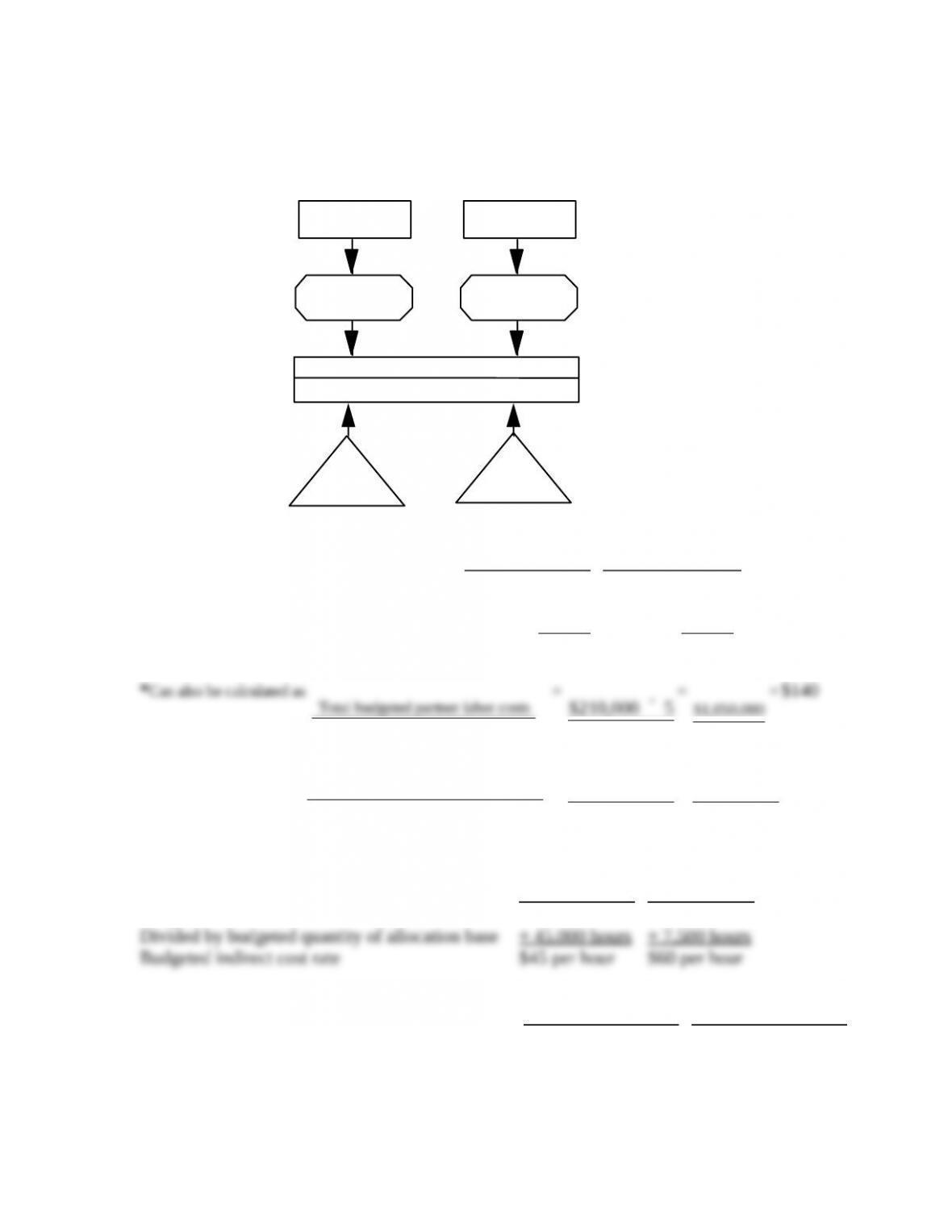

Although not required, the following overview diagram is helpful to understand Kidman’s

job-costing system.

Professional

Labor-Hours

General

Support

COST OBJECT:

JOB FOR

CLIENT

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

}

DIRECT

COST

Indirect Costs

Direct Costs

Partner

Labor-Hours

Secretarial

Support

Professional

Associate Labor

Professional

Partner Labor

1. Professional

Partner Labor

Professional

Associate Labor

Budgeted compensation per professional

Divided by budgeted hours of billable

time per professional

Budgeted direct-cost rate

$ 210,000

÷1 ,500

$140 per hour*

$75,000

÷1 ,500

$50 per hour†

*Can also be calculated as

Total budgeted partner labor costs

Total budgeted partner labor - hours

=

´

´

=

†Can also be calculated as

Total budgeted associate labor costs

Total budgeted associate labor - hours

=

= $50

2. General

Support

Secretarial

Support

Budgeted total costs

Divided by budgeted quantity of allocation base

Budgeted indirect cost rate

$2,025,000

3. Richardson Punch

Direct costs:

Professional partners,

$140 48 hr.; $140 32 hr.

Professional associates,

$50 72 hr.; $50 128 hr.

Direct costs

Indirect costs:

General support,

$45 120 hr.; $45 160 hr.

Secretarial support,

$60 48 hr.; $60 32 hr.

Indirect costs

Total costs

$6,720

4. Richardson Punch

Single direct – Single indirect

(from Problem 4-32)

Multiple direct – Multiple indirect

(from requirement 3 of Problem 4-33)

Difference

$14,400

The Richardson and Punch jobs differ in their use of resources. The Richardson job has a

mix of 40% partners and 60% associates, while Punch has a mix of 20% partners and 80%

5. I would recommend that Kidman & Associates use the job costing system in this problem

with two direct- and two indirect- cost categories.

Kidman & Associates should use multiple categories of direct costs (partner labor and

professional labor) because the costs of the different categories of labor are very different and

Kidman should use multiple indirect cost pools because partners use additional secretarial

The job costing system in this problem more accurately represents the costs incurred on

different jobs and therefore helps managers make better decisions.

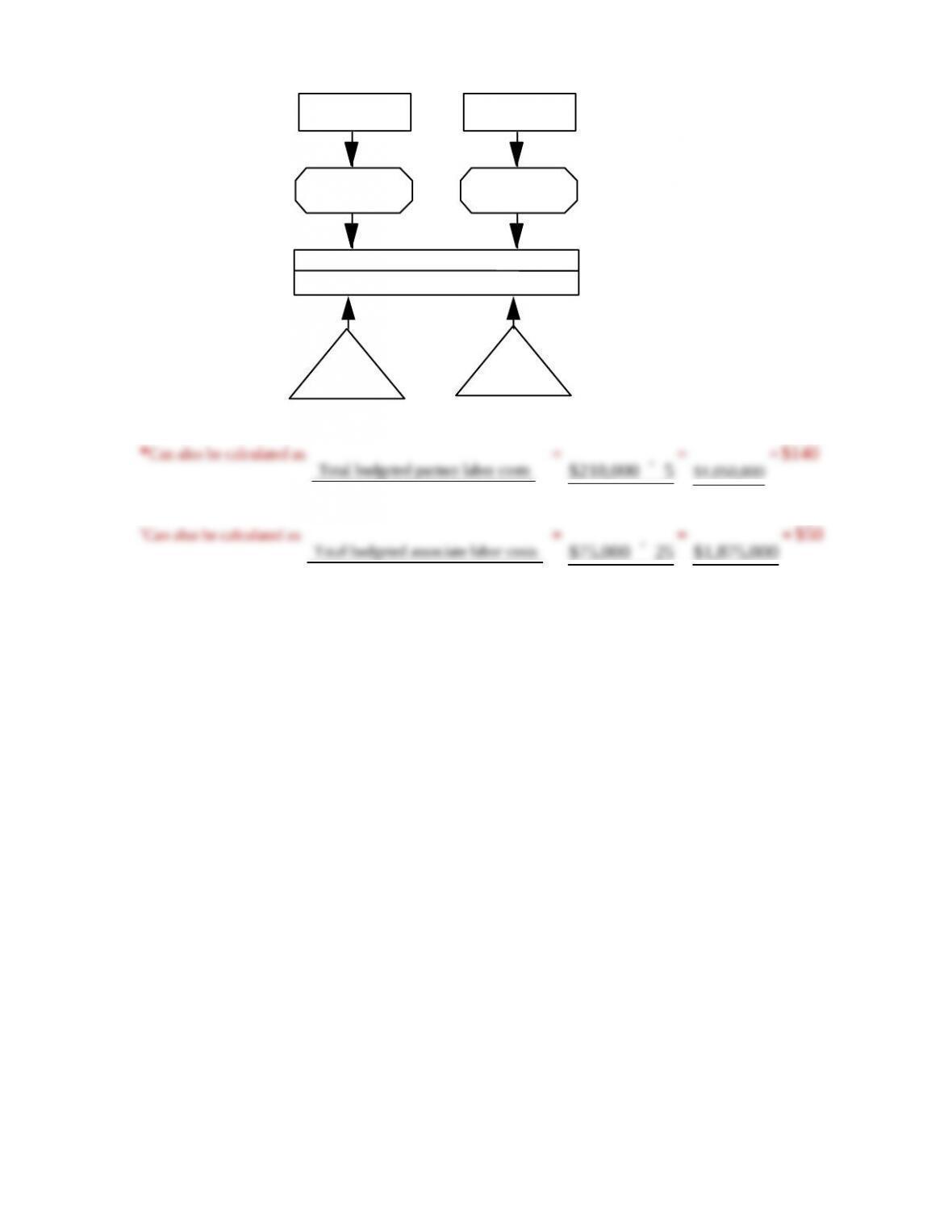

Professional

Labor-Hours

General

Support

COST OBJECT:

JOB FOR

CLIENT

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

}

DIRECT

COST

Indirect Costs

Direct Costs

Partner

Labor-Hours

Secretarial

Support

Professional

Associate Labor

Professional

Partner Labor

*Can also be calculated as

Total budgeted partner labor costs

Total budgeted partner labor - hours

=

´

´

=

†Can also be calculated as

Total budgeted associate labor costs

Total budgeted associate labor - hours

=

4-34 (2025 min.) Proration of overhead.

(Z. Iqbal, adapted) The Zaf Radiator Company uses a normal-costing system with a single

manufacturing overhead cost pool and machine-hours as the cost-allocation base. The

following data are for 2014:

Budgeted manufacturing overhead costs $4,800,000

Overhead allocation base Machine-hours

Budgeted machine-hours 80,000

Manufacturing overhead costs incurred $4,900,000

Actual machine-hours 75,000

Machine-hours data and the ending balances (before proration of under- or overallocated

overhead) are as follows:

Actual Machine-Hours 2014 End-of-Year Balance

Cost of Goods Sold 60,000 $8,000,000

Finished Goods Control 11,000 1,250,000

Work-in-Process Control 4,000 750,000

Required:

1. Compute the budgeted manufacturing overhead rate for 2014.

2. Compute the under- or overallocated manufacturing overhead of Zaf Radiator in 2014.

Dispose of this amount using the following:

a. Writeoff to Cost of Goods Sold

b. Proration based on ending balances (before proration) in Work-in-Process Control,

Finished Goods Control, and Cost of Goods Sold

c. Proration based on the overhead allocated in 2014 (before proration) in the ending

balances of Work-in-Process Control, Finished Goods Control, and Cost of Goods Sold

3. Which method do you prefer in requirement 2? Explain.

SOLUTION

2.

Manufacturing overhead

underallocated

=

Manufacturing overhead

incurred

–

Manufacturing overhead

allocated

a. Write-off to Cost of Goods Sold

Account

(1)

Dec. 31, 2014

Account

Balance

(Before Proration)

(2)

Write-off

of $400,000

Underallocated

Manufacturing

Overhead

(3)

Dec. 31, 2014

Account

Balance

(After Proration)

(4) = (2) + (3)

Work in Process

Finished Goods

Cost of Goods Sold

Total

$ 750,000

b. Proration based on ending balances (before proration) in Work in Process, Finished

Goods, and Cost of Goods Sold.

Account

(1)

Dec. 31, 2014

Account Balance

(Before Proration)

(2)

Proration of $400,000

Underallocated

Manufacturing

Overhead

(3)

Dec. 31, 2014

Account

Balance

(After Proration)

(4) = (2) + (3)

Work in Process

Finished Goods

Cost of Goods Sold

Total

$ 750,000

$ 780,000

c. Proration based on the allocated overhead amount (before proration) in the ending

balances of Work in Process, Finished Goods, and Cost of Goods Sold.

Account

(1)

Dec. 31, 2014

Account

Balance

(Before

Proration)

(2)

Allocated Overhead

Included in

Dec. 31, 2014

Account Balance

(Before Proration)

(3) (4)

Proration of $400,000

Underallocated

Manufacturing Overhead

(5)

Dec. 31, 2014

Account

Balance

(After

Proration)

(6) = (2) + (5)

Work in Process

$

750,000 $ 240,000a(5.33%) 0.0533$400,000 = $ 21,320 $ 771,320

3. Alternative (c) is theoretically preferred over (a) and (b) because the underallocated

Chapter 4 also discusses an adjusted allocation rate approach that results in the same

2.

Manufacturing overhead

underallocated

=

Manufacturing overhead

incurred

–

Manufacturing overhead

allocated

4-35 (15 min.) Normal costing, overhead allocation, working backward.

Gardi Manufacturing uses normal costing for its job-costing system, which has two direct-cost

categories (direct materials and direct manufacturing labor) and one indirect-cost category

(manufacturing overhead). The following information is obtained for 2014:

Total manufacturing costs, $8,300,000

Manufacturing overhead allocated, $4,100,000 (allocated at a rate of 250% of direct

manufacturing labor costs)

Work-in-process inventory on January 1, 2014, $420,000

Cost of finished goods manufactured, $8,100,000

Required:

1. Use information in the first two bullet points to calculate (a) direct manufacturing labor

costs in 2014 and (b) cost of direct materials used in 2014.

2. Calculate the ending work-in-process inventory on December 31, 2014.

SOLUTION

Direct manufacturing labor costs =

b.

Total manufacturing

cost

=

Cost of direct

materials used

+

Direct manufacturing

labor cost

+

Manufacturing

overhead allocated

2.

Work in process

1/1/2014

+

Total

manufacturing cost

=

Cost of goods

manufactured

+

Work in process

12/31/2014

2.

Work in process

1/1/2014

+

Total

manufacturing cost

=

Cost of goods

manufactured

+

Work in process

12/31/2014

4-36 (15 min.) Proration of overhead with two indirect cost pools.

Premier Golf Carts makes custom golf carts that it sells to dealers across the Southeast. The carts

are produced in two departments, fabrication (a mostly automated department) and custom

finishing (a mostly manual department). The company uses a normal-costing system in which

overhead in the fabrication department is allocated to jobs on the basis of machine-hours and

overhead in the finishing department is allocated to jobs based on direct labor-hours. During

May, Premier Golf Carts reported actual overhead of $49,500 in the fabrication department and

$22,200 in the finishing department. Additional information follows:

Manufacturing overhead rate (fabrication department) $20 per machine-hour

Manufacturing overhead rate (finishing department) $16 per direct labor-hour

Machine-hours (fabrication department) for May 2,000 machine-hours

Direct labor-hours (finishing department) for May 1,200 labor-hours

Work in process inventory, May 31 $50,000

Finished goods inventory, May 31 $150,000

Cost of goods sold, May $300,000

Premier Golf Carts prorates under- and overallocated overhead monthly to work in process,

finished goods, and cost of goods sold based on the ending balance in each account.

Required:

1. Calculate the amount of overhead allocated in the fabrication department and the finishing

department in May.

2. Calculate the amount of under- or overallocated overhead in each department and in total.

3. How much of the under- or overallocated overhead will be prorated to (a) work in process

inventory, (b) finished goods inventory, and (c) cost of goods sold based on the ending

balance (before proration) in each of the three accounts? What will be the balance in work in

process, finished goods, and cost of goods sold after proration?

4. What would be the effect of writing off under- and overallocated overhead to cost of goods

sold? Would it be reasonable for Premier Golf Carts to change to this simpler method?

SOLUTION

1. Fabrication department:

Finishing department:

2. Under- or overallocated overhead in each department and in total follows:

Fabrication department:

Finishing department:

3. Underallocated overhead prorated based on ending balances

Account

Account

Balance

(Before

Proration)

(1)

Account Balance

as a Percent of Total

(2) = (1) ÷ $500,000

Proration of $12,500

Underallocated Overhead

(3) = (2)

´

12,500

Account

Balance

(After

Proration)

(4) = (1) + (3)

Work in Process

$ 50,000 0.10

0.10

´

$12,500 = $ 1,250

$ 51,250

Finished Goods

Because Premier Golf Carts is disposing of underallocated costs based on the ending balance in

Work in Process, Finished Goods, and Cost of Goods Sold accounts, it does not have to allocate

4. The ending balance in Cost of Goods Sold would be $312,500 instead of $307,500 if the entire

4-37 (35 min.) General ledger relationships, under- and overallocation.

(S. Sridhar, adapted) Southwick Company uses normal costing in its job-costing system. Partially

completed T-accounts and additional information for Southwick for 2014 are as follows:

Additional information follows:

a. Direct manufacturing labor wage rate was $12 per hour.

b. Manufacturing overhead was allocated at $16 per direct manufacturing labor-hour.

c. During the year, sales revenues were $1,050,000, and marketing and distribution costs were

$125,000.

Required:

1. What was the amount of direct materials issued to production during 2014?

2. What was the amount of manufacturing overhead allocated to jobs during 2014?

3. What was the total cost of jobs completed during 2014?

4. What was the balance of work-in-process inventory on December 31, 2014?

5. What was the cost of goods sold before proration of under- or overallocated overhead?

6. What was the under- or overallocated manufacturing overhead in 2014?

7. Dispose of the under- or overallocated manufacturing overhead using the following:

a. Writeoff to Cost of Goods Sold

b. Proration based on ending balances (before proration) in Work-in-Process Control,

Finished Goods Control, and Cost of Goods Sold

8. Using each of the approaches in requirement 7, calculate Southwick’s operating income for

2014.

9. Which approach in requirement 7 do you recommend Southwick use? Explain your answer

briefly.

SOLUTION

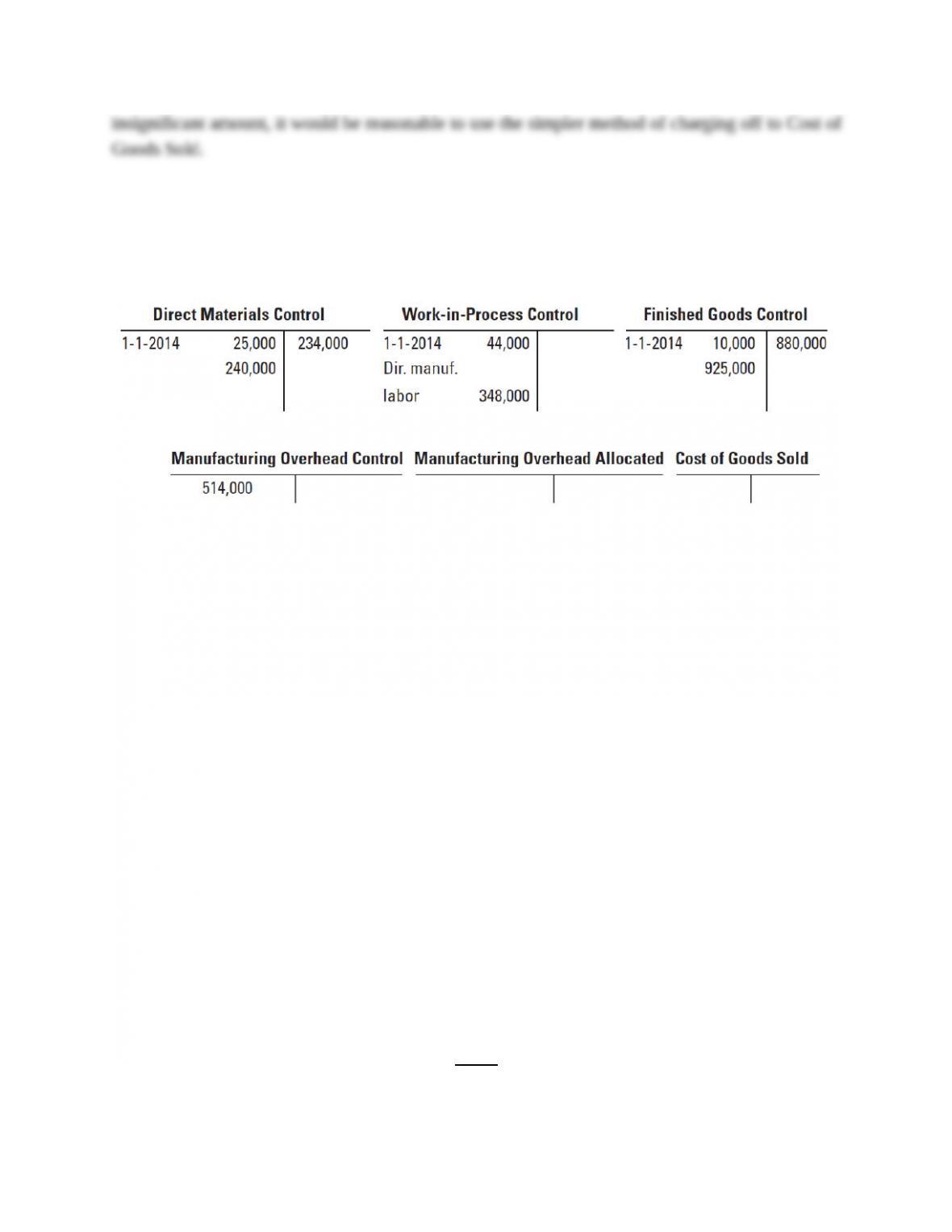

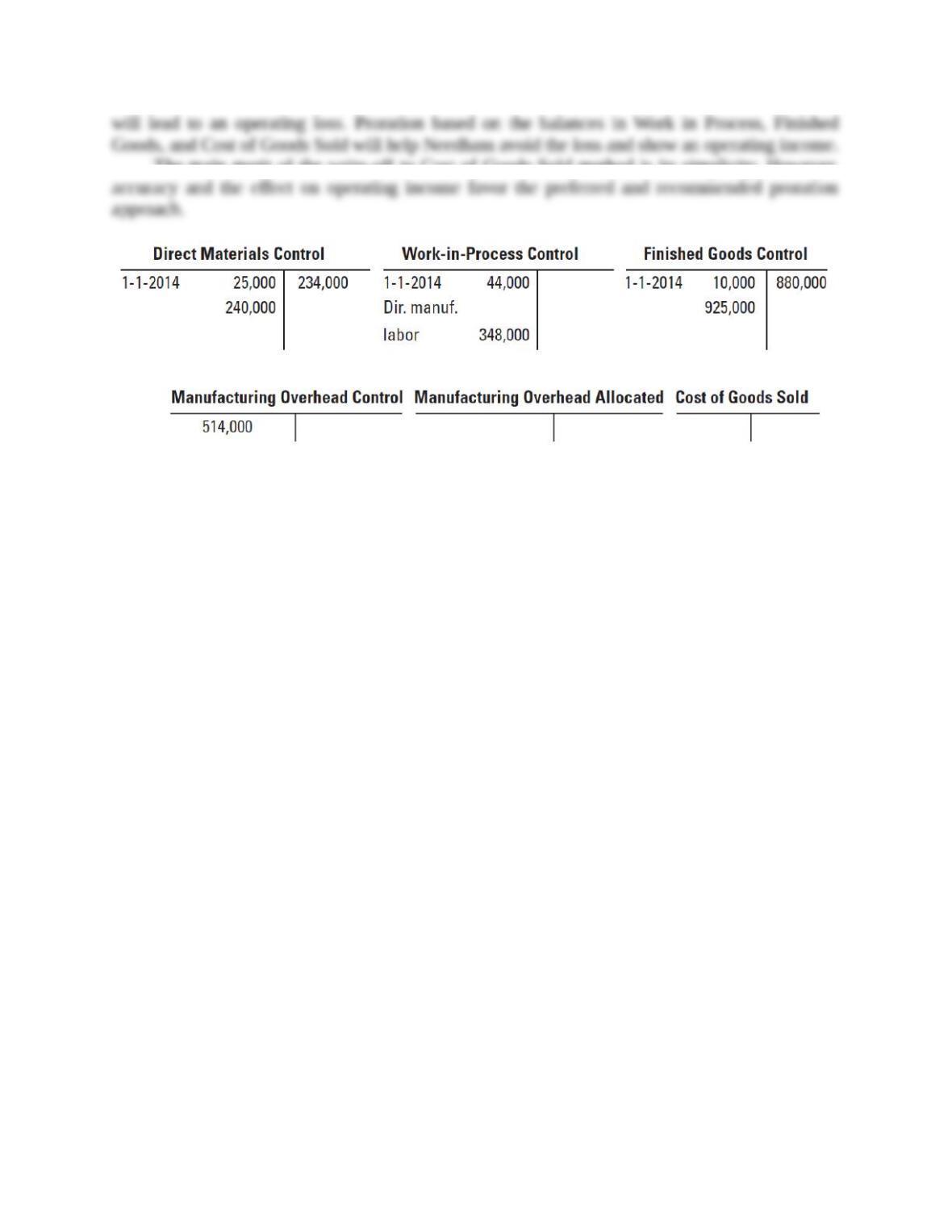

The solution assumes all materials used are direct materials. A summary of the T-accounts for

Southwick Company before adjusting for under- or overallocation of overhead follows:

Work in process inventory

on

12/31/2014

Direct Materials Control Work-in-Process Control

1-1-2014 25,000

Purchases 240,000

Material used for

manufacturing 234,000

1-1-2014 44,000

Direct materials 234,000

Transferred to

finished goods 925,000

Finished Goods Control Cost of Goods Sold

1-1-2014 10,000

Manufacturing Overhead Control Manufacturing Overhead Allocated

Manufacturing

overhead

costs 514,000

Manufacturing

overhead

allocated to

work in

process 464,000

1. From Direct Materials Control T-account,

2. Direct manufacturing labor-hours =

Direct manufacturing labor costs

Direct manufacturing wage rate per hour

=

Manufacturing overhead

allocated

=

Direct manufacturing

labor hours

Manufacturing

overhead rate

3. From the debit entry to Finished Goods T-account,

4. From Work-in-Process T-account,

5. From the credit entry to Finished Goods Control T-account, Cost of goods sold (before

6.

Manufacturing overhead

underallocated

=

Debits to Manufacturing

Overhead Control

–

Credit to Manufacturing

Overhead Allocated

7. a. Write-off to Cost of Goods Sold will increase (debit) Cost of Goods Sold by $50,000.

Hence, Cost of Goods Sold = $880,000 + $50,000 = $930,000.

b. Proration based on ending balances (before proration) in Work in Process, Finished

Goods, and Cost of Goods Sold.

Account balances in each account after proration follows:

Account

(1)

Account Balance

(Before Proration)

(2)

Proration of $50,000

Underallocated

Manufacturing Overhead

(3)

Account Balance

(After Proration)

(4) = (2) + (3)

Work in Process $ 165,000

(15%)

0.15 $50,000 = $ 7,500 $ 172,500

8. Needham’s operating income using write-off to Cost of Goods Sold and Proration based on

ending balances (before proration) follows:

Write-off to Proration Based

Cost of Goods Sold on Ending Balances

Revenues $1,050,000 $1,050,000

Cost of goods sold 930 ,000 920 ,000

9. If the purpose is to report the most accurate inventory and cost of goods sold figures, the

preferred method is to prorate based on the manufacturing overhead allocated component in the

inventory and cost of goods sold accounts. Proration based on the balances in Work in Process,

Another consideration in Needham’s decision about how to dispose of underallocated

manufacturing overhead is the effects on operating income. The write-off to Cost of Goods Sold

The main merit of the write-off to Cost of Goods Sold method is its simplicity. However,